Five things to watch in markets in the week ahead

Frontdoor Inc (NASDAQ:FTDR) reported strong first-quarter 2025 results on May 1, with double-digit revenue growth and significant margin expansion, prompting the company to raise its full-year guidance. The home service plan provider’s shares jumped 9.9% in premarket trading following the announcement.

Quarterly Performance Highlights

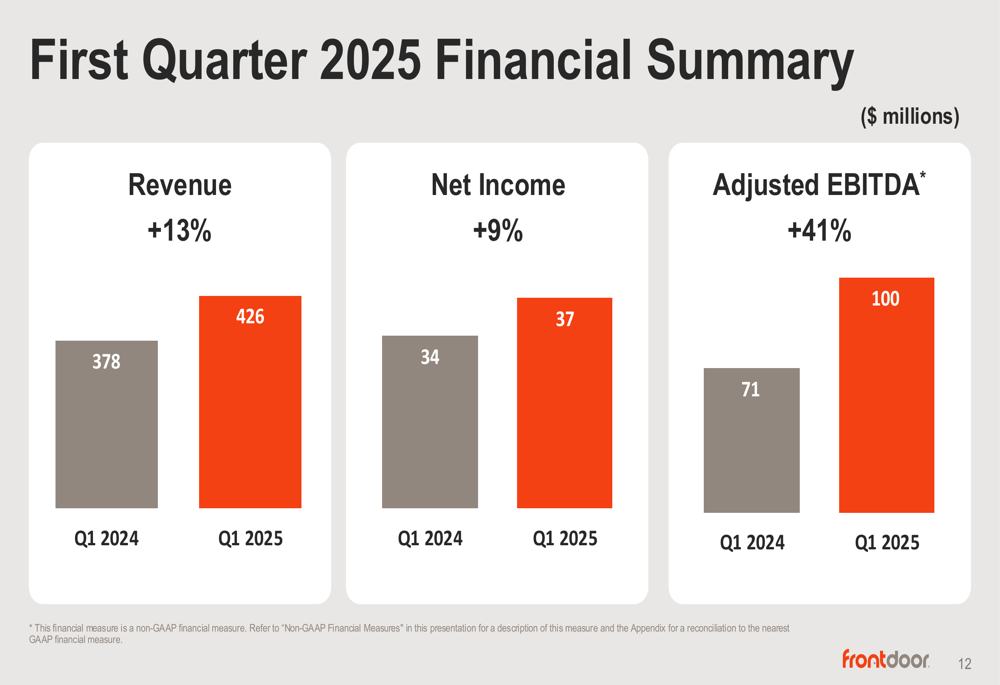

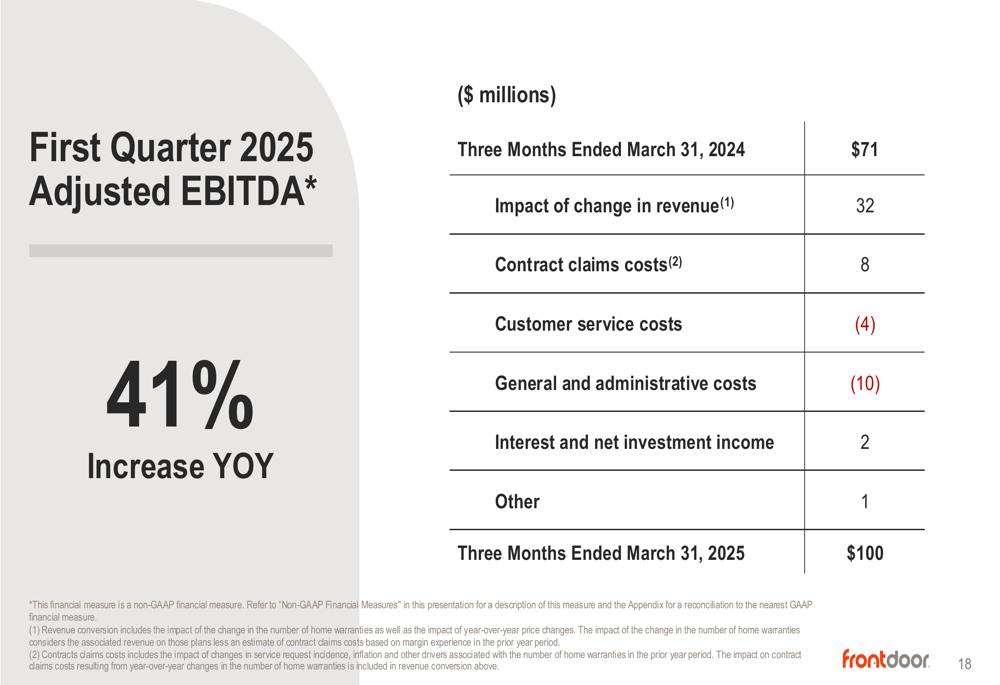

Frontdoor delivered robust financial results for the first quarter of 2025, with revenue increasing 13% year-over-year to $426 million. Net income grew 9% to $37 million, while adjusted EBITDA surged 41% to $100 million compared to the same period last year.

As shown in the following financial summary, the company demonstrated strong growth across key metrics:

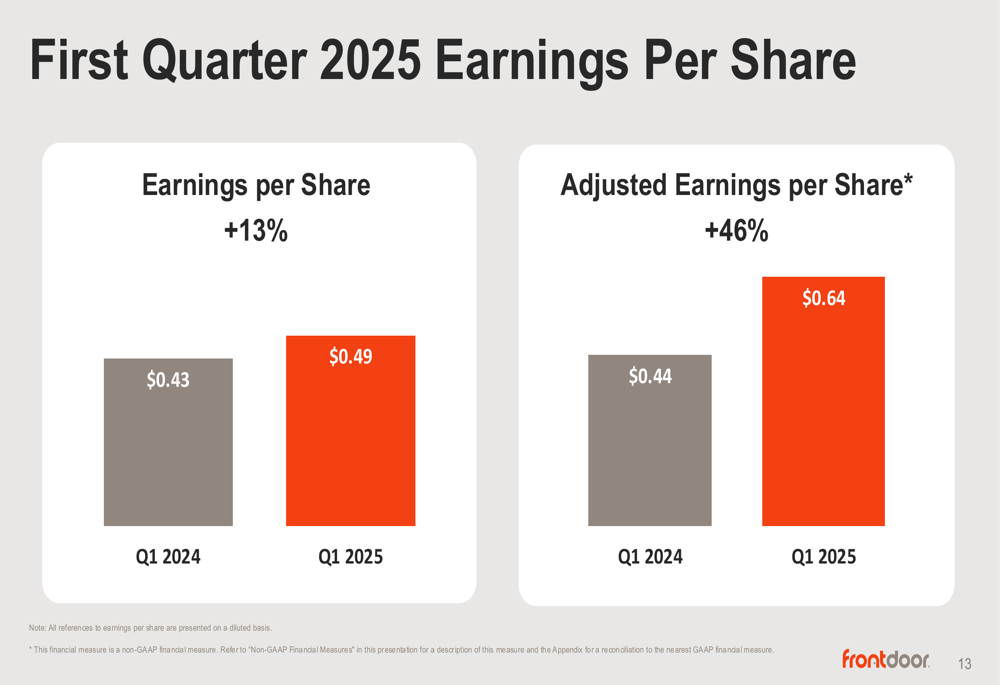

Earnings per share rose 13% to $0.49, while adjusted earnings per share jumped 46% to $0.64, reflecting the company’s operational efficiency and effective cost management.

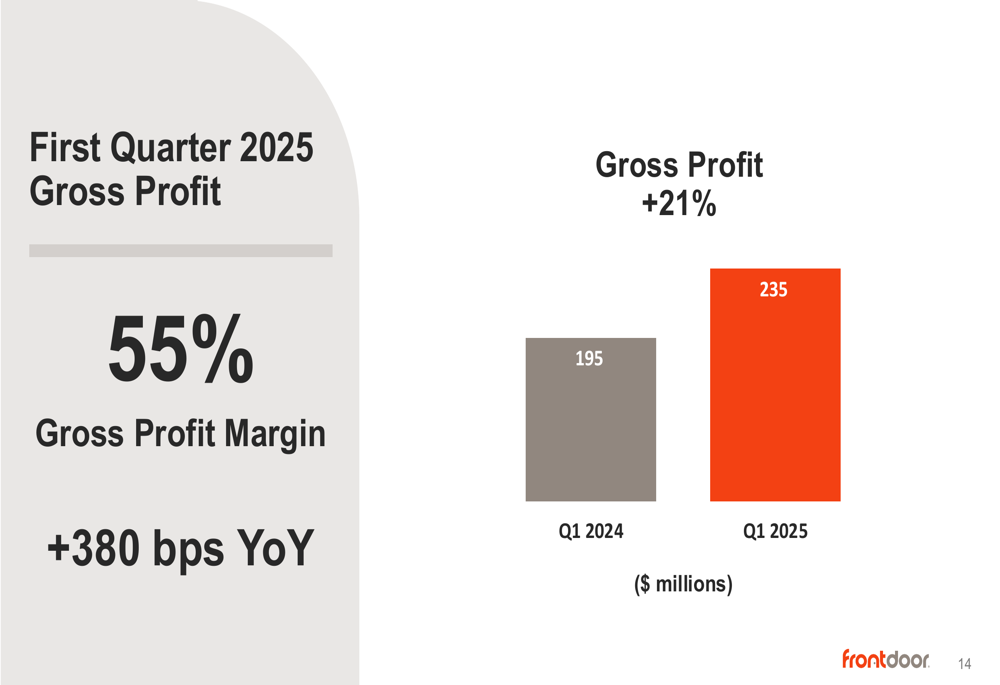

Gross profit increased 21% to $235 million, with gross profit margin expanding 380 basis points year-over-year to 55%, highlighting Frontdoor’s ability to manage costs while growing revenue.

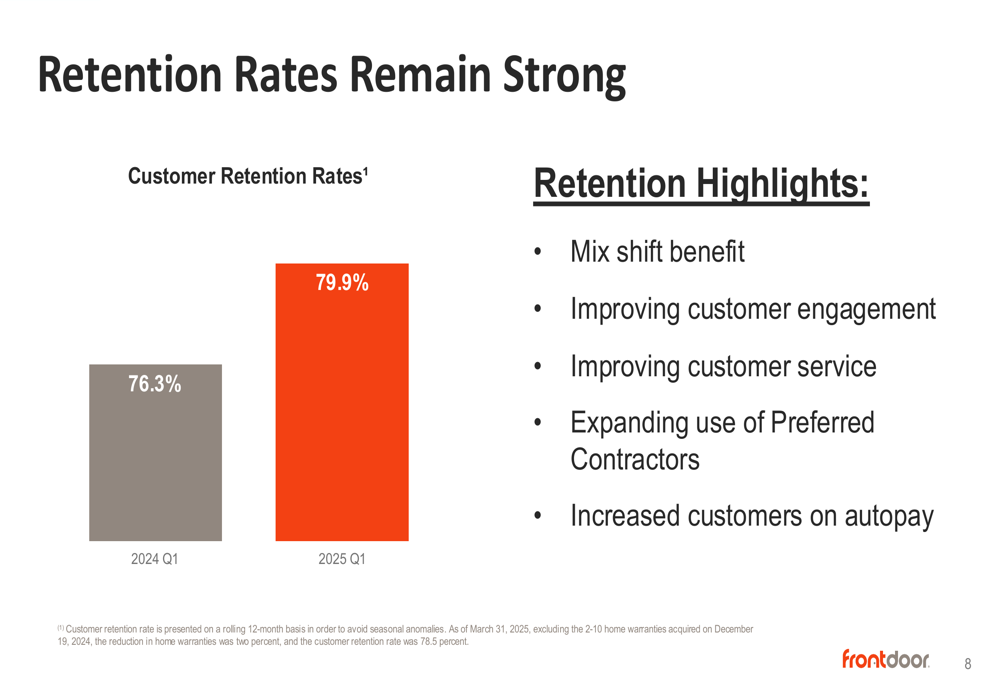

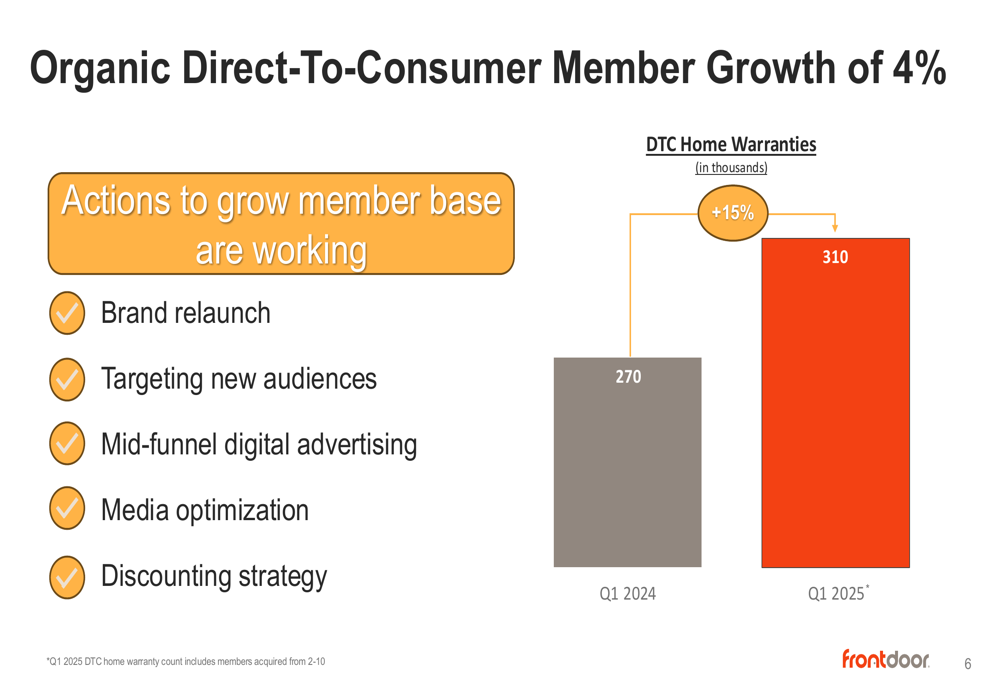

The company’s member count increased 7% to 2.1 million, with organic direct-to-consumer member growth of 4%. Customer retention rates improved significantly, rising from 76.3% in Q1 2024 to 79.9% in Q1 2025, demonstrating the effectiveness of Frontdoor’s customer engagement initiatives.

Strategic Initiatives

Frontdoor continues to execute on its three strategic priorities: growing and retaining warranty members, scaling non-warranty revenue, and optimizing the integration of 2-10 Home Buyers Warranty.

The company’s direct-to-consumer channel showed strong performance with 15% growth in home warranties, driven by brand relaunch efforts, targeted digital advertising, and optimized discounting strategies.

Despite a challenging real estate market, with existing home sales continuing near 30-year lows, Frontdoor has managed to drive growth through its direct-to-consumer channel and improved customer retention.

The company is leveraging digital innovation to enhance customer experience, with its American Home Shield app reaching approximately 200,000 downloads since its late October launch. Additionally, the Video Chat With An Expert feature has been well-received, with about 17% of video chats resolving issues without requiring a service call, saving both time and money.

Frontdoor is also expanding its non-warranty revenue streams, raising its 2025 new HVAC sales target to approximately $105 million due to positive demand trends and increasing contractor participation. The company has expanded its Moen partnership to 21 states and expects its New Home Structural Warranty to generate approximately $44 million in 2025.

Detailed Financial Analysis

Frontdoor’s adjusted EBITDA growth of 41% to $100 million was driven by multiple factors, including increased revenue, improved contract claims costs, and higher interest and net investment income, partially offset by higher customer service and general administrative costs.

The following chart breaks down the components contributing to the adjusted EBITDA improvement:

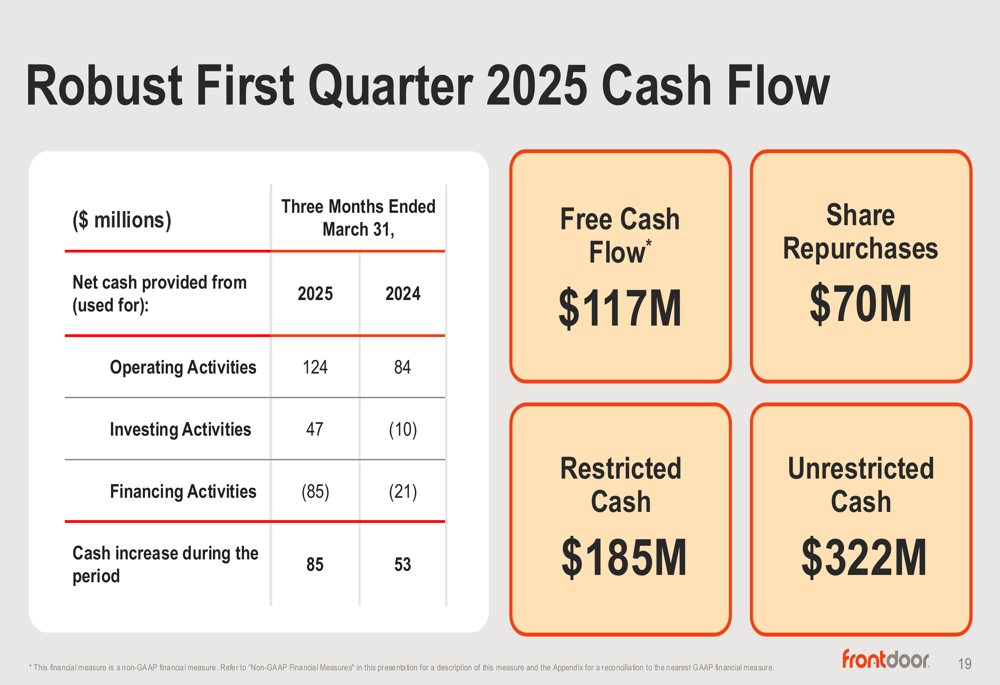

The company generated robust cash flow in the first quarter, with free cash flow of $117 million. Frontdoor maintained a strong financial position with $322 million in unrestricted cash and $185 million in restricted cash.

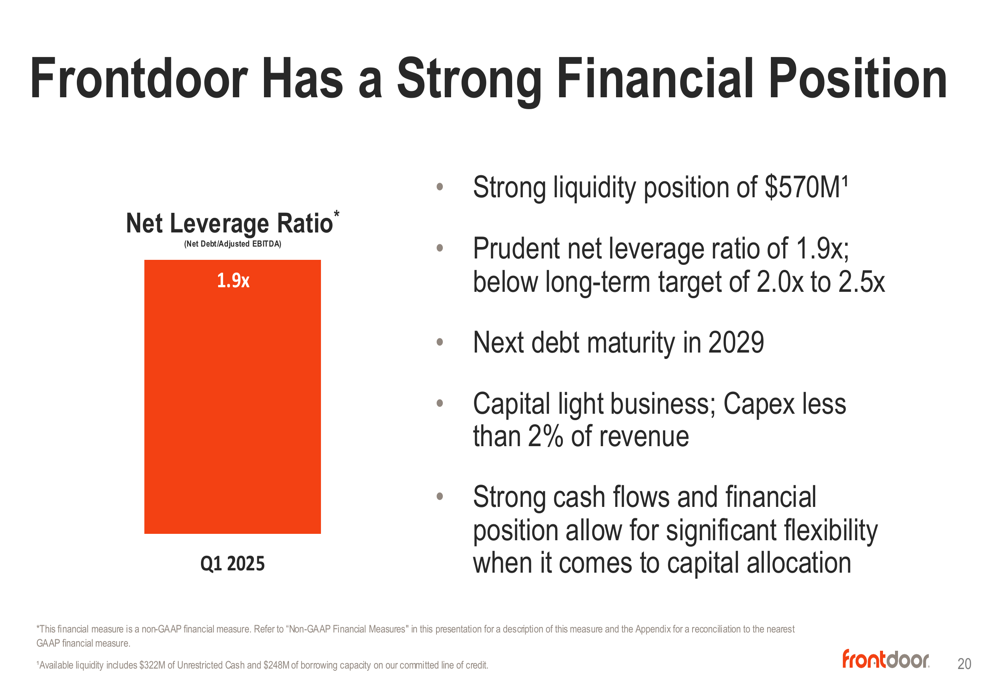

Frontdoor’s prudent financial management is reflected in its net leverage ratio of 1.9x, below its long-term target of 2.0x to 2.5x. The company’s next debt maturity is not until 2029, providing significant financial flexibility.

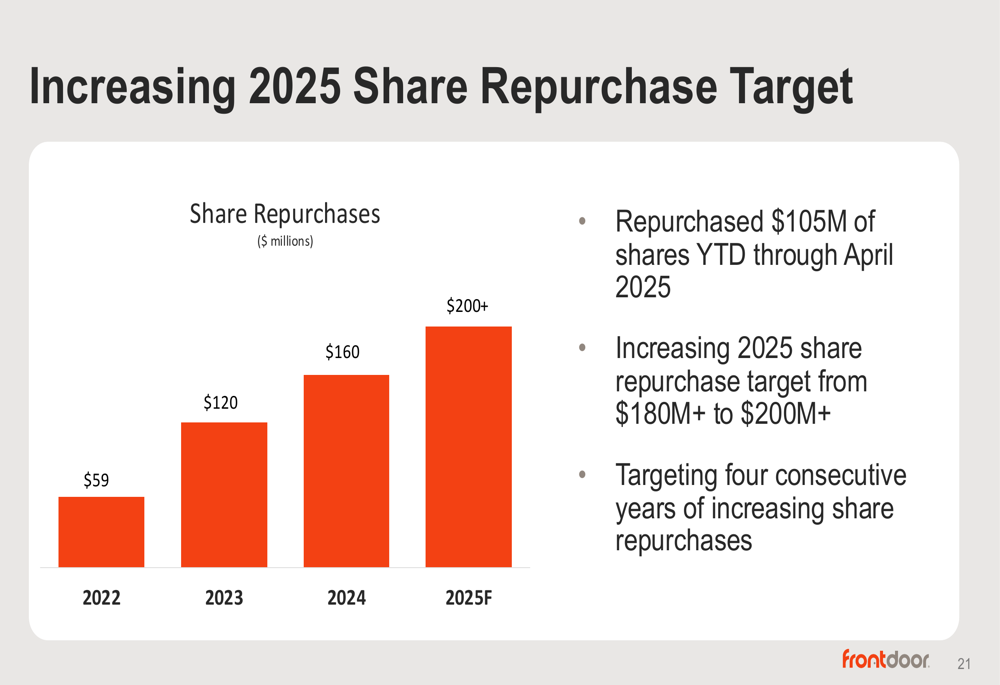

The company has increased its 2025 share repurchase target from $180+ million to $200+ million, having already repurchased $70 million of shares in Q1 and $105 million year-to-date through April 2025. This marks the fourth consecutive year of increasing share repurchases.

Forward-Looking Statements

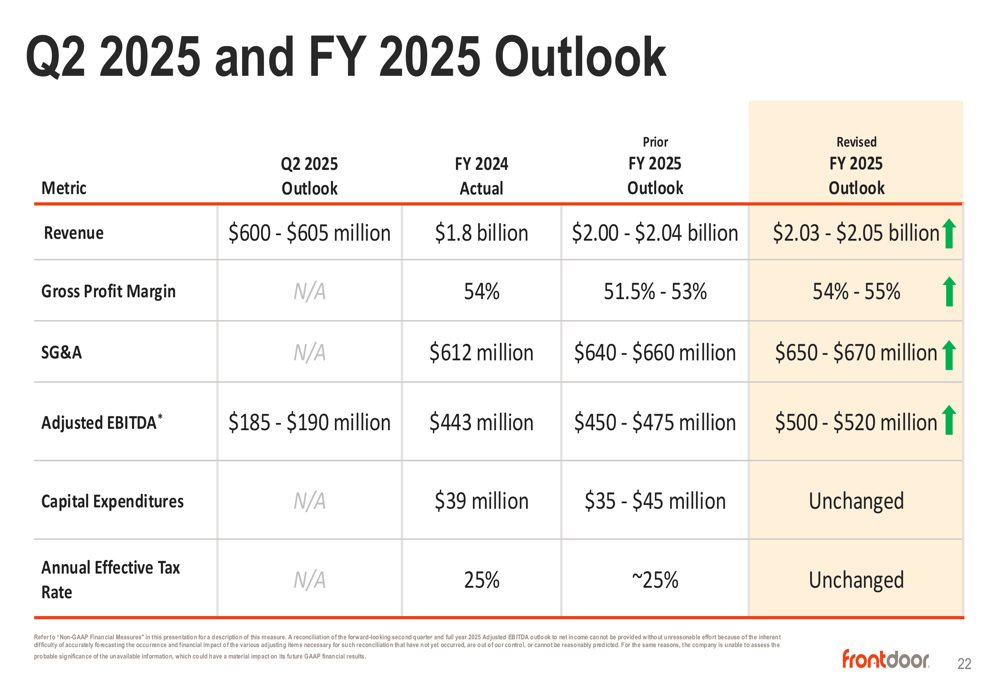

Based on its strong Q1 performance, Frontdoor has raised its full-year 2025 guidance. The company now expects revenue between $2.03 billion and $2.05 billion, up from its previous guidance of $2.00 billion to $2.04 billion. Gross profit margin is projected to be between 54% and 55%, an increase from the prior outlook of 51.5% to 53%.

Adjusted EBITDA guidance has been significantly raised to $500-$520 million from the previous $450-$475 million. For the second quarter of 2025, Frontdoor anticipates revenue of $600-$605 million and adjusted EBITDA of $185-$190 million.

Frontdoor’s management emphasized that the company is delivering outstanding results while raising guidance and positioning itself for future growth. Despite operating near its lowest valuation ever, the company continues to demonstrate strong operational performance and financial discipline.

The company’s ability to grow revenue and expand margins in a challenging real estate market underscores the resilience of its business model and the effectiveness of its strategic initiatives. With its strong cash position, disciplined capital allocation, and focus on both warranty and non-warranty revenue streams, Frontdoor appears well-positioned to continue its growth trajectory through 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.