Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Xinjiang Goldwind Science & Technology Co Ltd (SZEx:002202, HKEx:2208) recently released its 1H 2025 interim results presentation, revealing strong revenue growth in its core wind turbine manufacturing business despite an earnings per share miss noted in recent earnings reports.

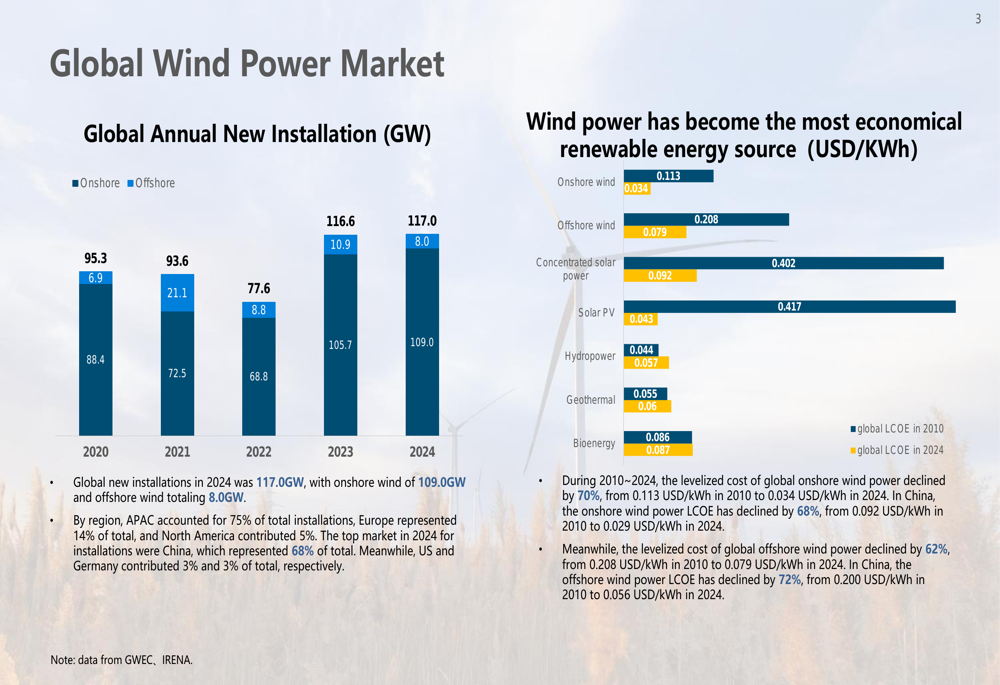

The company operates in a growing global wind power market that reached 117GW of new installations in 2024, with the Asia-Pacific region accounting for 75% of total installations. China continues to dominate the global wind power landscape, representing 68% of total installations worldwide.

As shown in the following chart detailing global wind power market trends:

The economics of wind power have improved dramatically over the past decade. From 2010 to 2024, the levelized cost of global onshore wind power declined by 70%, from 0.113 USD/kWh to 0.034 USD/kWh, while offshore wind power costs fell by 62%, from 0.208 USD/kWh to 0.079 USD/kWh. This cost reduction has made wind power increasingly competitive with conventional energy sources.

Financial Performance Highlights

Goldwind reported total revenue of RMB 28,537 million for the first half of 2025, with a comprehensive profit margin of 15.35%. Net profit attributable to owners of the company reached RMB 1,488 million, yielding a weighted average return on equity of 3.85%.

The following chart illustrates Goldwind’s key profitability metrics:

Despite these positive revenue figures, the company’s recent earnings report revealed an EPS of $0.21, missing analyst forecasts of $0.25. Nevertheless, investors appeared to focus on the company’s strong revenue growth and robust order backlog, as evidenced by the 10.46% stock surge in after-hours trading following the earnings release, with shares closing at $11.62.

Segment Analysis

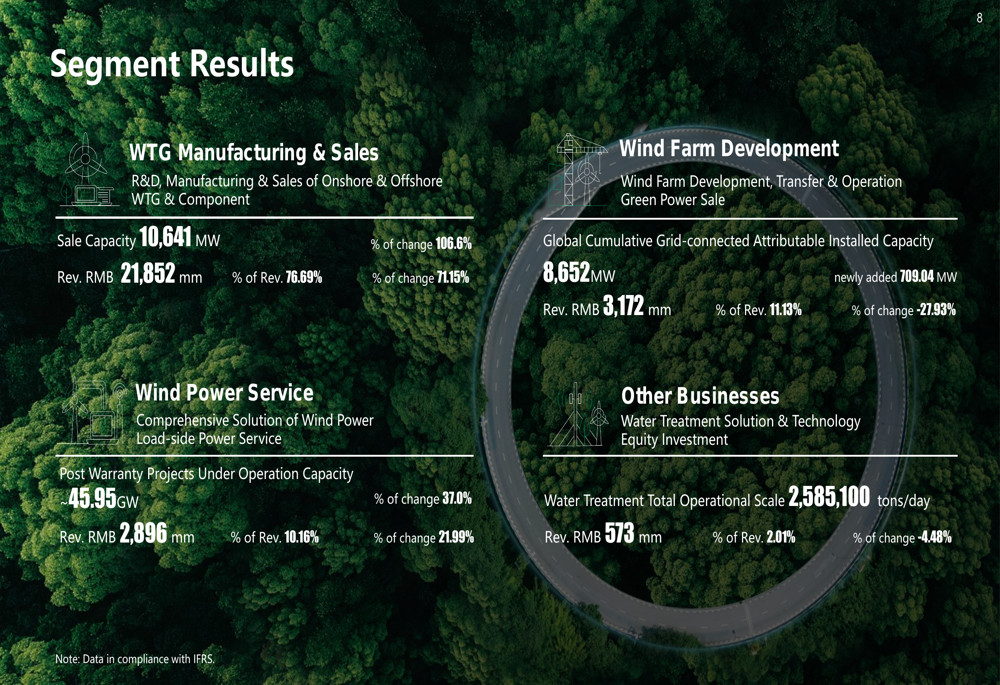

Goldwind’s business is divided into four main segments, with Wind Turbine Generator (WTG) Manufacturing & Sales serving as the primary revenue driver. This segment generated RMB 21,852 million in 1H25, representing 76.69% of total revenue and showing remarkable year-over-year growth of 71.15%.

The following breakdown illustrates the performance across all business segments:

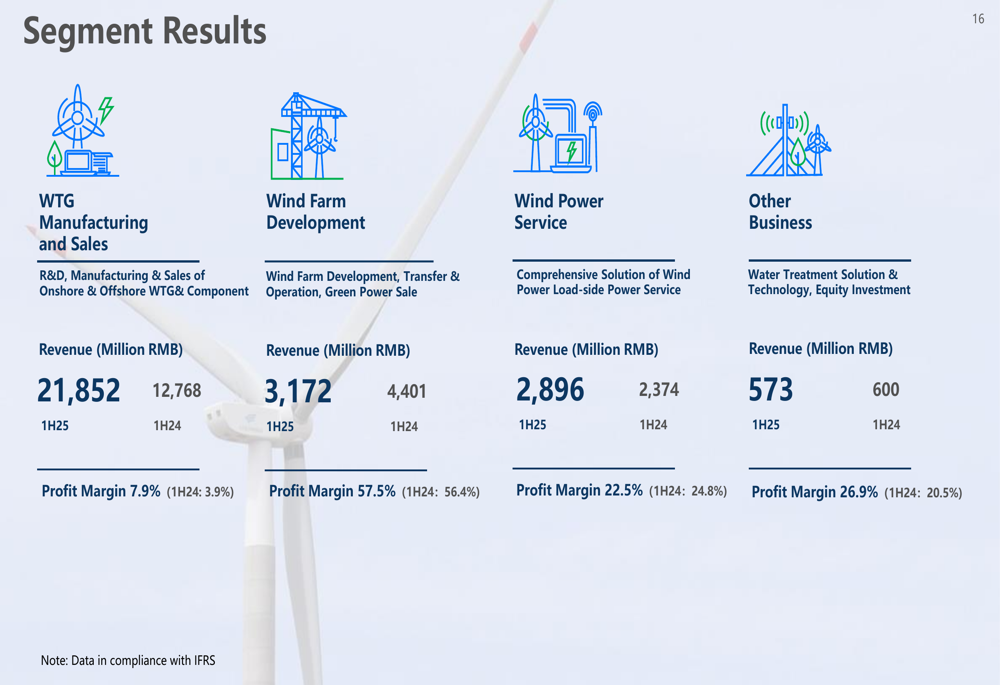

A closer look at segment profitability reveals that while WTG Manufacturing & Sales dominates revenue, Wind Farm Development delivers the highest profit margin at 57.5% in 1H25, up from 56.4% in 1H24. The WTG Manufacturing segment saw significant margin improvement, increasing from 3.9% in 1H24 to 7.9% in 1H25.

The detailed segment results are shown here:

Product Mix and Order Backlog

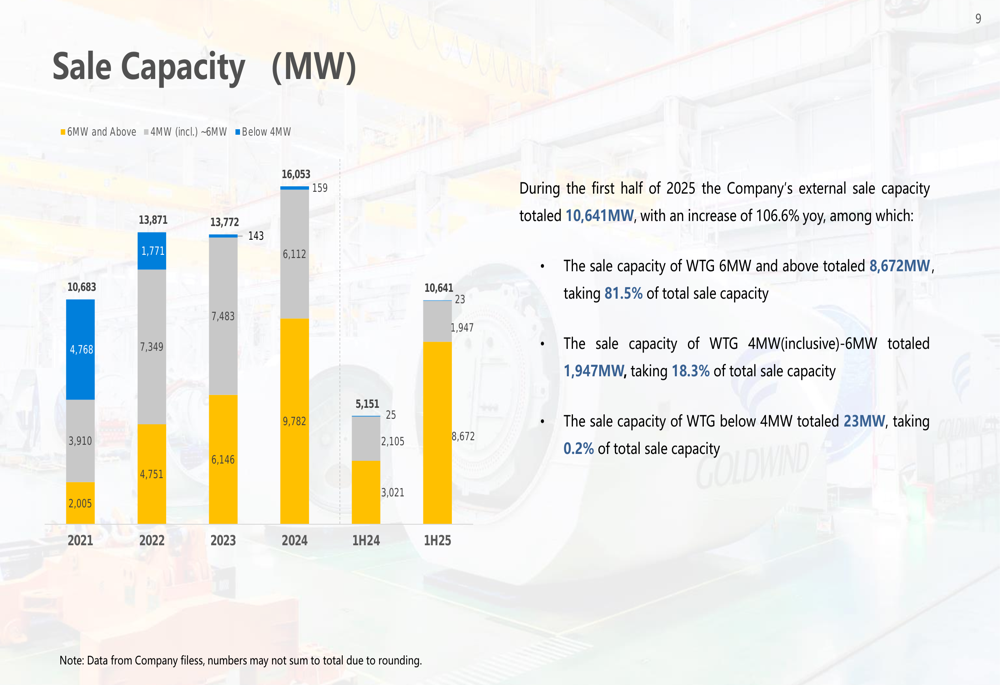

Goldwind’s product strategy has increasingly focused on larger capacity wind turbines. In 1H25, turbines of 6MW and above accounted for 81.5% of total sale capacity (8,672MW), while 4MW to 6MW units represented 18.3% (1,947MW). Units below 4MW have become nearly obsolete, accounting for just 0.2% (23MW) of sales.

This shift toward higher capacity turbines is illustrated in the following chart:

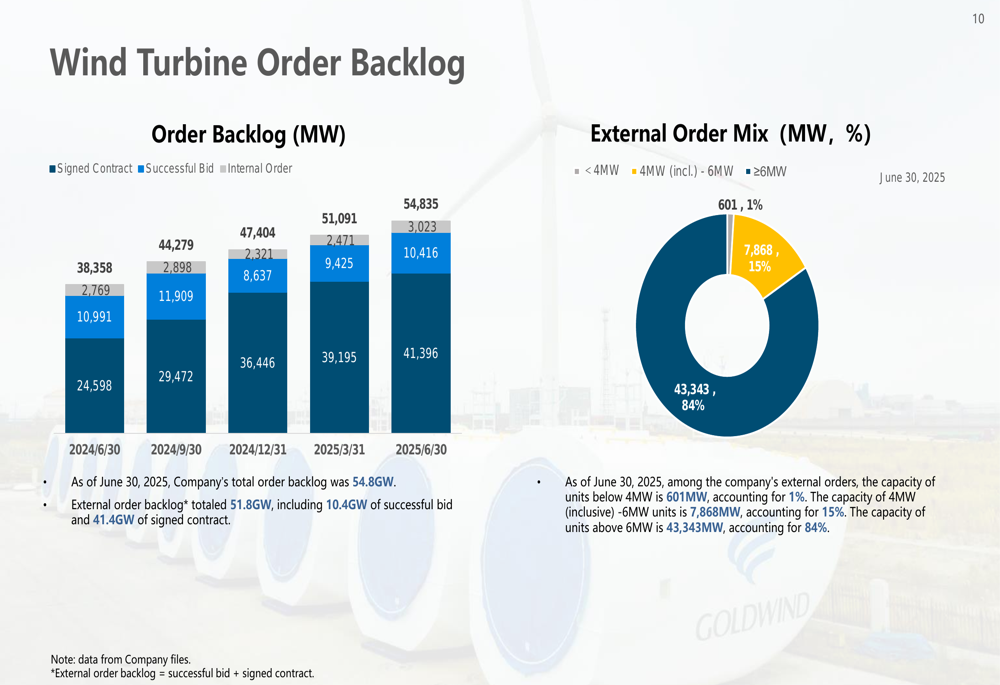

The company’s order backlog provides strong visibility for future revenue. As of June 30, 2025, Goldwind’s total order backlog stood at 54.8GW, with external orders accounting for 51.8GW (including 10.4GW of successful bids and 41.4GW of signed contracts).

The composition of the order backlog further demonstrates the market’s shift toward larger turbines, with units of 6MW and above representing 84% of external orders:

Global Expansion

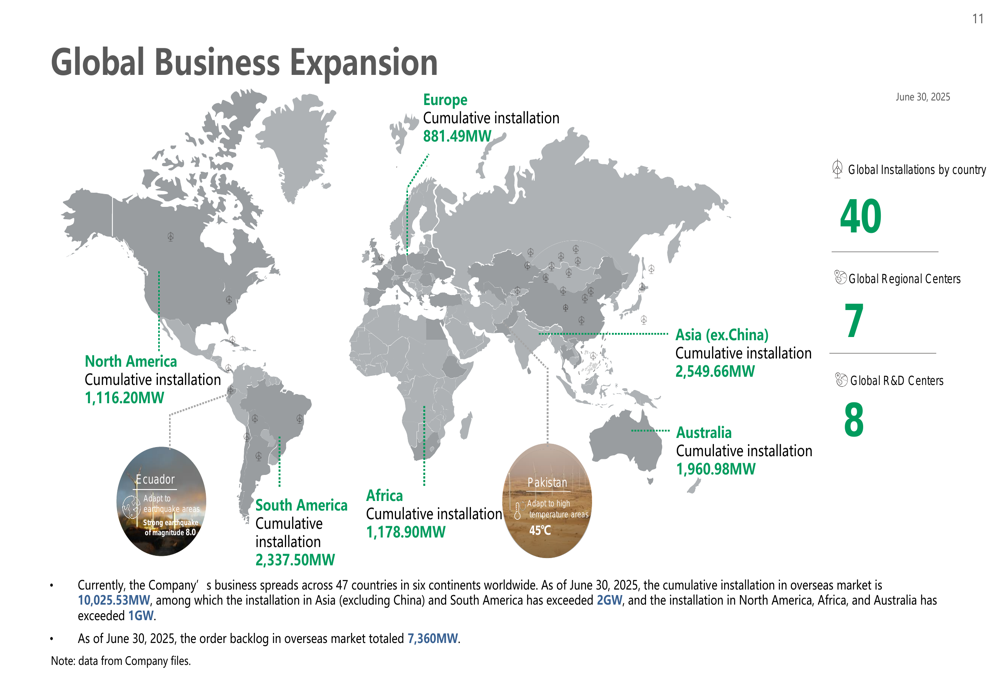

While China remains Goldwind’s primary market, the company continues to expand its global footprint. As of June 30, 2025, cumulative installations in overseas markets reached 10,025.53MW, with significant presence in Asia ex-China (2,549.66MW), South America (2,337.50MW), and Australia (1,960.98MW).

The company’s global expansion is visualized in this world map:

The overseas order backlog totaled 7,360MW as of June 30, 2025, indicating continued momentum in international markets despite the company’s primary focus on domestic Chinese opportunities.

Financial Health and Challenges

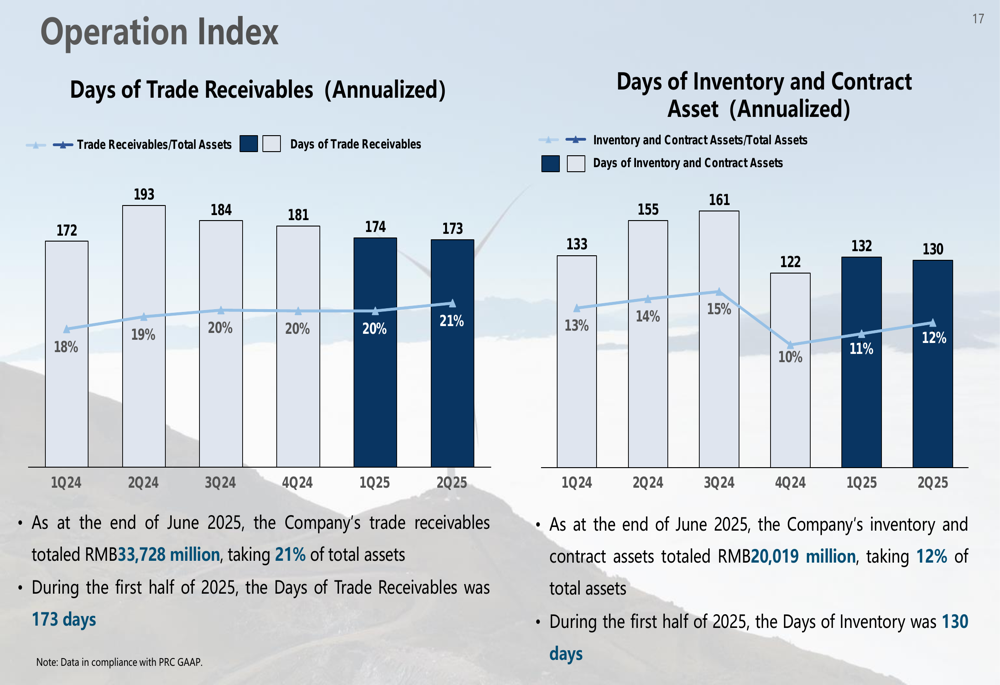

Despite strong revenue growth, Goldwind faces several financial challenges. The company reported net operating cash outflows of RMB 2,949 million in 1H25, suggesting potential working capital management issues. Days of trade receivables stood at 173 days, while days of inventory reached 130 days, indicating room for operational efficiency improvements.

The following chart details these operational metrics:

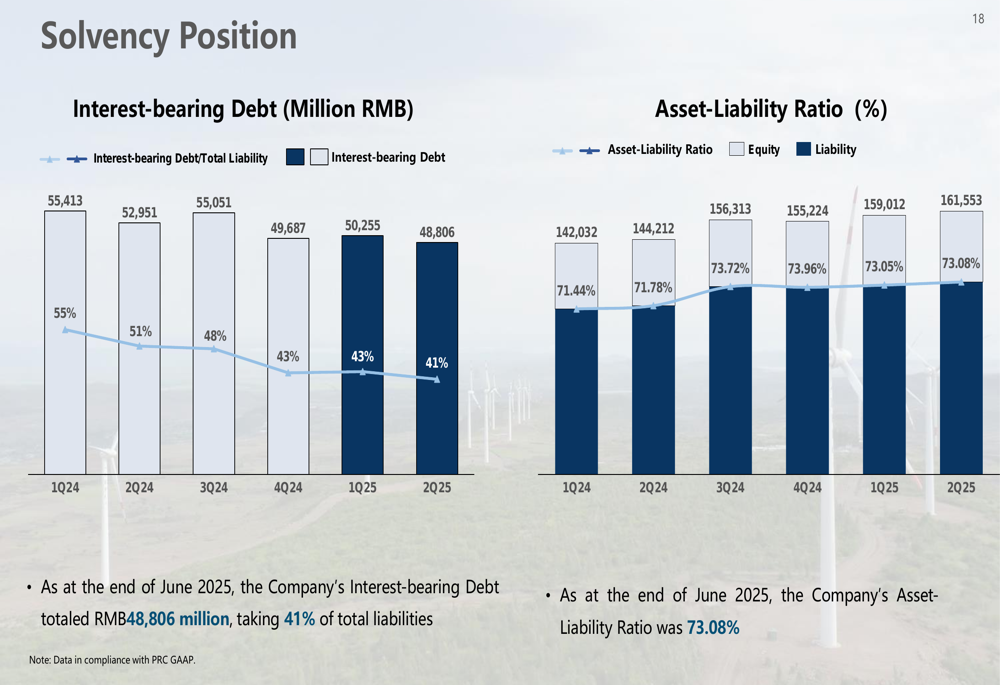

Goldwind’s balance sheet shows an asset-liability ratio of 73.08% as of June 30, 2025. Interest-bearing debt totaled RMB 48,806 million, representing 41% of total liabilities. The company’s cash position relative to total assets was 5.93%, which may limit financial flexibility.

The company’s solvency position is illustrated here:

Forward Outlook

Goldwind is well-positioned to benefit from China’s continued investment in renewable energy. In the first half of 2025, China recorded 51.4GW of new grid-connected wind power capacity, representing a 98.9% year-over-year increase. As of June 2025, China’s cumulative grid-connected wind power capacity totaled 572.6GW, accounting for 15.7% of the country’s power mix.

The domestic public tender market remains robust, totaling 71.9GW in 1H25 (an 8.8% year-over-year increase), with onshore projects accounting for 66.9GW and offshore projects for 5.0GW. The average bidding price in June 2025 was RMB 1,616/kW.

According to the company’s recent earnings call, Goldwind is currently drafting its fifteenth five-year strategy, which will focus on expanding overseas markets and improving cash flow management. While the robust order backlog provides strong revenue visibility, the company will need to address its cash flow challenges and high debt levels to sustain long-term growth.

As Goldwind’s CFO Wang Hong Yan noted during the earnings call, "Our revenue is very historically high, which is definitely attributable to our WTG manufacturing." The company’s focus on larger, more efficient turbines and its strong order backlog suggest continued revenue growth potential, though margin improvement and cash flow management will be key areas to watch in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.