IonQ reaches 1,000 patents milestone with new quantum computing grants

Introduction & Market Context

Gentex Corporation (NASDAQ:GNTX) presented its Q3 2024 investor slides on October 25, highlighting the company’s ability to maintain growth despite significant challenges in the automotive industry. The presentation, titled "Growth Over Market," emphasized how Gentex has navigated through a business environment characterized by light vehicle production declines, chip shortages, supply chain issues, record inflation, and labor shortages.

The automotive supplier, best known for its auto-dimming mirrors and other advanced electronic components, positioned itself as resilient in an industry undergoing significant transformation. According to the presentation, the automotive sector is experiencing multiple disruptive trends simultaneously, including digitalization, electrification, and autonomous driving.

Recent earnings results suggest these challenges are having an impact. In Q1 2025, Gentex reported an EPS of $0.42, slightly missing analyst expectations of $0.43, with revenue of $576.8 million falling short of the $578.68 million forecast. The stock is currently trading near its 52-week low of $20.28, with shares dipping 1.21% following the earnings release.

Financial Performance & Outlook

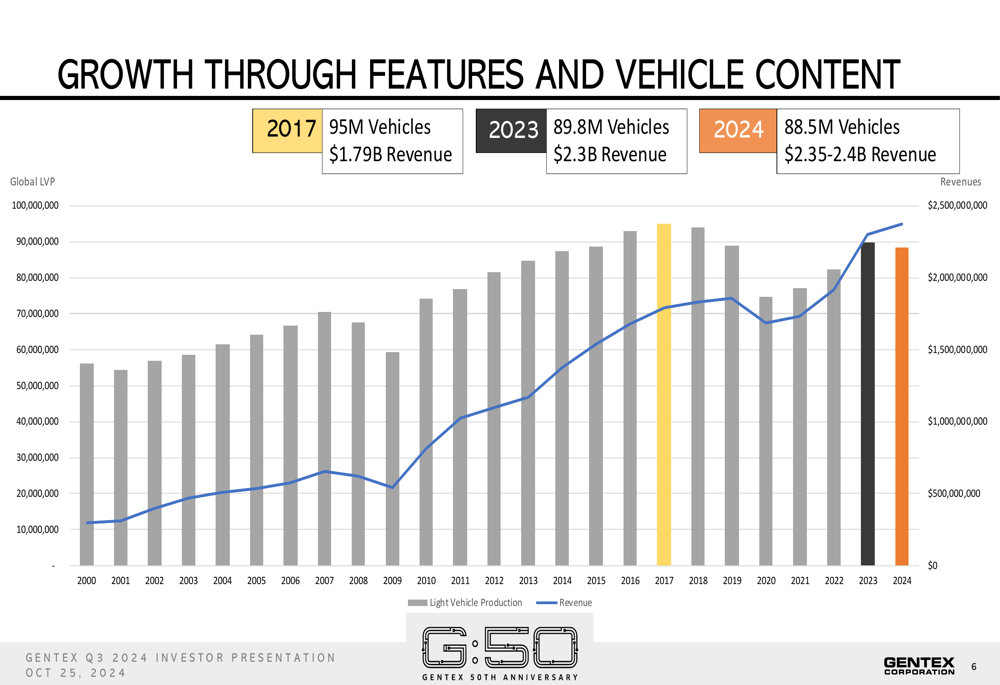

Gentex reported 2023 revenue of $2.3 billion with a gross margin of 33.2%, while operating expenses totaled $266.9 million. For 2024, the company projects revenue between $2.35-2.4 billion and improved gross margins of 33.5-34%. Looking further ahead, Gentex initially forecasted 2025 revenue of $2.45-2.55 billion in its October presentation, though more recent guidance in the Q1 2025 earnings call revised this downward to $2.1-2.2 billion.

A key highlight of the presentation was Gentex’s ability to grow revenue despite declining global light vehicle production. This is illustrated in the following chart showing how revenue has increased even as vehicle production volumes have fluctuated:

The company’s gross margin, while improving, remains below pre-pandemic levels. In 2019, Gentex achieved a 37% gross margin, which fell to 33.2% by 2023. Management expects modest improvement to 33.5-34% in 2024, though recent earnings suggest continued pressure with Q1 2025 gross margin at 33.2%, down from 34.3% in the same period last year.

Growth Strategy & Product Portfolio

Gentex’s growth strategy centers on increasing content per vehicle rather than relying solely on automotive production volume growth. The company has maintained a dominant market share in the electrochromic mirror market, consistently holding 80-90% of the market since 1995.

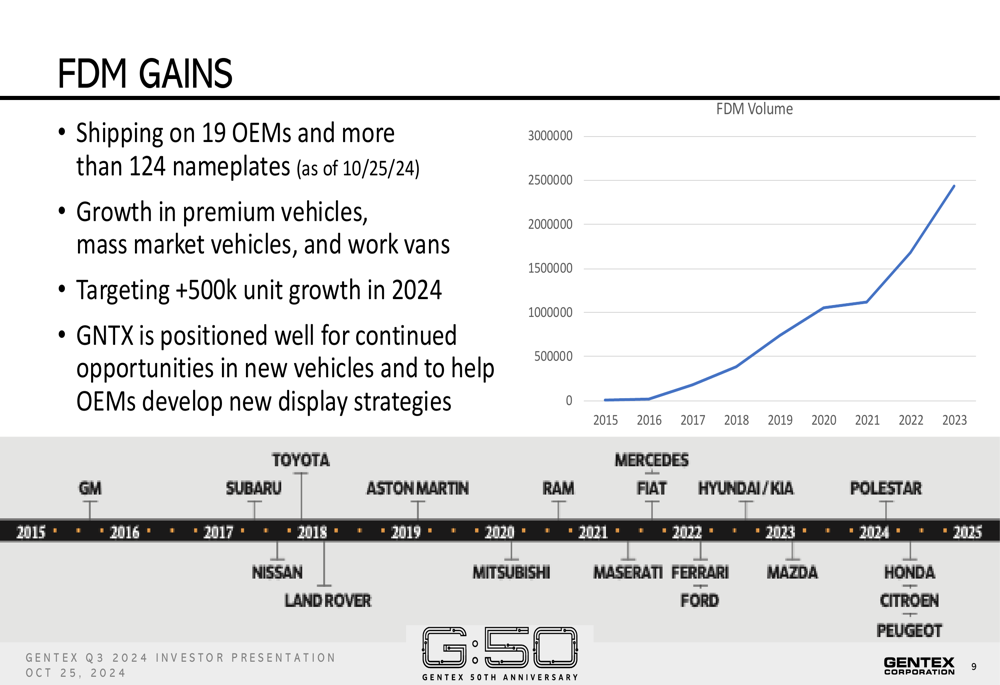

A significant growth driver is the Full Display Mirror (FDM), which is now shipping to 19 OEMs across more than 124 vehicle nameplates. The company is targeting over 500,000 units of FDM growth in 2024 alone, as illustrated in this chart:

Gentex’s product strategy extends beyond mirrors into four key technology platforms:

1. Digital Vision - Including Full Display Mirrors and camera monitoring systems

2. Dimmable Glass - For sunroofs, sun visors, and privacy applications

3. Connectivity - HomeLink and transactional vehicle technologies

4. Sensing - Biometrics, in-cabin monitoring, and chemical sensing

The company’s intellectual property portfolio continues to expand, with 449 trademarks, 190 patents granted, and 178 new applications filed in 2023. Gentex’s core competencies span multiple areas:

Capital Allocation & Shareholder Returns

Gentex outlined a comprehensive capital allocation strategy focused on balancing growth investments with shareholder returns. The company plans capital expenditures of $150-175 million in 2024, down from $183.7 million in 2023. Facility expansions are underway at multiple locations, including North Riley #3, State Street (NYSE:STT) North, and a new distribution facility, all scheduled to open in 2024.

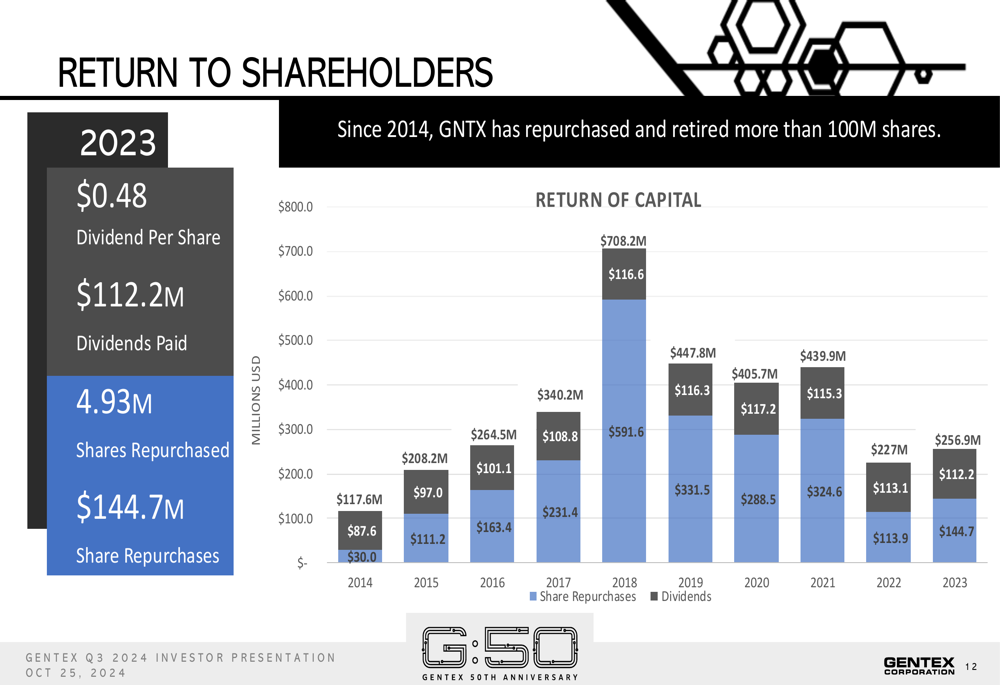

For shareholders, Gentex maintains an annual dividend of $0.48 per share (approximately $112 million per year) and continues its share repurchase program with approximately 10.1 million shares available under the current authorization as of October 25, 2024. Since 2014, the company has repurchased and retired more than 100 million shares, demonstrating its commitment to returning capital to shareholders:

Competitive Positioning & Customer Base

Gentex supplies to every major automotive OEM globally, with its top customers being Toyota (NYSE:TM) (18%), Volkswagen (ETR:VOWG_p) Group (14%), and General Motors (NYSE:GM) (10%). The company’s products are available on more than 660 vehicle nameplates across various segments. Notably, Gentex positions itself as both "powertrain agnostic" and "driver agnostic," meaning its products are designed to work across all vehicle types and driving modes, from traditional to fully autonomous.

The company’s primary competition comes not from other mirror manufacturers but from the 64% of vehicles worldwide that still use conventional prism mirrors, representing a significant growth opportunity. Global interior electrochromic mirror penetration stands at just 36%, suggesting substantial room for expansion.

Forward-Looking Statements & Challenges

While Gentex’s presentation painted an optimistic picture of growth through increased content per vehicle, recent earnings results suggest some headwinds. In the Q1 2025 earnings call, CEO Steve Downing acknowledged challenges from tariffs and operational costs but maintained confidence in the company’s long-term growth trajectory.

The revised 2025 revenue guidance of $2.1-2.2 billion (down from the $2.45-2.55 billion mentioned in the October presentation) indicates that market conditions may be more challenging than initially anticipated. Additional risks identified include tariff impacts (particularly in the China market), increasing operating expenses, market saturation, and ongoing supply chain disruptions.

Despite these challenges, Gentex continues to diversify its product portfolio and expand into new markets beyond automotive, including aerospace, fire protection, and medical applications, positioning the company for potential growth across multiple sectors in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.