Microsoft sued by Australia competition regulator over Copilot, 365 pricing

Introduction & Market Context

FTI Consulting, Inc. (NYSE:FCN) reported its third quarter 2025 financial results on October 23, showing substantial profit growth despite modest revenue increases. The company’s shares responded positively, rising 1.37% in regular trading after a 0.74% gain in pre-market activity following the earnings release.

The consulting firm’s performance demonstrated resilience in a challenging economic environment, with its diversified business model allowing strong results in restructuring and forensic services to offset weakness in other segments. This quarter’s results continue to reflect FTI’s strategic positioning as a leader in specialized consulting services.

Quarterly Performance Highlights

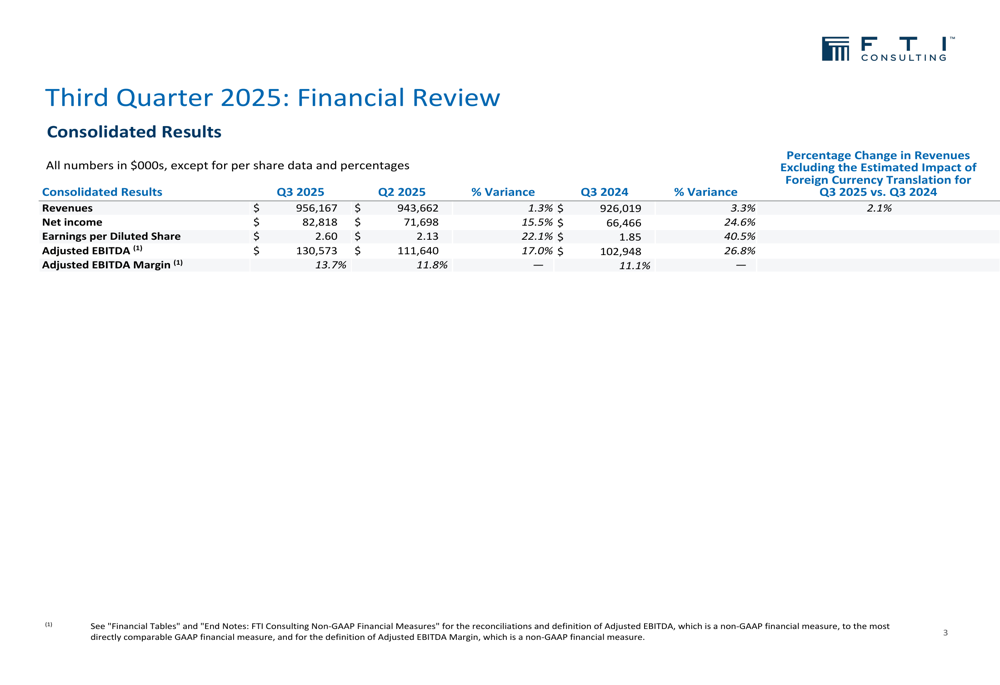

FTI Consulting reported Q3 2025 revenues of $956.2 million, representing a 3.3% increase year-over-year and a 1.3% increase from the previous quarter. More impressively, the company achieved substantial bottom-line growth with net income of $82.8 million, up 24.6% from Q3 2024 and 15.5% from Q2 2025.

Earnings per diluted share reached $2.60, marking a 40.5% increase year-over-year and significantly exceeding analyst expectations. According to the earnings report, this represented a 30.65% beat compared to the forecasted $1.99 EPS.

As shown in the following consolidated financial results:

Adjusted EBITDA showed similar strength, rising to $130.6 million, a 26.8% increase from the prior year. The adjusted EBITDA margin expanded to 13.7%, up from 11.1% in Q3 2024 and 11.8% in Q2 2025, reflecting improved operational efficiency and a favorable service mix.

Segment Performance Analysis

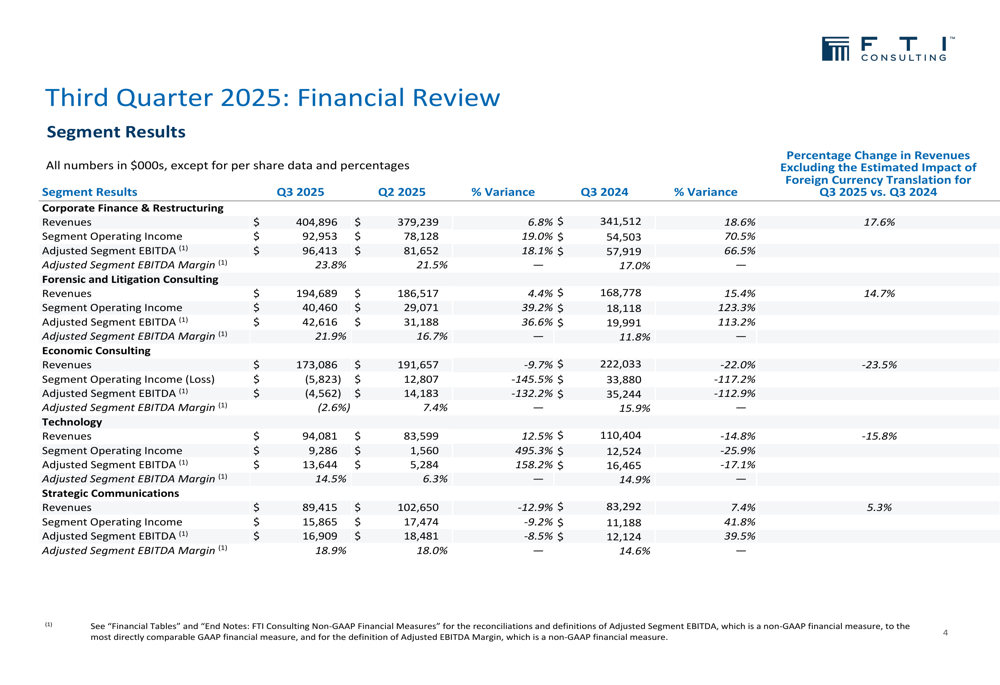

FTI Consulting’s performance varied significantly across its five business segments, with Corporate Finance & Restructuring and Forensic and Litigation Consulting delivering exceptional results while Economic Consulting faced substantial challenges.

The Corporate Finance & Restructuring segment was the standout performer, with revenues increasing 18.6% year-over-year to $404.9 million. More impressively, the segment’s operating income surged 70.5% to $93.0 million, while its adjusted EBITDA margin expanded to 23.8% from 17.0% in the prior year.

Similarly, the Forensic and Litigation Consulting segment showed strong growth, with revenues up 15.4% to $194.7 million and segment operating income more than doubling to $40.5 million. This segment’s adjusted EBITDA margin improved dramatically to 21.9% from 11.8% in Q3 2024.

In contrast, the Economic Consulting segment experienced a significant decline, with revenues falling 22.0% year-over-year to $173.1 million and swinging from an operating profit of $33.9 million in Q3 2024 to an operating loss of $5.8 million. The segment’s adjusted EBITDA margin deteriorated to -2.6% from 15.9% a year earlier.

The detailed segment performance is illustrated below:

The Technology segment also faced headwinds with revenues declining 14.8% year-over-year to $94.1 million, though it showed sequential improvement with a 12.5% increase from Q2 2025. The Strategic Communications segment delivered modest growth of 7.4% year-over-year to $89.4 million, with improved profitability.

These mixed results align with CEO Steven H. Gunby’s comment from the earnings call that the company is "closer to the beginning of this journey than the end," suggesting ongoing transformation across business segments.

Financial Position and Capital Allocation

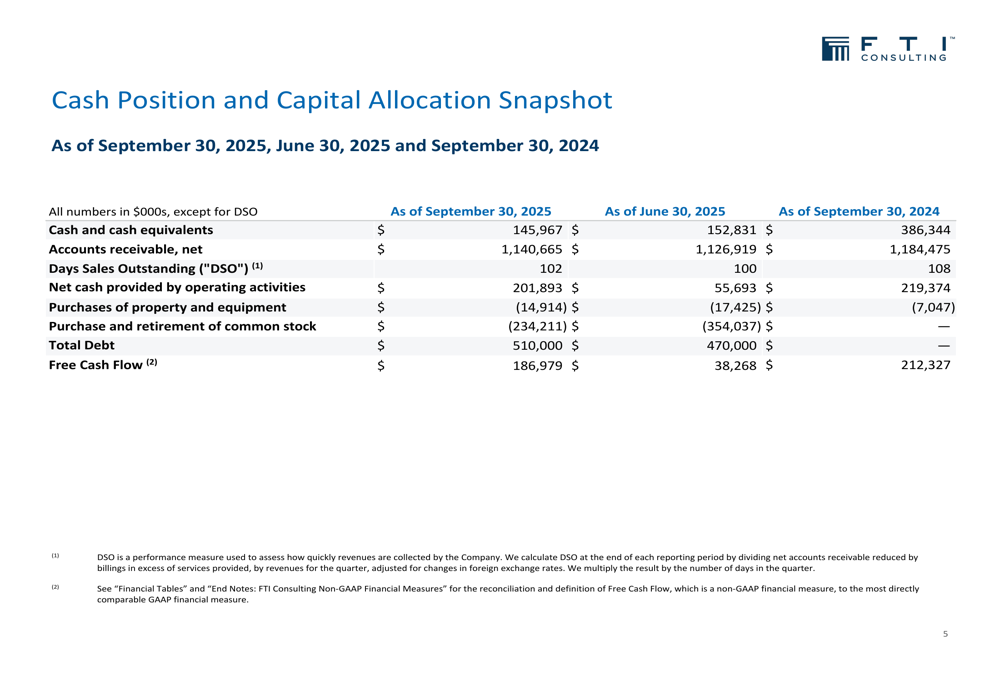

FTI Consulting’s balance sheet and capital allocation strategy showed significant changes compared to the prior year. Cash and cash equivalents stood at $146.0 million as of September 30, 2025, down substantially from $386.3 million a year earlier. This reduction reflects the company’s active share repurchase program, with $234.2 million spent on buying back shares year-to-date.

The company also took on $510 million in debt, a notable shift from having no debt a year earlier. Despite these changes, FTI maintained strong cash flow generation with $201.9 million in net cash provided by operating activities during the quarter and free cash flow of $187.0 million.

The following chart illustrates the company’s cash position and capital allocation:

Accounts receivable management showed improvement, with days sales outstanding (DSO) decreasing to 102 days from 108 days in the prior year, indicating enhanced collection efficiency.

Geographic Performance

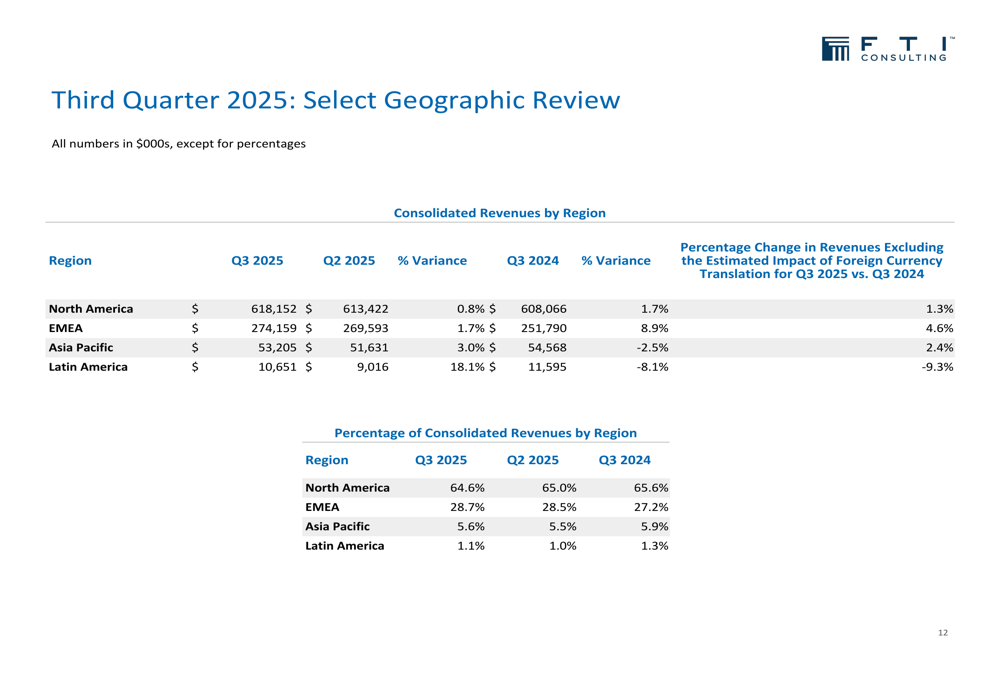

FTI Consulting’s geographic performance revealed strength in EMEA (Europe, Middle East, and Africa) and stability in North America, while Asia Pacific and Latin America experienced declines.

North America, which accounted for 64.6% of consolidated revenues in Q3 2025, showed modest growth of 1.7% year-over-year to $618.2 million. EMEA delivered more robust growth of 8.9% to $274.2 million, representing 28.7% of total revenues.

In contrast, Asia Pacific revenues declined 2.5% to $53.2 million, while Latin America saw a more significant drop of 8.1% to $10.7 million. When excluding the impact of foreign currency translation, the underlying performance was slightly better in Asia Pacific but worse in Latin America.

The geographic revenue breakdown is presented below:

This regional performance reflects varying economic conditions and demand for consulting services across markets, with particular strength in the European restructuring market.

Recognition and Market Position

During the quarter, FTI Consulting received several notable accolades that reinforce its market leadership position. These recognitions span various practice areas and highlight the company’s expertise and reputation in the consulting industry.

Key awards included Compass Lexecon being ranked as the Top Global Economic Consulting Firm on the Lexology Index Competition 2025 list, recognition as one of the Top 100 Internship Programs in the U.S., and winning the Global Turnaround Consulting Firm of the Year by Turnaround Atlas Awards. The company was also ranked #1 Financial Advisor in the Americas Restructuring Rankings for the first three quarters of 2025.

These accolades underscore FTI’s market leadership in key practice areas:

Forward Outlook

Based on its strong performance through the third quarter, FTI Consulting has raised its full-year EPS guidance to a range of $8.20-$8.70, reflecting confidence in continued growth. This upward revision suggests management’s optimism about the company’s prospects for the remainder of 2025.

The company faces both opportunities and challenges going forward. The strong performance in restructuring and forensic services is expected to continue, while management anticipates a gradual recovery in the Economic Consulting segment. However, potential risks include global transaction volume declines, antitrust market weakness (particularly in EMEA), and the typical seasonal business slowdown expected in Q4.

Interim CFO Paul Linton highlighted the company’s resilience during the earnings call, noting, "We have a set of businesses that are uniquely diverse and resilient." This diversity appears to be serving the company well as it navigates varying market conditions across segments and geographies.

As FTI Consulting continues to invest in AI tools and talent acquisition, the company appears well-positioned to maintain its competitive edge despite the mixed performance across business segments. Investors will be watching closely to see if the struggling Economic Consulting segment can return to growth and whether the strong momentum in restructuring services can be sustained.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.