TPI Composites files for Chapter 11 bankruptcy, plans delisting from Nasdaq

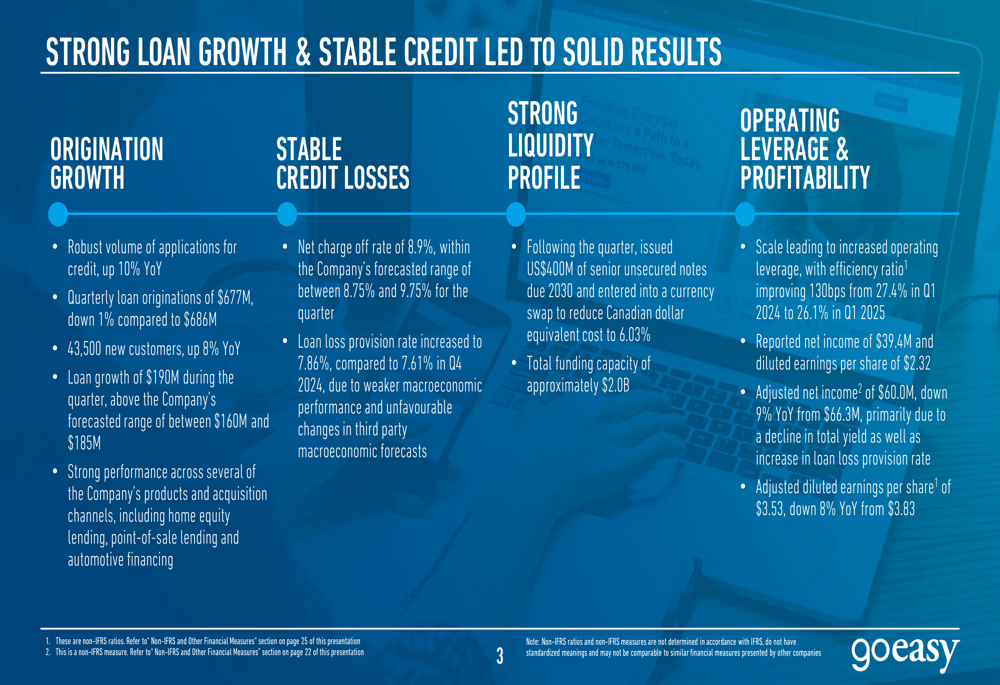

Canadian non-prime lender goeasy Ltd (TSX:GSY) reported its first quarter 2025 results on May 8, showing continued expansion of its loan portfolio despite a slight decline in originations, as the company increasingly shifts toward secured lending to manage risk in the current economic environment.

Executive Summary

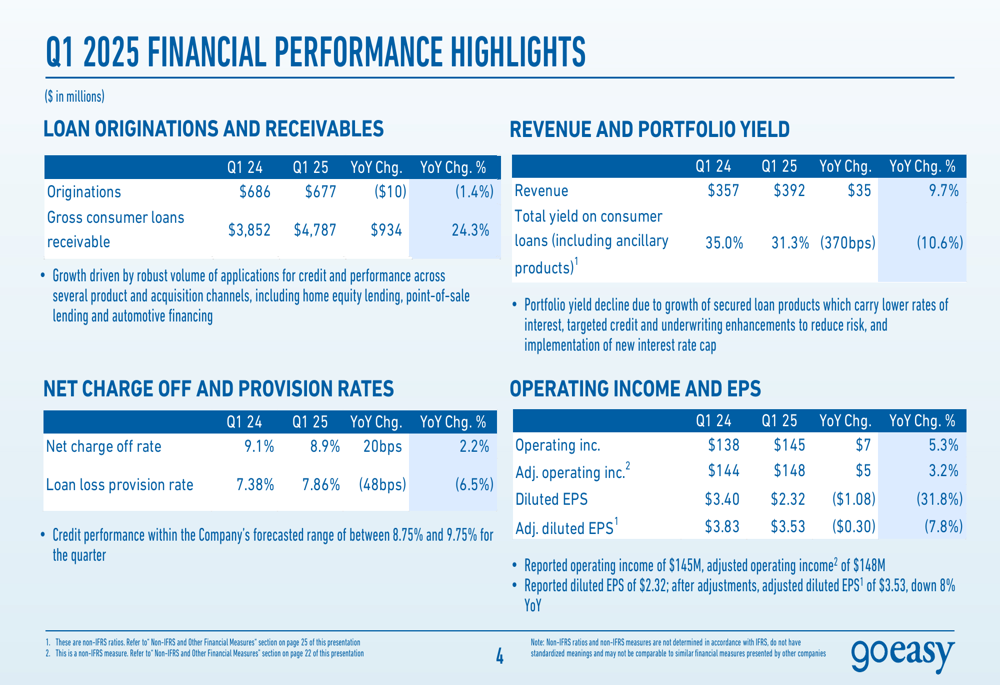

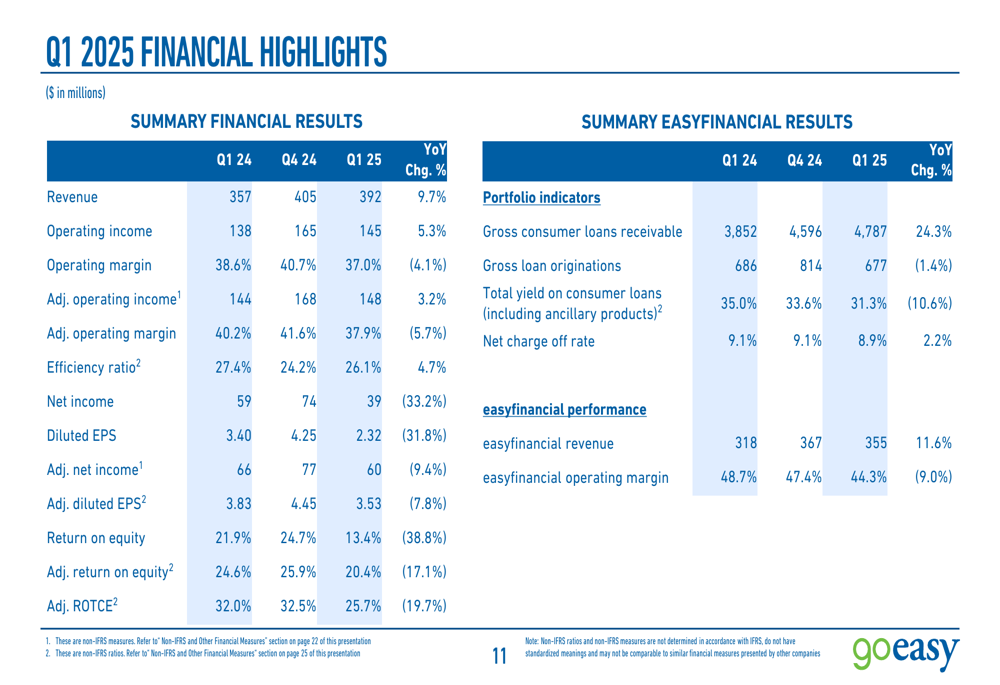

goeasy’s gross consumer loans receivable reached $4.79 billion at the end of Q1 2025, representing a 24.3% increase year-over-year, while quarterly loan originations decreased slightly to $677 million, down 1.4% compared to the same period last year. The company reported revenue of $392 million, up 9.7% year-over-year, but saw declines in profitability metrics with adjusted net income falling 9.4% to $60 million and adjusted diluted earnings per share decreasing 7.8% to $3.53.

As shown in the following summary of key performance highlights, goeasy maintained stable credit performance while continuing to grow its customer base:

"We delivered solid results in the first quarter, with strong loan growth and stable credit performance," said Jason Mullins, goeasy’s President and CEO. "Our strategy of diversifying into secured lending continues to strengthen our portfolio, with 46% now secured by hard assets, up from 42.7% a year ago."

Quarterly Performance Highlights

The company’s financial performance showed mixed results, with strong top-line growth but pressure on profitability metrics. Total (EPA:TTEF) revenue increased 9.7% to $392 million, while operating income grew 5.3% to $145 million. However, reported net income declined 33.2% to $39.4 million, with diluted earnings per share falling 31.8% to $2.32. On an adjusted basis, which excludes certain non-recurring items, net income decreased 9.4% to $60 million and diluted EPS fell 7.8% to $3.53.

The following chart provides a detailed breakdown of goeasy’s financial performance for Q1 2025 compared to the previous year:

The company’s efficiency ratio improved to 26.1% from 27.4% in the prior year, reflecting enhanced operating leverage as goeasy continues to scale its operations. This improvement came despite ongoing investments in technology and infrastructure to support future growth.

A comprehensive summary of goeasy’s financial results shows the pressure on profitability metrics, with return on equity declining to 13.4% from 21.9% in the prior year:

Strategic Initiatives

goeasy continues to focus on diversifying its product mix and enhancing credit quality. The company reported strong application volume of 672,000, up 10% year-over-year, and added 43,500 new customers, an 8% increase from the prior year. Notably, the company achieved its highest weighted average credit score for quarterly loan originations in its history at 632.

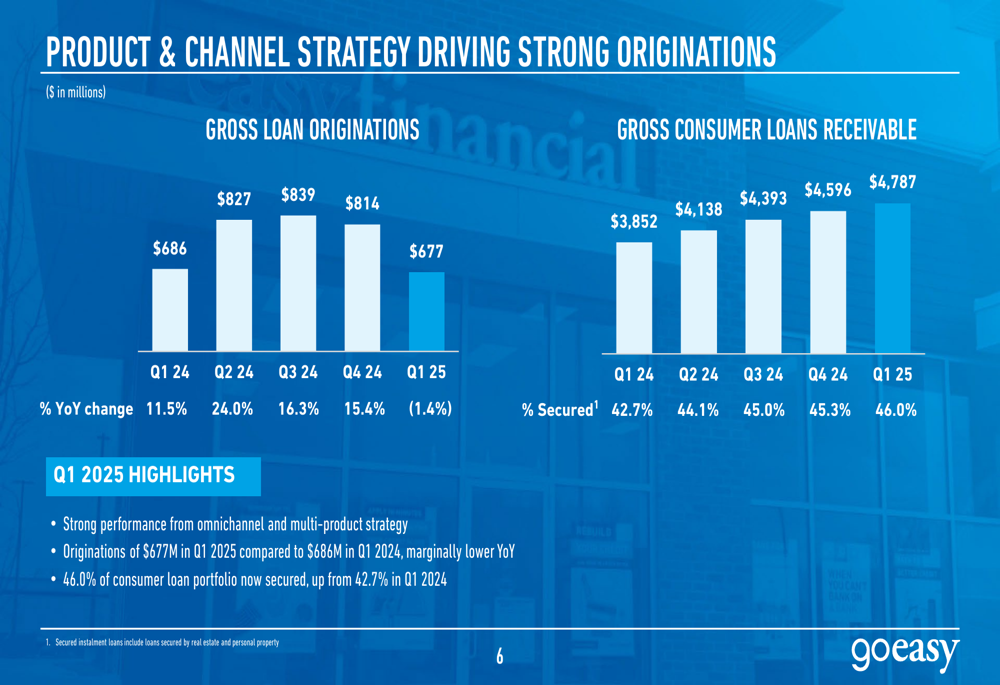

The following chart illustrates goeasy’s product and channel strategy, which has driven consistent growth in its loan portfolio despite the recent moderation in originations:

The company has made significant progress in expanding its secured lending offerings, with home equity loan originations increasing 29% year-over-year and auto financing originations reaching a record $150 million for the first quarter, up 30% from the prior year. This strategic shift toward secured lending helps reduce credit risk and positions the company for more stable performance in varying economic conditions.

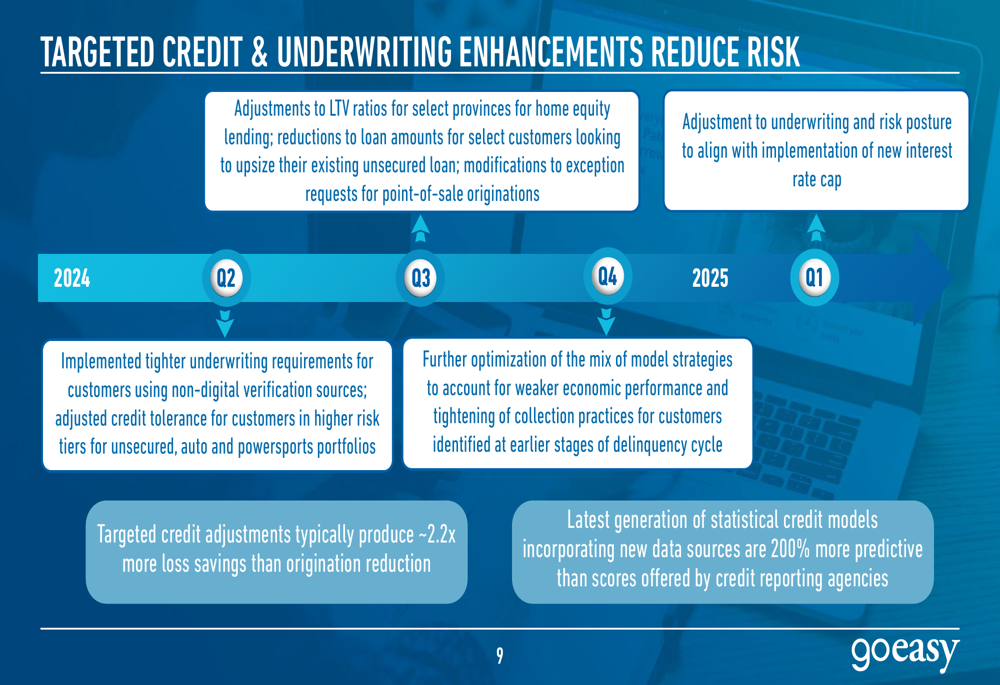

As shown in the following slide, goeasy has implemented targeted credit and underwriting enhancements to reduce risk:

"Our latest generation of statistical credit models incorporating new data sources are 200% more predictive than scores offered by credit reporting agencies," noted Mullins. "These targeted credit adjustments typically produce 2.2 times more loss savings than origination reduction."

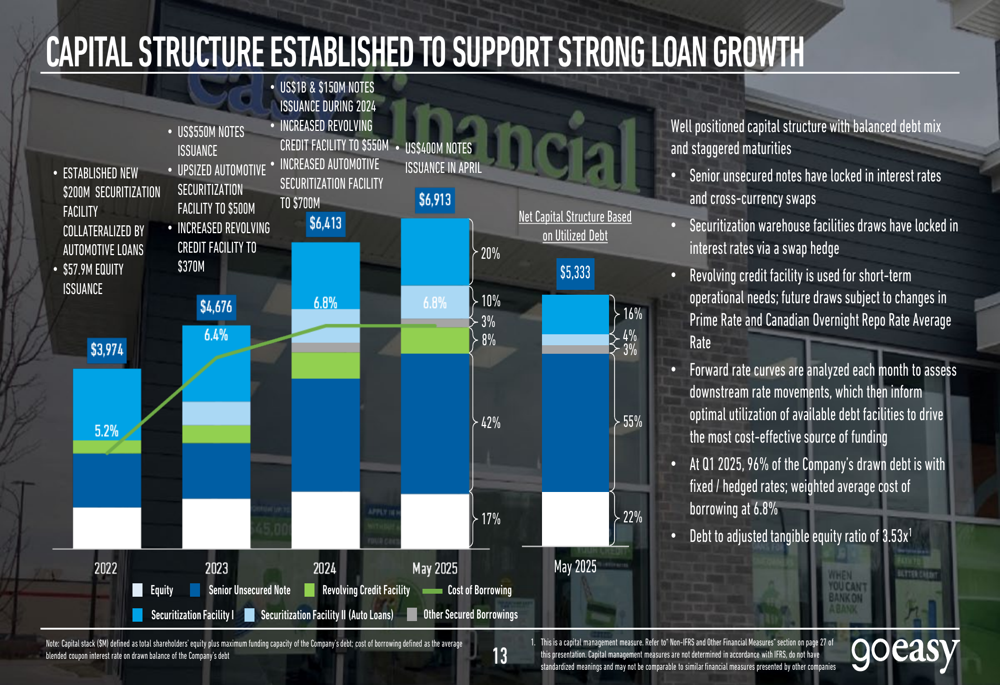

Liquidity and Capital Position

goeasy maintains a strong liquidity position to support its growth objectives. Following the quarter, the company issued US$400 million of senior unsecured notes, further strengthening its capital structure. The company’s funding capacity stands at approximately $2.0 billion, providing ample resources to fund future loan growth.

The following chart illustrates goeasy’s capital structure evolution:

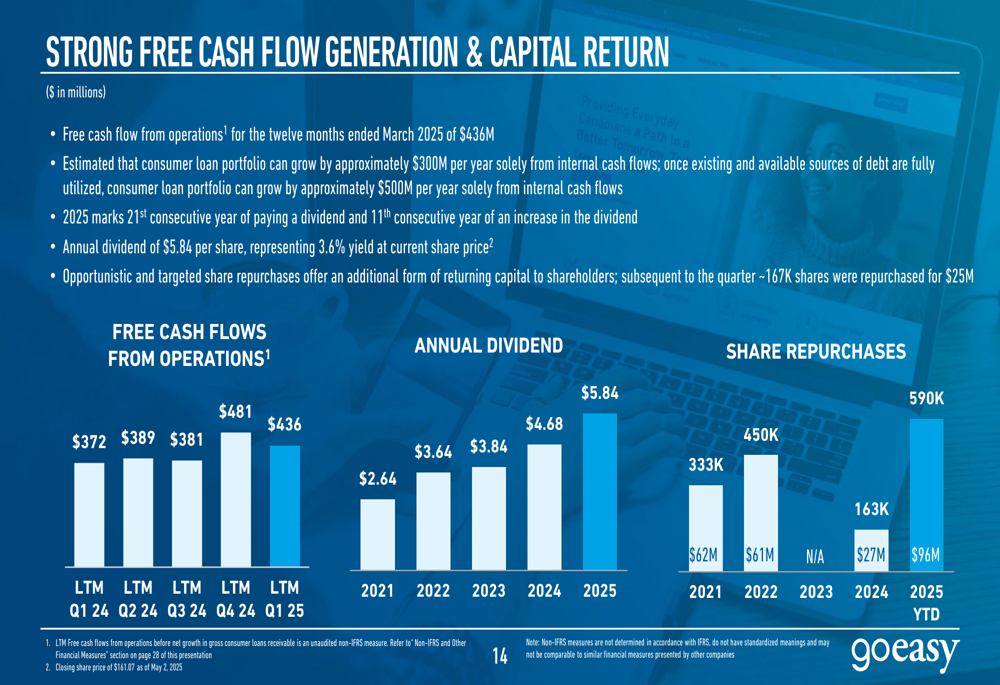

The company continues to generate strong free cash flow, with $436 million from operations for the twelve months ended March 2025. This robust cash generation supports both portfolio growth and shareholder returns, with goeasy marking its 21st consecutive year of paying a dividend and 11th consecutive year of dividend increases. The annual dividend now stands at $5.84 per share, representing a 3.6% yield at the current share price.

As illustrated in the following chart, goeasy’s free cash flow generation and capital return strategy have remained strong:

Forward-Looking Statements

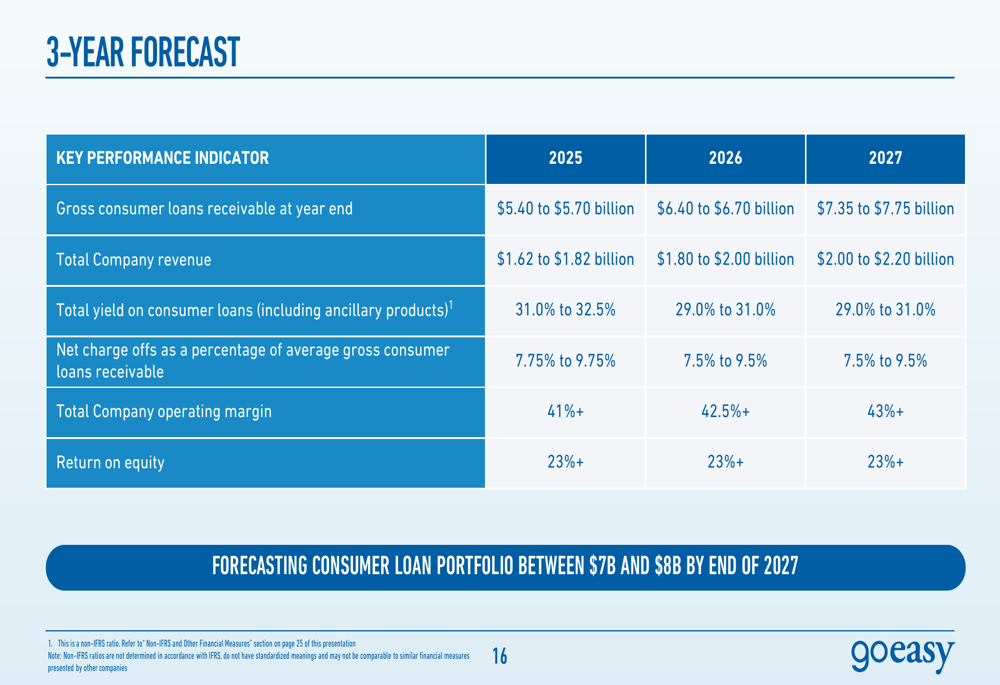

goeasy provided a three-year forecast projecting continued growth in its loan portfolio, expecting to reach between $7.35 billion and $7.75 billion by the end of 2027. The company anticipates total revenue to grow to between $2.00 billion and $2.20 billion by 2027, with operating margins expanding to 43%+ and return on equity maintaining at 23%+.

The detailed three-year forecast provides visibility into goeasy’s expected performance metrics:

For the immediate future, goeasy expects its gross consumer loan portfolio to grow between $275 million and $300 million in Q2 2025, with the total yield on consumer loans (including ancillary products) between 31.0% and 32.0%, and a net charge off rate between 8.75% and 9.75%.

"We remain confident in our ability to continue growing our business while maintaining strong credit performance," said Mullins. "Our diversified product mix, enhanced underwriting capabilities, and strong capital position provide us with the foundation to execute on our long-term growth strategy."

goeasy shares closed at $158.88 on May 7, 2025, up 1.11% for the day. The stock has traded between $134.01 and $206.02 over the past 52 weeks.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.