Daiichi Sankyo and Merck report phase 2 trial results for lung cancer drug

Freeport-McMoRan Inc. (NYSE:FCX) reported strong second-quarter 2025 results on July 23, exceeding guidance across key metrics while benefiting from favorable copper and gold pricing. The company’s shares rose 1.75% in premarket trading to $46.60, building on yesterday’s close of $45.80.

Quarterly Performance Highlights

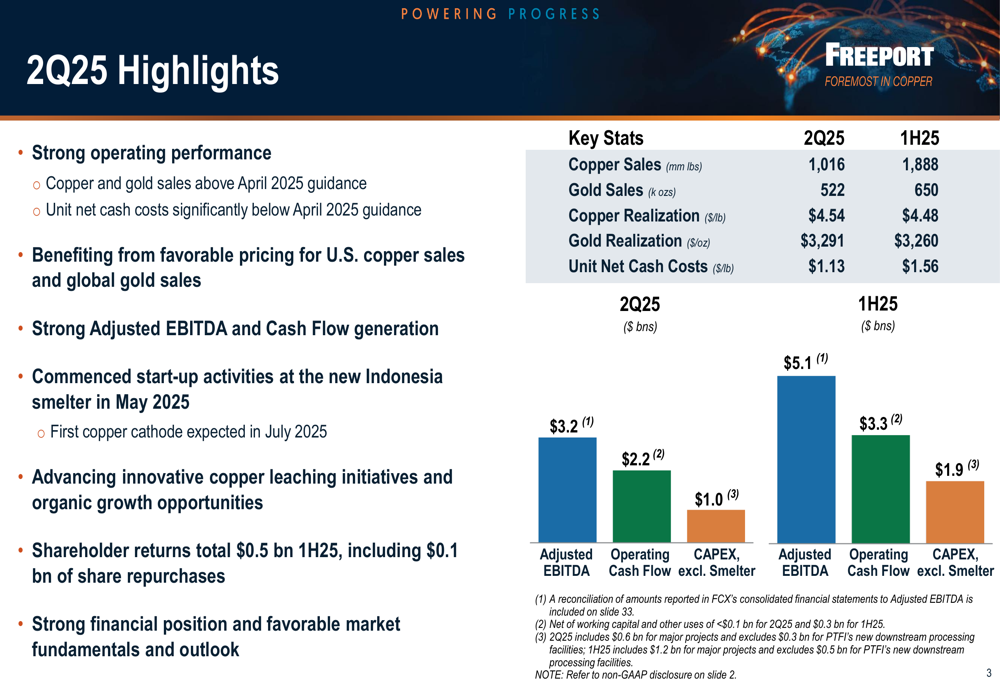

FCX delivered robust operational performance in Q2 2025, with copper and gold sales surpassing April 2025 guidance. The company reported copper sales of 1,016 million pounds and gold sales of 522,000 ounces, while achieving unit net cash costs of $1.13 per pound, significantly below guidance.

The strong performance translated into impressive financial results, with Q2 2025 adjusted EBITDA reaching $3.2 billion and operating cash flow (excluding smelter) of $2.2 billion. Net income attributable to common stock increased to $0.8 billion in Q2 2025, compared to $0.6 billion in the same period last year.

As shown in the following quarterly highlights chart, FCX benefited from favorable pricing for U.S. copper sales and global gold sales, with copper realization of $4.54 per pound and gold realization of $3,291 per ounce:

This performance represents a significant improvement from Q1 2025, when the company reported EBITDA of $1.9 billion and earnings per share of $0.24 on revenue of $5.73 billion.

U.S. Copper Market Position

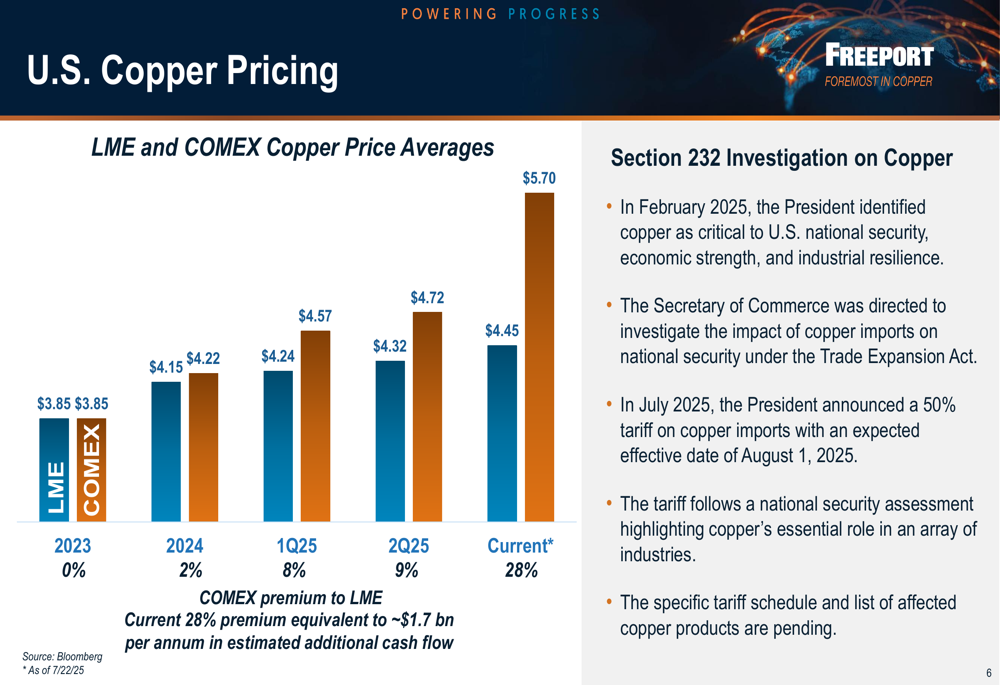

Freeport-McMoRan is strategically positioned as "America’s Copper Champion" with approximately one-third of its copper production coming from U.S. operations. This positioning has become increasingly valuable following the Section 232 Investigation, which identified copper as critical to U.S. national security and resulted in a 50% tariff on copper imports effective August 1, 2025.

The company has observed a growing premium for COMEX copper prices relative to the London Metal Exchange (LME) benchmark. This premium has expanded from 0% in 2023 to 28% currently, providing a significant advantage for FCX’s U.S. operations.

The following chart illustrates the widening gap between COMEX and LME copper prices, highlighting the potential benefit to FCX’s U.S. production:

Freeport’s U.S. franchise includes fully integrated operations in the Southwest, with upstream copper mines featuring SX/EW facilities and downstream smelting and refining capabilities. The company employs over 39,000 workers in the U.S. and controls 43% of its reserves and 46% of its copper resources within the United States.

Operational Performance by Region

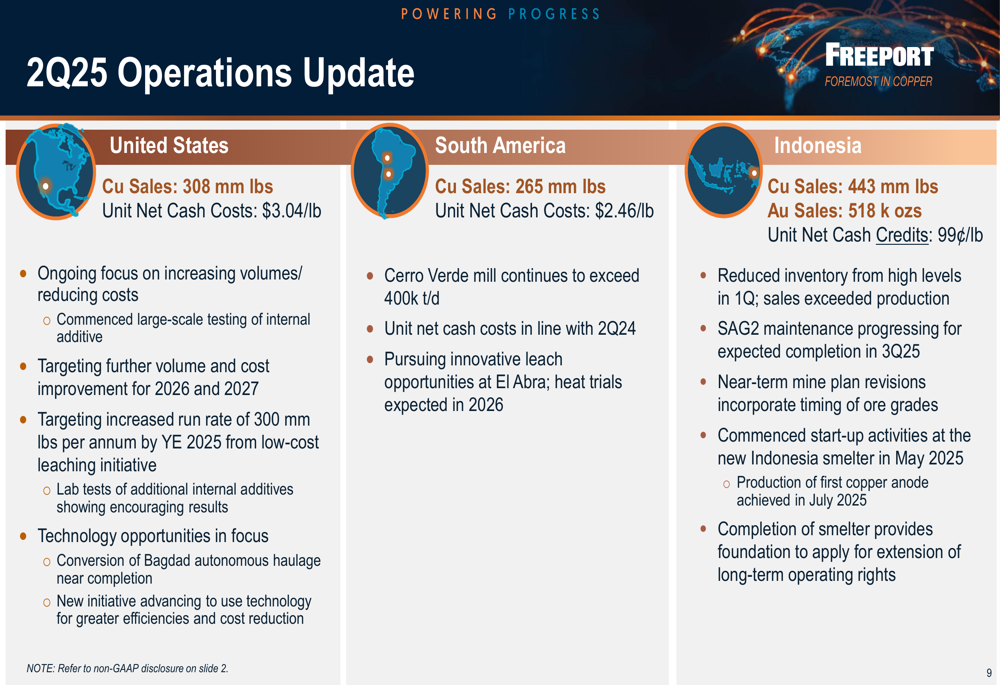

FCX’s operations delivered strong results across all three of its primary regions. In the United States, the company reported copper sales of 308 million pounds with unit net cash costs of $3.04 per pound. South American operations contributed 265 million pounds of copper at unit net cash costs of $2.46 per pound, while Indonesian operations delivered 443 million pounds of copper and 518,000 ounces of gold, achieving unit net cash credits of $0.99 per pound.

The following regional breakdown provides a comprehensive view of FCX’s Q2 2025 operational performance:

A notable development in Indonesia was the commencement of start-up activities at the new smelter in May 2025, with production of the first copper anode achieved in July 2025. This milestone advances FCX’s objective of becoming a fully integrated producer in Indonesia.

Strategic Growth Initiatives

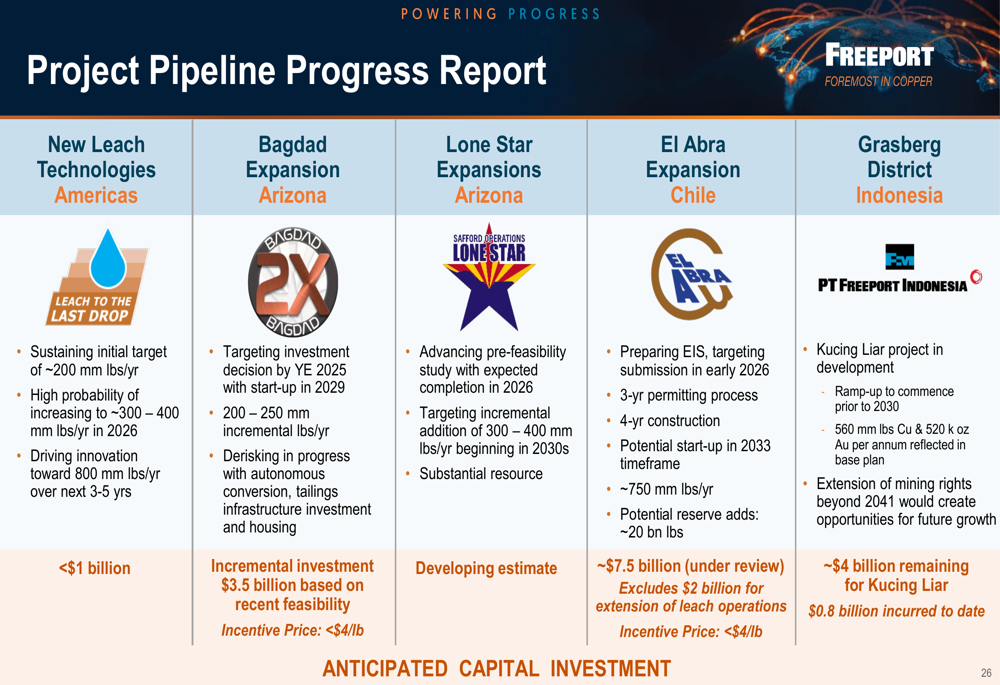

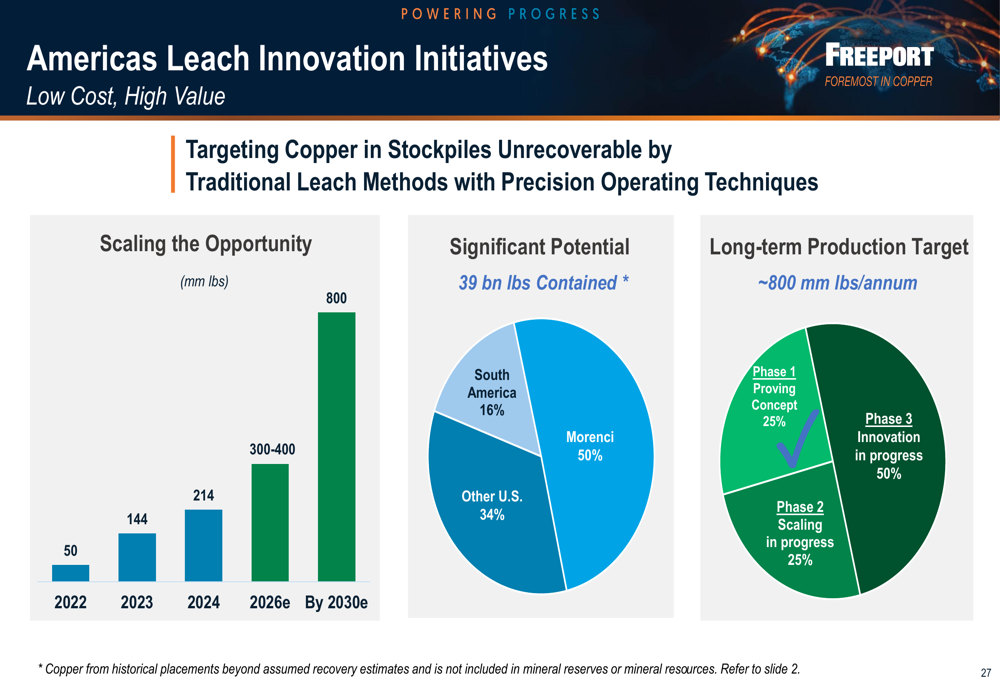

Freeport-McMoRan is advancing several key growth initiatives to enhance long-term production capacity and operational efficiency. The company’s innovative leaching technologies target approximately 800 million pounds of annual copper production from previously unrecoverable resources, with a goal of reaching a run rate of 300 million pounds per annum by year-end 2025.

The company’s project pipeline encompasses multiple growth opportunities across its global operations, as illustrated in the following progress report:

The Americas leaching innovation initiatives represent a particularly promising opportunity, targeting copper in stockpiles that was previously unrecoverable through traditional leaching methods. These initiatives leverage precision operating techniques to extract value from approximately 39 billion pounds of contained copper.

As shown in the following chart, the leaching initiatives are being scaled up with significant potential across FCX’s operations:

Other key projects include the Bagdad 2X expansion in Arizona, which could potentially double concentrator capacity, and the implementation of autonomous haulage systems to improve efficiency and reduce emissions. In Indonesia, the company is evaluating a combined cycle gas turbine power plant at Grasberg to replace the existing coal plant, which would significantly reduce greenhouse gas emissions.

Financial Outlook and Shareholder Returns

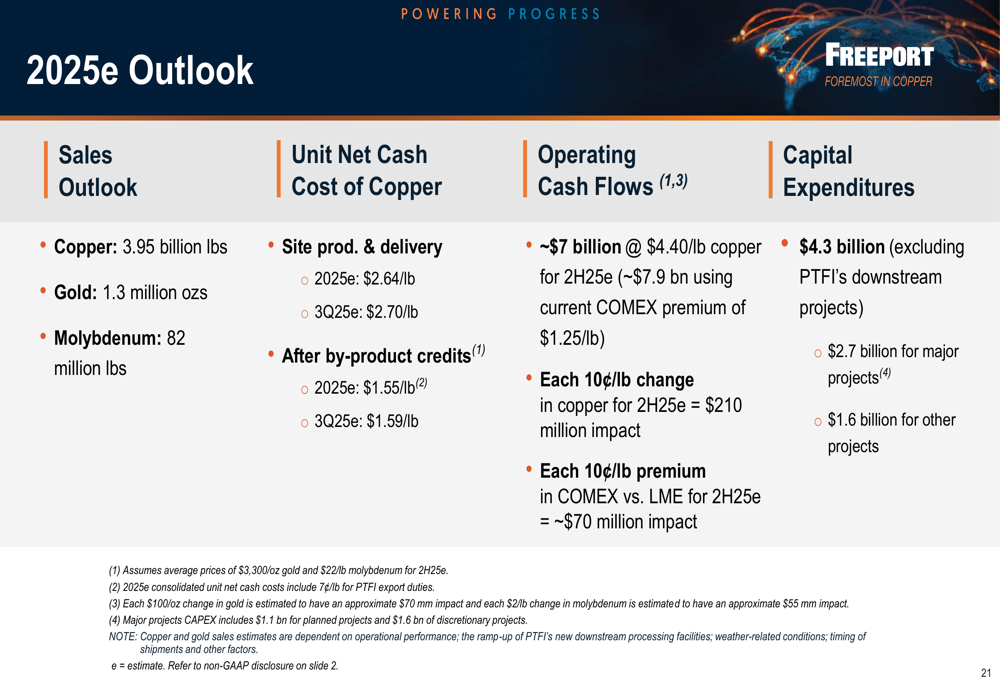

FCX provided a comprehensive outlook for 2025, projecting copper sales of 3.95 billion pounds, gold sales of 1.3 million ounces, and molybdenum sales of 82 million pounds. The company expects unit net cash costs of copper to average $1.55 per pound for the full year 2025.

The following chart details FCX’s 2025 outlook, including production targets and financial projections:

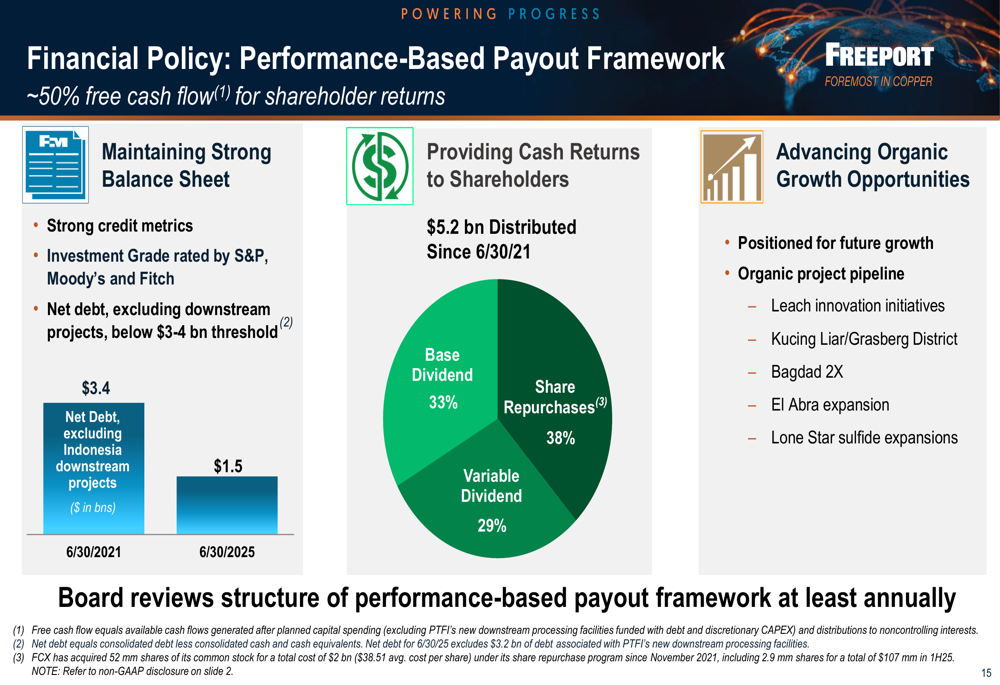

The company maintains a strong balance sheet with consolidated cash and cash equivalents of $4.5 billion and a net debt to adjusted EBITDA ratio of 0.5x. This financial strength supports FCX’s performance-based payout framework, which allocates approximately 50% of free cash flow to shareholder returns.

Since June 30, 2021, FCX has distributed $5.2 billion to shareholders, with 33% allocated to base dividends, 38% to share repurchases, and 29% to variable dividends. In the first half of 2025, shareholder returns totaled $0.5 billion, including $0.1 billion in share repurchases.

The following chart illustrates FCX’s financial policy and shareholder return framework:

Long-Term Market Fundamentals

Freeport-McMoRan emphasized the favorable long-term fundamentals for copper, highlighting its critical role in electrification and decarbonization. Over 65% of the world’s copper is used in applications that deliver electricity, positioning the metal as essential for future infrastructure, technology advancement, decarbonization efforts, and transportation electrification.

Despite economic and trade uncertainties, demand drivers for copper remain positive, supported by electrification, AI infrastructure buildout, and power grid expansion. Global exchange inventories remain low, and there is an absence of material near-term supply growth, creating a favorable environment for copper producers.

The company’s sensitivity analysis indicates that for each $0.10 per pound change in copper prices, EBITDA would be impacted by approximately $425 million based on average 2026-2027 projections. Similarly, each $0.10 per pound premium in COMEX prices relative to LME would contribute an additional $135 million to EBITDA.

FCX’s strategic positioning as a leading global copper producer with significant U.S. operations, combined with its advancing growth initiatives and strong financial position, provides a solid foundation for capturing value from favorable copper market fundamentals in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.