Trump meets Zelenskiy, says Putin wants war to end, mulls trilateral talks

Introduction & Market Context

Galderma Group AG (SWX:GALD) reported strong first-quarter results on April 24, 2025, with sales growth exceeding expectations across all product categories and geographies. The Swiss dermatology company’s shares surged 11.66% following the announcement, reflecting investor confidence in its performance and outlook.

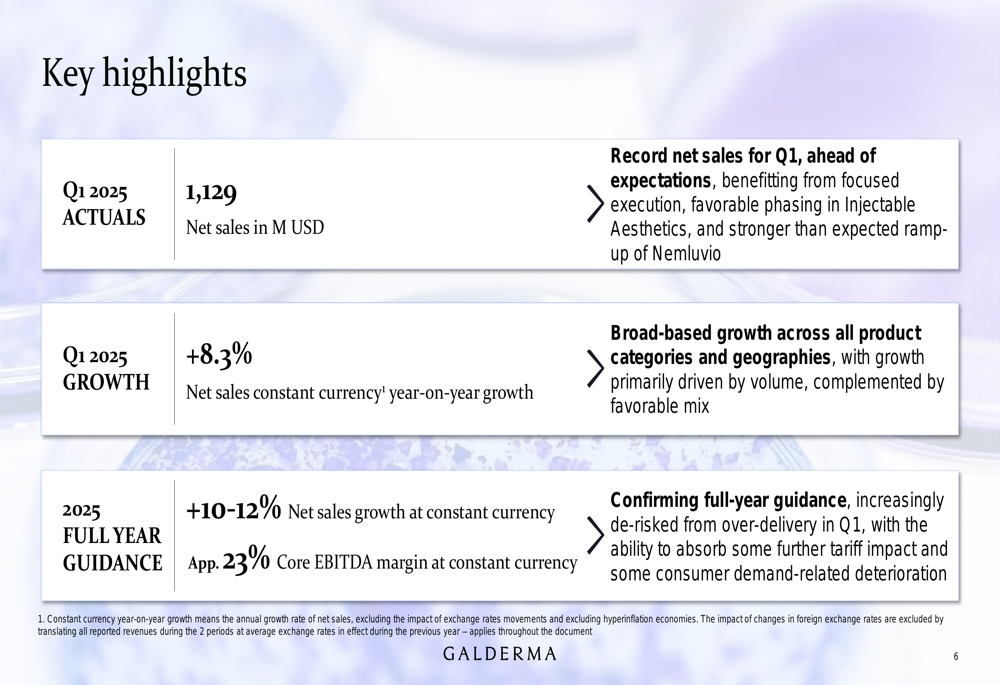

The company achieved record net sales of $1.129 billion in Q1, representing an 8.3% year-on-year increase at constant currency. This performance comes amid what the company described as a "volatile" U.S. market, highlighting Galderma’s resilience and the effectiveness of its diversified portfolio strategy.

Quarterly Performance Highlights

Galderma’s Q1 2025 results exceeded management expectations, driven primarily by strong execution, favorable phasing in Injectable Aesthetics, and a stronger-than-anticipated ramp-up of Nemluvio, the company’s new treatment for atopic dermatitis and prurigo nodularis.

As shown in the following key highlights from the presentation:

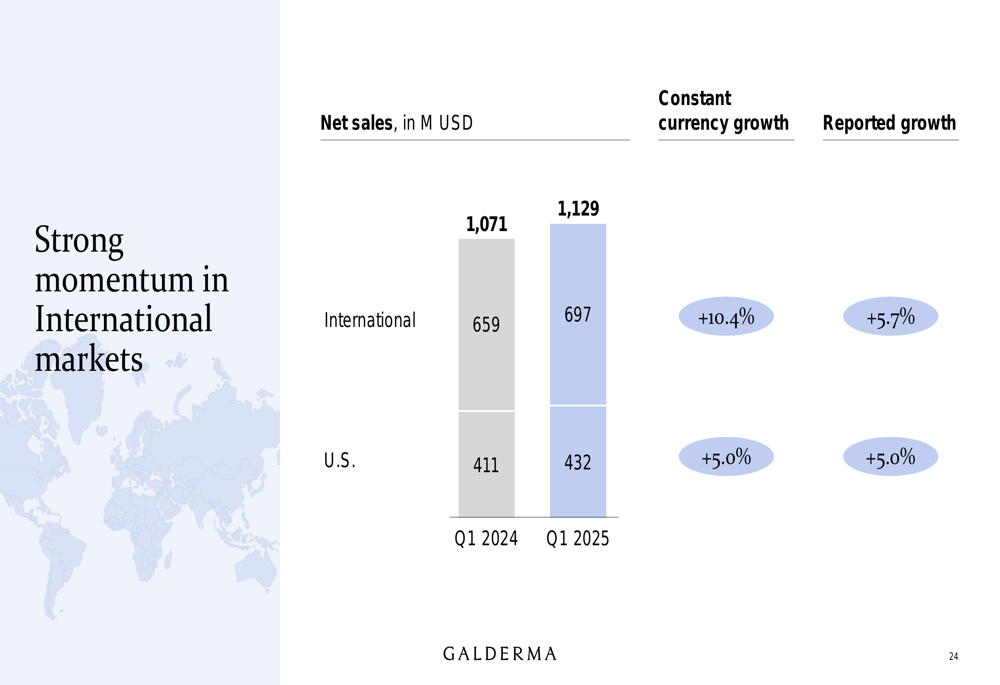

The company emphasized that volume was the primary growth driver across its portfolio. International markets delivered particularly strong performance with 10.4% growth, while U.S. sales increased by 5.0% despite market volatility.

Segment Performance Analysis

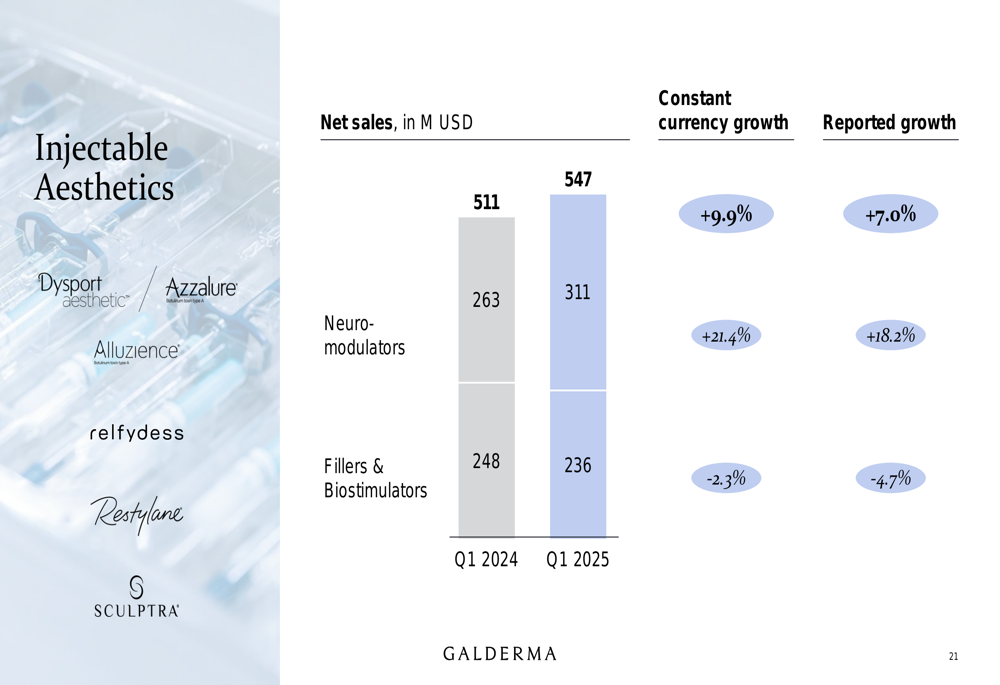

Galderma’s performance was broad-based across all three of its product categories, with particularly strong results in neuromodulators.

The following chart illustrates the company’s net sales growth by product category:

In the Injectable Aesthetics segment, which accounts for nearly half of Galderma’s revenue, sales grew 9.9% to $547 million. This growth was driven by exceptional performance in neuromodulators (Dysport, Azzalure, Alluzience, Relfydess), which saw a 21.4% increase, offsetting a 2.3% decline in fillers and biostimulators (Restylane, Sculptra).

The detailed breakdown of Injectable Aesthetics performance shows the strength of the neuromodulator portfolio:

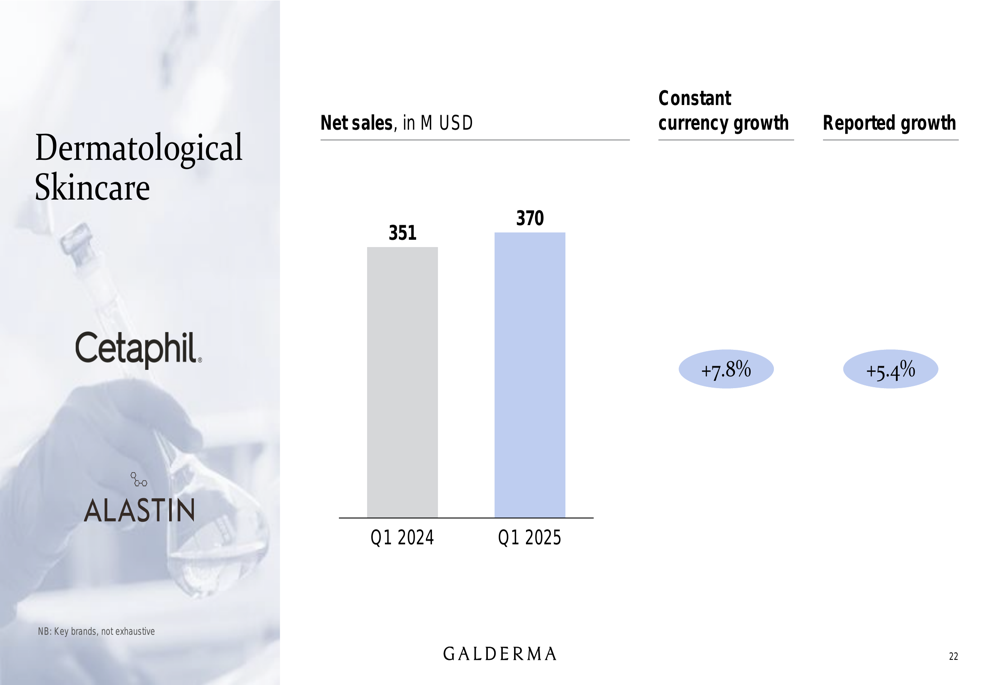

Dermatological Skincare, which includes brands like Cetaphil and Alastin, delivered 7.8% growth, reaching $370 million in Q1 2025:

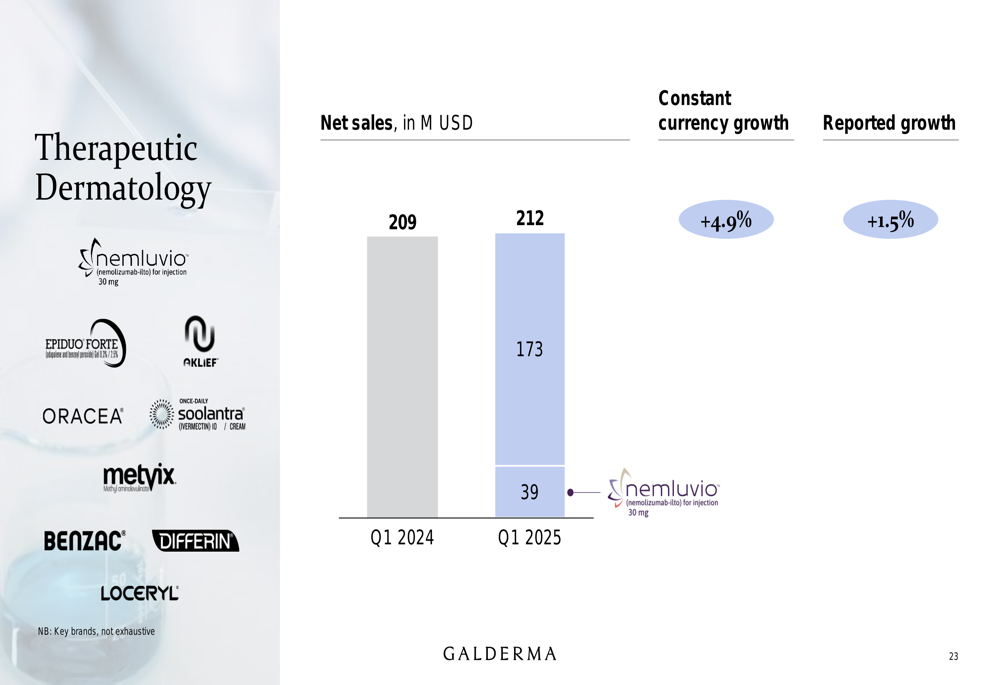

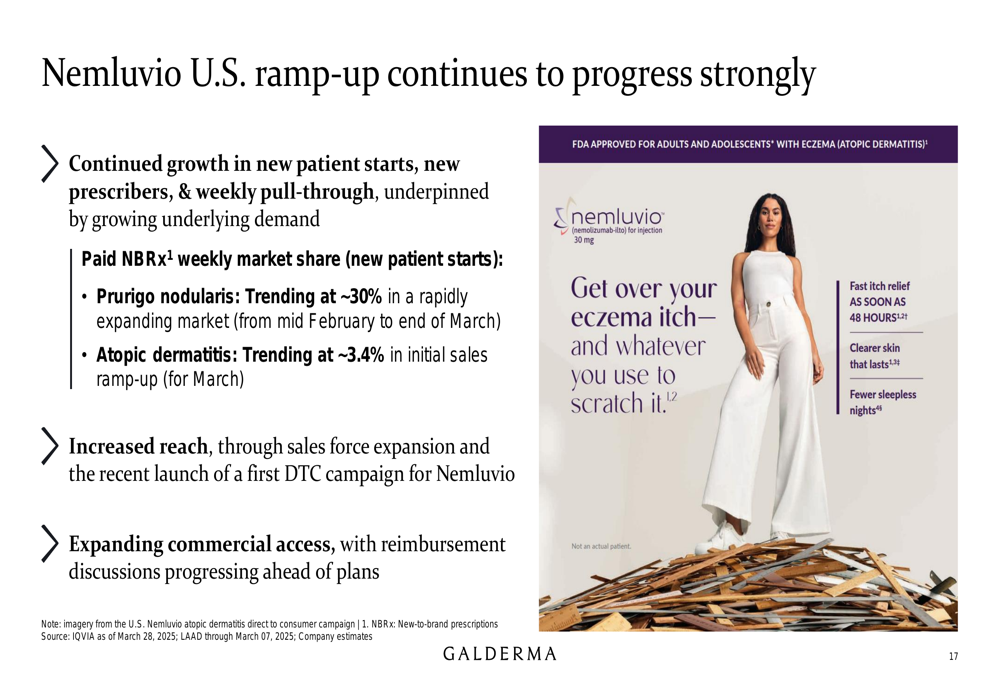

Therapeutic Dermatology grew 4.9% to $212 million, with Nemluvio contributing $39 million in Q1 sales:

Regional performance shows stronger growth in international markets compared to the U.S.:

Strategic Initiatives & New Product Launches

Galderma described 2025 as the "first of 2 years with significant launches," highlighting several key products that will drive future growth. The company is focusing on geographic expansion, particularly in underpenetrated international markets.

Nemluvio’s U.S. launch continues to gain momentum, with market share trending at approximately 30% in prurigo nodularis and 3.4% in atopic dermatitis. The product is also launching internationally, beginning with Germany, where it has exceeded targets for healthcare professional reach and patient demand.

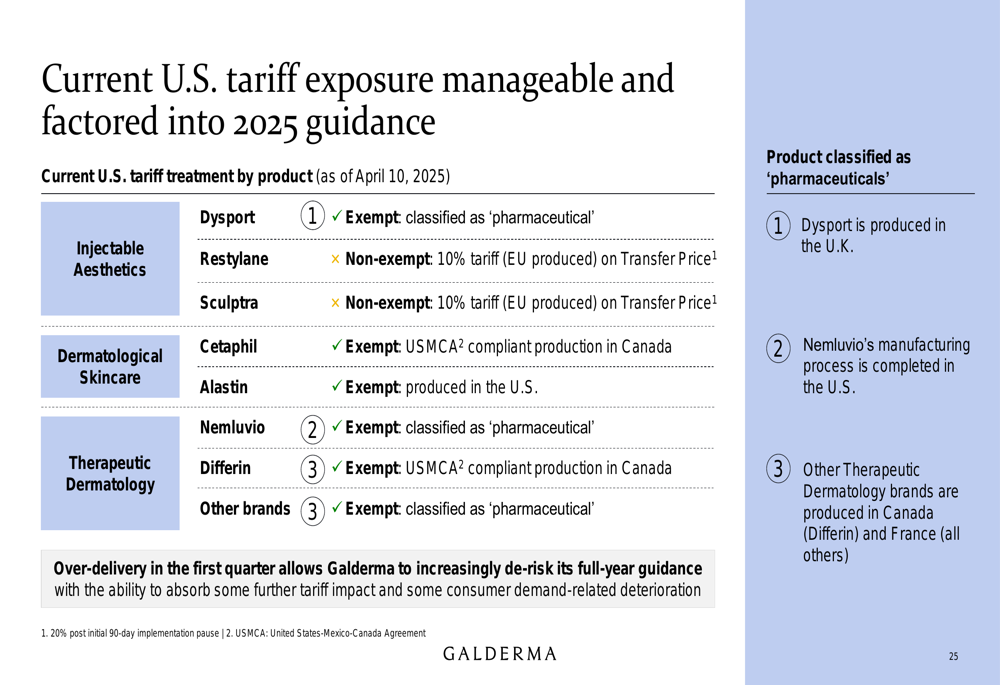

The company is actively managing its exposure to U.S. tariffs, with several key products exempt from additional duties:

Outlook & Guidance

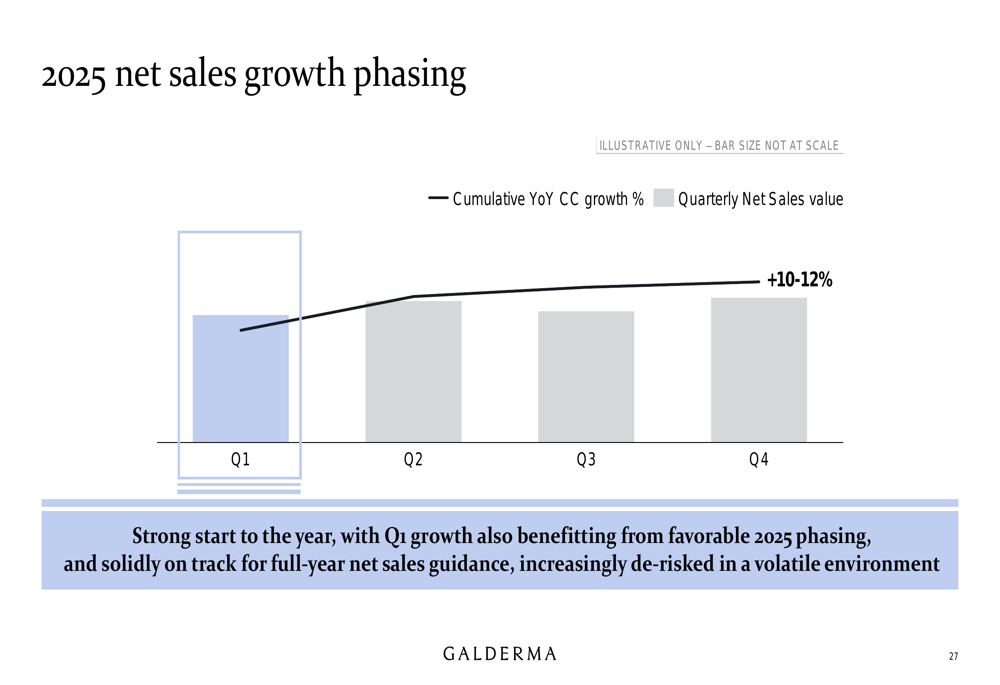

Galderma confirmed its full-year 2025 guidance of 10-12% net sales growth at constant currency and approximately 23% Core EBITDA margin. Management expressed confidence that the strong Q1 performance has "increasingly de-risked" the full-year outlook.

The company provided insight into the expected quarterly phasing of growth throughout 2025:

Galderma’s strategic focus on new product launches and international expansion appears to be paying off, as evidenced by its strong Q1 performance. The company emphasized its strengthened financial profile, including an improved balance sheet from continued rapid deleveraging and robust cash flow.

Management highlighted that its guidance fully factors in the currently announced U.S. tariff exposure. With a diversified geographic footprint and strong performance across all product categories, Galderma appears well-positioned to navigate market volatility while continuing to deliver growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.