AI is a game of kings, and OpenAI knows it

Introduction & Market Context

GrafTech International Ltd (NYSE:EAF) presented its second quarter 2025 results on July 25, showing operational improvements amid persistent financial challenges. The graphite electrode manufacturer’s stock surged 14.07% to $1.35 following the presentation, despite reporting a widened net loss, suggesting investors are focusing on the company’s improving operational metrics and strategic positioning.

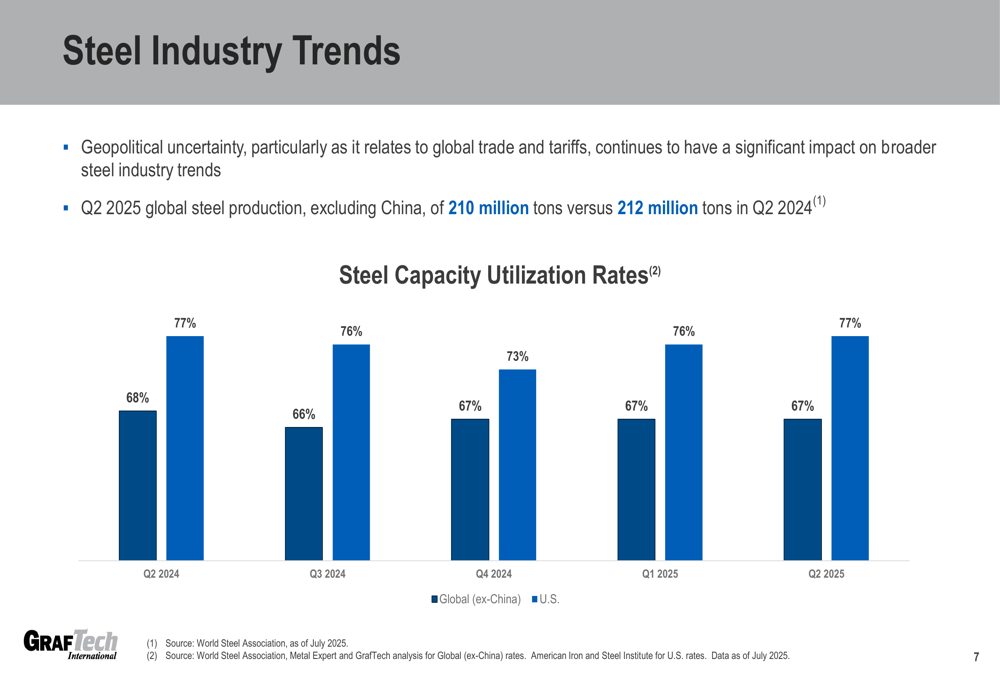

The presentation comes as the global steel industry continues to face headwinds, with Q2 2025 global steel production (excluding China) at 210 million tons, slightly below the 212 million tons produced in Q2 2024. Steel capacity utilization rates remained relatively stable at 67% globally (excluding China) and 77% in the U.S. during the quarter.

As shown in the following chart of steel industry capacity utilization rates:

Quarterly Performance Highlights

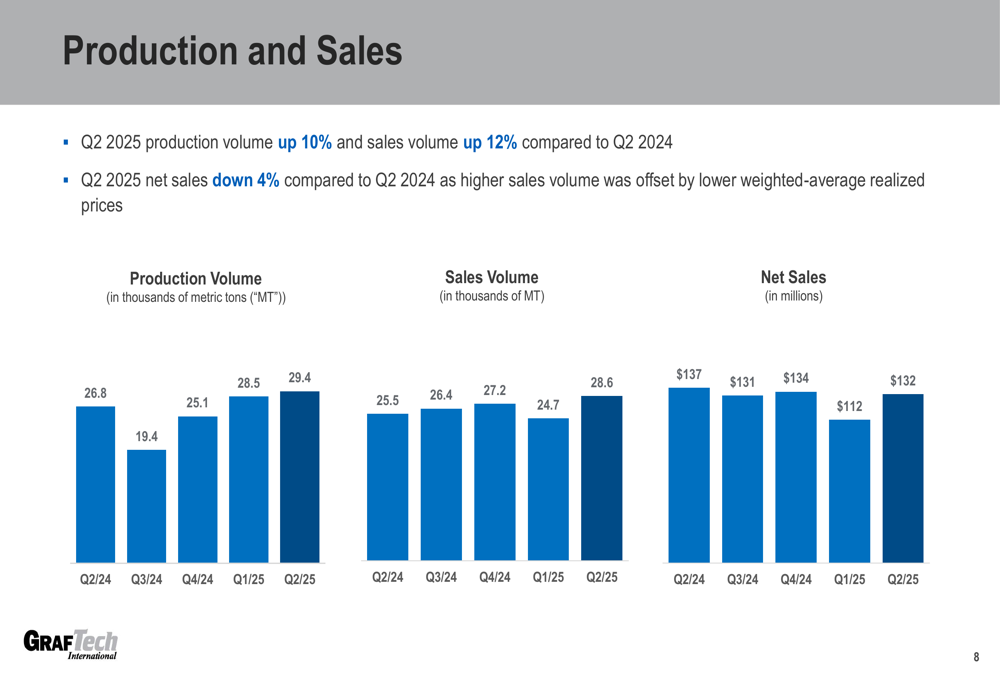

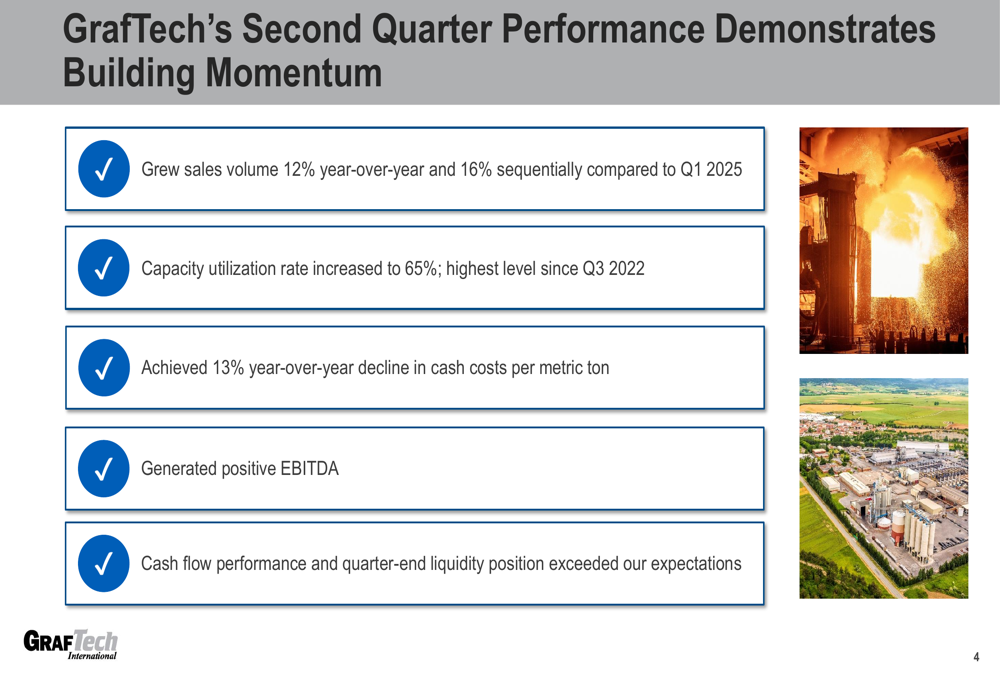

GrafTech reported significant operational improvements in Q2 2025, with sales volume increasing 12% year-over-year and 16% sequentially compared to Q1 2025. The company’s capacity utilization rate reached 65%, its highest level since Q3 2022, reflecting improved operational efficiency.

"We grew sales volume 12% year-over-year and 16% sequentially compared to Q1 2025," said Tim Flanagan, Chief Executive Officer and President, highlighting the company’s focus on volume growth amid challenging market conditions.

The company also achieved a 13% year-over-year decline in cash costs per metric ton, demonstrating progress in its cost-reduction initiatives. These operational improvements are illustrated in the production and sales volume trends:

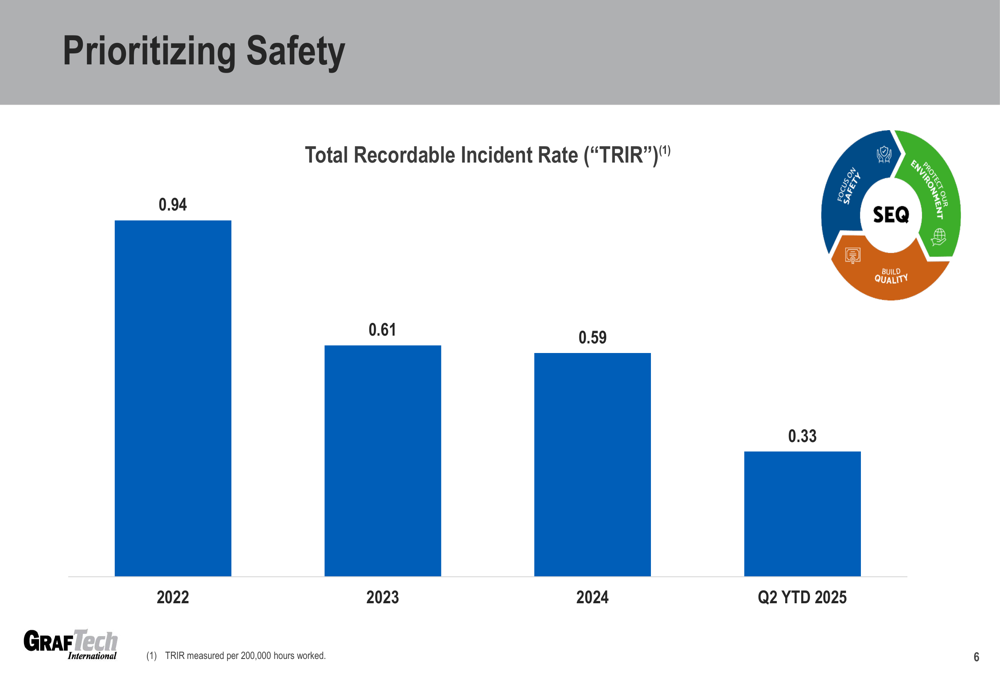

Safety performance also showed marked improvement, with the Total (EPA:TTEF) Recordable Incident Rate (TRIR) declining to 0.33 in Q2 YTD 2025, down from 0.59 in 2024 and 0.94 in 2022. This represents a continued focus on workplace safety across GrafTech’s operations.

Detailed Financial Analysis

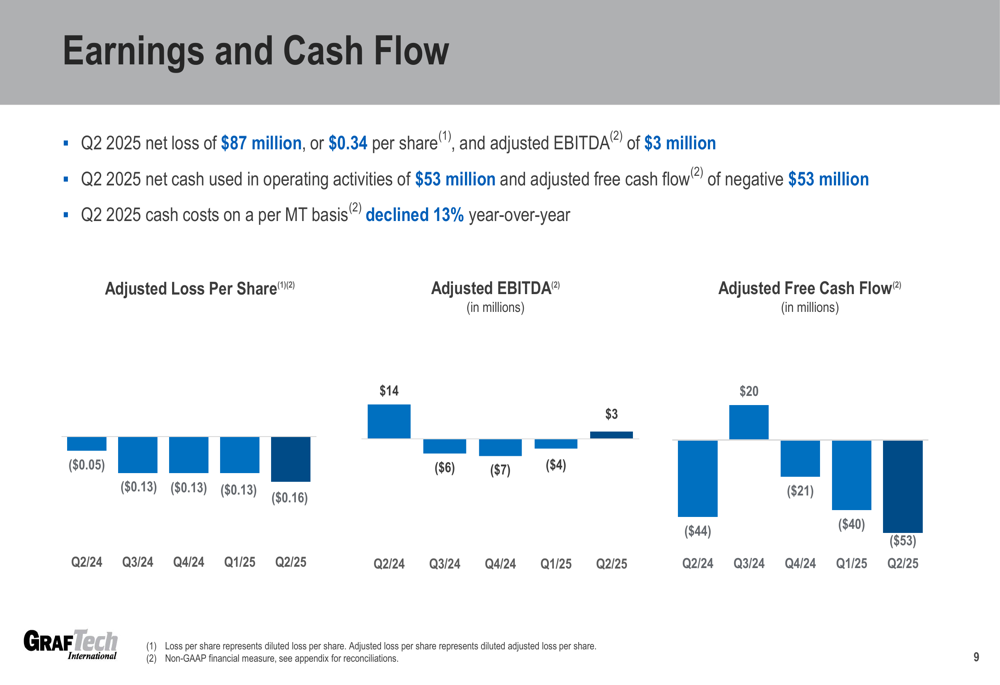

Despite operational improvements, GrafTech’s financial results remained challenged. The company reported a net loss of $87 million, or $0.34 per share, in Q2 2025, compared to a net loss of $39 million, or $0.15 per share, in Q1 2025. On an adjusted basis, the loss per share was $0.16.

Q2 2025 net sales were $132 million, down 4% compared to Q2 2024, as higher sales volume was offset by lower weighted-average realized prices. This represents a sequential improvement from Q1 2025’s $112 million in revenue.

The company did achieve positive adjusted EBITDA of $3 million in Q2 2025, an improvement from the negative $4 million reported in Q1 2025 and negative $7 million in Q4 2024. This marks the first quarter of positive EBITDA after several consecutive negative quarters, potentially signaling a turning point in the company’s financial performance.

The following chart illustrates GrafTech’s recent earnings and cash flow trends:

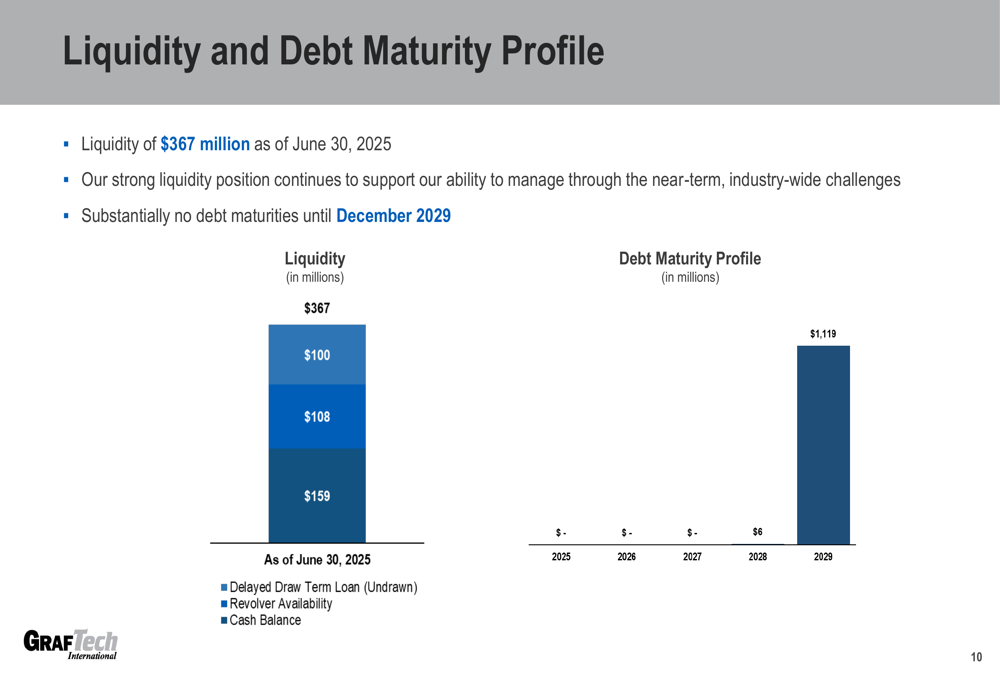

GrafTech maintained a strong liquidity position of $367 million as of June 30, 2025, consisting of $159 million in cash, $108 million in revolver availability, and $100 million in undrawn delayed draw term loan. The company has substantially no debt maturities until December 2029, providing financial flexibility to navigate current market challenges.

Strategic Initiatives

GrafTech outlined several key strategic initiatives aimed at improving its competitive position and financial performance. These include leveraging its customer value proposition to drive volume and market share growth, optimizing its order book by shifting sales to regions with higher pricing, executing cost-reduction initiatives, and managing potential impacts of global trade policies.

The company’s Q2 2025 performance highlights demonstrate progress on these initiatives:

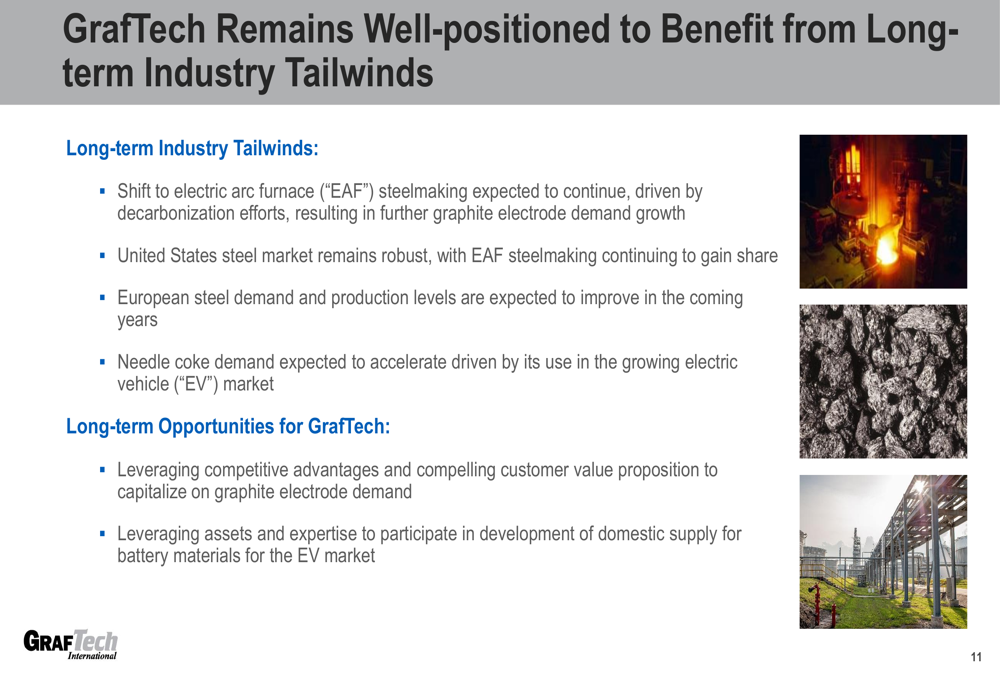

Looking ahead, GrafTech is positioning itself to capitalize on long-term industry trends, including the continued shift to electric arc furnace (EAF) steelmaking, robust U.S. steel market conditions, expected improvement in European steel demand, and accelerating needle coke demand driven by the growing electric vehicle market.

Forward-Looking Statements

GrafTech emphasized its competitive advantages as it navigates current challenges, including its position as an industry leader in high-quality graphite electrode production, vertical integration into petroleum needle coke, and focus on value-added services for customers.

"We are executing actions to accelerate our path back to normalized levels of profitability," management stated in the presentation, highlighting the company’s focus on improving financial performance while maintaining operational excellence.

The market’s positive reaction to the presentation, with the stock rising 14.07%, suggests investors are encouraged by the operational improvements and strategic positioning despite the widened net loss. However, the stock experienced a 5.19% decline in after-hours trading, indicating some uncertainty about the company’s near-term prospects.

As GrafTech continues to execute its strategy, investors will be watching for sustained volume growth, further cost reductions, and most importantly, improvement in the company’s bottom line in coming quarters. The company’s ability to capitalize on its competitive advantages while navigating challenging market conditions will be crucial to its long-term success.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.