AlphaTON stock soars 200% after pioneering digital asset oncology initiative

GrafTech International Ltd (NYSE:EAF) presented its first quarter 2025 results on April 25, revealing a mixed performance as the graphite electrode manufacturer continues to navigate challenging market conditions. While production volumes showed improvement, financial results remained under pressure, with the stock dropping 8.12% in premarket trading following the announcement.

Quarterly Performance Highlights

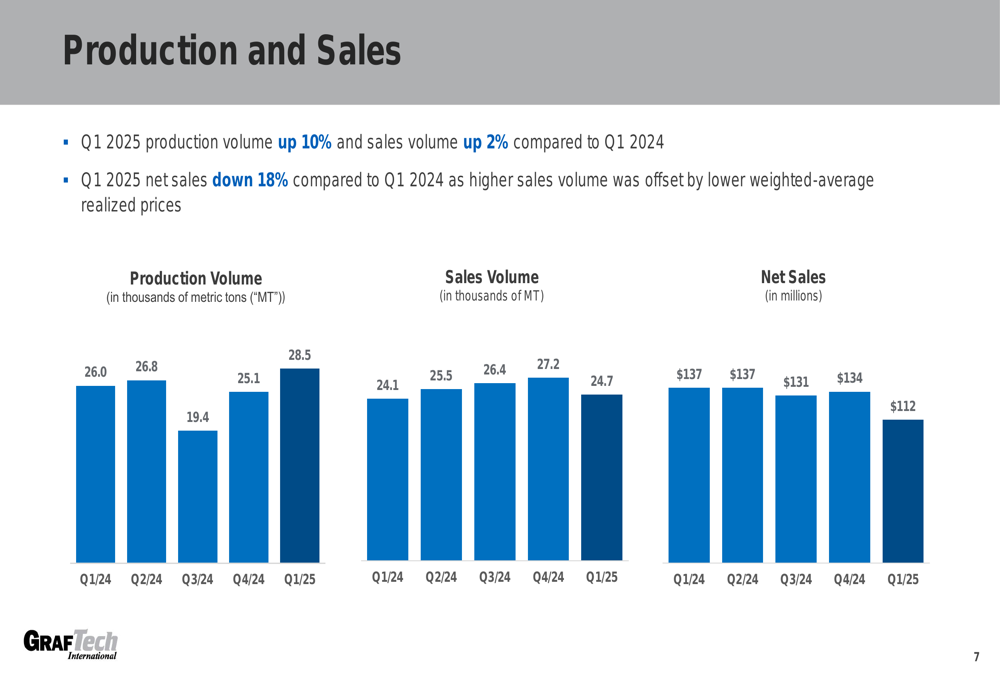

GrafTech reported a 10% year-over-year increase in production volume for Q1 2025, reaching 28,500 metric tons compared to 26,000 metric tons in Q1 2024. Sales volume also saw a modest 2% improvement, rising to 24,700 metric tons from 24,100 metric tons in the prior-year period. However, these operational gains were offset by pricing challenges, as net sales declined 18% year-over-year to $112 million from $137 million.

As shown in the following chart of production and sales volumes over recent quarters:

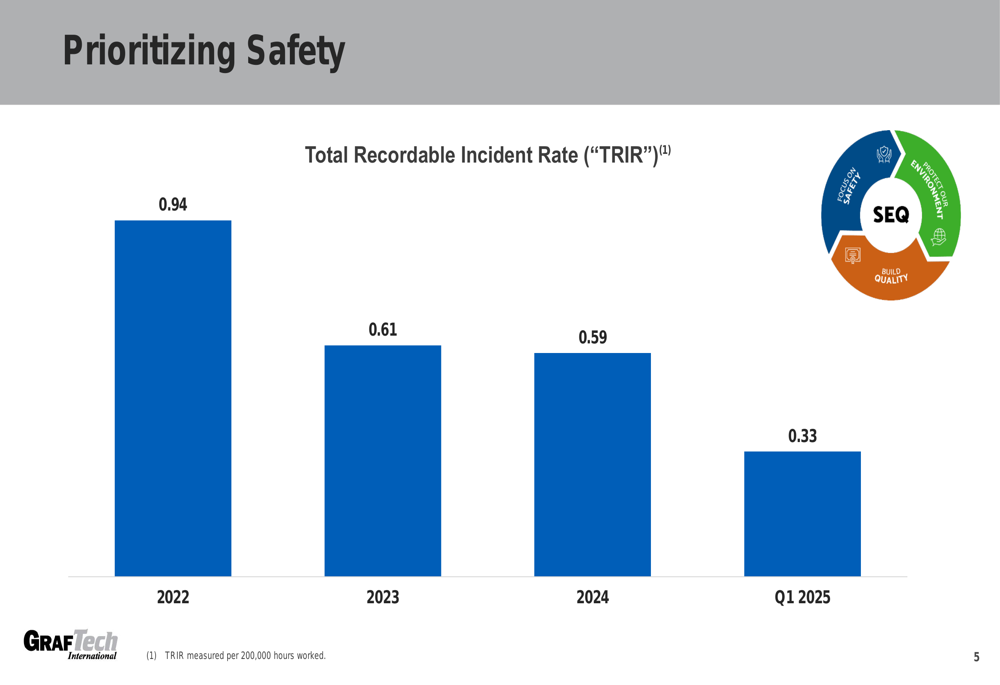

The company’s safety performance continues to improve, with the Total (EPA:TTEF) Recordable Incident Rate (TRIR) decreasing to 0.33 in Q1 2025, compared to 0.59 in 2024 and 0.61 in 2023. This represents a significant improvement from the 0.94 rate recorded in 2022.

Detailed Financial Analysis

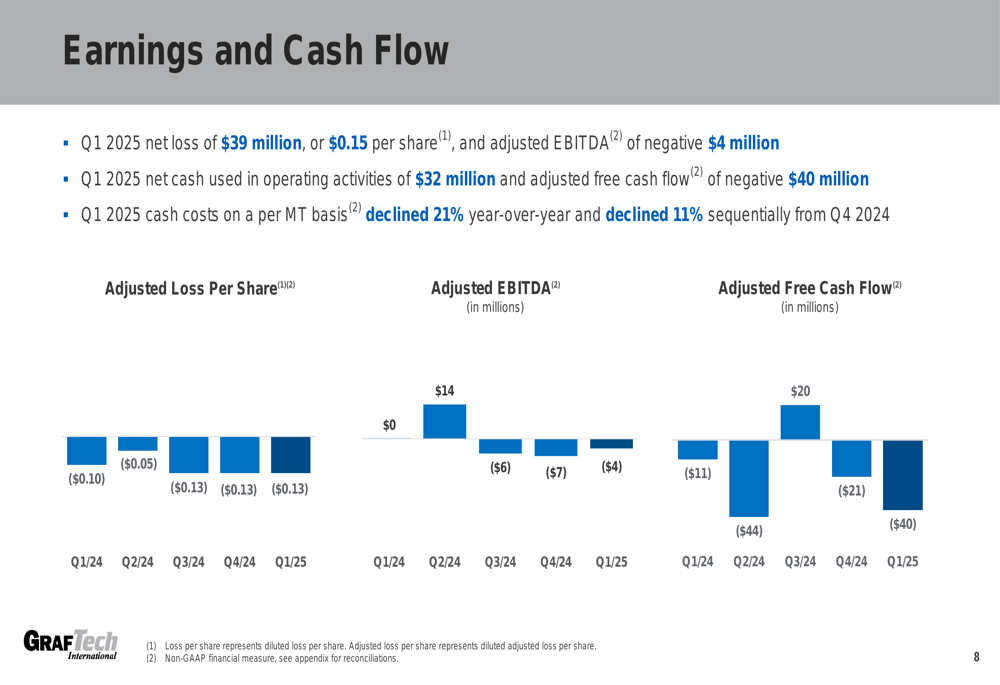

Despite operational improvements, GrafTech reported a net loss of $39 million, or $0.15 per share, for Q1 2025. Adjusted EBITDA was negative $4 million, showing a slight improvement from negative $7 million in Q4 2024, but still reflecting the challenging market environment. The company also reported negative adjusted free cash flow of $40 million for the quarter.

The following chart illustrates GrafTech’s recent earnings and cash flow performance:

On a positive note, GrafTech’s cost-cutting initiatives are showing results, with cash costs on a per MT basis declining 21% year-over-year and 11% sequentially from Q4 2024. This improvement in cost structure is crucial as the company works to return to profitability amid persistent pricing pressures.

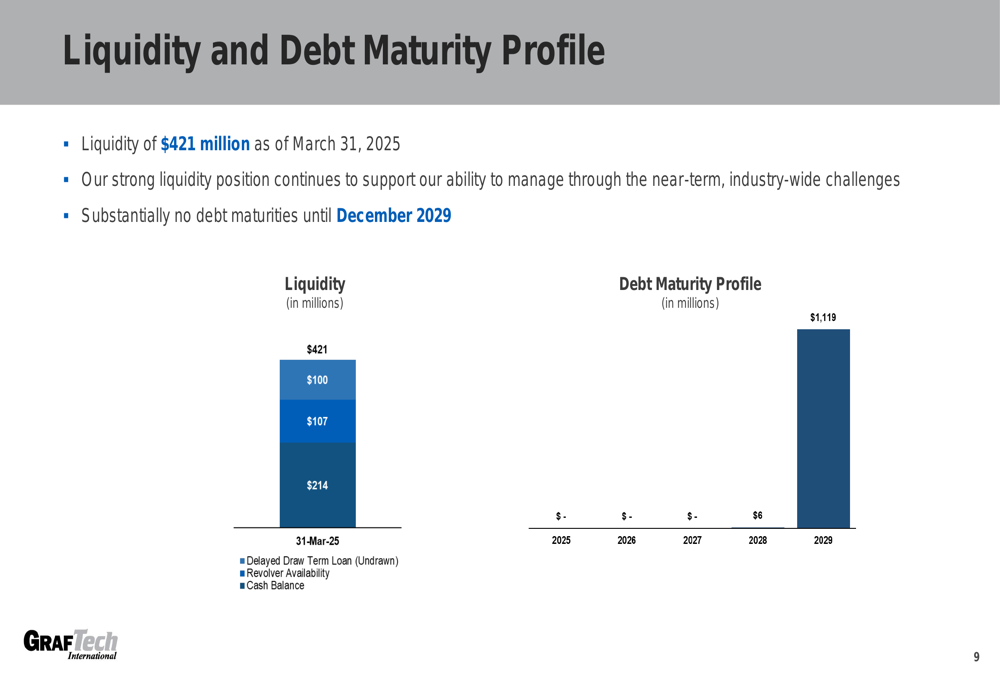

The company maintains a solid liquidity position of $421 million as of March 31, 2025, consisting of $214 million in cash, $107 million in revolver availability, and $100 million in undrawn delayed draw term loan. GrafTech faces no significant debt maturities until December 2029, when $1,119 million comes due.

Market Context

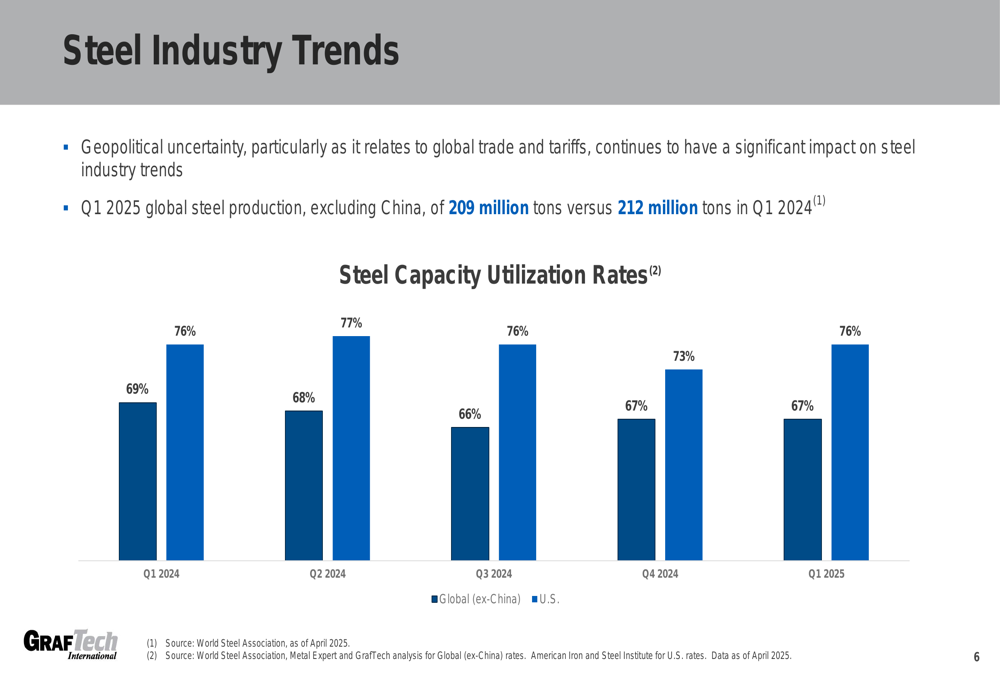

GrafTech’s performance reflects broader challenges in the global steel industry, which continues to face geopolitical uncertainty and trade policy pressures. Global steel production (excluding China) reached 209 million tons in Q1 2025, slightly down from 212 million tons in Q1 2024. Steel capacity utilization rates remained relatively stable at 67% globally (excluding China) and 76% in the U.S. for Q1 2025.

The following chart details recent steel industry capacity utilization trends:

These industry conditions continue to impact the graphite electrode market, with pricing pressure persisting despite some volume recovery. This aligns with trends observed in the company’s Q3 2024 results, where GrafTech reported similar challenges with weak pricing despite volume improvements.

Strategic Initiatives

GrafTech’s management outlined four key initiatives aimed at improving performance:

1. Leveraging customer value proposition to drive volume and market share growth

2. Optimizing order book by shifting geographic mix to regions with higher pricing

3. Executing initiatives to significantly improve all elements of cost structure

4. Proactively managing uncertainty surrounding global trade policymaking

CEO Tim Flanagan emphasized the company’s focus on accelerating profitability recovery through these strategic actions. The company’s vertical integration with needle coke production remains a key competitive advantage in the graphite electrode market.

Forward-Looking Statements

Despite near-term challenges, GrafTech expressed optimism about long-term prospects, citing several industry tailwinds:

1. A robust United States steel market

2. Ongoing shift to electric arc furnace (EAF) steelmaking, which requires graphite electrodes

3. Growing needle coke demand

The company also highlighted opportunities in the battery materials market for electric vehicles, leveraging its expertise in carbon and graphite technologies.

However, investors should note the disconnect between the company’s optimistic long-term outlook and its current financial performance. The continued net losses and negative adjusted EBITDA suggest that market recovery may take longer than previously anticipated, despite operational improvements and cost-cutting measures.

As GrafTech navigates these challenging market conditions, the focus on cost structure improvements and strategic positioning for long-term industry trends will be crucial for the company’s path back to profitability. Investors will be watching closely to see if production volume gains can eventually translate into improved financial performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.