Domo signs strategic collaboration agreement with AWS for AI solutions

Introduction & Market Context

Gentherm Inc (NASDAQ:THRM) shares plunged 6.93% in premarket trading to $23.10 following the release of its first quarter 2025 results on April 24, extending a challenging period for the thermal management technology provider. The stock has already been under pressure, trading near its 52-week low of $22.75, far below its 52-week high of $56.72.

The company reported modest revenue growth of 1% excluding foreign exchange impacts, but saw its adjusted EBITDA margin contract to 11.1% from 12.2% in the same period last year. This performance comes after a disappointing fourth quarter 2024, when Gentherm missed both earnings and revenue forecasts significantly.

Quarterly Performance Highlights

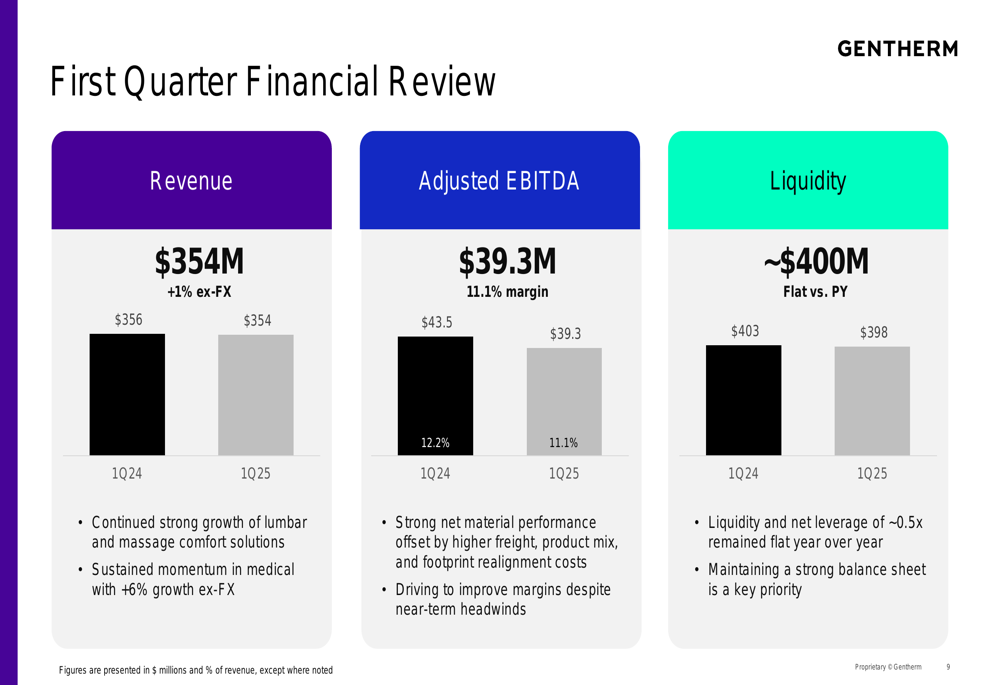

Gentherm reported Q1 2025 revenue of $354 million, representing a 1% increase excluding foreign exchange impacts, though slightly down from $356 million in Q1 2024 on a reported basis. The company’s adjusted EBITDA reached $39.3 million with an 11.1% margin, compared to $43.5 million and a 12.2% margin in the prior year period.

As shown in the following financial review chart:

Diluted adjusted earnings per share fell to $0.51 from $0.62 in Q1 2024, continuing the downward trend seen in the previous quarter. The company maintained its liquidity position at approximately $400 million, with a net leverage ratio of around 0.5x, unchanged year-over-year.

Despite margin pressures, Gentherm highlighted $400 million in automotive new business awards during the quarter, led by conquest awards, and noted continued strong growth in its lumbar and massage comfort solutions segment.

Operating Environment & Challenges

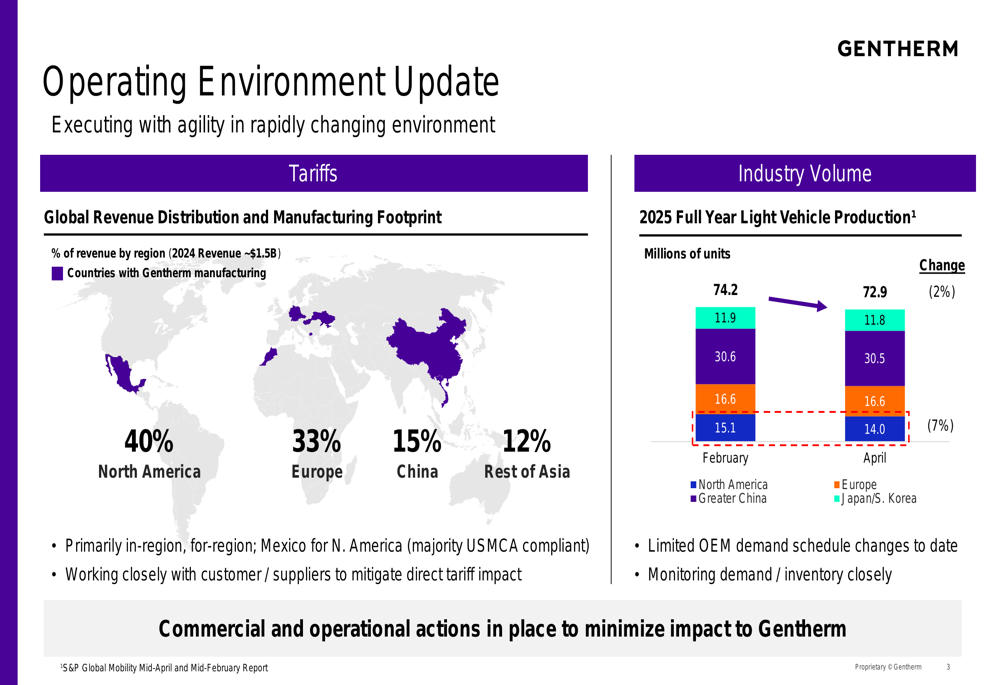

Gentherm faces significant headwinds in its operating environment, particularly regarding global light vehicle production forecasts and tariff impacts. The company’s presentation revealed that 2025 full-year light vehicle production estimates have decreased by 2% since February, with North American production forecasts showing the most significant decline of 7%.

The following chart illustrates these production forecast changes:

The company emphasized its "in-region, for-region" manufacturing approach, with Mexico serving as its primary production base for North American customers. This strategy may help mitigate some tariff impacts, though the company acknowledged it is working closely with customers and suppliers to address these challenges.

Gentherm’s global revenue distribution shows North America accounting for 40% of sales, Europe for 33%, China for 15%, and the rest of Asia for 12%, making the North American production slowdown particularly concerning for near-term results.

Strategic Initiatives

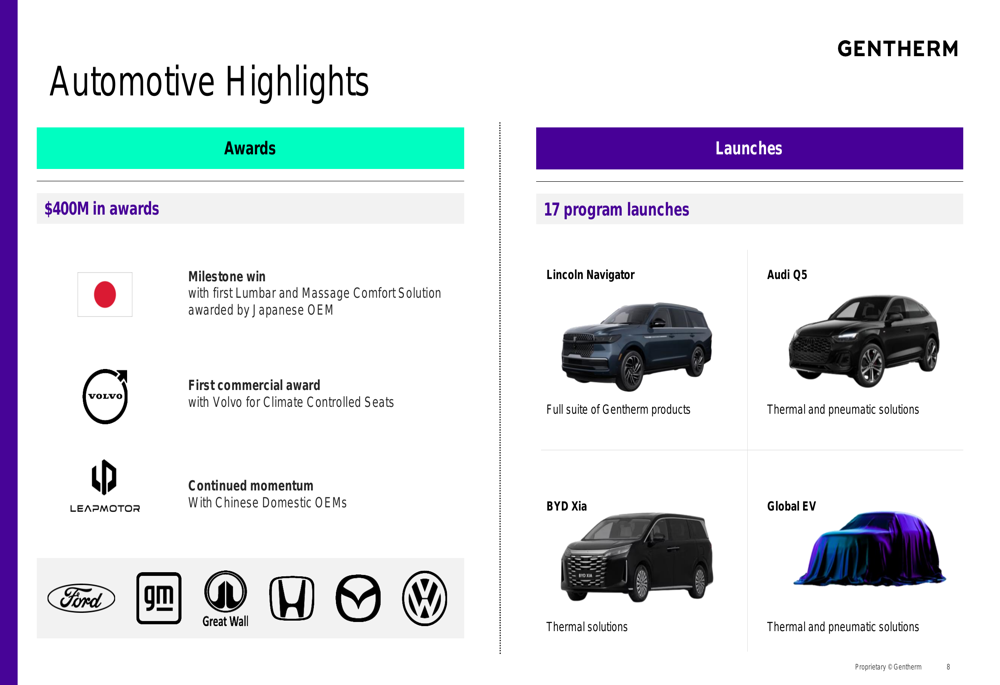

Despite near-term challenges, Gentherm continues to advance several strategic initiatives. The company completed 17 program launches across 11 OEMs during the quarter, including models such as the Lincoln Navigator (ELI:NVGR), Audi Q5, and BYD (SZ:002594) Xia.

The company’s automotive highlights showcase these achievements:

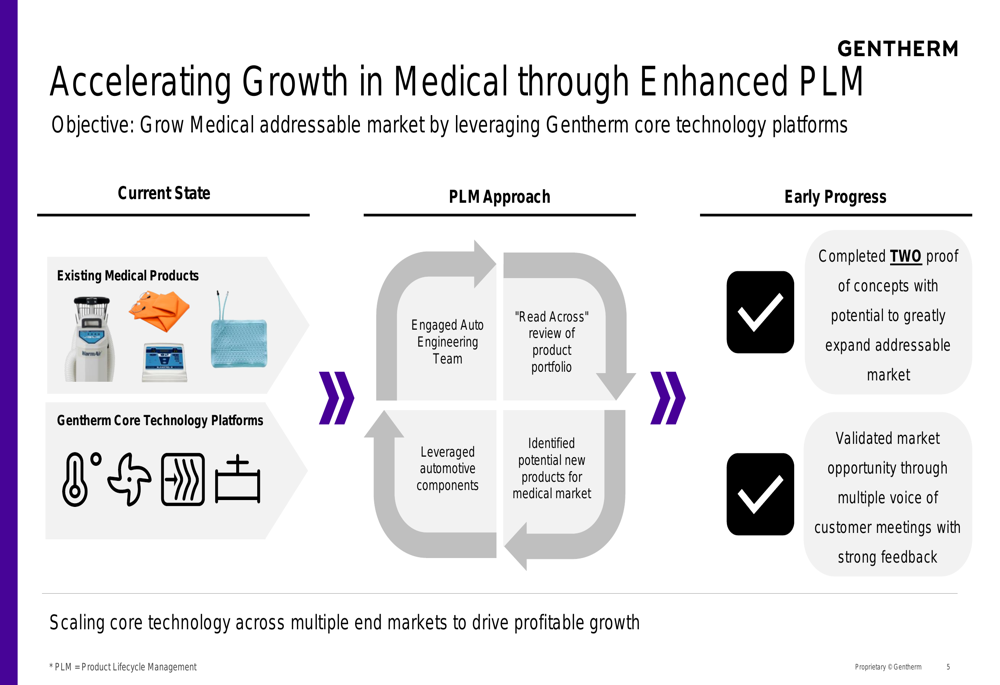

Particularly promising is Gentherm’s medical segment, which grew 6% excluding foreign exchange impacts. The company is accelerating growth in this sector through enhanced Product Lifecycle Management (PLM), leveraging its automotive engineering expertise to identify new medical market opportunities.

The medical growth strategy is illustrated in this diagram:

Management reported completing two proofs of concept and validating market opportunities through customer meetings. This diversification strategy could provide growth avenues beyond the cyclical automotive industry.

Financial Outlook

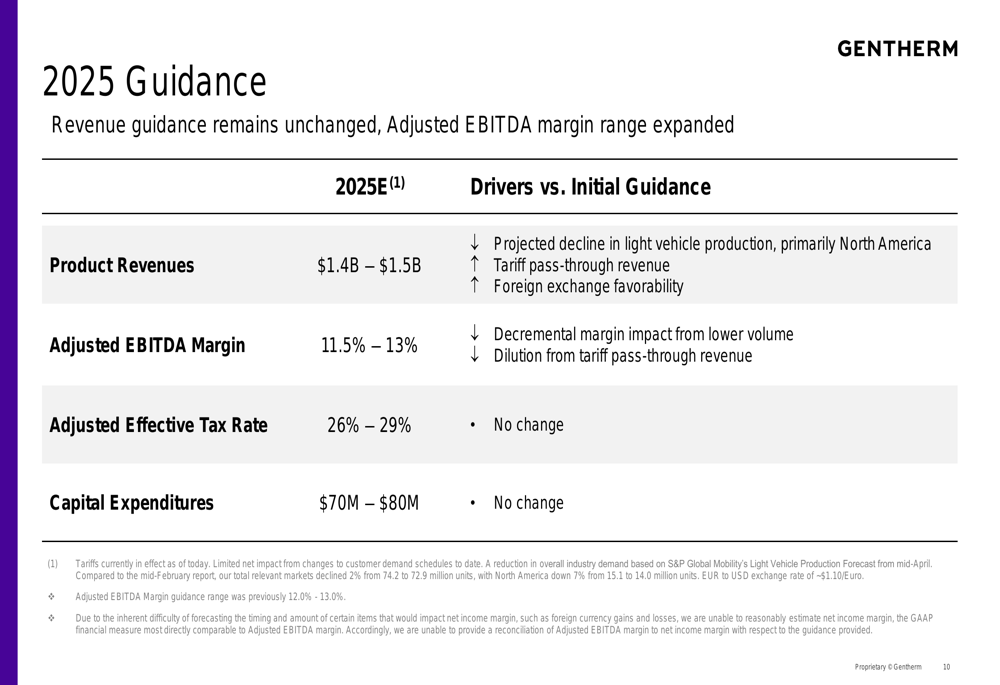

Gentherm maintained its 2025 revenue guidance of $1.4 billion to $1.5 billion but expanded its adjusted EBITDA margin range to 11.5% - 13%, suggesting increased uncertainty about profitability. The company cited several factors affecting its outlook, including the projected decline in light vehicle production, particularly in North America, and dilution from tariff pass-through revenue.

The guidance details are presented in this table:

Capital expenditures are expected to remain between $70 million and $80 million for the year, with the company noting it is hard to forecast the timing and amount of certain items that would impact net income margin.

This cautious outlook follows a pattern seen in the previous quarter, where Gentherm’s results fell significantly short of expectations. The expanded EBITDA margin range suggests management is preparing for potential continued volatility in the operating environment.

Despite these challenges, the company emphasized its strong financial position with a net leverage ratio of approximately 0.5x and its commitment to efficient capital deployment to drive shareholder value. However, the significant premarket stock decline indicates investors remain concerned about Gentherm’s ability to navigate the current challenging automotive production environment while maintaining profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.