Chip stocks fall with Nvidia after data center rev disappointment

Graphic Packaging Holding Company (NYSE:GPK) presented its second quarter 2025 earnings results on July 29, showing modest volume growth but continued margin pressure as the company navigates a challenging market environment while investing in future capabilities.

Quarterly Performance Highlights

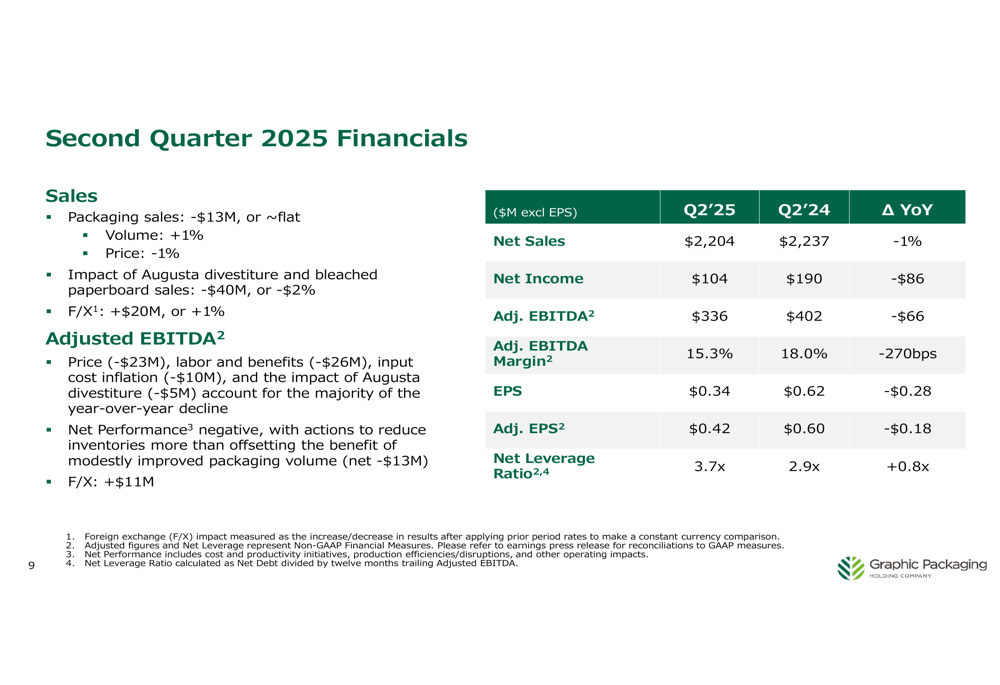

Graphic Packaging reported Q2 2025 net sales of $2,204 million, representing a 1% year-over-year decline from $2,237 million in Q2 2024. The company’s net income fell to $104 million from $190 million in the prior year period, while adjusted EBITDA decreased to $336 million from $402 million, resulting in an adjusted EBITDA margin of 15.3%, down 270 basis points from 18.0% a year ago.

The company’s packaging sales remained relatively flat, with a 1% increase in volume offset by a 1% decrease in pricing. The divestiture of Augusta and reduced bleached paperboard sales negatively impacted revenue by $40 million or 2%, while favorable foreign exchange contributed $20 million or 1%.

Earnings per share fell to $0.34 from $0.62 in Q2 2024, while adjusted EPS declined to $0.42 from $0.60. The company’s net leverage ratio increased to 3.7x from 2.9x a year earlier, reflecting higher debt levels as the company continues to invest in strategic initiatives.

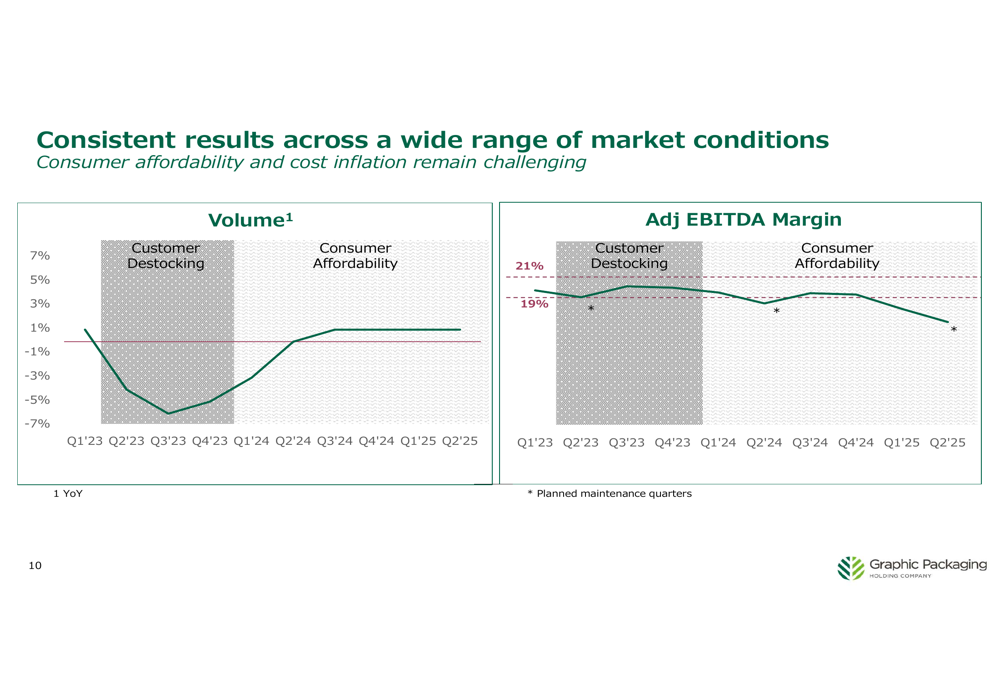

The volume trend shows signs of stabilization after previous periods of customer destocking and consumer affordability challenges, with a return to modest growth in Q2 2025.

Strategic Initiatives and Innovation

Graphic Packaging continues to focus on innovation as a key growth driver, highlighting a $15 billion addressable market opportunity across various packaging categories. The company reported innovation sales growth of $61 million in the quarter, maintaining its target of innovation contributing more than 2% to annual sales growth.

A notable example of the company’s innovation efforts is its new coffee pod packaging solution, which targets the $2.0 billion global strength packaging market. The redesigned packaging offers sustainability benefits by replacing plastic, bleached paperboard, and corrugated materials, while also improving functionality and convenience. The new design increases pallet efficiency from 80 to 104 salable units per pallet.

The company’s Waco, Texas recycled paperboard investment remains on track for startup in Q4 2025, although final design and completion costs are higher than initially projected. Management noted that these increased costs will not impact the expected 2025 free cash flow. Additionally, the company closed its Middletown, Ohio recycled paperboard facility on May 27, 2025, as part of ongoing operational optimization.

In a positive development for the company’s sustainability initiatives, the Recycled Materials Association has added paper cups to recycling specifications, which Graphic Packaging views as a key development for collection and circular economy efforts.

Capital Allocation and Shareholder Returns

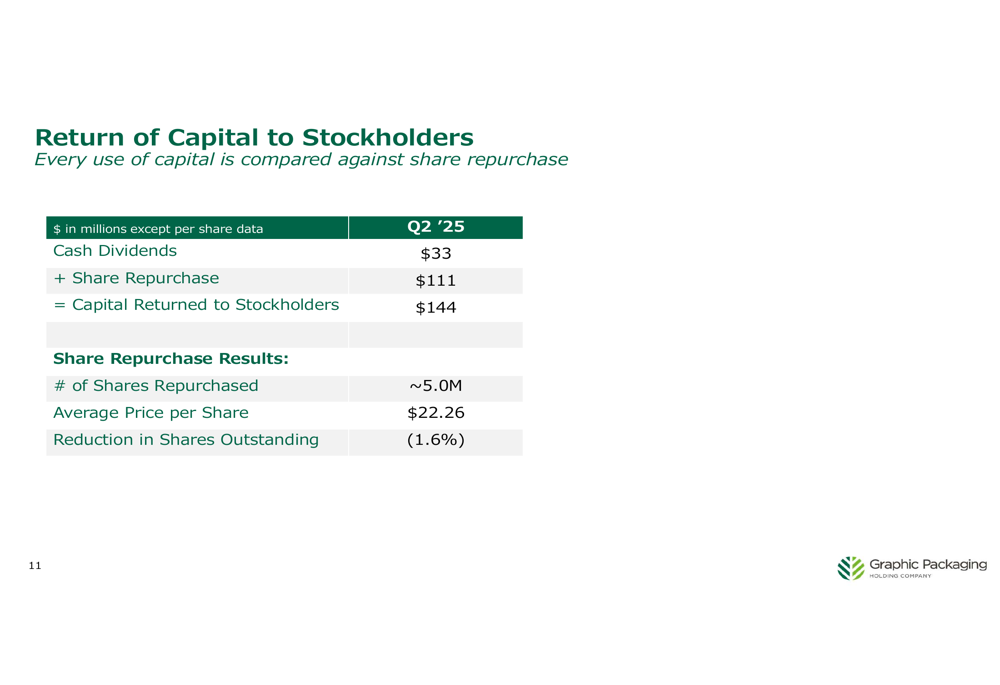

Despite the earnings decline, Graphic Packaging continued its share repurchase program, buying back approximately 5.0 million shares at an average price of $22.26 during Q2 2025, for a total of $111 million. Combined with $33 million in cash dividends, the company returned $144 million to stockholders in the quarter, reducing shares outstanding by 1.6%.

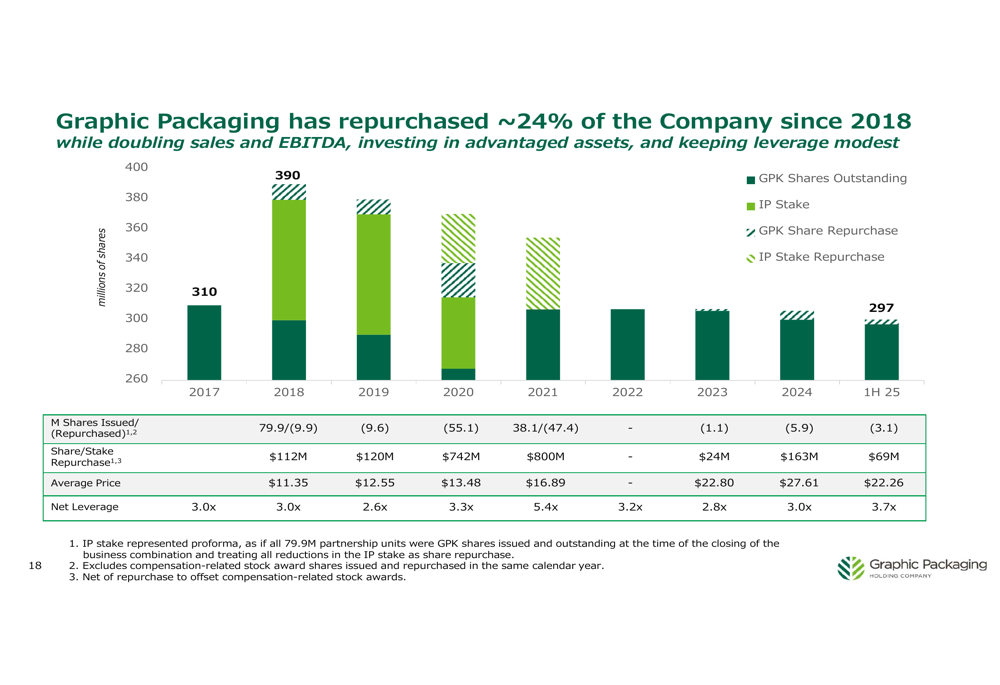

Since 2018, Graphic Packaging has repurchased approximately 24% of its shares while doubling sales and EBITDA, investing in assets, and maintaining what management describes as modest leverage. The company’s net leverage has increased from 2.8x at the end of 2023 to 3.7x at the end of Q2 2025.

Forward Guidance and Vision 2030

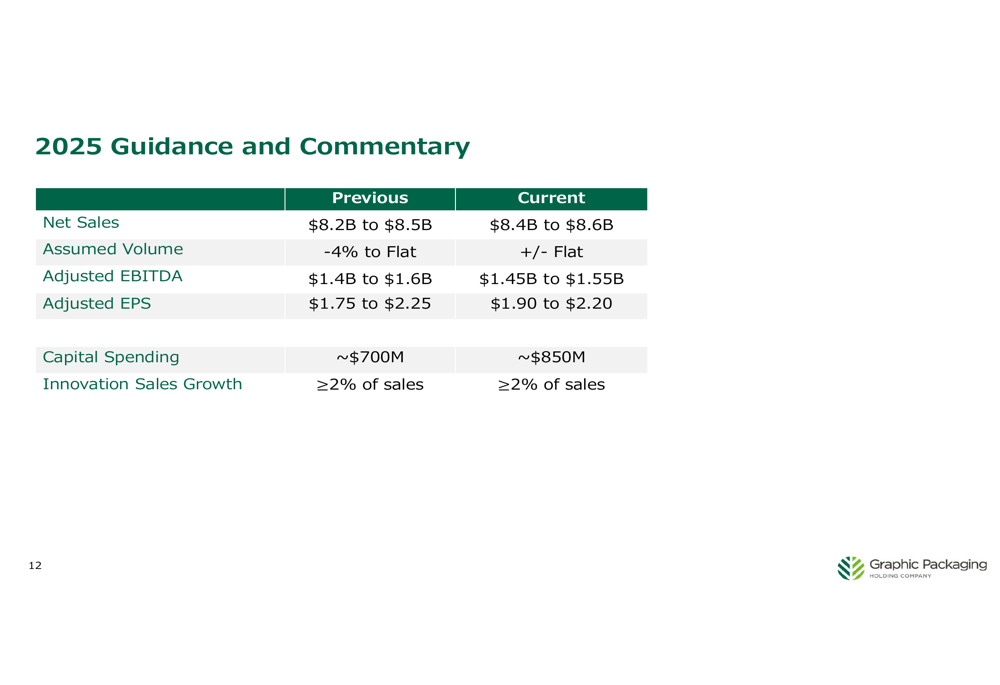

Graphic Packaging raised its 2025 net sales guidance to $8.4-$8.6 billion from the previous range of $8.2-$8.5 billion. The company also narrowed its adjusted EBITDA guidance to $1.45-$1.55 billion from $1.4-$1.6 billion, and adjusted EPS guidance to $1.90-$2.20 from $1.75-$2.25.

Capital spending guidance was increased to approximately $850 million from the previous estimate of $700 million, reflecting higher investments in the Waco facility. The company expects to maintain its innovation sales growth target of more than 2% of sales.

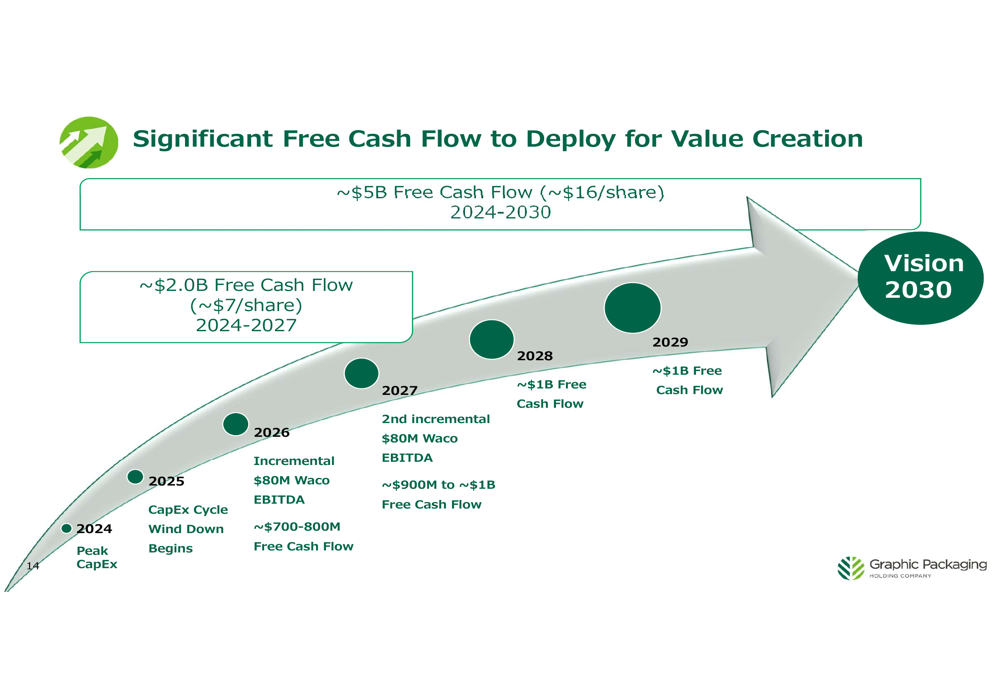

Looking further ahead, Graphic Packaging’s Vision 2030 strategy outlines a financial model targeting low-single-digit annual sales growth, mid-single-digit adjusted EBITDA growth, and high-single-digit adjusted EPS growth. The company expects normalized capital expenditures to be approximately 5% of sales after 2025.

The long-term plan projects approximately $5 billion in free cash flow (about $16 per share) from 2024 to 2030, with annual free cash flow expected to increase from $700-800 million in 2026 to approximately $1 billion by 2028.

Market Context

The Q2 2025 results come after a challenging first quarter, where Graphic Packaging missed analyst expectations with an adjusted EPS of $0.51 versus a $0.59 forecast, leading to a 14.48% stock drop. The improved volume trends in Q2 and raised sales guidance appear to have been received positively by investors, with the stock trading up 3.76% to $24.00 in premarket trading following the earnings release.

The company’s diversified consumer packaging portfolio, which spans food (38% of sales), beverage (25%), foodservice (21%), household (12%), and health & beauty (4%), provides some resilience against market volatility. However, the persistent margin pressure highlights ongoing challenges in the operating environment.

As Graphic Packaging continues to execute its Vision 2030 strategy, investors will likely focus on the company’s ability to restore margins while managing higher debt levels and delivering on its innovation and sustainability initiatives. The successful completion and startup of the Waco facility in Q4 2025 will be a critical milestone in the company’s strategic roadmap.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.