Stock market today: S&P 500 rides Apple-led tech rally to close higher

Introduction & Market Context

Gibson Energy Inc . (TSX:GEI) reported strong second-quarter 2025 results, with earnings per share of $0.37 exceeding forecasts by 32.43% and revenue of $2.76 billion surpassing expectations by 57.71%. The company’s stock rose 1.41% following the announcement, closing at $24.80, and has continued its upward trend to reach $25.04 as of July 29, 2025.

In its Q2 2025 corporate presentation, Gibson Energy positions itself as a critical player in North American liquids infrastructure with 70 years of industry experience. The company emphasizes its strategic terminal assets and disciplined growth approach as key drivers of its recent performance and future prospects.

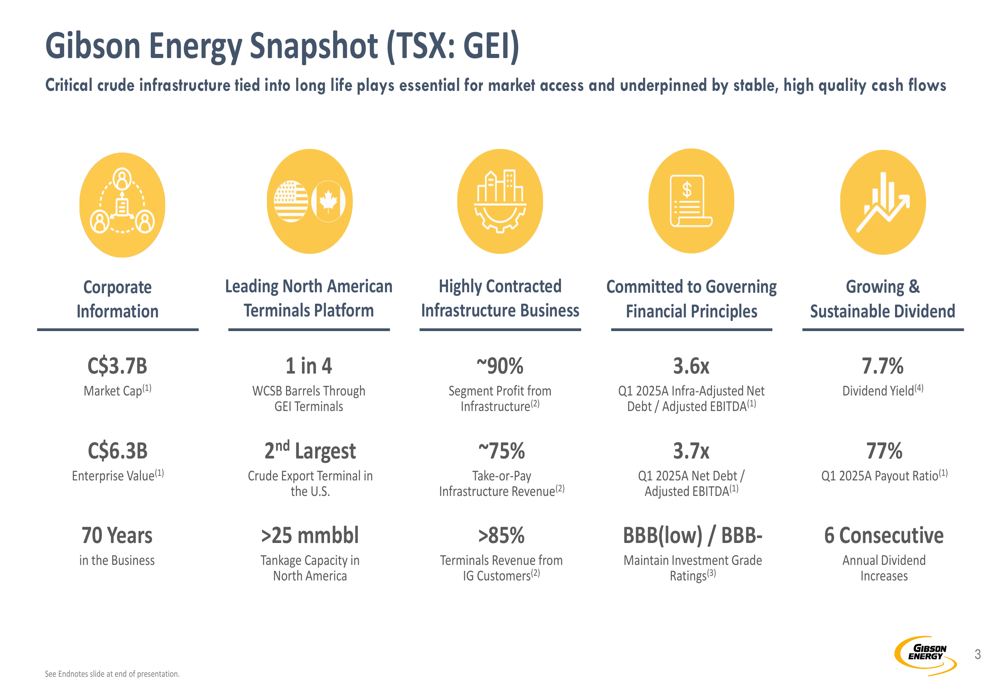

As shown in the following snapshot of Gibson Energy’s key metrics:

Gibson maintains a market capitalization of C$3.7 billion and enterprise value of C$3.6 billion. The company highlights that approximately 90% of its segment profit comes from infrastructure, with 75% of infrastructure revenue derived from take-or-pay contracts. Its strong dividend yield of 7.7% is supported by six consecutive annual dividend increases, with a Q1 2025 payout ratio of 77%.

Strategic Infrastructure Position

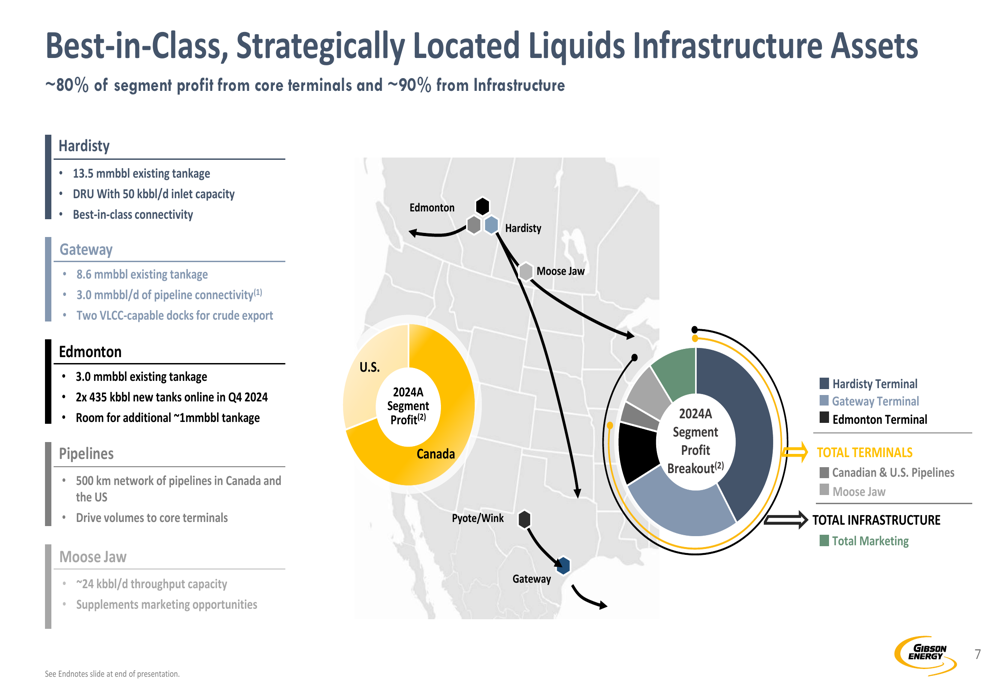

Gibson Energy’s core strategy revolves around its strategically located terminal assets across North America, which handle over 25 million barrels of total terminal capacity. The company’s infrastructure footprint includes three key terminals: Hardisty (13.5 million barrels), Edmonton (3.0 million barrels), and Gateway (8.6 million barrels).

The company’s infrastructure assets are illustrated in the following slide:

During the earnings call, CEO Curtis Filton emphasized the strategic advantage of the Gateway terminal, noting that "Ingleside is the most cost-effective place to export crude out of the U.S." This terminal, acquired in 2023, represents Gibson’s expansion into U.S. export markets and positions the company to benefit from growing Permian Basin production and increasing global demand for U.S. crude exports.

Gibson’s Hardisty terminal maintains a dominant position in Western Canada, handling one in four barrels in the Western Canadian Sedimentary Basin (WCSB). The company’s Edmonton terminal recently completed two new 435,000-barrel tanks in Q4 2024 to support Trans Mountain Expansion (TMX) shippers.

Growth Strategy

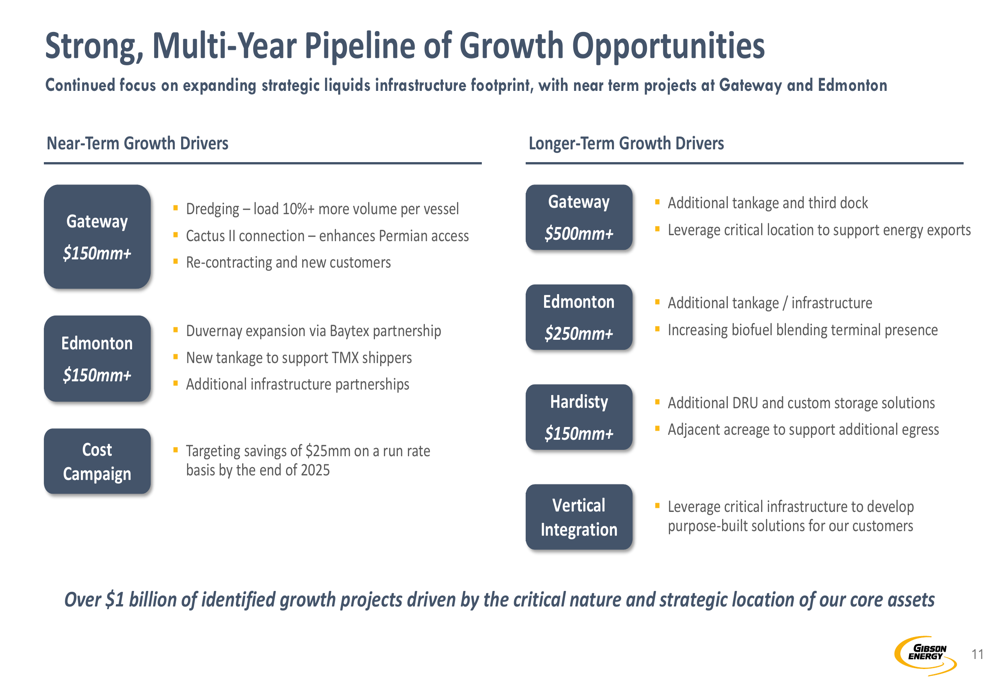

Gibson Energy’s presentation outlines a robust pipeline of growth opportunities exceeding $1 billion, focused on expanding its strategic liquids infrastructure footprint. Near-term growth is centered on the Gateway terminal and Edmonton facilities, while longer-term initiatives target additional capacity across all three core terminals.

The following slide details Gibson’s multi-year growth pipeline:

Near-term growth drivers include Gateway terminal enhancements such as dredging to load 10% more volume per vessel, Cactus (NYSE:WHD) II pipeline connection to improve Permian access, and customer re-contracting initiatives totaling over $150 million in investments. At Edmonton, the company is pursuing Duvernay expansion through a Baytex partnership and additional infrastructure to support TMX shippers, representing another $150+ million opportunity.

Gibson is also implementing a cost reduction campaign targeting $25 million in annual savings by the end of 2025. During the earnings call, Filton confirmed, "We’re on track to exceed the $25,000,000 target."

Financial Performance & Capital Allocation

Gibson Energy’s Q2 2025 financial performance demonstrated the resilience of its business model despite some year-over-year declines. While Adjusted EBITDA decreased by $13 million to $146 million and Distributable Cash Flow fell by $20 million to $81 million compared to Q2 2024, the company still significantly outperformed market expectations.

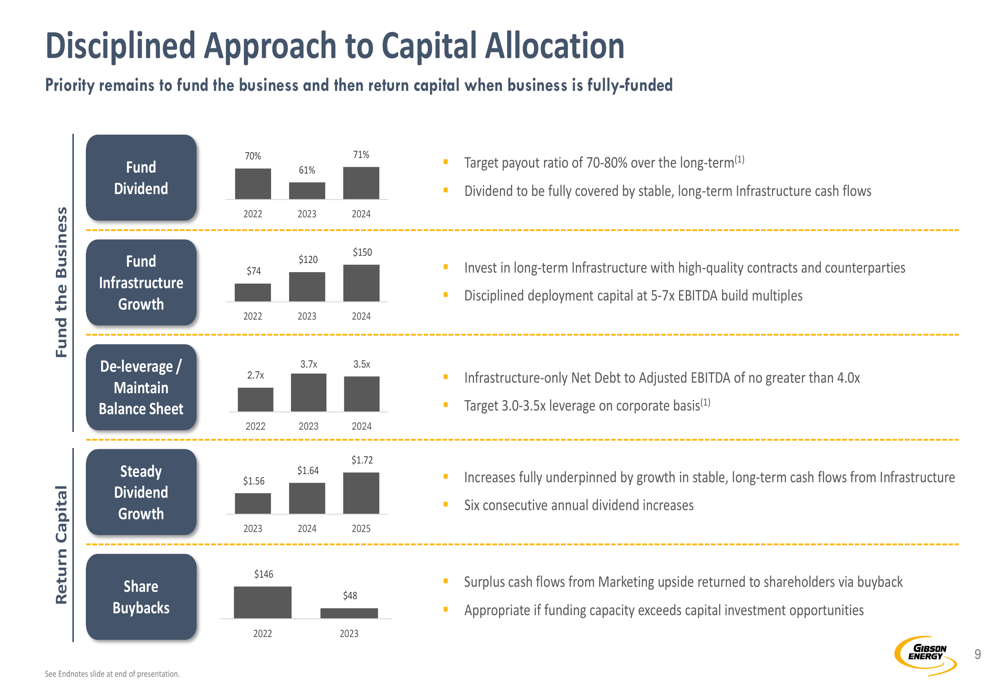

The company’s financial strategy emphasizes disciplined capital allocation, as illustrated in this slide:

Gibson prioritizes funding its dividend (targeting a 70-80% payout ratio), investing in infrastructure growth with 5-7x EBITDA build multiples, maintaining balance sheet strength, and returning surplus cash to shareholders through buybacks when appropriate. The current debt-to-EBITDA ratio stands at 4.0x, above the target range of 3.0-3.5x, but management expects to return to the target range by early 2026.

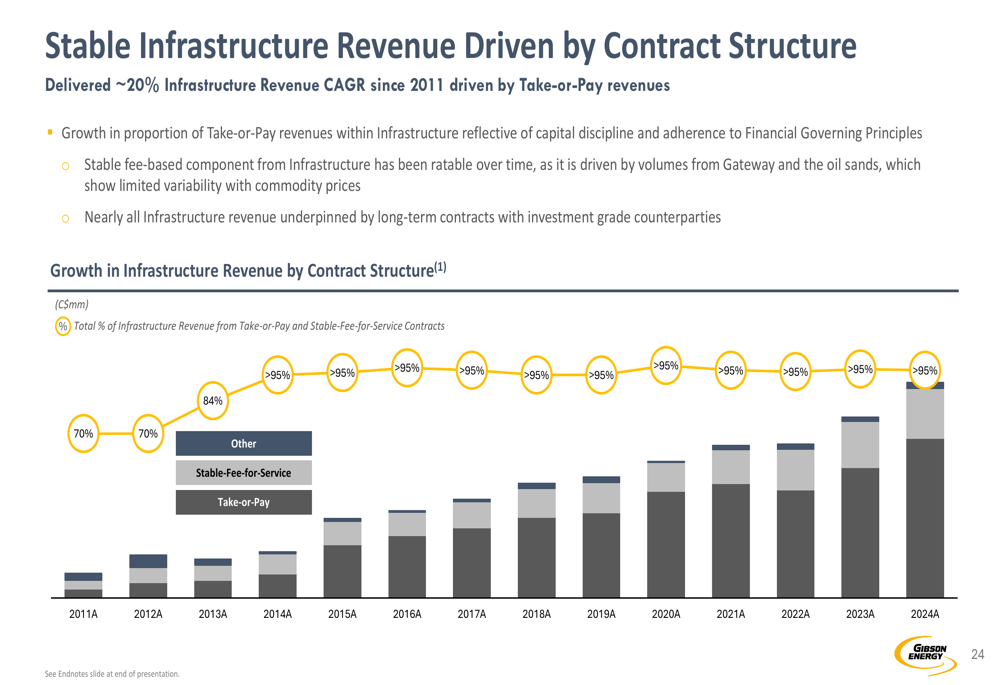

The stability of Gibson’s infrastructure revenue stream is a key strength, with over 95% of revenues coming from stable fee-for-service arrangements:

This revenue stability has supported consistent growth in shareholder returns, with the dividend per share growing at approximately 5% CAGR from 2019 to 2025. Gibson’s current dividend yield of 7.7% ranks among the highest in the S&P/TSX Composite Index.

Market Outlook & Challenges

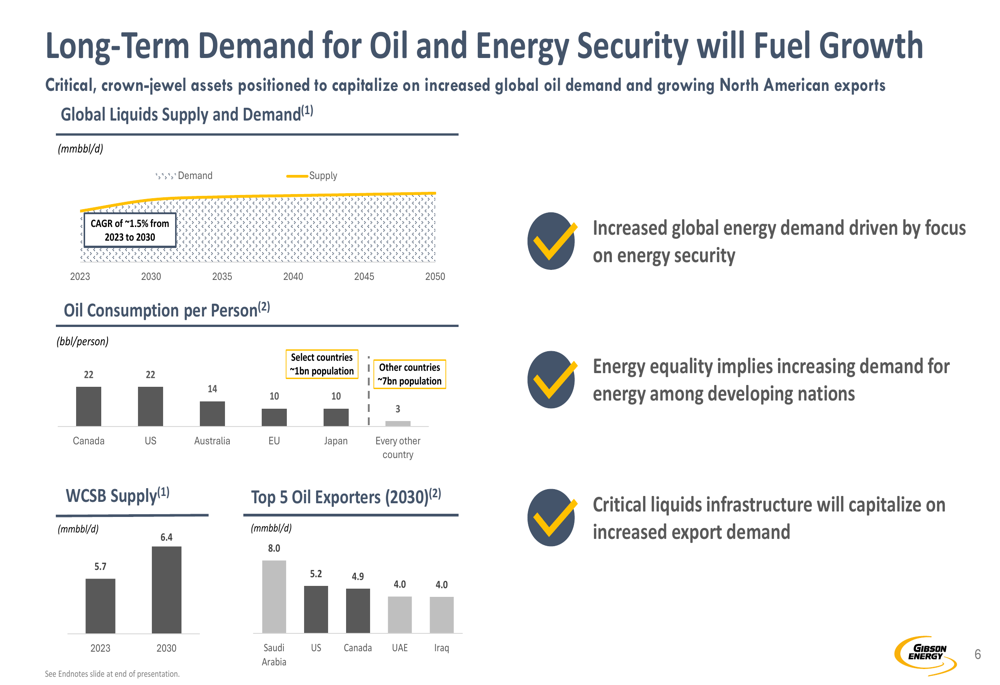

Gibson Energy’s presentation highlights favorable long-term market dynamics, including growing global oil demand (projected at ~1.5% CAGR from 2023 to 2030) and increasing North American export volumes. The company expects Western Canadian crude production to grow from 5.7 million barrels per day in 2023 to 6.4 million barrels per day by 2030.

The following slide illustrates these market trends:

While current market conditions include excess pipeline capacity due to the Trans Mountain Expansion (TMX) coming online in May 2024, Gibson expects this egress capacity to tighten by 2026-27, creating additional opportunities for its infrastructure and marketing segments.

Despite the positive long-term outlook, Gibson faces near-term challenges including a "muted marketing environment" due to low inventory levels and tight commodity differentials limiting storage opportunities. The company’s marketing segment guidance for 2025 is set between $20 million and $40 million, reflecting these market conditions.

ESG Performance

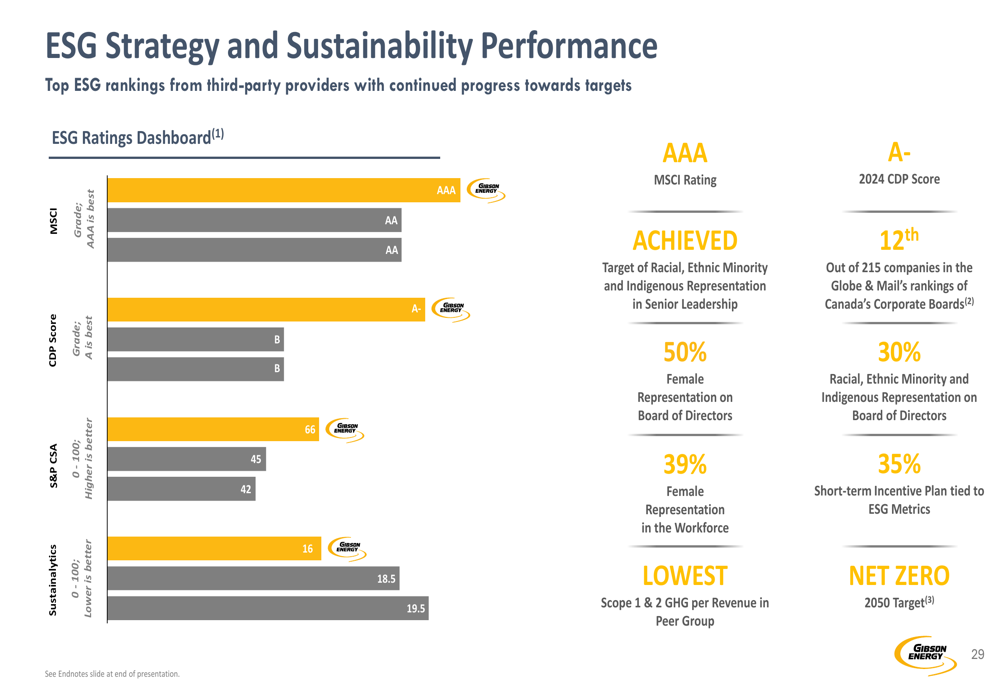

Gibson Energy emphasizes its commitment to environmental, social, and governance (ESG) principles, highlighting top rankings from third-party ESG providers:

The company has established sustainability targets for 2025 and 2030, focusing on reducing greenhouse gas emissions intensity and improving other environmental metrics. This ESG focus aligns with Gibson’s strategy to maintain its investment-grade credit ratings (currently BBB(low)/BBB-) and attract high-quality investors.

Conclusion

Gibson Energy’s Q2 2025 presentation and earnings results demonstrate the company’s strong position in North American liquids infrastructure and its ability to deliver results above market expectations. With a clear growth strategy focused on expanding its terminal capacity, particularly at the Gateway export terminal, Gibson is positioning itself to benefit from long-term growth in oil demand and exports.

While facing some near-term challenges in its marketing segment and elevated leverage ratios, the company’s stable infrastructure revenue stream, disciplined capital allocation approach, and attractive dividend yield provide a compelling investment case. Management’s focus on cost reduction and strategic growth initiatives suggests Gibson is well-positioned to navigate current market conditions while pursuing long-term value creation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.