Gold prices bounce off 3-week lows; demand likely longer term

Introduction & Market Context

Genco Shipping & Trading Limited (NYSE:GNK) reported a net loss for the first quarter of 2025 amid challenging market conditions, according to the company’s Q1 earnings presentation delivered on May 8, 2025. Despite the loss, Genco maintained its quarterly dividend and emphasized its strong balance sheet position as freight rates show signs of significant improvement.

The company’s shares were down 2.9% in premarket trading at $13.07, reflecting investor reaction to the quarterly results. This follows a modest 0.15% gain in the previous session, with the stock trading well below its 52-week high of $23.43.

Quarterly Performance Highlights

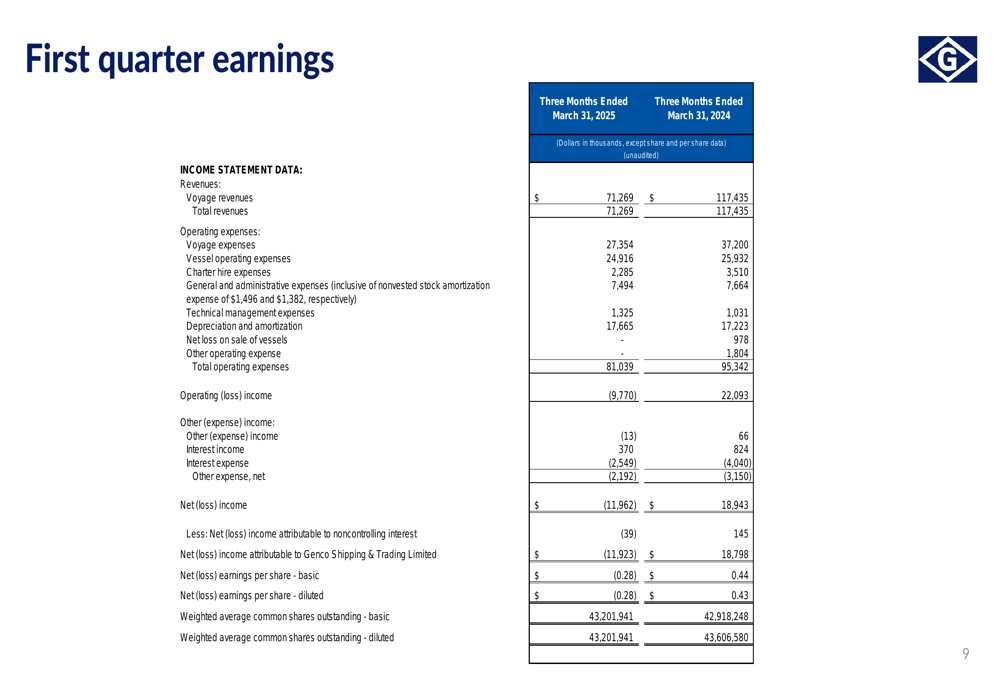

Genco reported a net loss of $11.9 million or $0.28 per share for Q1 2025, a significant reversal from the $18.9 million profit or $0.44 per share recorded in the same period last year. Total (EPA:TTEF) revenues declined substantially to $71.3 million from $117.4 million in Q1 2024, while operating expenses decreased to $81.0 million from $95.3 million.

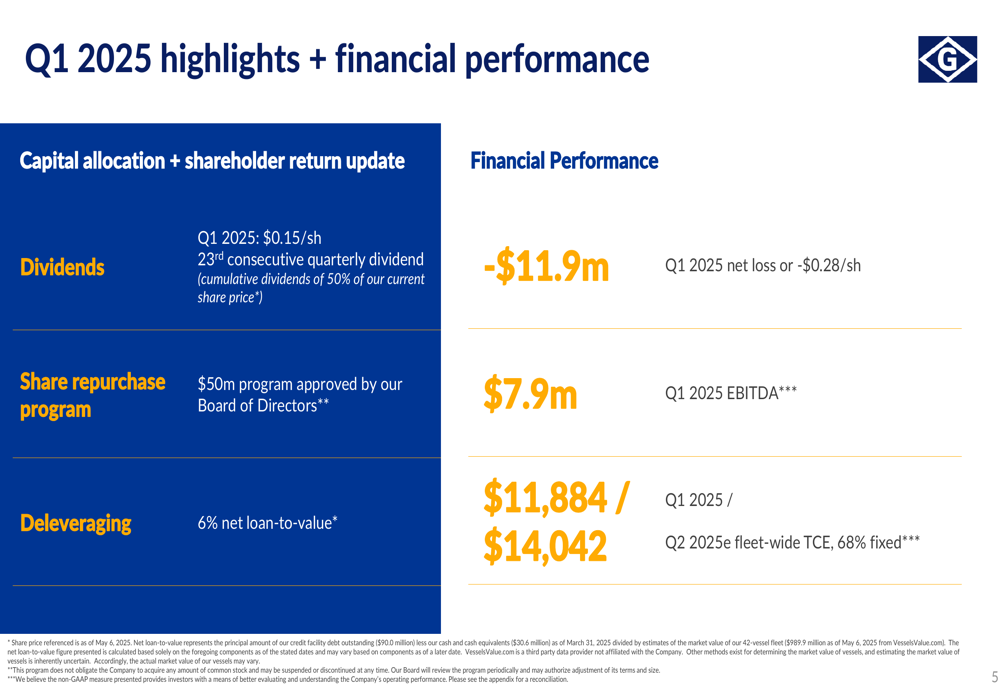

The company’s Time Charter Equivalent (TCE) rate was $11,884 per day during the quarter, with Q2 2025 estimates projecting an improvement to $14,042 per day with 68% of available days already fixed. Fleet utilization remained strong at 98.0%, with daily vessel operating expenses averaging $6,592 per vessel.

As shown in the following quarterly earnings summary:

Despite the challenging quarter, Genco generated EBITDA of $7.9 million and maintained operational efficiency with its 42-vessel fleet. The company highlighted its key financial metrics and performance indicators:

Financial Position and Capital Allocation

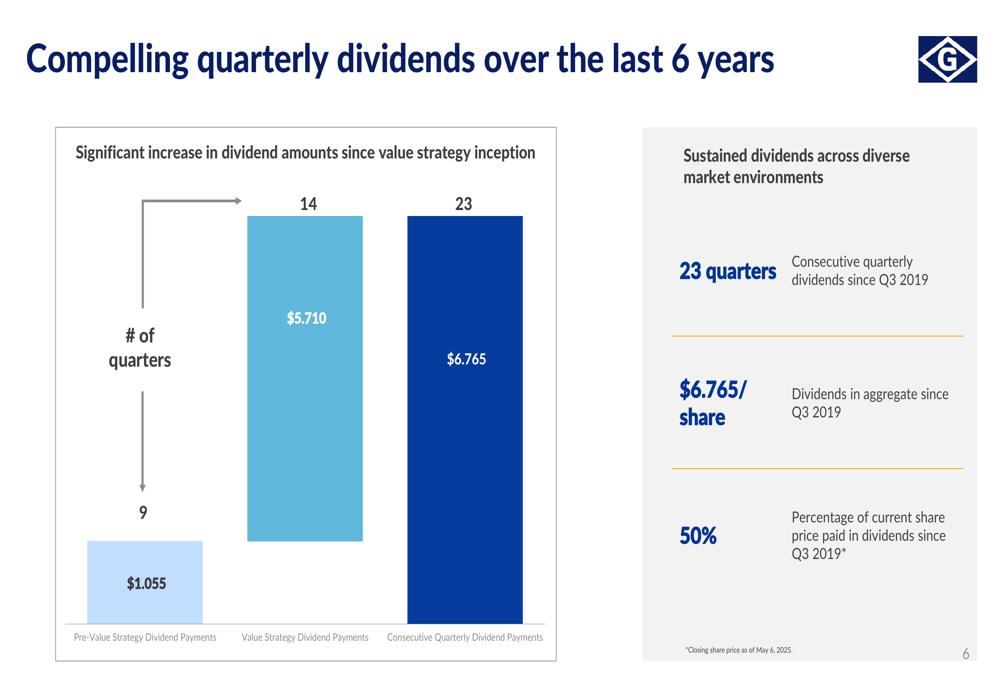

Genco maintained its commitment to shareholder returns by declaring a Q1 2025 dividend of $0.15 per share, marking its 23rd consecutive quarterly dividend. The company noted that cumulative dividends since Q3 2019 represent approximately 50% of its current share price.

The Board of Directors also approved a $50 million share repurchase program, signaling confidence in the company’s long-term prospects despite current market challenges. Genco’s balance sheet remains robust with $30.6 million in cash and a significantly reduced debt position of $82.7 million as of March 31, 2025.

The company’s dividend history demonstrates its consistent commitment to shareholder returns across varying market conditions:

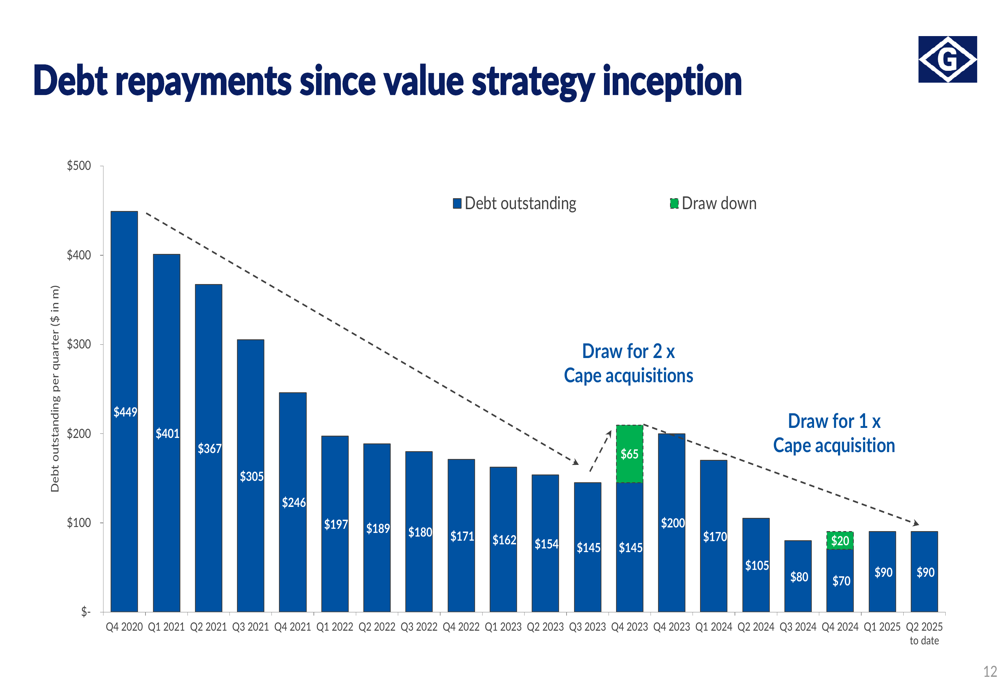

Genco has made substantial progress in deleveraging its balance sheet since implementing its value strategy. Debt outstanding has decreased from $449 million in Q4 2020 to a projected $90 million in Q2 2025, representing an 80% reduction since the beginning of 2021:

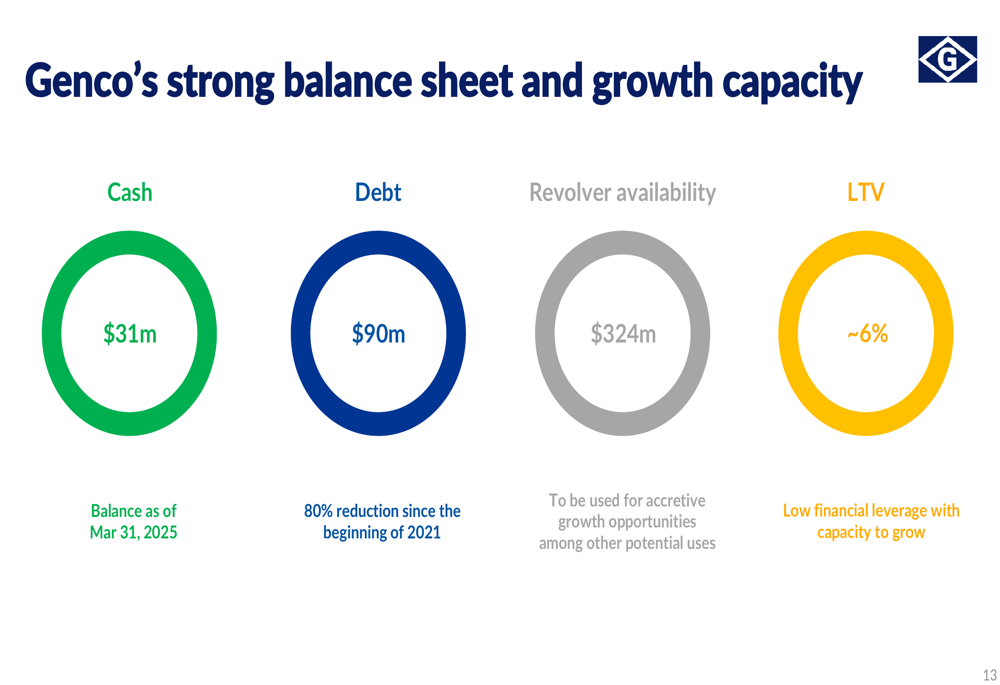

This deleveraging has positioned the company with considerable financial flexibility and growth capacity, as illustrated in the following slide:

Industry Outlook and Strategic Positioning

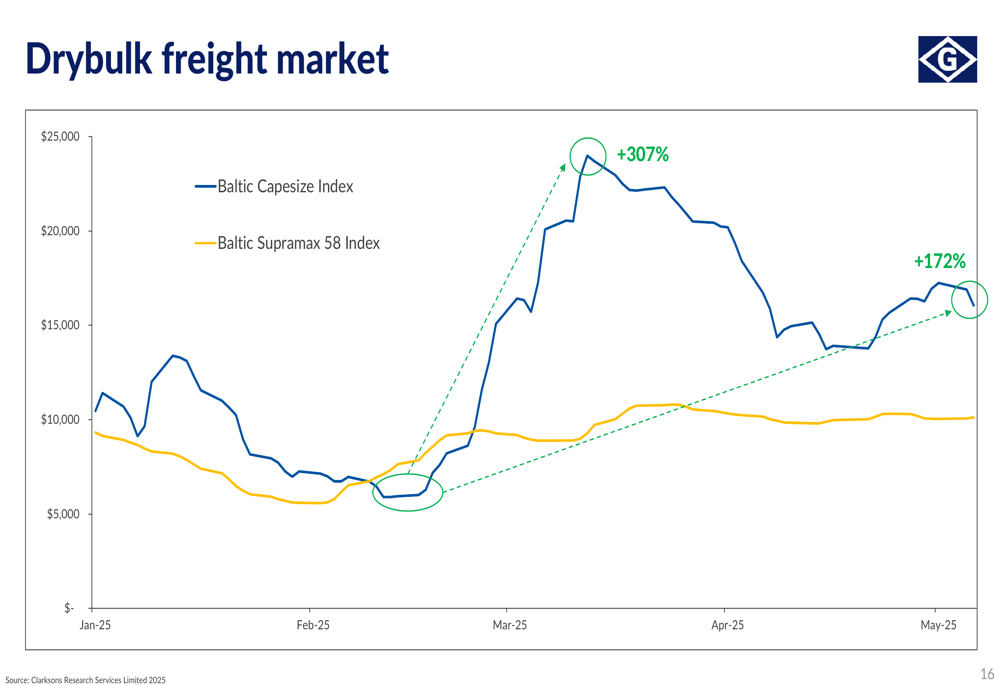

The drybulk freight market has shown significant improvement in 2025, with the Baltic Capesize Index increasing 307% and the Baltic Supramax 58 Index rising 172% year-to-date. These positive trends suggest a potential recovery in the sector that could benefit Genco in upcoming quarters.

The following chart illustrates the substantial improvement in freight rates:

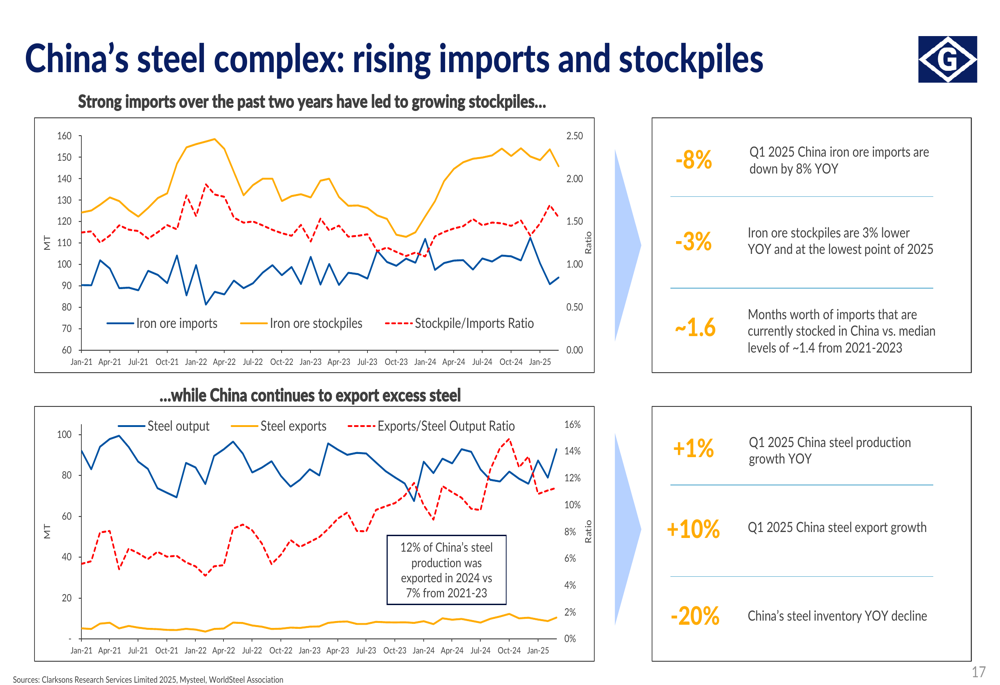

China’s steel complex continues to be a key driver for the drybulk shipping market. While iron ore imports were down 8% year-over-year, steel production increased by 1% and steel exports rose by 10%, indicating shifting trade patterns that impact shipping demand:

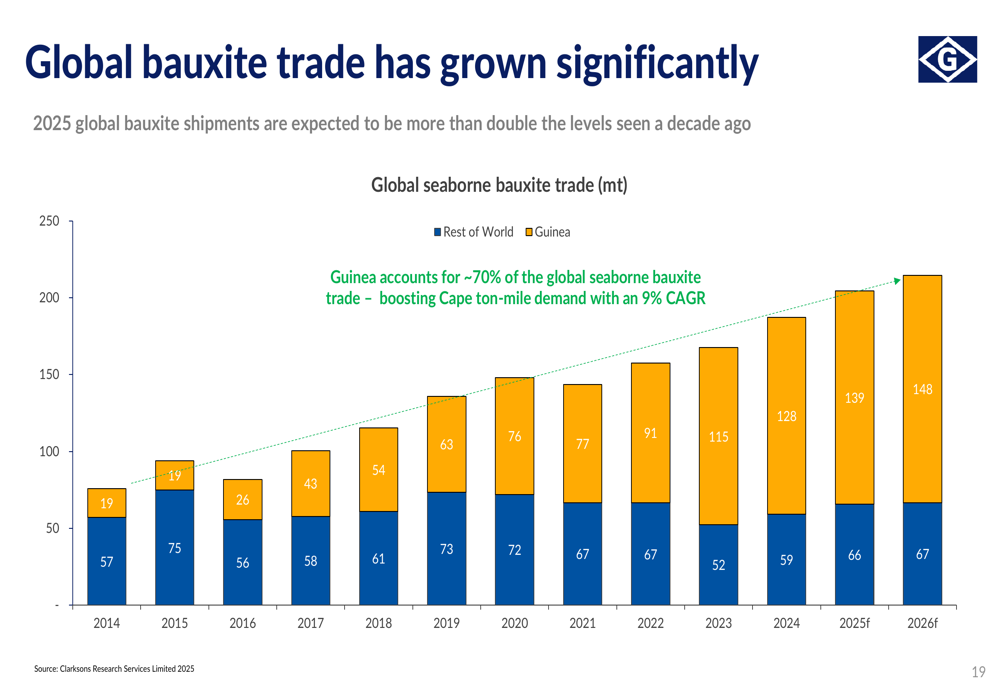

Genco highlighted several long-term industry trends supporting its strategic positioning, including global bauxite trade growth that is expected to double compared to a decade ago. Guinea accounts for 70% of global seaborne bauxite trade and is driving Cape ton-mile demand with a 9% CAGR:

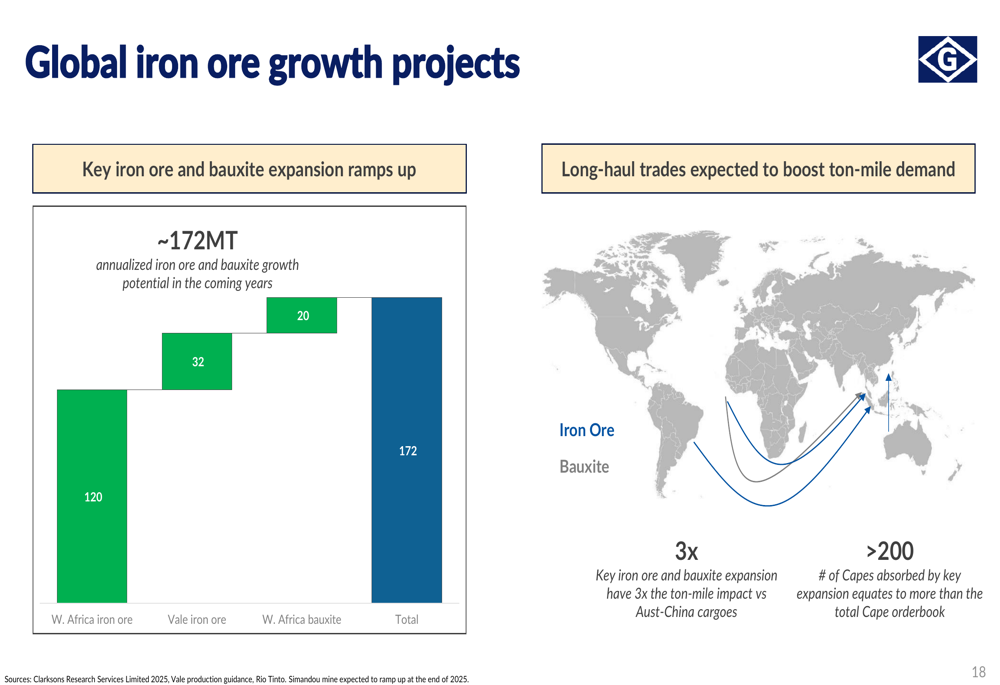

The company also pointed to significant growth potential from global iron ore projects that could generate substantial ton-mile demand in the coming years:

Forward-Looking Statements

Looking ahead, Genco emphasized the aging global drybulk fleet as a potential catalyst for improved market conditions. By 2030, approximately 30% of the current drybulk fleet will be 20 years or older, representing about 4,200 ships. Combined with yard capacity that is down approximately 60% compared to 2008, this could create supply constraints that support higher freight rates.

The company highlighted its operating leverage, noting that every $1,000 increase in TCE rates generates approximately $15 million in incremental annualized EBITDA across its 42-vessel fleet. For its 16 Capesize vessels specifically, every $5,000 increase in TCE rates translates to approximately $29 million in incremental annualized EBITDA.

Genco’s management expressed confidence in the company’s ability to navigate current market challenges while positioning for future growth opportunities. With a low net loan-to-value of approximately 6% and $324 million in revolver availability, the company maintains significant financial flexibility to pursue accretive growth while continuing its commitment to shareholder returns through dividends and share repurchases.

The Q2 2025 dividend calculation indicates a continued focus on balancing shareholder returns with maintaining financial strength, with a voluntary quarterly reserve of $19.50 million for the upcoming quarter compared to $1.14 million in Q1 2025, reflecting a prudent approach to capital allocation in the current market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.