Bank CEOs meet with Trump to discuss Fannie Mae and Freddie Mac - Bloomberg

Introduction & Market Context

Graphic Packaging Holding Company (NYSE:GPK) reported a challenging first quarter for 2025, with declining financial performance across key metrics and a significant downward revision to its full-year guidance. The packaging manufacturer’s shares fell 5.1% in premarket trading following the May 1 earnings presentation, reflecting investor concerns about the company’s near-term outlook.

The results come amid what the company describes as "economic uncertainty" affecting customer launch plans and "consumers pulling back spending" as they search for value. These headwinds have materialized despite the company’s previous optimism expressed during its Q3 2024 earnings call, where it had anticipated consistent performance for 2025.

Quarterly Performance Highlights

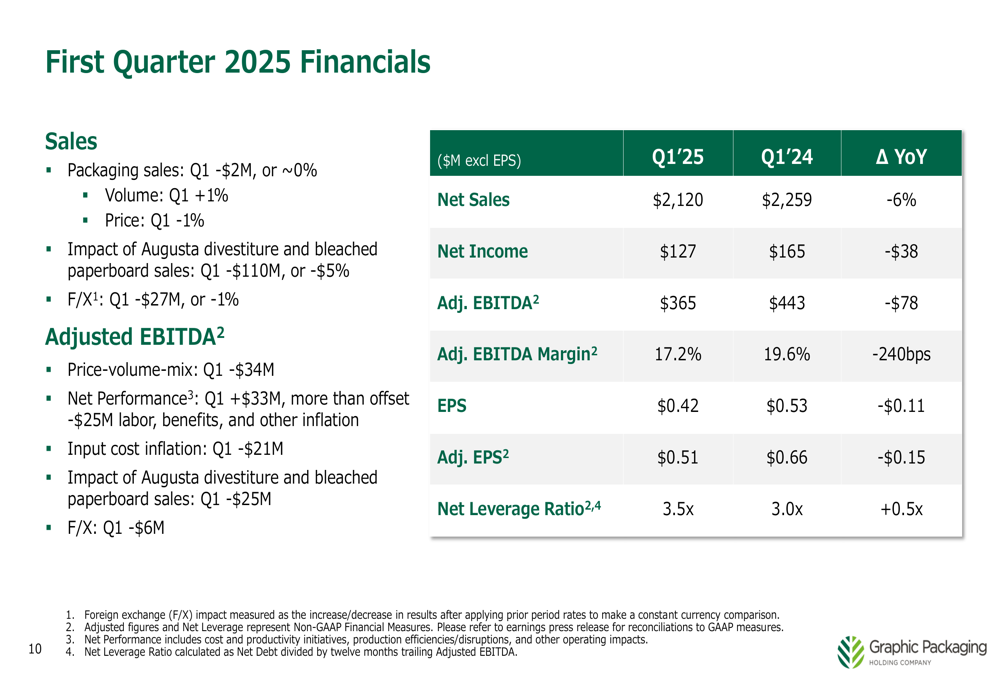

Graphic Packaging reported Q1 2025 net sales of $2,120 million, representing a 6% year-over-year decline from $2,259 million in Q1 2024. Net income fell to $127 million from $165 million in the prior-year period, while adjusted EBITDA dropped to $365 million from $443 million, with margins contracting 240 basis points to 17.2%.

As shown in the following financial summary:

The company’s adjusted earnings per share came in at $0.51, down from $0.66 in Q1 2024, while its net leverage ratio increased to 3.5x from 3.0x a year earlier. Despite these challenges, Graphic Packaging did report modest volume growth of 1% year-over-year, with international markets showing stronger performance at +3% while Americas declined by 1%.

The company maintains a diversified product portfolio across multiple consumer sectors, which provides some resilience against category-specific downturns. Food and Health & Beauty segments showed improvement, while Beverage performed weaker.

The following breakdown illustrates the company’s diversified presence across consumer categories:

Revised Guidance & Outlook

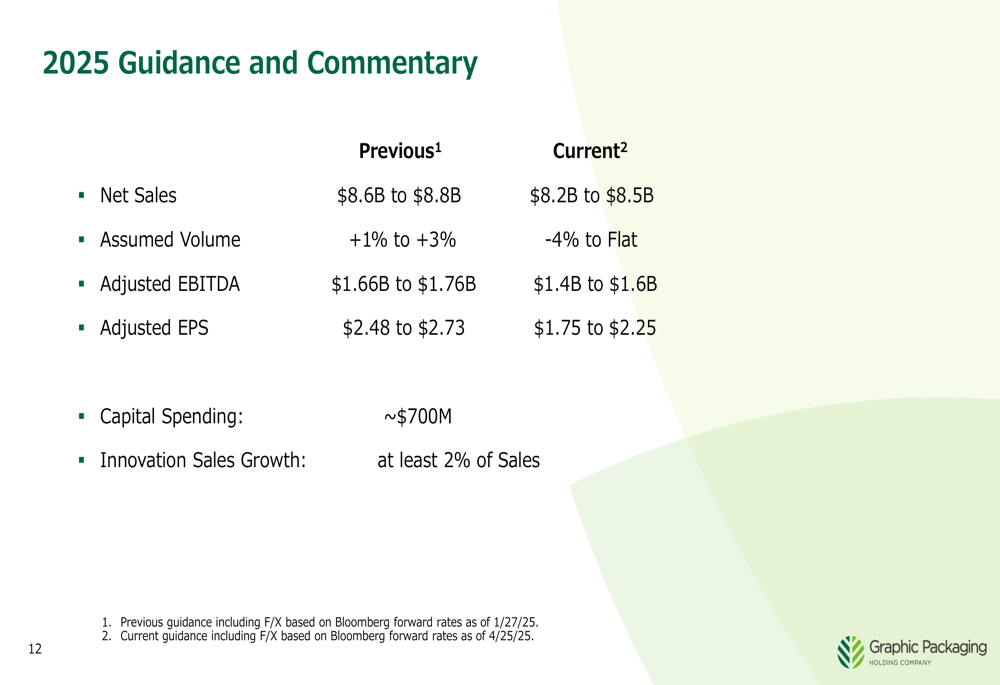

In a significant shift from previous projections, Graphic Packaging substantially lowered its full-year 2025 guidance across all key metrics. The company now expects net sales between $8.2 billion and $8.5 billion, down from its previous range of $8.6 billion to $8.8 billion. Volume expectations were dramatically reduced from growth of 1-3% to a range of -4% to flat.

The guidance revision extends to profitability metrics as well, with adjusted EBITDA now projected at $1.4 billion to $1.6 billion (previously $1.66 billion to $1.76 billion) and adjusted EPS at $1.75 to $2.25 (previously $2.48 to $2.73).

The following slide details these significant revisions:

Management cited several factors contributing to the weaker outlook, including consumers’ search for value, increased promotional activity, growing private label share, continued inflation risk, and uncertainty in CPG and QSR volumes. The company has announced price increases in response to recent input cost inflation, but these appear insufficient to offset the volume and margin pressures.

Strategic Initiatives

Despite near-term challenges, Graphic Packaging continues to advance several strategic initiatives aimed at long-term growth. The company highlighted its Waco, Texas recycled paperboard investment, which is moving toward completion with startup planned for Q4 2025. This facility is expected to contribute incremental EBITDA of $80 million in 2026 and another $80 million in 2027.

The company also announced the closure of its Middletown, Ohio recycled paperboard manufacturing facility as part of ongoing operational optimization. Additionally, a new $1.5 billion share repurchase authorization was approved, bringing the total available authorization to $1.865 billion.

Innovation remains a key focus, with the company reporting $44 million in innovation sales growth during the quarter. Graphic Packaging continues to target addressable market opportunities totaling approximately $15 billion across various packaging segments.

The company showcased its EnviroClip™ Beam innovation, a paperboard clip-style multi-pack carrier for PET bottles designed as an alternative to plastic ring carriers and shrink wrap:

This innovation addresses a global market opportunity estimated at $1.5 billion, primarily replacing plastic and plastic film packaging solutions. The company noted that European regulations are driving new growth opportunities in beverage packaging, creating additional tailwinds for sustainable packaging solutions.

Long-term Vision

Looking beyond current headwinds, Graphic Packaging maintained its commitment to its Vision 2030 strategy, which aims to position the company as a global leader in sustainable consumer packaging. The long-term financial model targets low-single-digit annual sales growth, mid-single-digit adjusted EBITDA growth, and high-single-digit adjusted EPS growth.

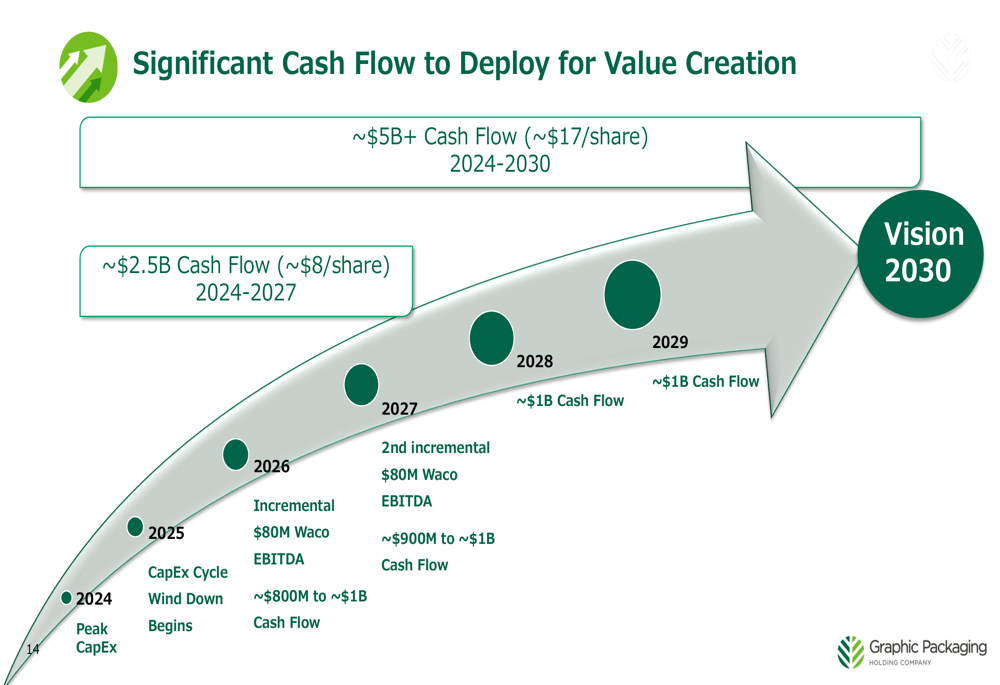

The company projects significant cash flow generation of approximately $5 billion from 2024 to 2030, equivalent to about $17 per share. This cash flow is expected to increase substantially after the completion of the capital-intensive Waco facility, with annual cash flow projected to reach approximately $800 million to $1 billion by 2026.

As illustrated in this cash flow projection timeline:

Management emphasized that "After Waco, Graphic Packaging has the assets, the capabilities, and the team needed to achieve Vision 2030 financial goals, and to generate cash well in excess of reinvestment needs." The company plans to deploy this cash for dividend growth, share repurchases, debt reduction to achieve investment grade ratings, and potential tuck-in acquisitions.

While Graphic Packaging’s long-term strategy remains intact, the significant downward revision to near-term guidance suggests a challenging path ahead as the company navigates economic uncertainty and changing consumer behaviors. Investors will likely focus on whether the company can stabilize performance in upcoming quarters and demonstrate progress toward its Vision 2030 objectives despite the current headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.