Gold prices dip as December rate cut bets wane; economic data in focus

Introduction & Market Context

Gestamp Automocion (BME:GEST) reported its first half 2025 results on July 28, showcasing record second-quarter profitability despite facing revenue headwinds. The Spanish auto parts manufacturer saw its stock rise slightly by 0.25% to €3.25 following the presentation, as investors responded positively to margin improvements and strong free cash flow generation despite top-line pressure.

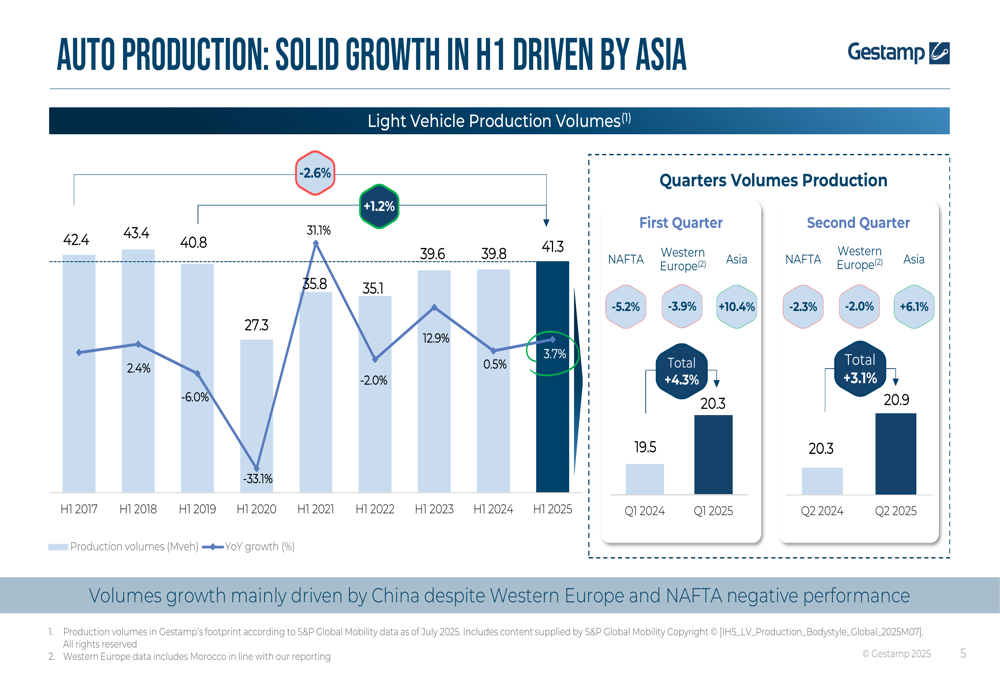

The global automotive market showed modest growth in the first half of 2025, with light vehicle production increasing by 1.2% year-over-year to 41.3 million vehicles. This growth was primarily driven by Asia, while Western Europe and North America experienced production declines.

Financial Performance Highlights

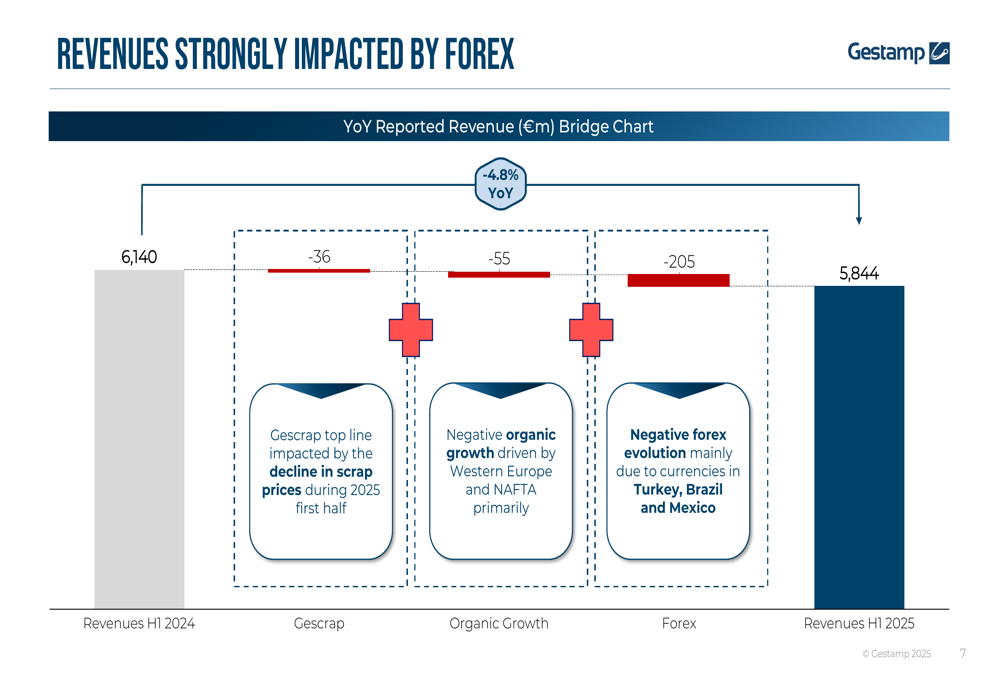

Gestamp reported H1 2025 revenues of €5,844 million, representing a 4.8% decrease compared to the same period last year. This decline was attributed to negative forex impact (€205 million), primarily from currencies in Turkey, Brazil, and Mexico, as well as negative organic growth (€55 million) mainly in Western Europe and NAFTA regions.

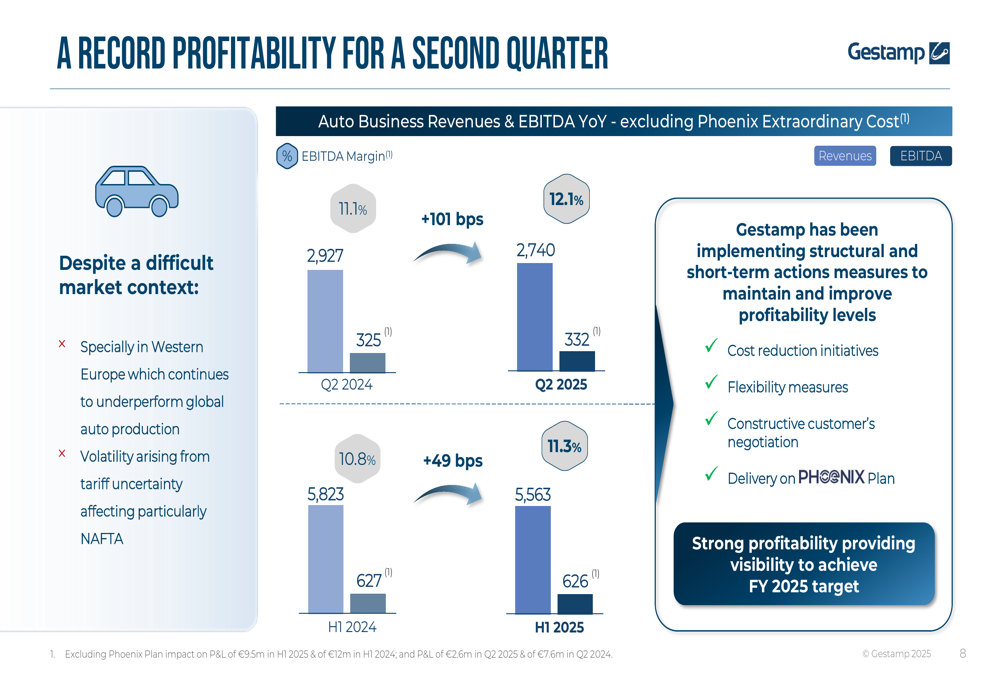

Despite the revenue decline, Gestamp achieved a record profitability for a second quarter. The company’s EBITDA margin for Q2 2025 reached 12.1% (excluding Phoenix Plan extraordinary costs), representing a 101 basis point improvement compared to Q2 2024. For the first half overall, EBITDA remained stable at €626 million (excluding Phoenix costs), with margin expanding to 11.3% from 10.8% in H1 2024.

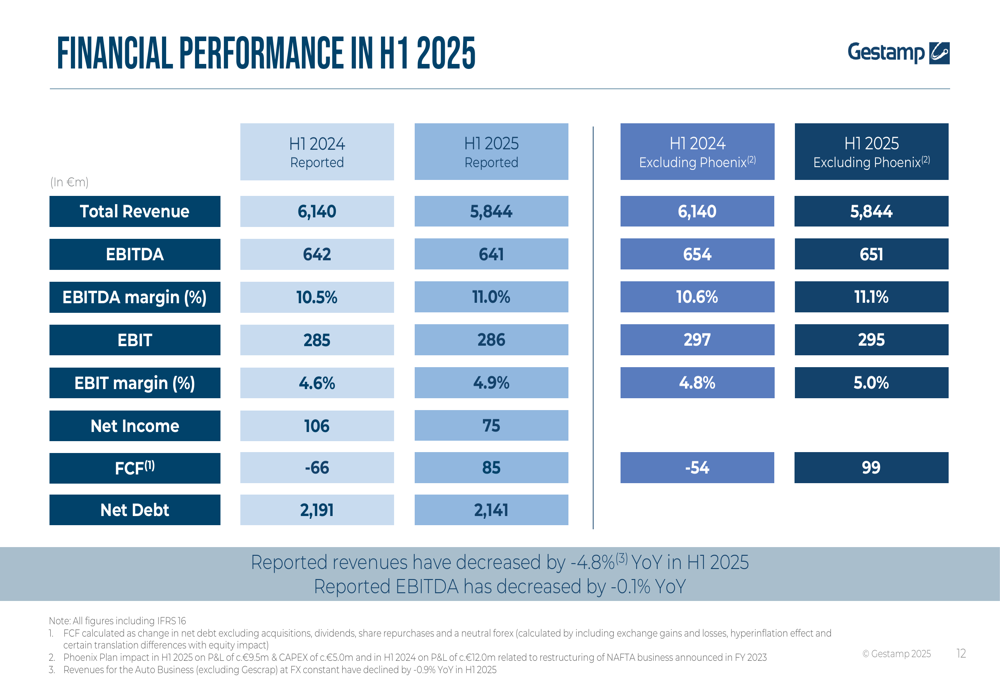

The company’s financial performance summary shows that while revenue declined, profitability metrics improved across the board. Reported EBITDA for H1 2025 was €641 million with an 11.0% margin, compared to €642 million and 10.5% in H1 2024. Net income decreased to €75 million from €106 million in the prior year.

Regional Analysis

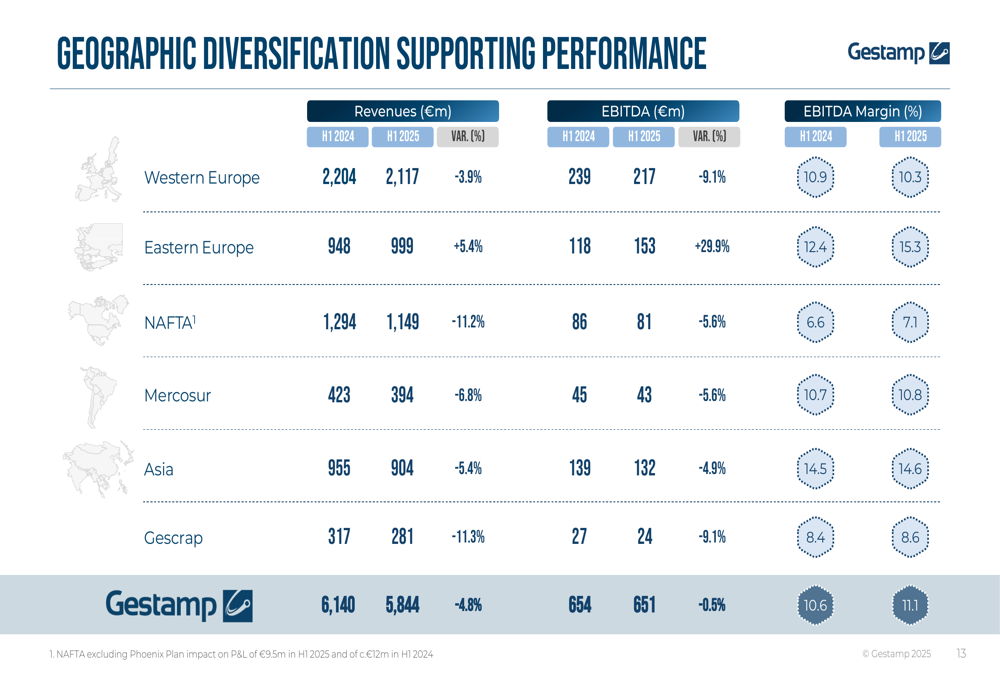

Gestamp’s geographic diversification proved valuable in offsetting regional challenges. Eastern Europe emerged as the standout performer, with revenues increasing by 5.4% to €999 million and EBITDA surging 29.7% to €153 million, resulting in a robust 15.3% margin.

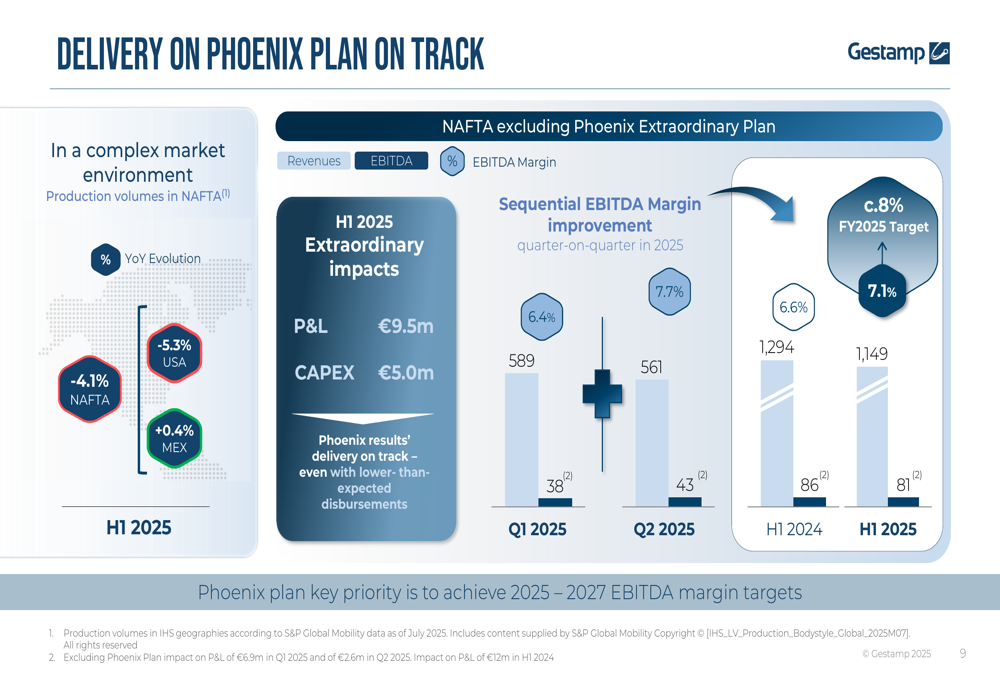

Western Europe, the company’s largest market, saw revenues decline by 4.0% to €2,117 million, with EBITDA falling 9.2% to €217 million. NAFTA (North America) experienced the steepest revenue decline of 11.2% to €1,149 million, though EBITDA margin improved to 7.1% from 6.6% as the Phoenix restructuring plan began to yield results.

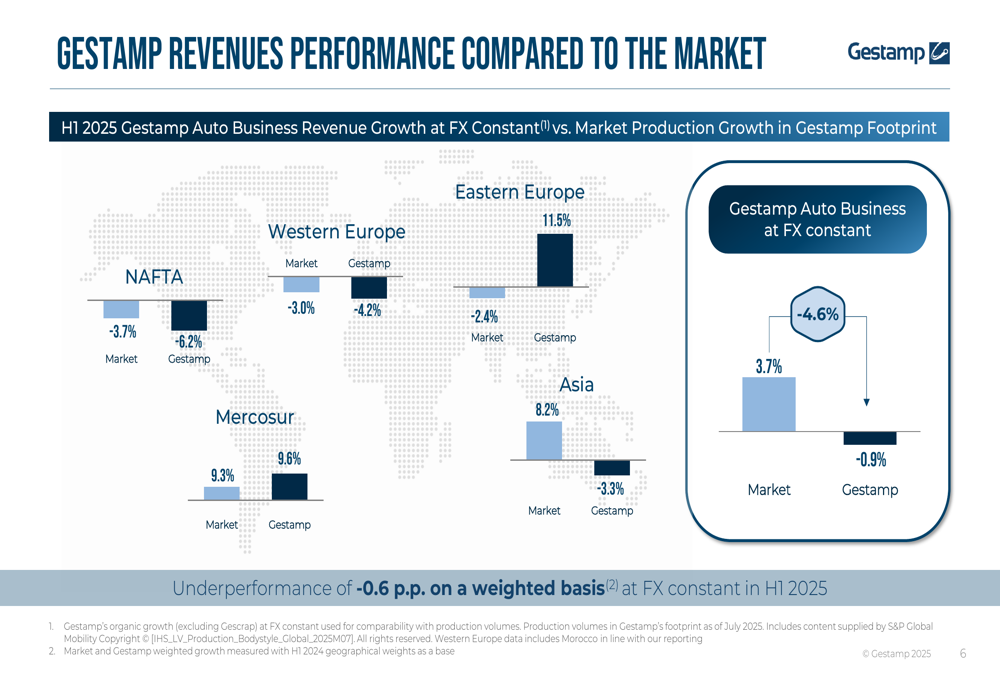

The company’s performance relative to the market varied by region. In Mercosur (South America), Gestamp outperformed the market with 9.6% growth versus 9.3% market growth. However, the company underperformed in NAFTA (-6.2% vs. -3.7% market), Western Europe (-4.2% vs. -3.0% market), and most significantly in Asia (-3.3% vs. 8.2% market growth).

Cash Flow and Balance Sheet

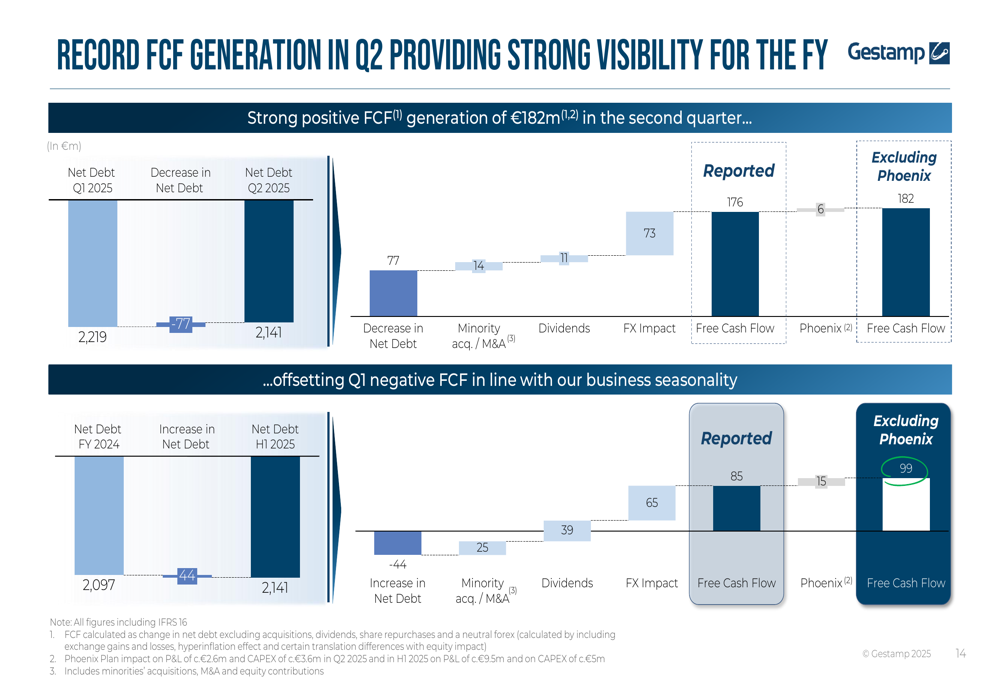

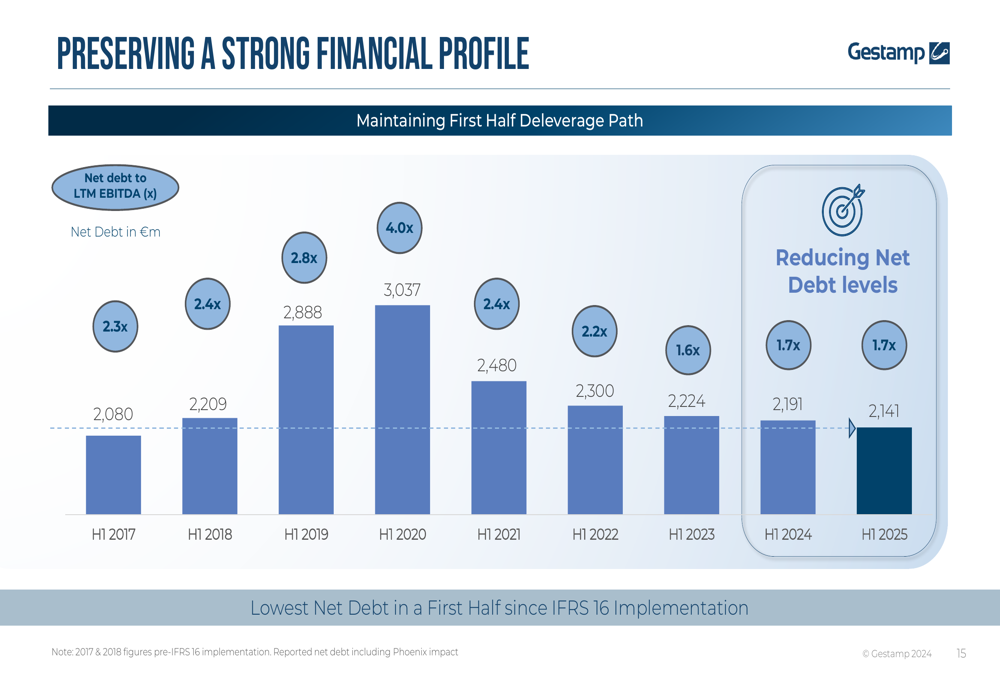

A standout achievement in Gestamp’s H1 2025 results was the record free cash flow generation of €182 million in the second quarter (excluding Phoenix Plan impacts). This strong performance helped reduce net debt to €2,141 million, down from €2,219 million at the end of Q1 2025 and €2,191 million in H1 2024.

The company has maintained its deleverage path, with net debt to LTM EBITDA ratio stable at 1.7x. Gestamp highlighted that this represents the lowest net debt level in a first half since IFRS 16 implementation.

Strategic Initiatives

Gestamp is executing two key strategic initiatives to strengthen its financial position. First, the Phoenix Plan targeting NAFTA operations is showing progress, with EBITDA margin in the region improving from 6.4% in Q1 2025 to 7.7% in Q2 2025. The plan incurred €9.5 million in extraordinary costs in H1 2025.

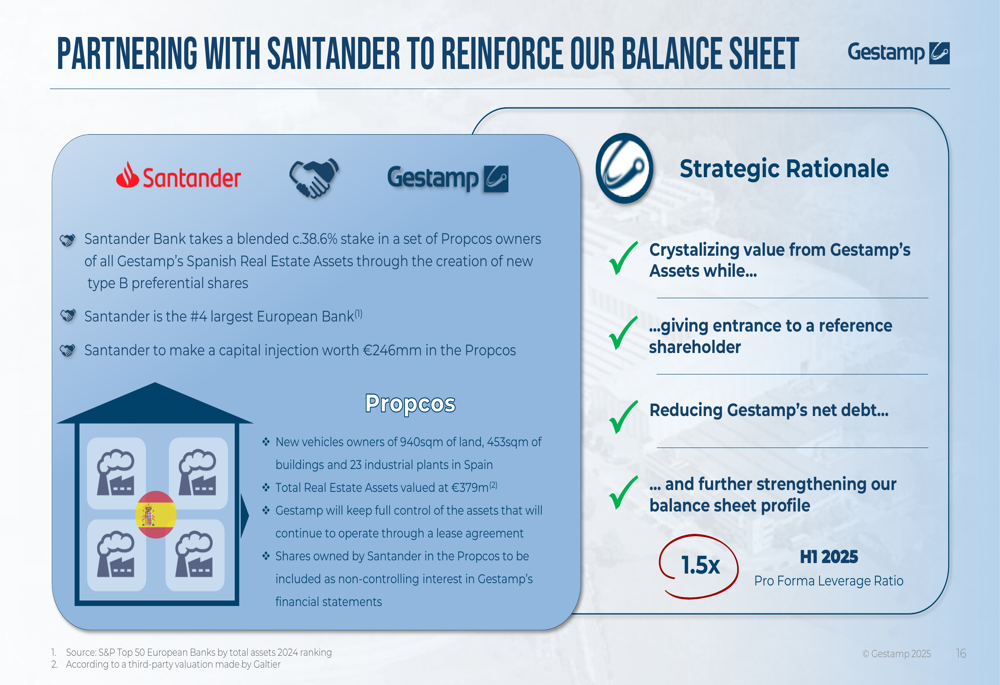

Second, Gestamp announced a significant partnership with Santander (BME:SAN) Bank, which will take a 38.6% stake in a set of property companies owning all of Gestamp’s Spanish real estate assets. This transaction involves a capital injection of €246 million from Santander, which will reduce Gestamp’s net debt and strengthen its balance sheet, bringing the pro forma leverage ratio to 1.5x for H1 2025.

Outlook and Guidance

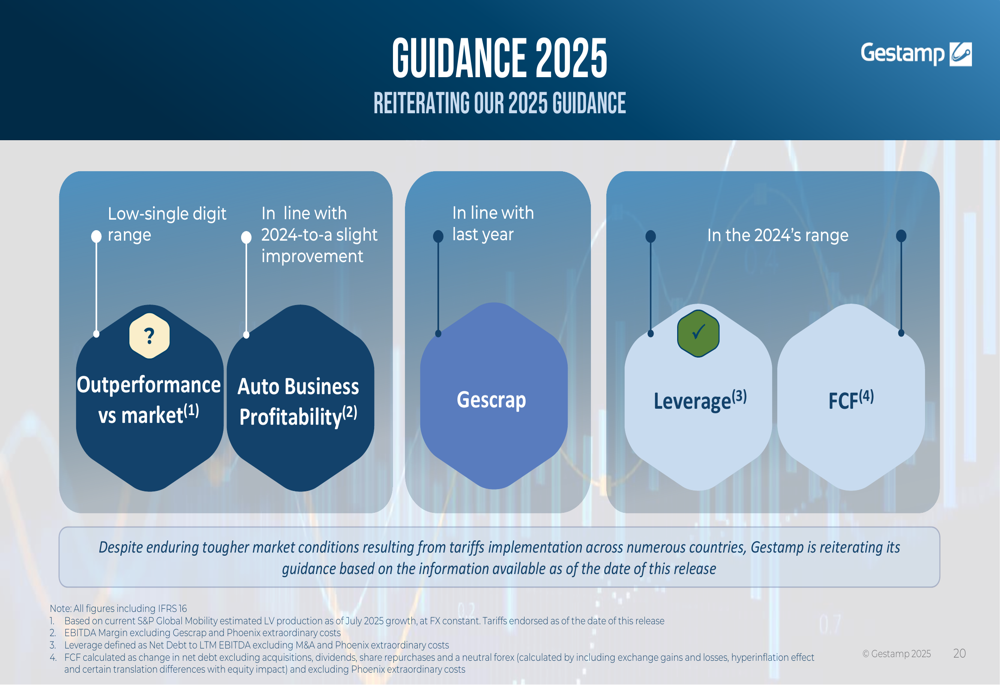

Despite market uncertainties, including potential impacts from tariff implementations across numerous countries, Gestamp reiterated its full-year 2025 guidance. The company expects:

- Low-single digit range outperformance versus the market

- Auto business profitability in line with 2024 to a slight improvement

- Gescrap performance in line with last year

- Leverage and free cash flow in the 2024 range

For the longer term, Gestamp outlined its 2027 strategic pillars, focusing on being a trusted partner supplier, technology and innovation differentiation, growth ambition, operational excellence, pioneering the circular economy, profitable growth, and maintaining a disciplined balance sheet profile.

Executive Summary

Gestamp’s H1 2025 results demonstrate the company’s ability to enhance profitability and generate strong cash flow despite revenue challenges. The record Q2 EBITDA margin of 12.1% and significant free cash flow generation of €182 million highlight the effectiveness of cost control measures and operational improvements.

The strategic partnership with Santander Bank and ongoing implementation of the Phoenix Plan in North America position Gestamp to further strengthen its financial profile. While regional performance varies significantly, with Eastern Europe showing robust growth and NAFTA and Western Europe facing headwinds, the company’s geographic diversification continues to provide resilience.

As Gestamp navigates a challenging automotive market environment, its focus on profitability enhancement, balance sheet strength, and strategic initiatives provides a solid foundation for sustainable long-term value creation for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.