Interactive Brokers shares jump as it secures spot in S&P 500

Introduction & Market Context

Getty Realty Corporation (NYSE:GTY), a leading owner of convenience and automotive retail properties, presented its Q1 2025 corporate profile highlighting portfolio stability despite missing earnings expectations. The company’s stock fell 2.42% to $27.82 on April 24, 2025, following its April 23 earnings release that showed an EPS miss of $0.25 against forecasts of $0.3202, despite revenue slightly exceeding expectations at $50.6 million.

The REIT, which owns 1,119 properties across 42 states, emphasized its resilience amid macroeconomic uncertainty while maintaining high occupancy rates and consistent rent collections. However, investors appeared more focused on the earnings shortfall, with the stock now trading closer to its 52-week low of $25.70 than its high of $33.85.

Portfolio Performance Highlights

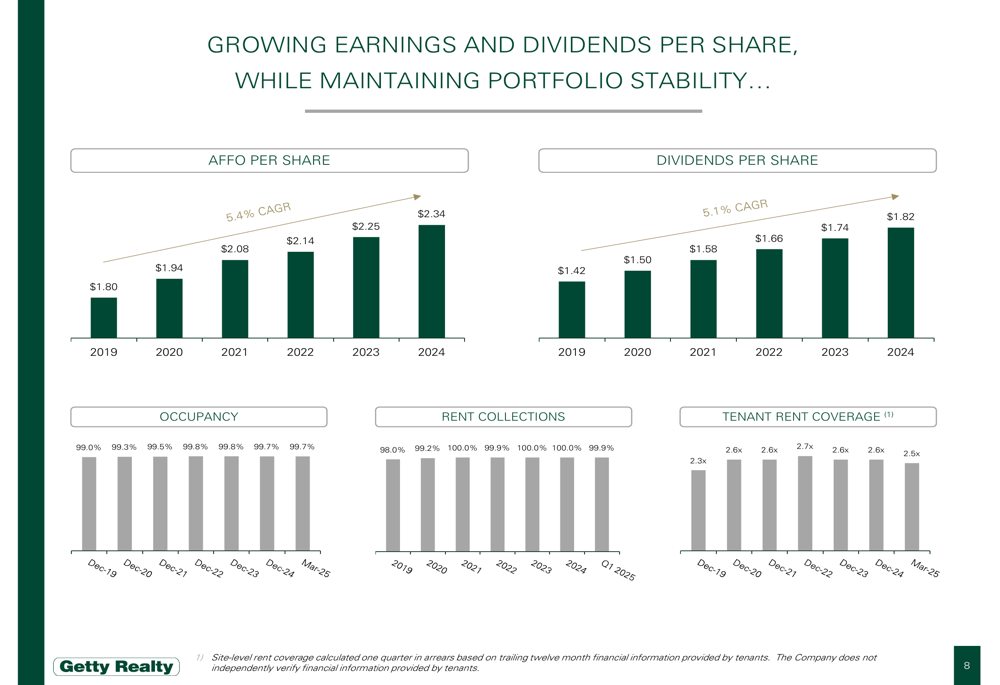

Getty Realty’s presentation emphasized the stability of its portfolio, maintaining a 99.7% occupancy rate and 10.0-year weighted average lease term (WALT). The company reported $199 million in annualized base rent (ABR) with 99.9% rent collections and 2.5x tenant rent coverage, demonstrating the durability of its tenant relationships despite market challenges.

As shown in the following chart, Getty has maintained consistent growth in both AFFO and dividends per share while preserving portfolio stability metrics:

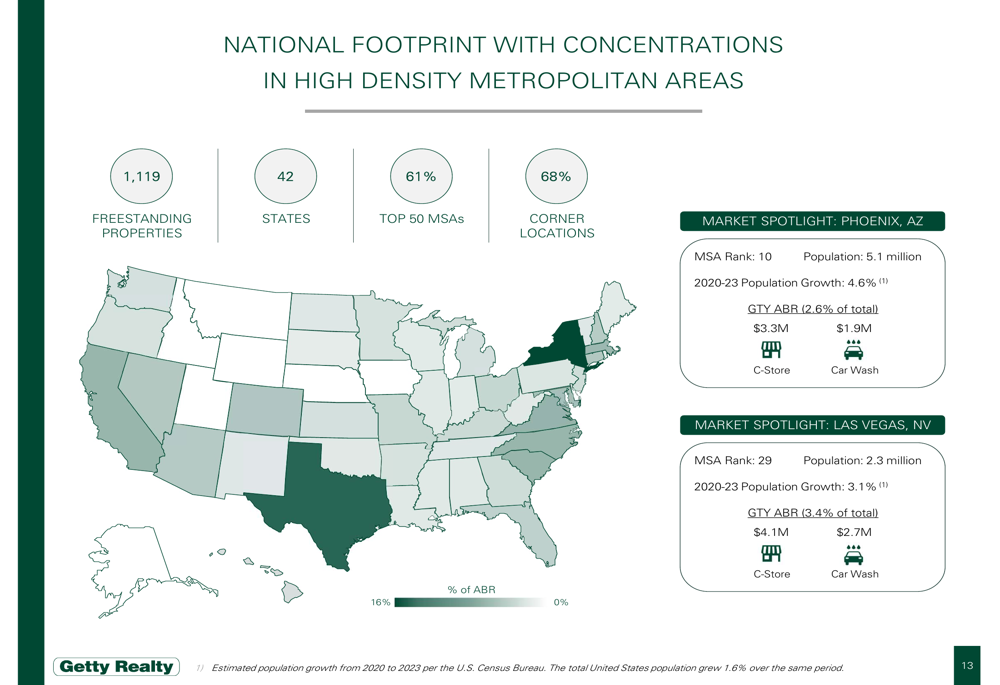

The company’s portfolio is strategically positioned in high-density metropolitan areas, with 61% of properties located in the top 50 MSAs and 68% at corner locations. This geographic focus supports the company’s emphasis on properties with strong visibility, easy access, and high traffic counts.

The following map illustrates Getty’s national footprint with concentrations in key markets:

Detailed Financial Analysis

Getty reported Q1 2025 AFFO of $33.8 million, up 7.6% year-over-year, with AFFO per share increasing 3.5% to $0.59. Despite this growth, the company’s EPS of $0.25 fell short of analyst expectations, contributing to the stock’s decline following the earnings release.

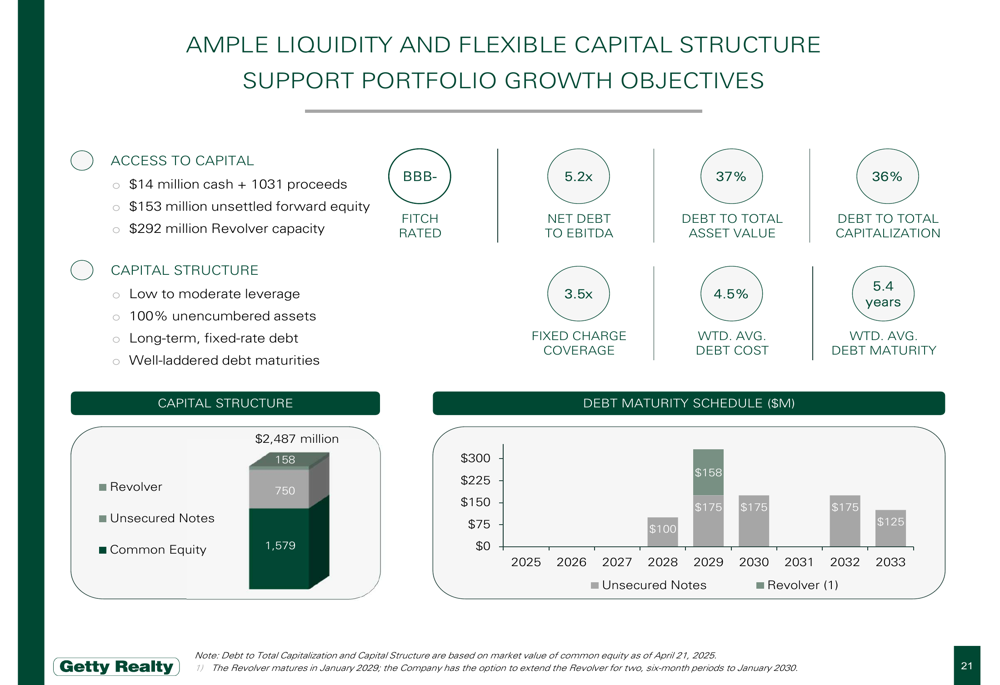

The company maintains a conservative balance sheet with 5.2x net debt to EBITDA (4.4x pro forma for unsettled forward equity), a BBB- Fitch rating, and no debt maturities until June 2028. Getty highlighted its ample liquidity of over $450 million, including $14 million in cash and 1031 proceeds, $153 million in unsettled forward equity, and $292 million in revolver capacity.

The following chart details Getty’s capital structure and debt maturity schedule:

Year-to-date, Getty has invested $17.3 million at a 7.7% initial cash yield, acquiring eight drive-thru QSRs, one express tunnel car wash, and one auto service center. The company has more than $110 million of investments under contract, with the majority expected to close in the next 9-12 months.

Strategic Initiatives

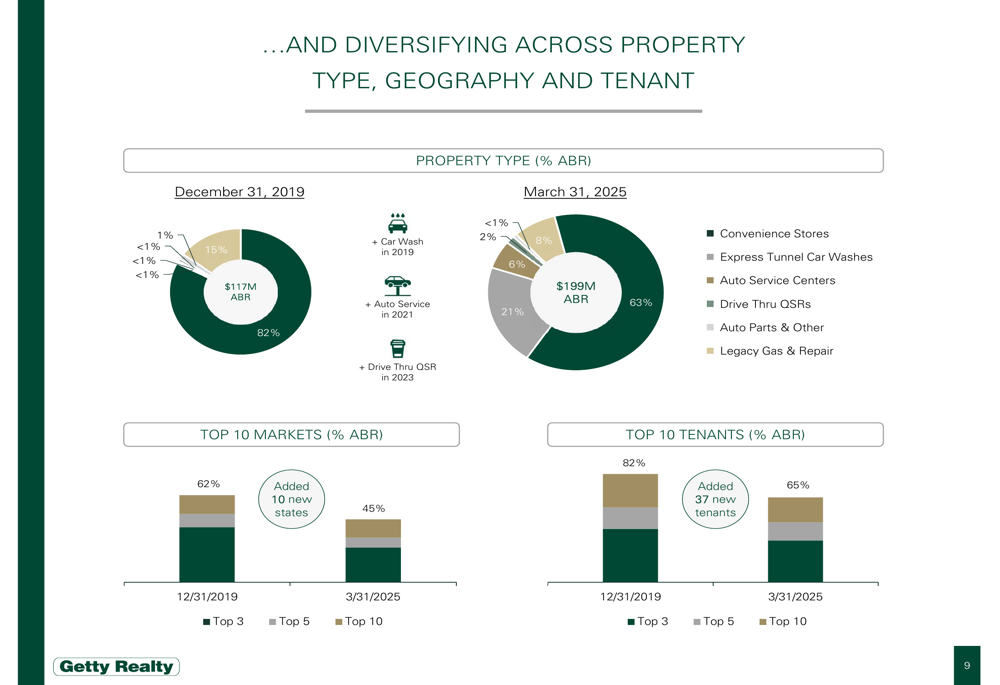

Getty’s presentation highlighted its ongoing diversification strategy across property types, geography, and tenants. Since December 2019, the company has reduced concentration in its top 10 markets from 62% to 45% of ABR while expanding into 10 new states. Similarly, concentration in the top 10 tenants decreased from 82% to 65% of ABR as the company added 37 new tenants.

The following chart illustrates this diversification trend:

The company’s property portfolio has also evolved, with convenience stores representing 63.2% of ABR, express tunnel car washes 20.8%, auto service centers 7.8%, and drive-thru QSRs 8.2%. This diversification helps mitigate sector-specific risks while maintaining focus on essential, recession-resistant retail categories.

Getty’s tenant base includes multi-store operators with national and regional brands across various stages of growth. The company emphasizes credit enhancements through sector selection, site selection, and lease structure, with 83% of ABR derived from unitary leases.

The following image showcases Getty’s diverse tenant portfolio:

Competitive Industry Position

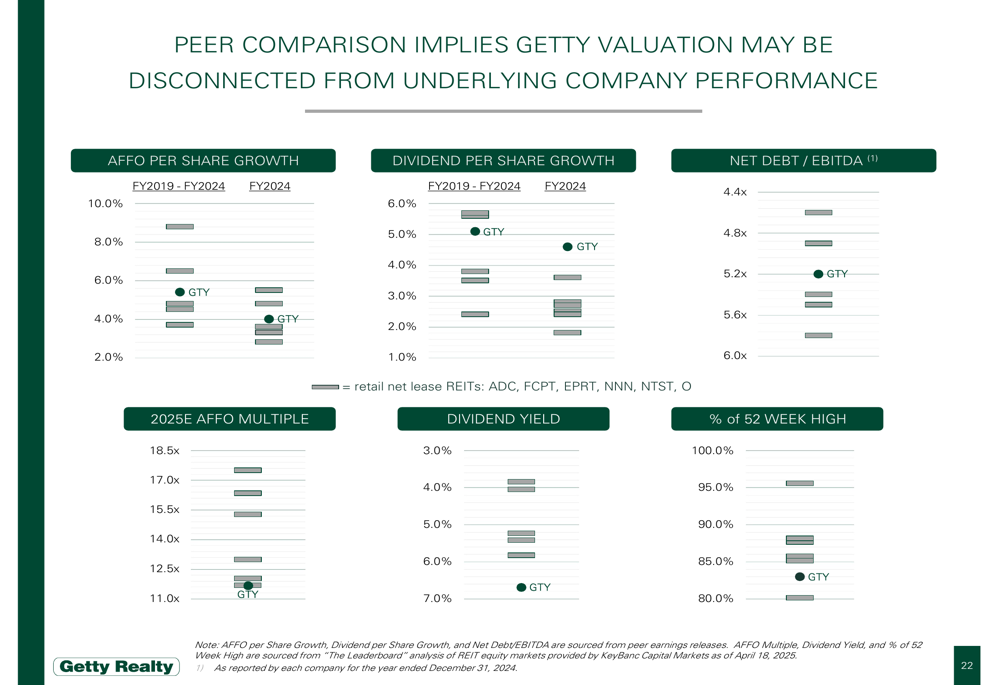

Getty’s presentation included a peer comparison suggesting its valuation may be disconnected from underlying company performance. Despite delivering competitive AFFO per share growth and dividend growth from 2019 to 2024, Getty trades at a discount to peers on several metrics.

The following chart compares Getty to industry peers including ADC, FCPT, EPRT, NNN, NTST, and O:

This valuation gap exists despite Getty’s 5.4% CAGR in AFFO per share and 5.1% CAGR in dividends per share from 2019 to 2024, competitive with or exceeding many peers. The company’s current dividend yield of 6.59% (according to recent data) is well above its 5-year average, potentially offering value to income-focused investors.

Forward-Looking Statements

Getty reaffirmed its full-year 2025 AFFO per share guidance of $2.38-$2.41 despite the Q1 earnings miss. The company’s investment pipeline includes $110 million in potential acquisitions, with 50% allocated to auto service and two-thirds directed toward development funding.

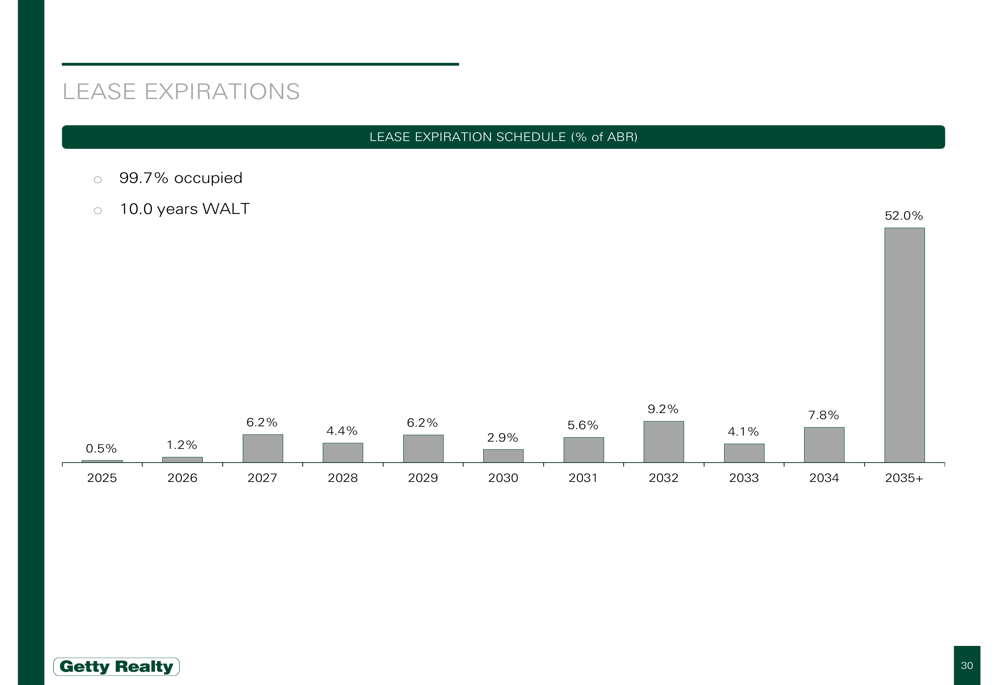

The company’s lease expiration schedule shows minimal near-term lease roll, with only 0.5% of ABR expiring in 2025 and 1.2% in 2026. The majority (52.0%) of leases expire in 2035 or later, providing long-term stability to the portfolio:

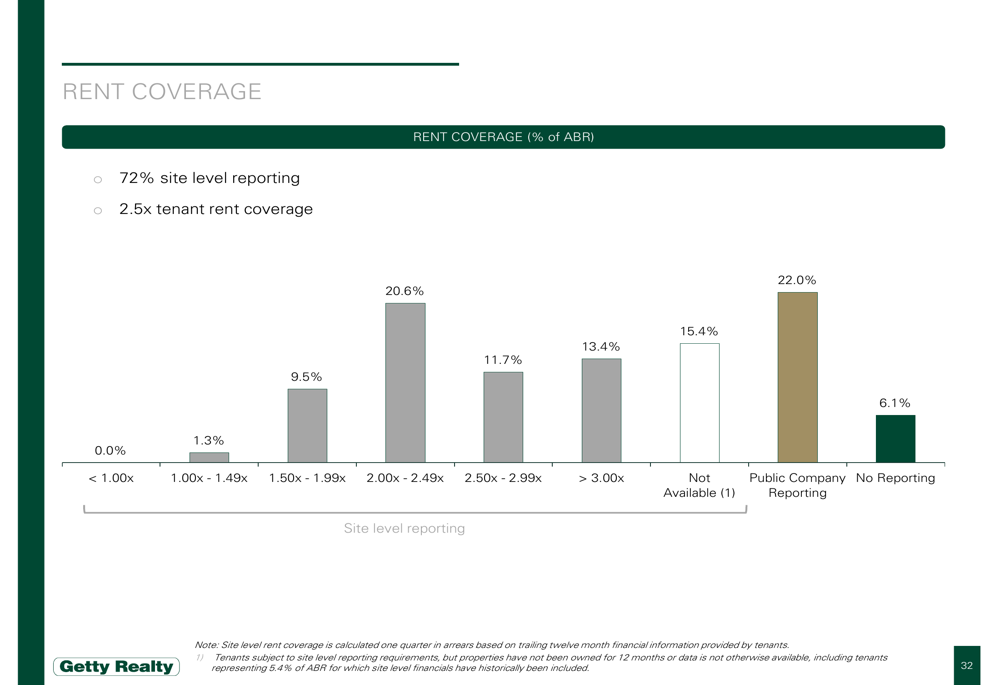

Getty also highlighted strong rent coverage across its portfolio, with 47.7% of ABR having rent coverage of 2.0x or higher, demonstrating the financial health of its tenant base:

During the earnings call, management addressed the ongoing resolution of the ZiPS car wash bankruptcy, expecting the situation to be resolved by the end of Q2 2025. CEO Christopher Constant emphasized the recession-resistant nature of Getty’s tenant businesses, while CFO Brian Dickman highlighted the company’s strong capital position.

Despite the EPS miss and subsequent stock decline, Getty’s presentation portrays a company with stable fundamentals, a diversified portfolio of essential retail properties, and a clear strategy for continued growth in a challenging market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.