US stock futures inch higher with Q3 earnings on tap

Introduction & Market Context

Graco Inc . (NYSE:GGG), a leading manufacturer of fluid handling equipment, reported its second quarter 2025 financial results on July 24, 2025, showing modest revenue growth but facing margin pressure from tariffs and product costs. The company’s stock closed at $87.20 on July 23, 2025, virtually unchanged (-0.02%) ahead of the earnings release.

The company’s presentation highlighted a 3% increase in quarterly sales to $571.8 million, primarily driven by acquisitions, while organic growth faced headwinds across various segments and regions. Despite the revenue growth, operating margins declined as tariffs and product costs weighed on profitability.

Quarterly Performance Highlights

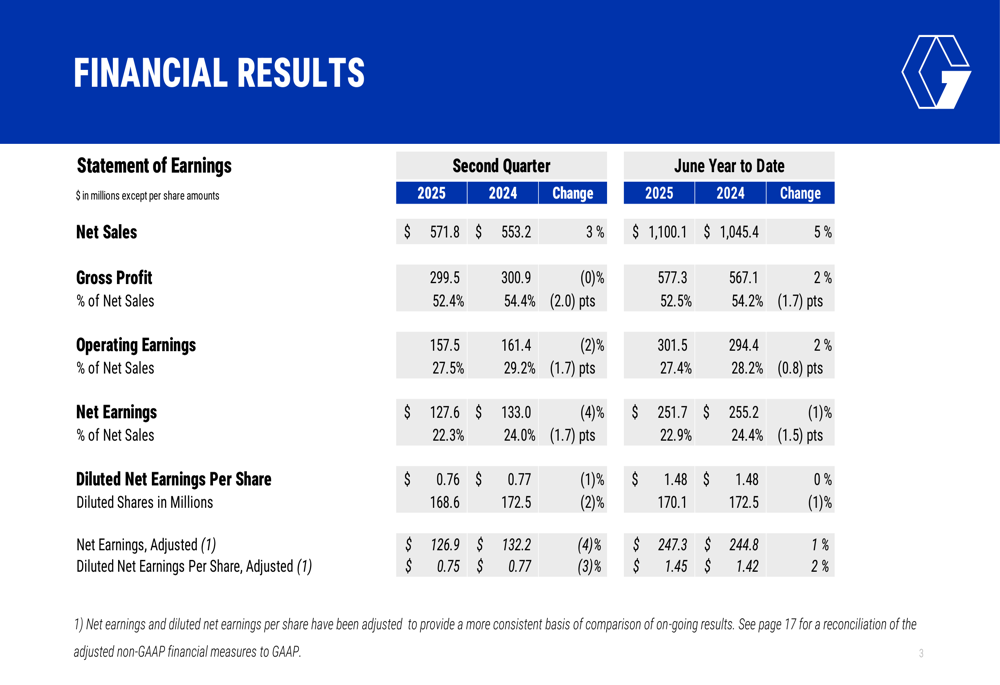

Graco reported second quarter 2025 net sales of $571.8 million, up 3% from $553.2 million in Q2 2024. Net earnings reached $127.6 million with diluted earnings per share of $0.76. Year-to-date sales increased 5% to $1,100.1 million, with net earnings of $251.7 million and diluted EPS of $1.48.

As shown in the following comprehensive financial summary:

While revenue growth was positive, the company’s gross margin declined by 2 percentage points due to higher product costs, including tariff impacts. Operating earnings decreased to $157.5 million (27.5% of sales) from 29% in the comparable period, reflecting these cost pressures.

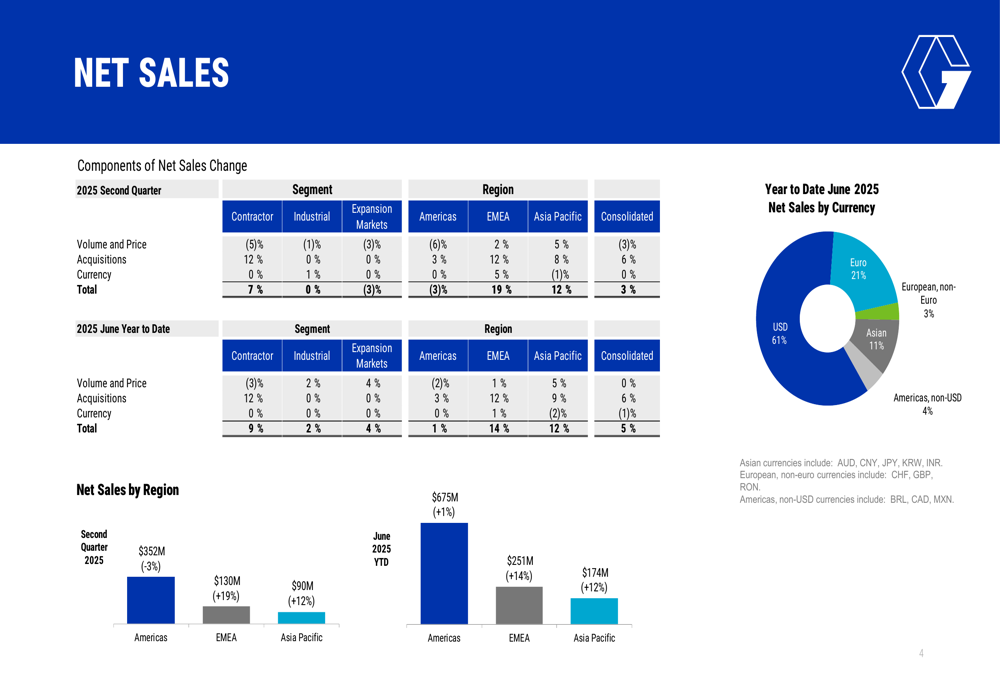

The company’s sales growth was primarily acquisition-driven, as illustrated in this breakdown of sales by segment and region:

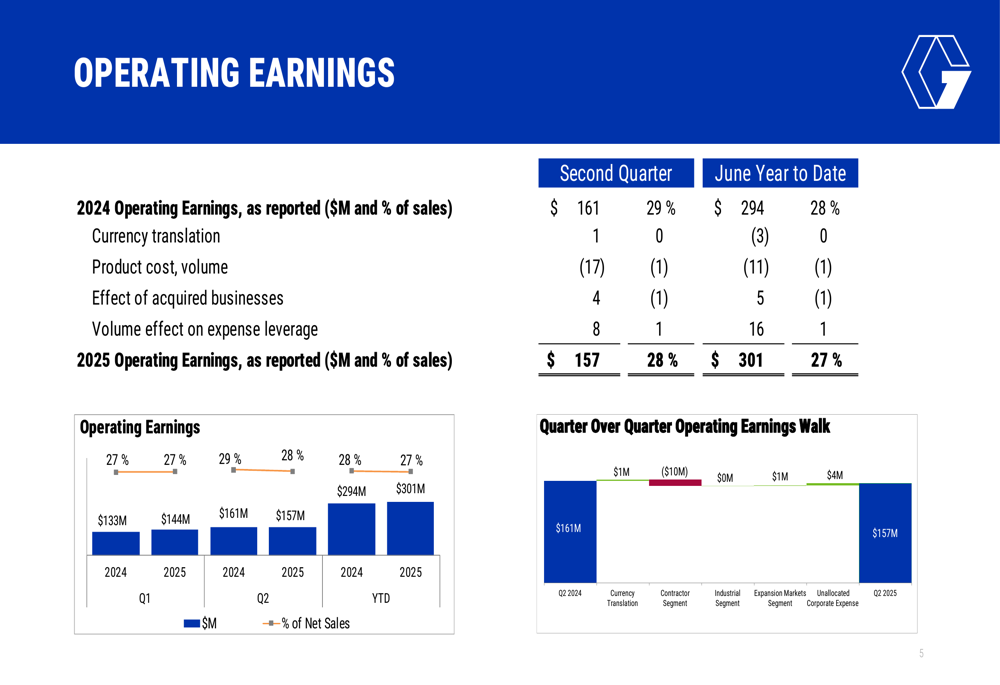

Operating earnings were negatively impacted by several factors, as shown in this analysis of the changes from 2024 to 2025:

Segment Analysis

Graco’s performance varied significantly across its three business segments:

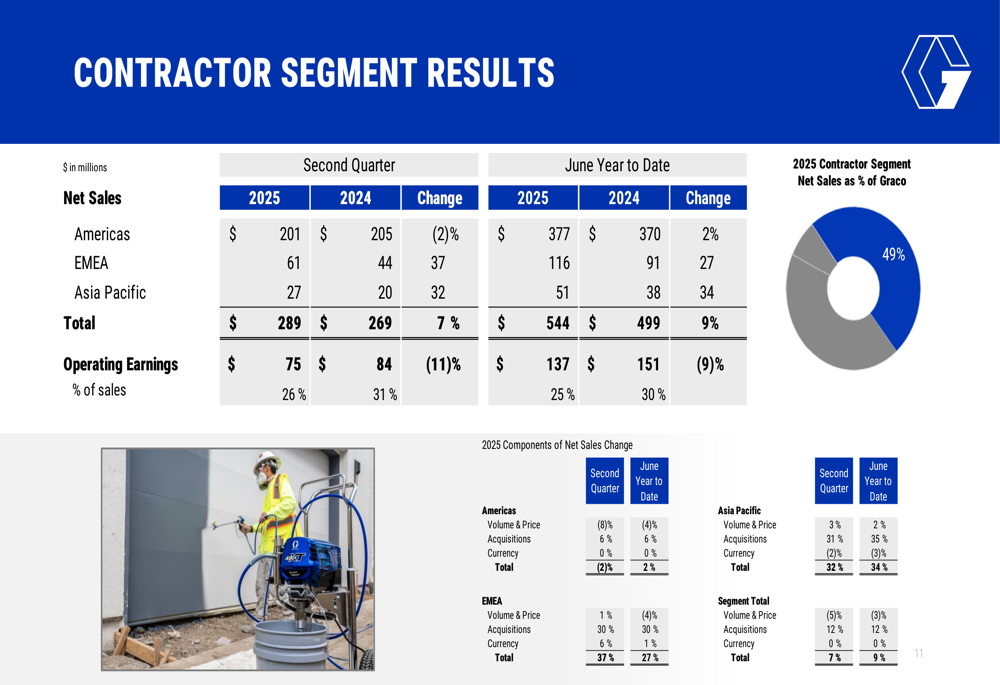

The Contractor segment showed 7% sales growth to $289 million, but operating margins declined substantially from 31% to 26% due to product costs and mix challenges. This segment, which serves construction and home improvement markets, saw its profitability impacted by product cost increases and channel mix shifts.

As shown in the detailed Contractor segment results:

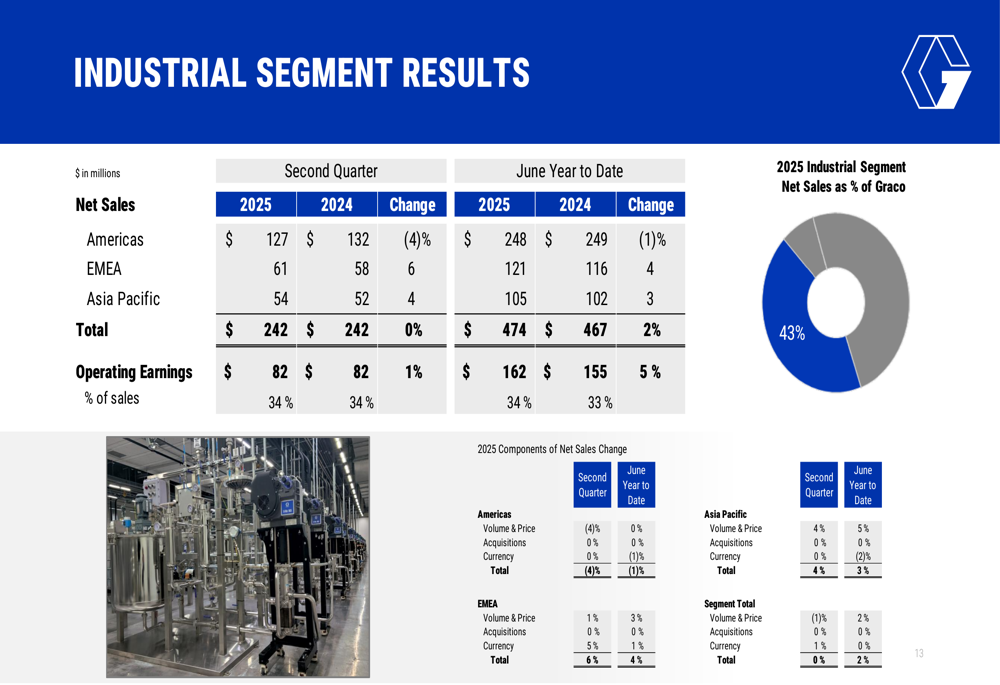

The Industrial segment maintained stable performance with sales flat at $242 million and operating margins unchanged at 34%. This segment, which provides equipment for industrial applications, demonstrated resilience despite challenging market conditions.

The segment’s performance is illustrated in this breakdown:

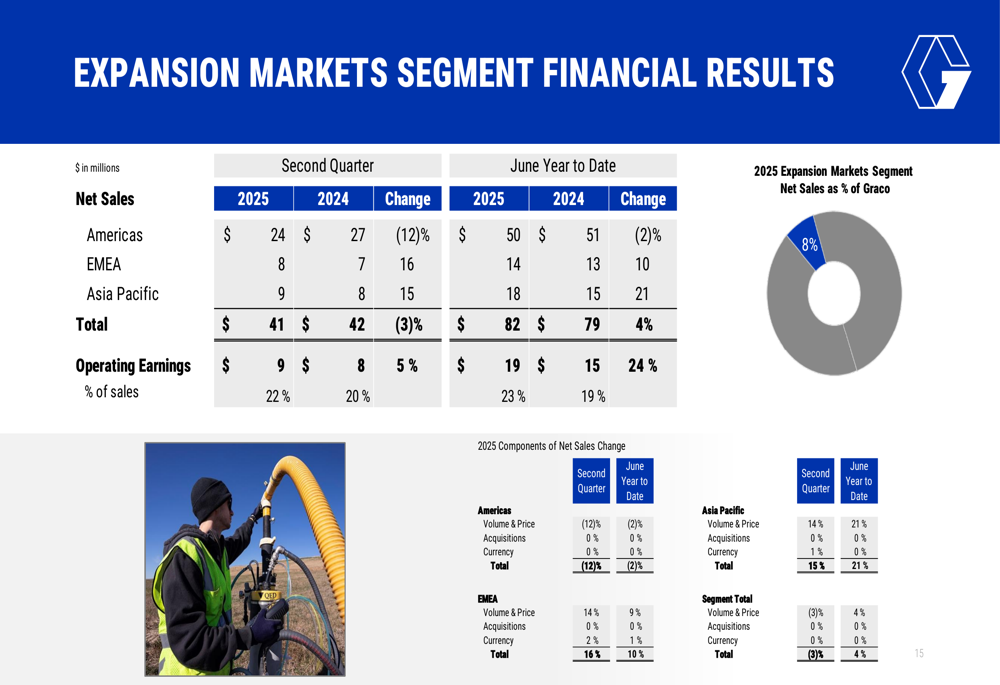

The Expansion Markets segment, which includes process, oil and natural gas, and semiconductor applications, saw sales decline by 3% to $41 million. However, operating margins improved from 20% to 22% due to lower expenses and favorable volume effects, demonstrating effective cost management.

The following chart details the Expansion Markets segment performance:

Cash Flow and Capital Allocation

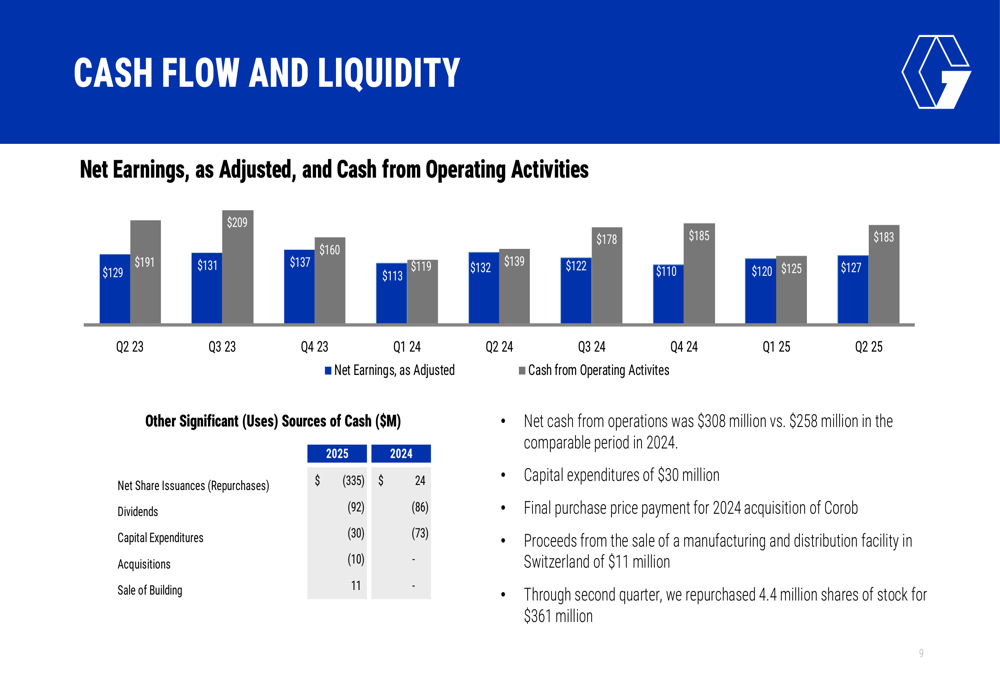

Despite margin pressures, Graco demonstrated strong cash generation, with net cash from operations reaching $308 million compared to $258 million in the comparable period of 2024. The company continued to invest in growth while returning significant capital to shareholders.

As illustrated in this cash flow summary:

Capital expenditures totaled $30 million during the first half of 2025, with full-year expectations of $60-70 million. The company completed the final purchase price payment for its 2024 acquisition of Corob and generated $11 million from the sale of a manufacturing and distribution facility in Switzerland.

Notably, Graco continued its aggressive share repurchase program, buying back 4.4 million shares for $361 million through the second quarter, demonstrating confidence in its long-term prospects despite near-term challenges.

Outlook and Guidance

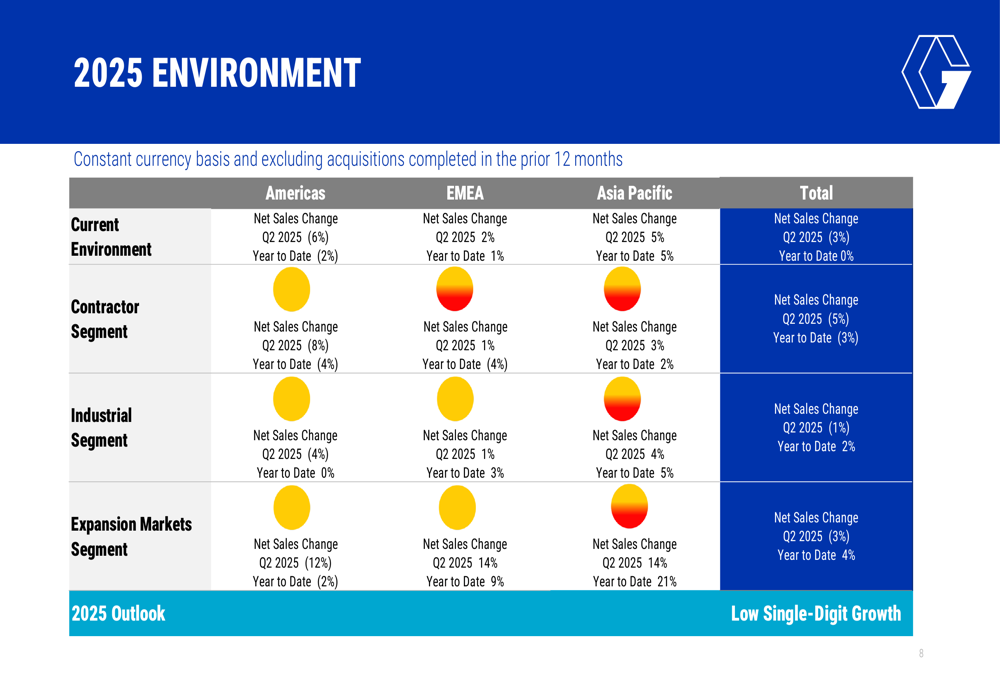

Looking ahead, Graco provided a cautious outlook for the remainder of 2025, projecting low single-digit growth. The company’s assessment of the current business environment reveals varying conditions across regions and segments.

The following chart provides a detailed view of the 2025 operating environment:

On a constant currency basis and excluding acquisitions, Graco’s overall sales declined 3% in Q2 2025 but remained flat for the year-to-date period. The Contractor segment faced the most significant challenges with a 5% sales decline in Q2, while Industrial sales decreased 1% and Expansion Markets sales fell 3%.

The company expects currency movements at current exchange rates to have a favorable impact of 1 percentage point on sales with no impact on net earnings. The effective tax rate for Q3 and full year 2025 is projected to be between 19.5% and 20.5%.

Management continues to focus on operational efficiency and strategic acquisitions to drive growth while navigating the challenges of tariffs and product cost pressures that have impacted margins in recent quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.