What happens to stocks if AI loses momentum?

Introduction & Market Context

Genesco Inc . (NYSE:GCO) released its first quarter fiscal 2026 results on June 4, 2025, showing modest sales growth and improved bottom-line performance despite the seasonally challenging quarter. The footwear-focused retailer, which operates brands including Journeys, Schuh, and Johnston & Murphy, reported a 4% increase in total sales compared to the same period last year.

The company’s stock, which had fallen sharply following its Q4 FY25 earnings miss in March, showed signs of stabilization with a 4.88% gain in the previous session and a 0.89% increase in premarket trading, suggesting investors may be finding encouragement in the Q1 results.

Quarterly Performance Highlights

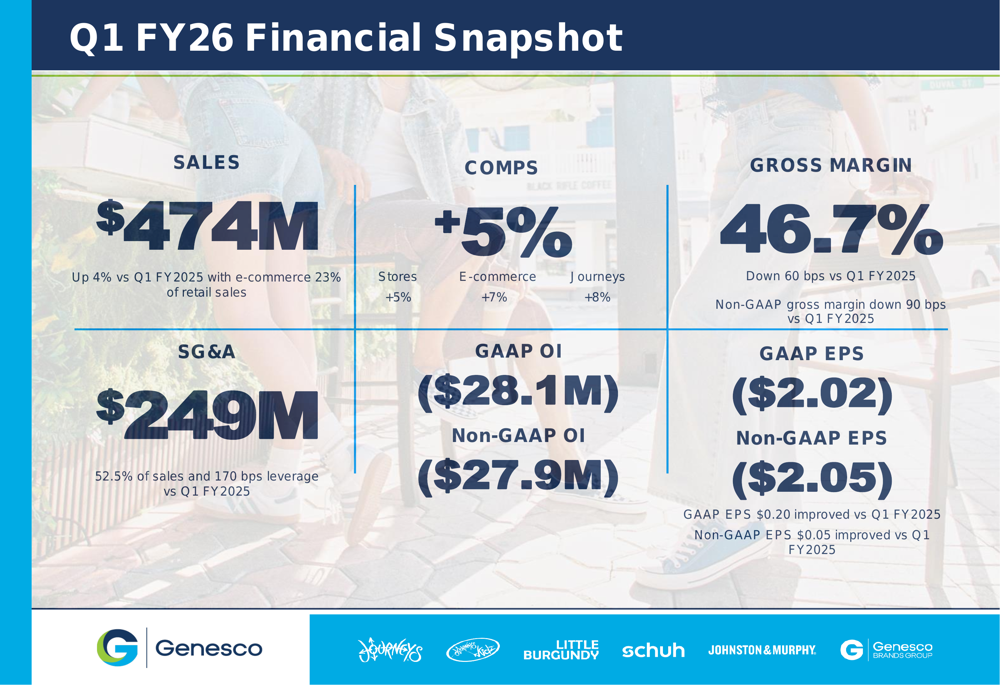

Genesco reported Q1 FY26 sales of $474 million, representing a 4% increase over the prior year period. Comparable sales grew by 5%, with both physical stores and e-commerce channels showing strength at 5% and 7% growth, respectively. The Journeys brand was the standout performer with comparable sales increasing by 8%.

As shown in the following comprehensive financial snapshot:

Despite the sales growth, Genesco reported a GAAP operating loss of $28.1 million and a non-GAAP operating loss of $27.9 million for the quarter. However, this represents an improvement from the prior year, with GAAP EPS of ($2.02) improving by $0.20 and non-GAAP EPS of ($2.05) improving by $0.05 compared to Q1 FY25.

The company’s gross margin declined slightly to 46.7%, down 60 basis points from the prior year. This was offset by improved expense management, with SG&A expenses representing 52.5% of sales, a 170 basis point improvement from Q1 FY25.

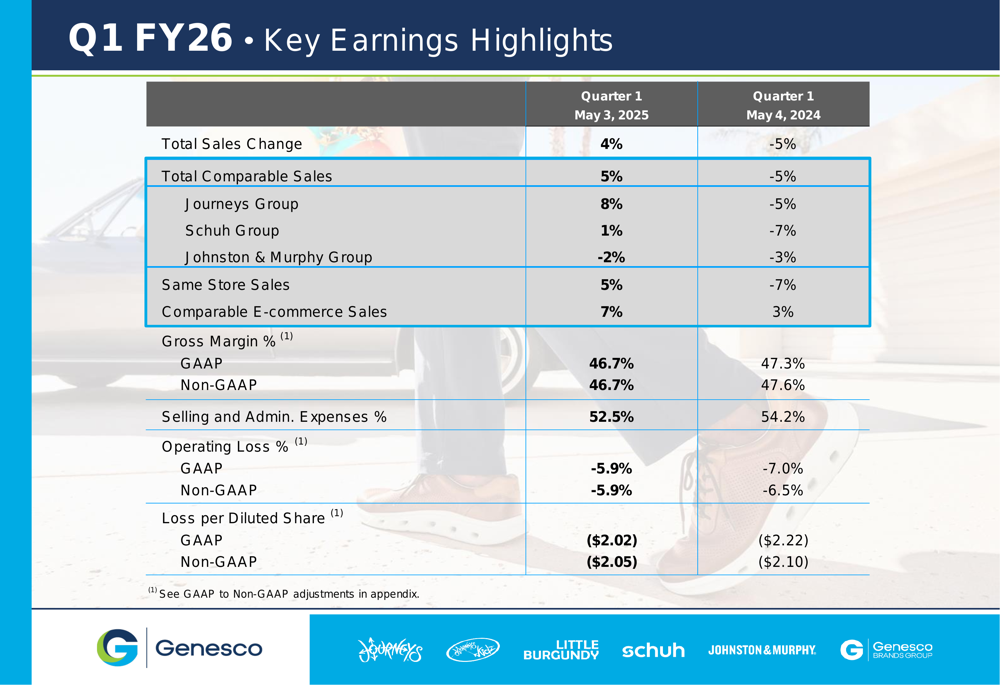

A detailed breakdown of key earnings metrics shows the company’s year-over-year improvement:

Strategic Initiatives

Genesco continues to execute its footwear-focused strategy, with particular emphasis on the Journeys brand. The company is investing in its "Journeys 4.0" store concept, completing 29 remodels during the quarter for a total of 39 to date, with plans to exceed 75 remodels by the end of the fiscal year.

The company is also expanding its consumer segmentation strategy for Journeys, targeting three distinct consumer segments to reach a wider teen audience. This approach is expected to increase Journeys’ total addressable market by 6-7 times, according to management.

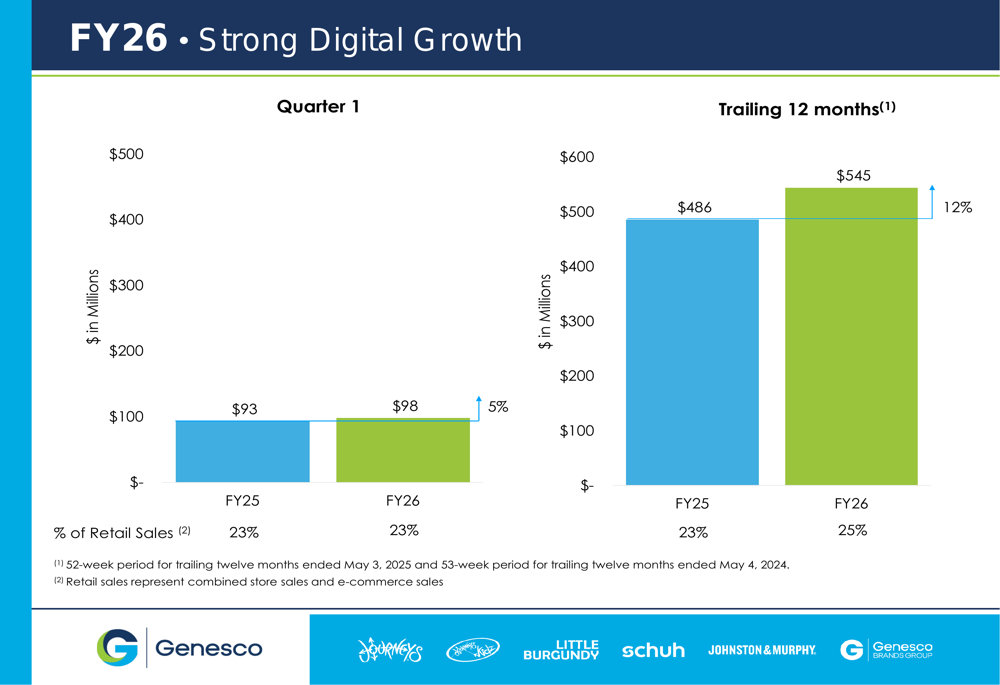

Digital growth remains a priority, with e-commerce sales increasing 5% in Q1 and 12% on a trailing 12-month basis. E-commerce now represents 23% of Genesco’s retail sales, highlighting the company’s successful omnichannel approach.

The following chart illustrates the company’s digital growth trajectory:

Capital Allocation and Store Portfolio

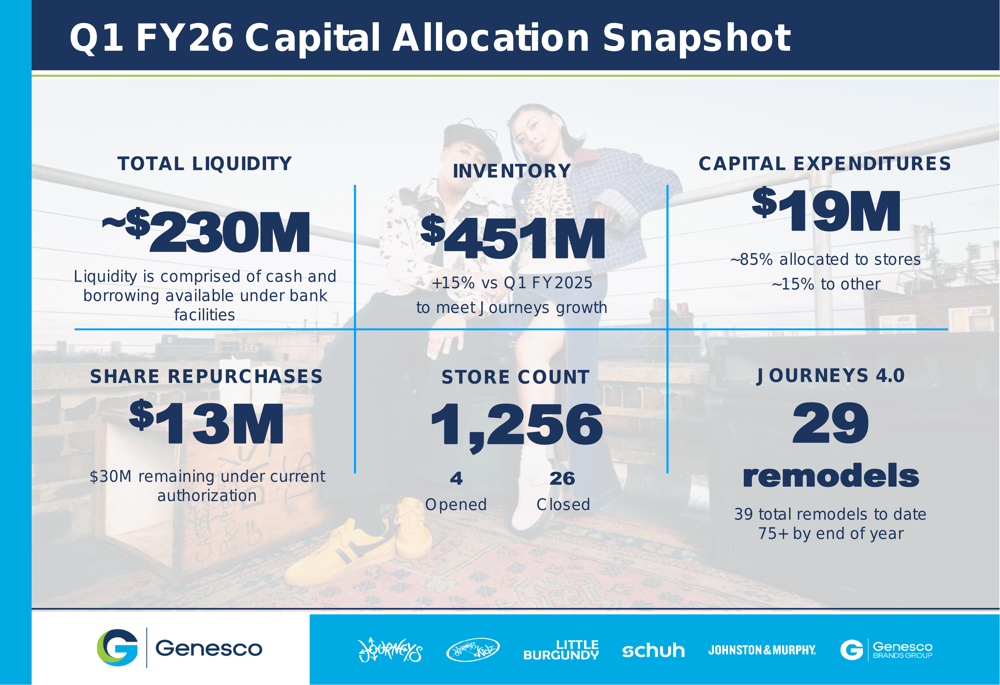

Genesco maintained a strong liquidity position of approximately $230 million at the end of Q1 FY26. The company’s inventory stood at $451 million, up 15% compared to the prior year, which management attributed to supporting Journeys’ growth.

The company continued its share repurchase program, buying back $13 million worth of shares during the quarter, with $30 million remaining under the current authorization. Capital expenditures totaled $19 million, with approximately 85% allocated to stores.

The following capital allocation snapshot provides additional details:

Genesco is actively managing its store portfolio, closing 26 stores while opening 4 during the quarter, bringing the total store count to 1,256. The company projects further consolidation by the end of FY26, with a net reduction of 47 stores planned.

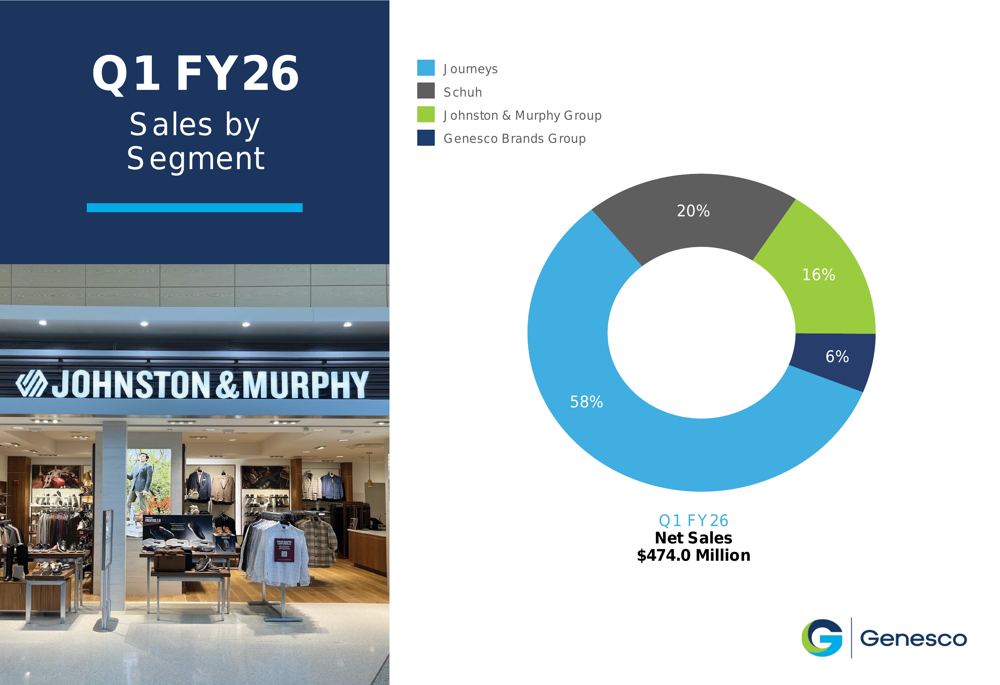

The company’s sales remain heavily weighted toward the Journeys Group, which accounted for 58% of total sales in Q1 FY26:

Tariff Mitigation Strategy

A significant focus of the presentation was Genesco’s approach to mitigating the impact of tariffs. Management indicated that approximately 11% of the company’s products currently come from China, but they expect to reduce this exposure by half or more by the end of FY26.

The company outlined several mitigation strategies, including accelerating inventory, diversifying suppliers, working with factory partners, identifying cost reductions, and planning for price increases. Management expressed confidence that these actions would mostly offset the tariff impact for the fiscal year.

Forward-Looking Statements

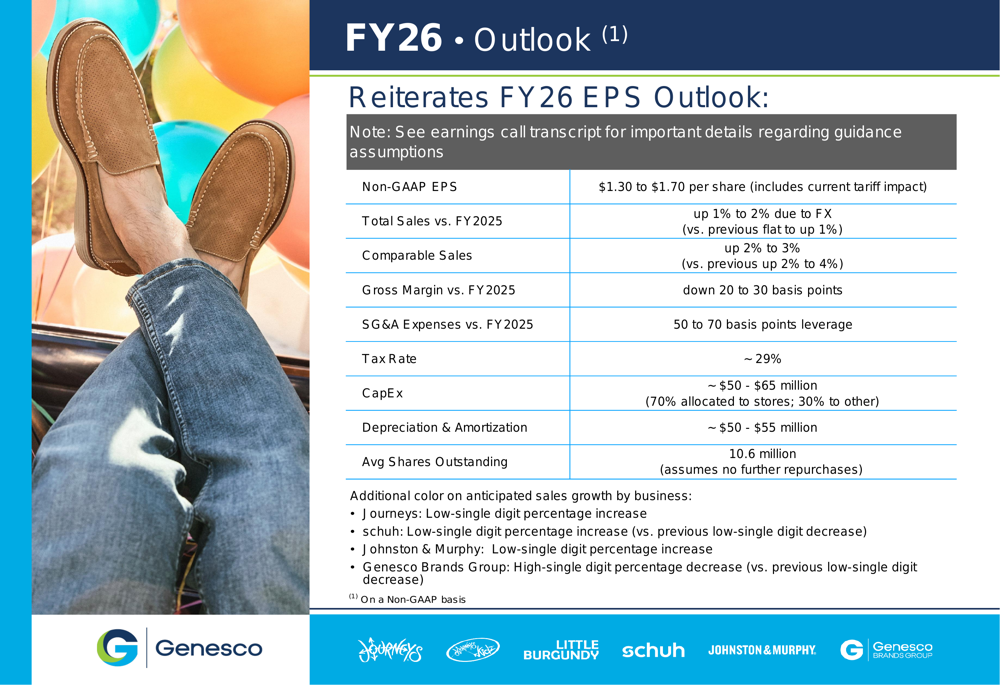

Genesco maintained its full-year FY26 guidance, projecting non-GAAP EPS of $1.30 to $1.70 per share. The company expects total sales to increase by 1% to 2% compared to FY25, with comparable sales growth of 2% to 3%.

Gross margin is expected to decline by 20 to 30 basis points compared to FY25, while SG&A expenses are projected to leverage by 50 to 70 basis points. The company anticipates capital expenditures of $50 to $65 million for the full year.

The detailed outlook is presented in the following slide:

By business segment, Genesco expects low-single digit percentage increases for Journeys, Schuh, and Johnston & Murphy, while the Genesco Brands Group is projected to see a high-single digit percentage decrease.

Detailed Financial Analysis

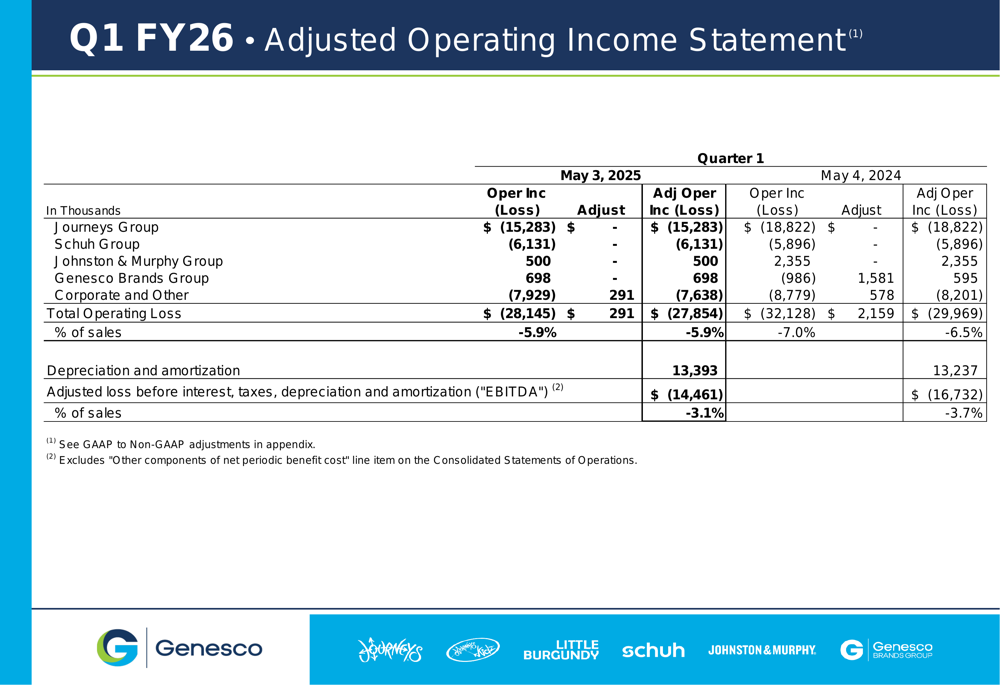

A closer examination of Genesco’s Q1 FY26 adjusted operating income statement reveals the performance by segment:

The Journeys Group, despite being the largest contributor to sales, posted an operating loss of $15.3 million, though this represents an improvement from the $18.8 million loss in the prior year period. The Johnston & Murphy Group and Genesco Brands Group were the only segments to report positive operating income for the quarter.

Overall, Genesco’s Q1 FY26 results show modest improvement in a traditionally challenging quarter for the company. The strength of the Journeys brand and the company’s digital growth provide positive indicators, while management’s confidence in maintaining full-year guidance suggests they believe the strategic initiatives are gaining traction despite ongoing challenges from tariffs and a competitive retail environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.