Chip stocks fall with Nvidia after data center rev disappointment

Gilead Sciences Inc (NASDAQ:GILD) presented its first quarter 2025 financial results on April 24, showing 4% year-over-year growth in its base business despite a 4.19% decline in after-hours trading following the announcement.

Quarterly Performance Highlights

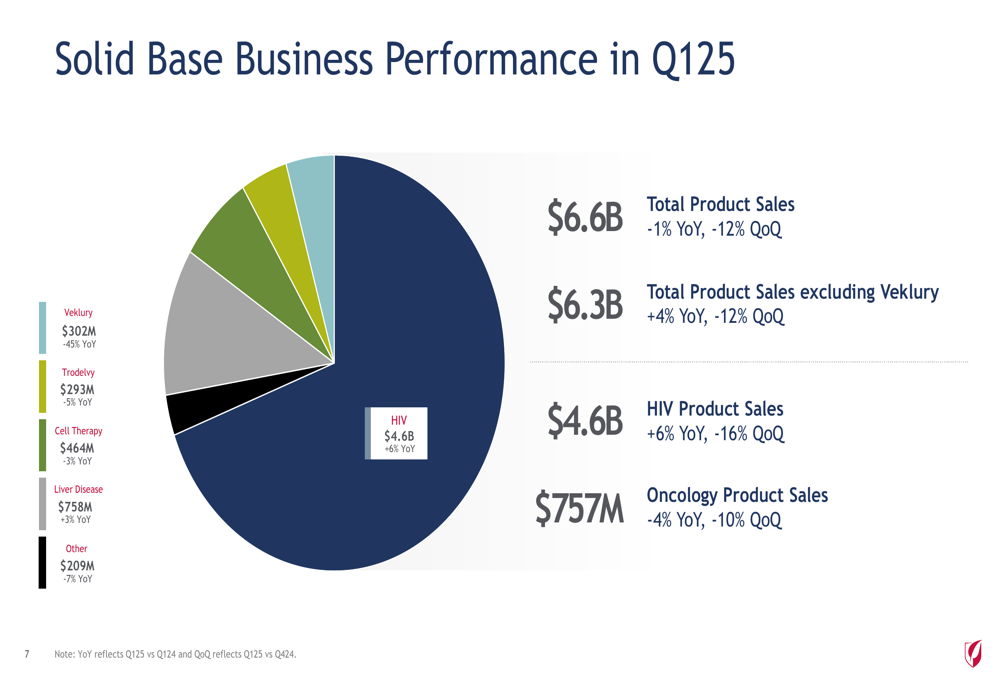

Gilead reported total product sales of $6.6 billion for Q1 2025, representing a 1% year-over-year decline. However, excluding Veklury (remdesivir), the company’s base business grew 4% year-over-year to $6.3 billion, demonstrating the underlying strength of its core portfolio amid declining COVID-19 treatment sales.

"We delivered strong execution across our business in the first quarter," said Daniel O’Day, Chairman and CEO of Gilead Sciences. "Our HIV franchise continues to perform well, with 6% growth year-over-year, while we maintain operating expense discipline to drive bottom line outperformance."

The company highlighted several key achievements in its presentation, including positive Phase 3 data for Trodelvy in combination with pembrolizumab for first-line PD-L1+ metastatic triple-negative breast cancer (mTNBC), EU approval for Livdelzi for primary biliary cholangitis (PBC), and promising Phase 1 data for once-yearly lenacapavir supporting plans for a Phase 3 trial in the second half of 2025.

As shown in the following breakdown of Gilead’s Q1 2025 revenue by product category:

Detailed Financial Analysis

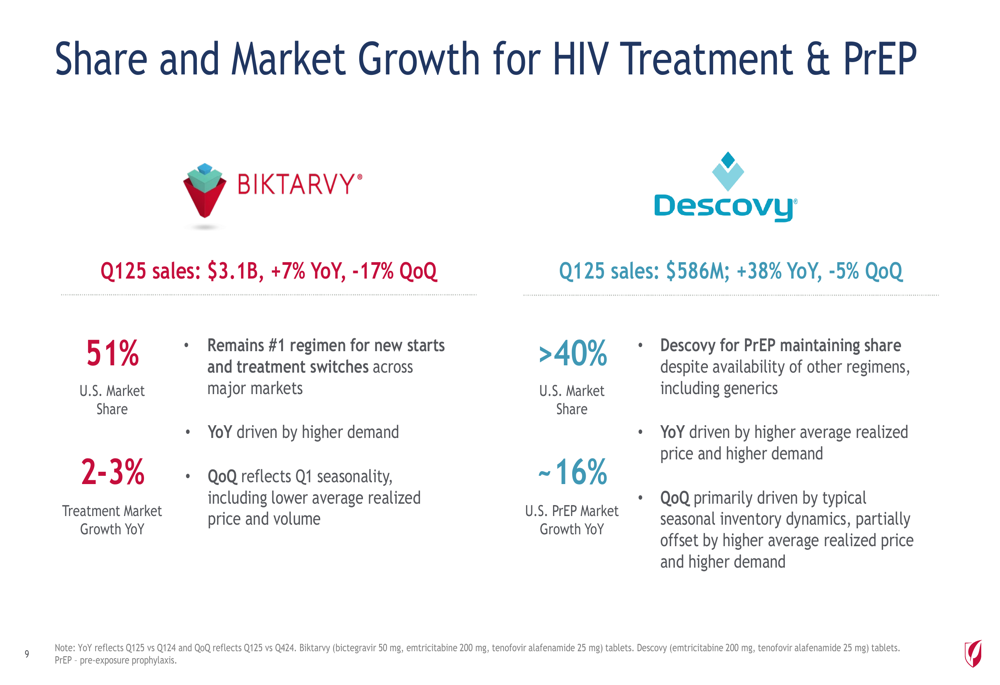

HIV products remained the cornerstone of Gilead’s business, contributing $4.6 billion in sales (70% of total revenue) and growing 6% year-over-year. This growth was driven by higher average realized price and increased demand. Biktarvy, the company’s flagship HIV treatment, grew 7% year-over-year to $3.1 billion, maintaining its position as the #1 regimen for new starts and treatment switches across major markets with a 51% U.S. market share.

Notably, Descovy for PrEP (pre-exposure prophylaxis) showed impressive growth of 38% year-over-year to $586 million, maintaining over 40% U.S. market share despite the availability of generic alternatives. This performance demonstrates the strength of Gilead’s HIV franchise in a competitive market.

The following slide details market share and growth metrics for Gilead’s key HIV products:

Liver disease products contributed $758 million in Q1 2025, up 3% year-over-year, reflecting increased demand across PBC, HBV, and HDV products, partially offset by lower average realized prices for HCV products in the U.S. The company noted continued momentum for the early launch of Livdelzi in primary biliary cholangitis.

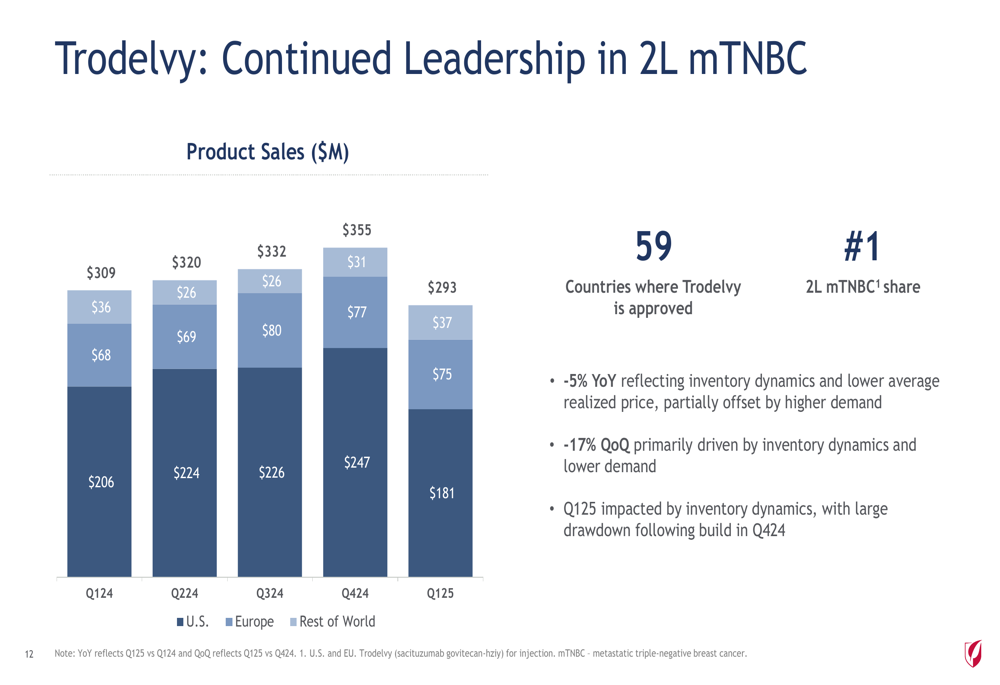

Oncology remains a strategic focus area, with Trodelvy generating $293 million in sales, though this represented a 5% year-over-year decline attributed to inventory dynamics and lower average realized price. Despite the quarterly decline, Trodelvy maintains its leadership position in the second-line mTNBC market in both the U.S. and EU.

As shown in the following chart of Trodelvy sales performance:

Cell therapy products, including Yescarta and Tecartus, generated $464 million in sales, down 3% year-over-year. While Yescarta sales increased 2% year-over-year due to higher average realized price and increased demand outside the U.S., Tecartus sales declined 22% year-over-year due to increased competition.

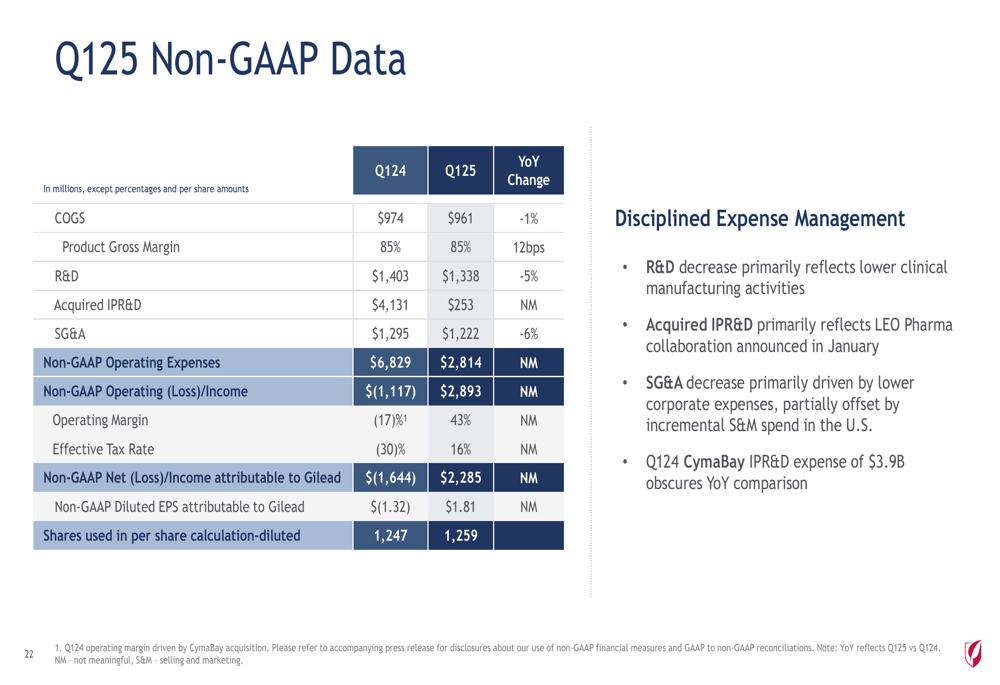

On the financial front, Gilead reported non-GAAP earnings per share of $1.81 for Q1 2025, with a strong operating margin of 43%. The company maintained disciplined expense management, with R&D expenses down 5% year-over-year to $1.34 billion and SG&A expenses down 6% year-over-year to $1.22 billion.

The following slide provides a comprehensive overview of Gilead’s Q1 2025 non-GAAP financial performance:

Pipeline and Strategic Initiatives

Gilead continues to advance its pipeline across viral diseases, oncology, and inflammatory conditions. At the Conference on Retroviruses and Opportunistic Infections (CROI) 2025, the company presented promising data on once-yearly lenacapavir, which maintained blood concentrations higher than those associated with twice-yearly lenacapavir for PrEP for over one year. Based on these results, Gilead plans to initiate a Phase 3 trial in the second half of 2025, with potential regulatory filing around 2028.

In oncology, the company reported positive topline results from the Phase 3 ASCENT-04 trial evaluating Trodelvy in combination with pembrolizumab in first-line PD-L1+ mTNBC, showing a clinically meaningful progression-free survival benefit compared to pembrolizumab plus chemotherapy. Data from this trial will be presented at a medical congress later in 2025.

Gilead is also advancing next-generation CAR T treatments, with data for Kite-363 (CD19/CD20 bicistronic-CAR for relapsed/refractory B-cell lymphoma) and EGFR/IL13Ra2 CAR T (for recurrent glioblastoma) expected at ASCO 2025.

The following slide outlines key milestones expected throughout 2025:

Forward-Looking Statements

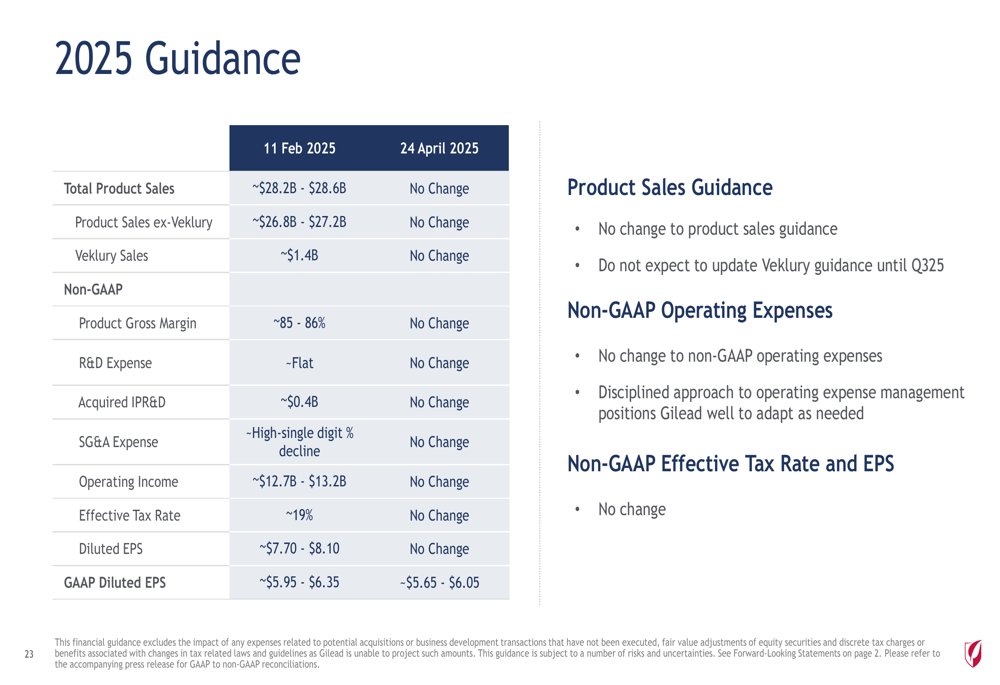

Gilead maintained its full-year 2025 guidance for total product sales of approximately $28.2-$28.6 billion and non-GAAP diluted EPS of $7.70-$8.10. However, the company lowered its GAAP diluted EPS guidance to $5.65-$6.05 from the previous range of $5.95-$6.35, which may have contributed to the after-hours stock decline.

The company continues to prioritize shareholder returns, with $1.7 billion returned to shareholders in Q1 2025, including $1.0 billion in dividends and $730 million in share repurchases. Gilead’s strategic capital allocation priorities remain unchanged, focusing on business investment, partnerships, dividend growth, and share repurchases.

As shown in the following guidance table, Gilead maintains a confident outlook for 2025:

Looking ahead, Gilead is well-positioned for potential launches, including lenacapavir for PrEP in the U.S., anito-cel for multiple myeloma, and Trodelvy for first-line PD-L1+ mTNBC in 2026. The company noted that it has no major product loss of exclusivity events until late 2033, providing a stable foundation for long-term growth.

Despite the positive overall performance and maintained guidance, investors may be concerned about the challenges in certain segments and the lowered GAAP EPS guidance, as reflected in the after-hours trading decline of 4.19% to $101.71.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.