DexCom earnings beat by $0.03, revenue topped estimates

Introduction & Market Context

Genesis Energy, L.P. (NYSE:GEL) released its first quarter 2025 earnings presentation on May 8, showing the master limited partnership is navigating a transitional period following its strategic exit from the soda ash business. The company’s stock closed at $14.36, down 0.56% on the day, but has shown significant improvement from the $11.29 level seen after its Q4 2024 earnings report.

The presentation highlights Genesis Energy’s continued focus on its core offshore pipeline transportation and marine transportation segments, with major offshore developments expected to drive growth in the coming quarters. This strategic repositioning comes after a challenging period, as the company reported a significant net loss for the quarter while maintaining its distribution.

Quarterly Performance Highlights

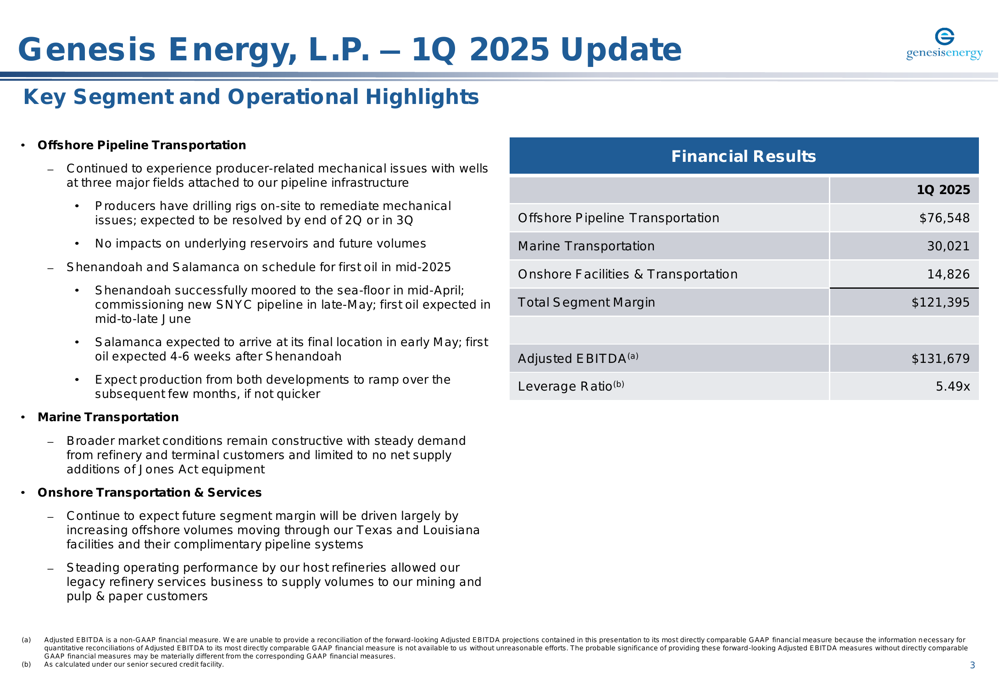

Genesis Energy reported Adjusted EBITDA of $131.7 million for the first quarter of 2025, continuing to navigate operational challenges while preparing for anticipated growth. The company maintained its quarterly distribution of $0.165 per common unit, resulting in a tight distribution coverage ratio of 1.01x.

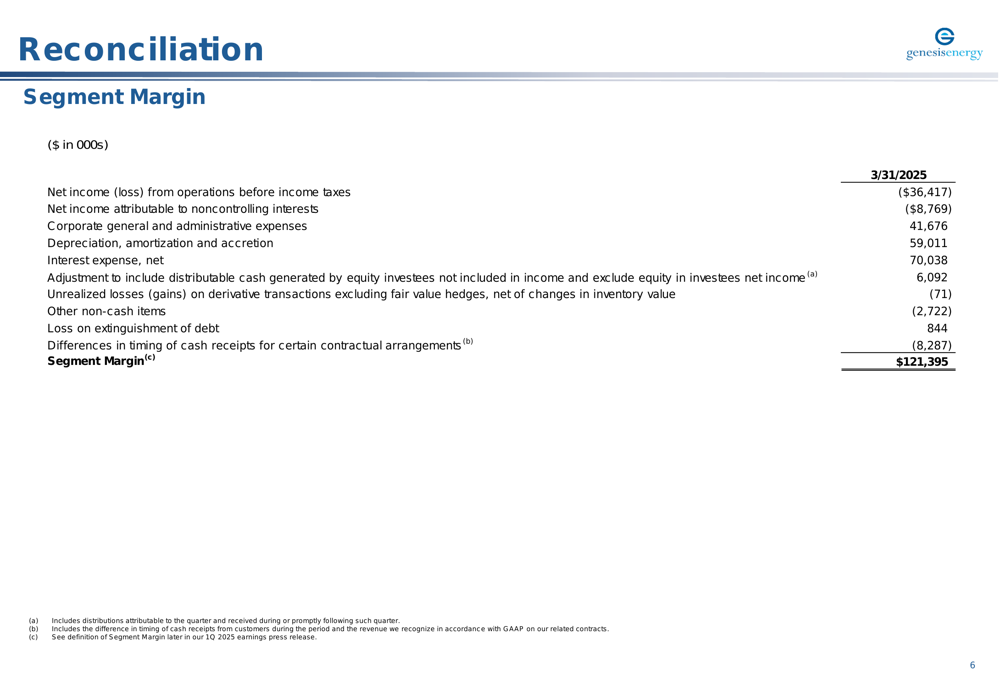

The key segment breakdown reveals the company’s current revenue structure, with Offshore Pipeline Transportation generating $76.5 million, Marine Transportation contributing $30.0 million, and Onshore Facilities & Transportation adding $14.8 million to the total segment margin of $121.4 million.

As shown in the following segment and operational highlights:

Despite producer-related mechanical issues affecting the Offshore Pipeline Transportation segment, management emphasized that its key growth projects remain on schedule. The Marine Transportation segment is experiencing constructive market conditions, while the Onshore segment is positioned to benefit from increased offshore volumes as new developments come online.

Strategic Initiatives

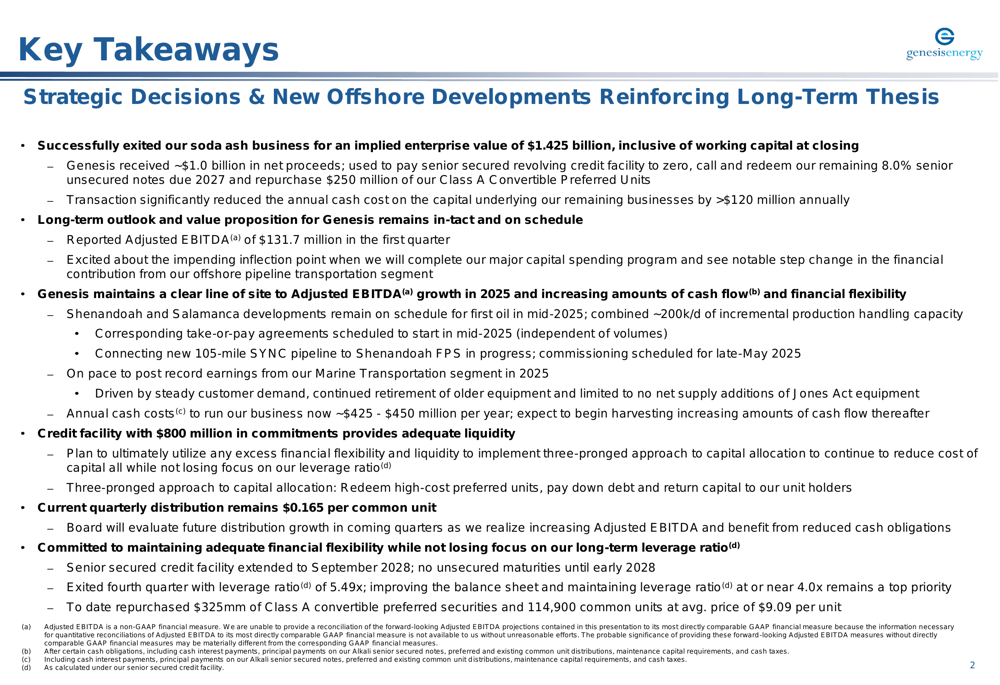

The most significant strategic development highlighted in the presentation is Genesis Energy’s successful exit from the soda ash business for $1.425 billion. This transaction represents a major shift in the company’s portfolio and provides substantial liquidity to address capital structure concerns.

The company’s strategic focus is clearly articulated in its key takeaways slide, which outlines both recent accomplishments and forward-looking priorities:

Management emphasized its commitment to utilizing excess liquidity to reduce the cost of capital while maintaining adequate financial flexibility. The presentation highlighted the extension of the company’s credit facility and noted plans to repurchase Class A convertible preferred securities and common units, signaling confidence in the company’s long-term value proposition.

Detailed Financial Analysis

Genesis Energy’s financial position remains challenging, with a leverage ratio of 5.49x as of March 31, 2025. The balance sheet shows senior unsecured notes of approximately $3.44 billion, partially offset by cash and cash equivalents of $377 million, resulting in adjusted debt of $3.05 billion.

The detailed breakdown of the company’s balance sheet and credit profile provides insight into its current financial standing:

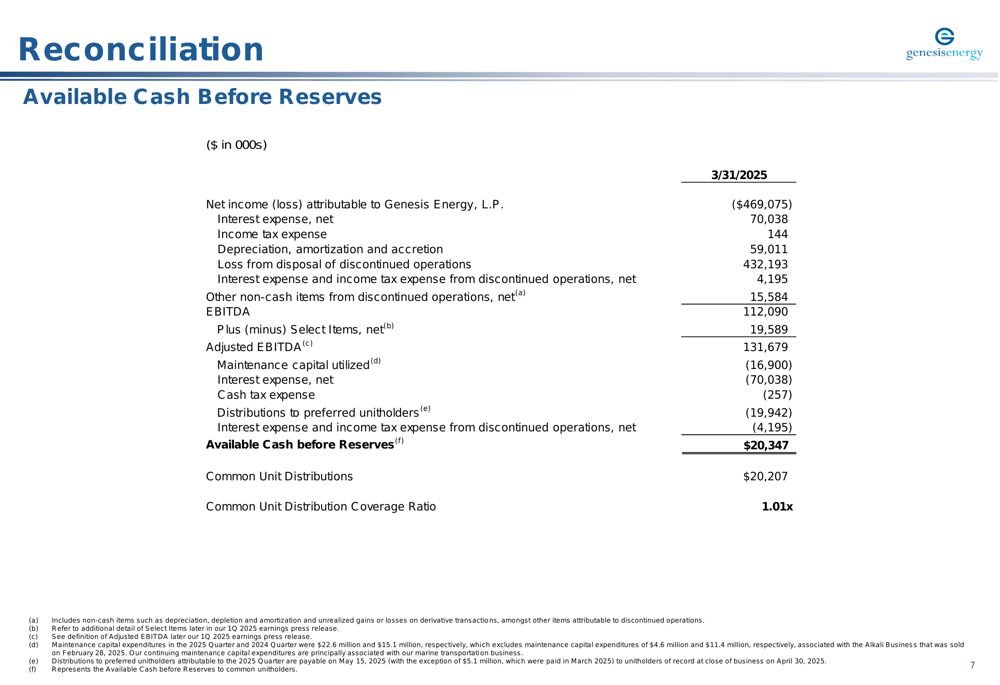

The reconciliation of Available Cash Before Reserves reveals the significant gap between reported net income and distributable cash. Genesis reported a net loss attributable to the partnership of $469.1 million, but after various adjustments, arrived at Available Cash Before Reserves of $20.3 million, barely covering the $20.2 million in common unit distributions.

The historical leverage ratio trend shows Genesis Energy’s debt position over time, providing context for the current 5.49x ratio:

Forward-Looking Statements

Genesis Energy’s presentation emphasizes its optimistic outlook despite current challenges. The company maintains that its long-term thesis remains intact, with a clear path to Adjusted EBITDA growth in 2025 and increasing cash flow and financial flexibility thereafter.

The most significant catalysts on the horizon are the Shenandoah and Salamanca developments, which remain on schedule for first oil in mid-2025. These projects are expected to add approximately 200,000 barrels per day of incremental production handling capacity, potentially transforming the company’s financial profile.

This timeline aligns with statements from the previous quarter’s earnings call, where management projected significant cash flow generation starting in late 2025. However, investors should note that the Q1 2025 Adjusted EBITDA of $131.7 million, if annualized, would fall short of the previously projected ~$700 million for full-year 2025, suggesting the company is counting heavily on these offshore projects coming online as scheduled.

Genesis Energy’s tight distribution coverage ratio of 1.01x underscores the importance of these upcoming developments for maintaining the current distribution level. While the company has successfully completed its strategic exit from the soda ash business, providing valuable liquidity, its high leverage ratio of 5.49x remains a concern that management will need to address as it works to strengthen its financial position throughout 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.