Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Griffon Corporation (NYSE:GFF) recently presented its Q2 FY25 investor slides highlighting the company’s financial performance and strategic direction. However, the optimistic tone of the presentation stands in contrast to the company’s subsequent Q3 earnings release, which triggered a significant 13.75% stock decline to $71.02 as of August 6, 2025.

The presentation showcases Griffon’s transformation into a focused enterprise with two core segments: Home and Building Products (HBP) and Consumer and Professional Products (CPP). While the slides emphasize strong margins and strategic portfolio reshaping, recent market performance suggests investors are concerned about revenue challenges and segment-specific headwinds.

Executive Summary

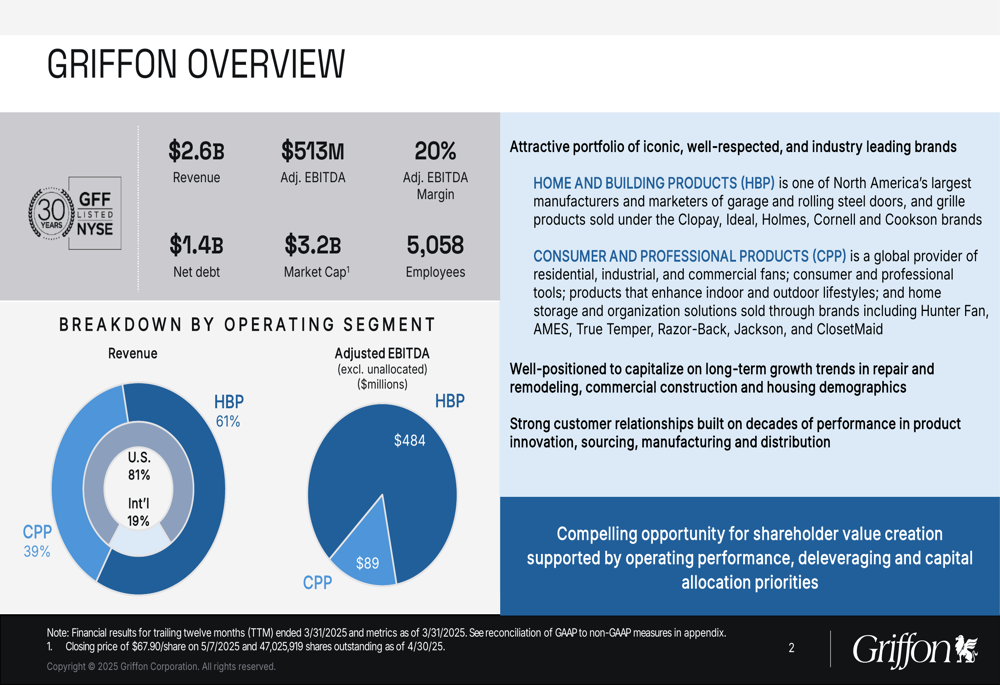

Griffon’s investor presentation outlines a company with $2.6 billion in revenue, $513 million in adjusted EBITDA (20% margin), and a market capitalization of $3.2 billion. The company maintains a net debt position of $1.4 billion with a leverage ratio of 2.6x, improved from 2.8x in FY21.

The business is structured around two segments: Home and Building Products, contributing 61% of revenue with an impressive 31% EBITDA margin, and Consumer and Professional Products, accounting for 39% of revenue with a 9% EBITDA margin.

As shown in the following company overview:

However, Griffon’s Q3 earnings release revealed a revenue miss of $614 million against analyst expectations of $651.91 million, along with a $244 million pretax charge for goodwill impairment. The company has subsequently revised its full-year revenue expectation downward to $2.5 billion from the $2.6 billion highlighted in the presentation.

Quarterly Performance Highlights

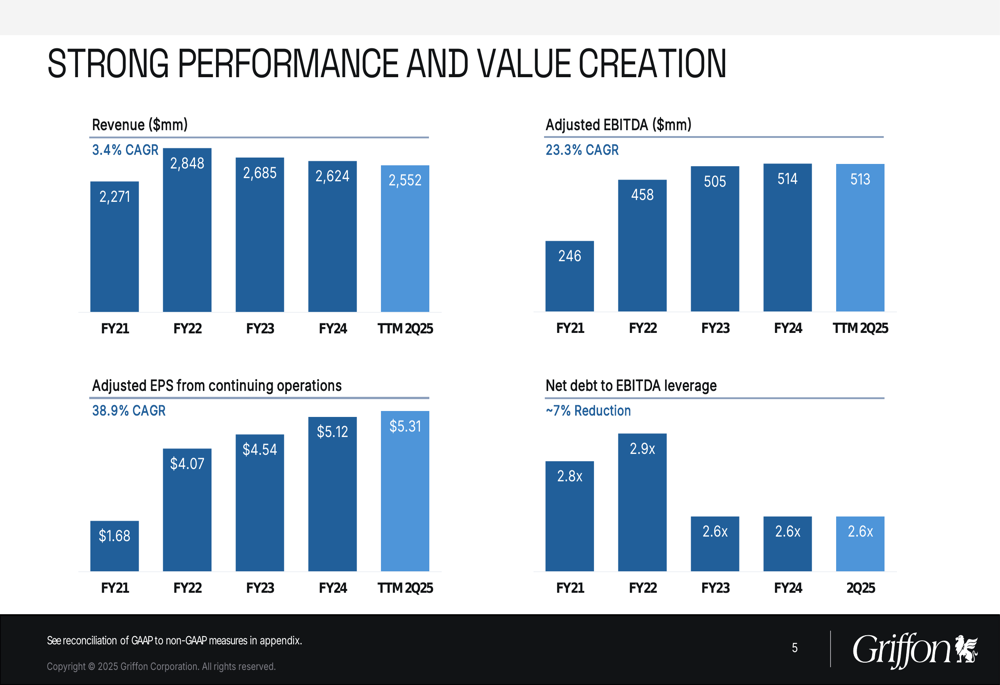

The presentation emphasizes Griffon’s financial progress, with revenue growing from $2,271 million in FY21 to $2,552 million in the trailing twelve months ending Q2 FY25. Adjusted EBITDA more than doubled during this period, from $246 million to $513 million, while adjusted EPS from continuing operations increased from $1.68 to $5.31.

These performance metrics are illustrated in the following chart:

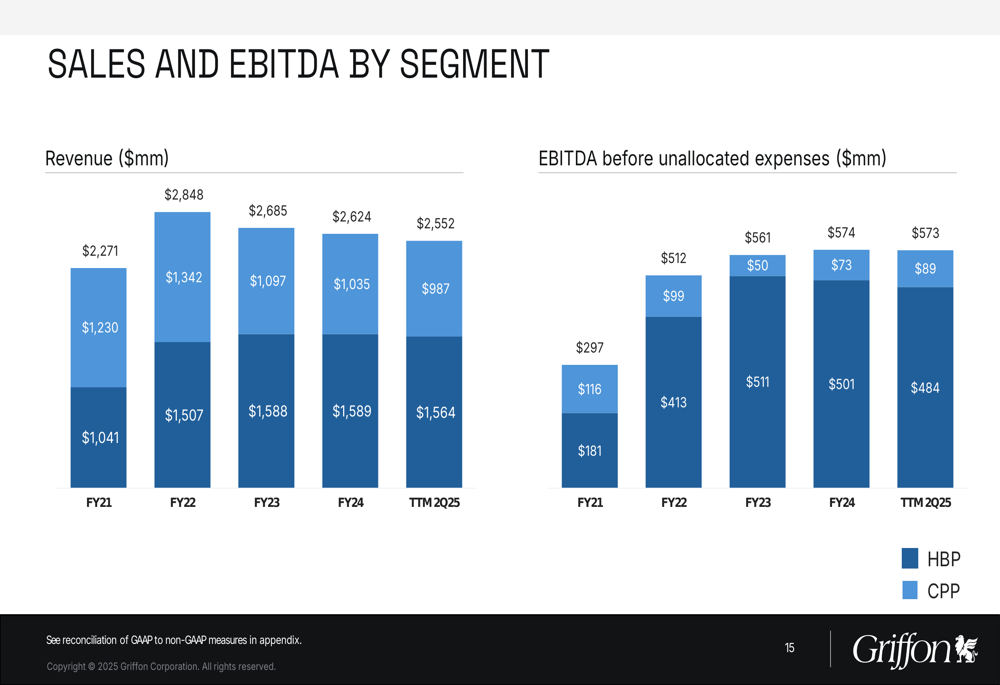

Segment performance reveals diverging trajectories. The Home and Building Products segment has demonstrated consistent strength, with revenue stable at approximately $1.6 billion and EBITDA of $484 million, yielding a 31% margin. This segment primarily serves residential repair and remodel (49%) and commercial (42%) markets, with minimal exposure to new residential construction (9%).

The Consumer and Professional Products segment has faced more challenges, with revenue declining from $1,230 million in FY21 to $987 million in TTM Q2 FY25. However, EBITDA has shown recent improvement, reaching $89 million with a 9% margin.

The following chart details sales and EBITDA trends by segment:

Strategic Initiatives

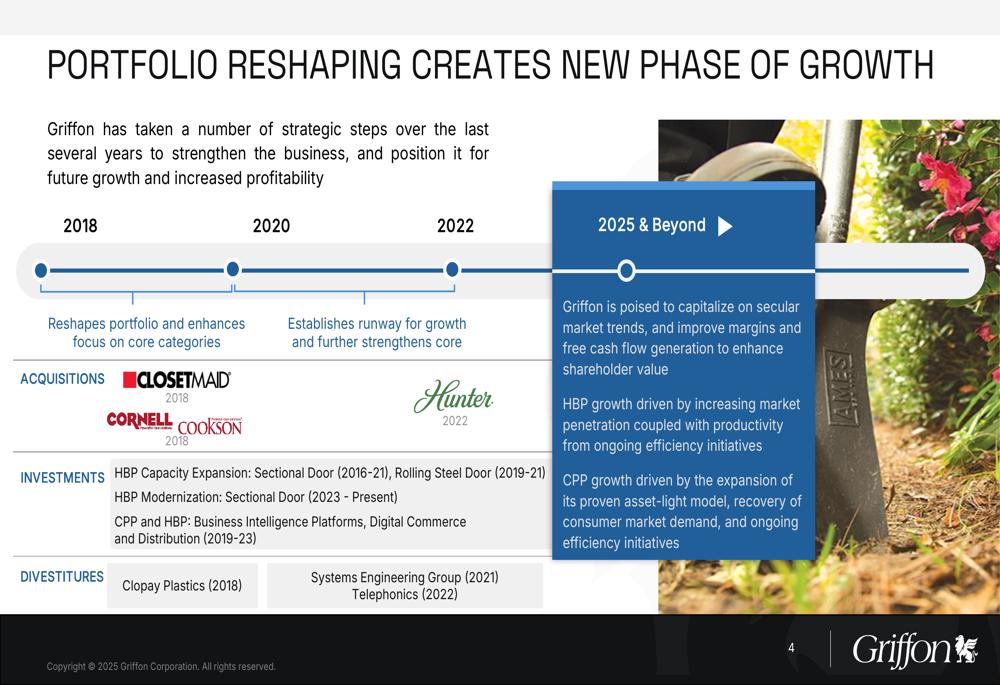

Griffon’s presentation emphasizes its portfolio transformation through strategic acquisitions and divestitures. Since 2018, the company has acquired ClosetMaid and Hunter to strengthen its core businesses while divesting Clopay Plastics, Systems Engineering Group, and Telephonics to focus on higher-margin opportunities.

The company’s strategic roadmap is illustrated below:

This portfolio reshaping has created a strong brand presence across both segments. In Home and Building Products, Griffon offers leading brands like Clopay, Cornell, and Cookson in residential and commercial garage doors. The Consumer and Professional Products segment features recognized brands including AMES, ClosetMaid, Hunter, and True Temper across lawn and garden, storage, and outdoor décor categories.

The company’s brand portfolio is showcased in the following image:

Forward-Looking Statements

Griffon’s presentation outlines several macroeconomic trends expected to drive product demand, including elevated repair and remodel activity, growing commercial construction, housing underbuilding, increasing household formations among millennials and Gen Z, and expanding outdoor living trends.

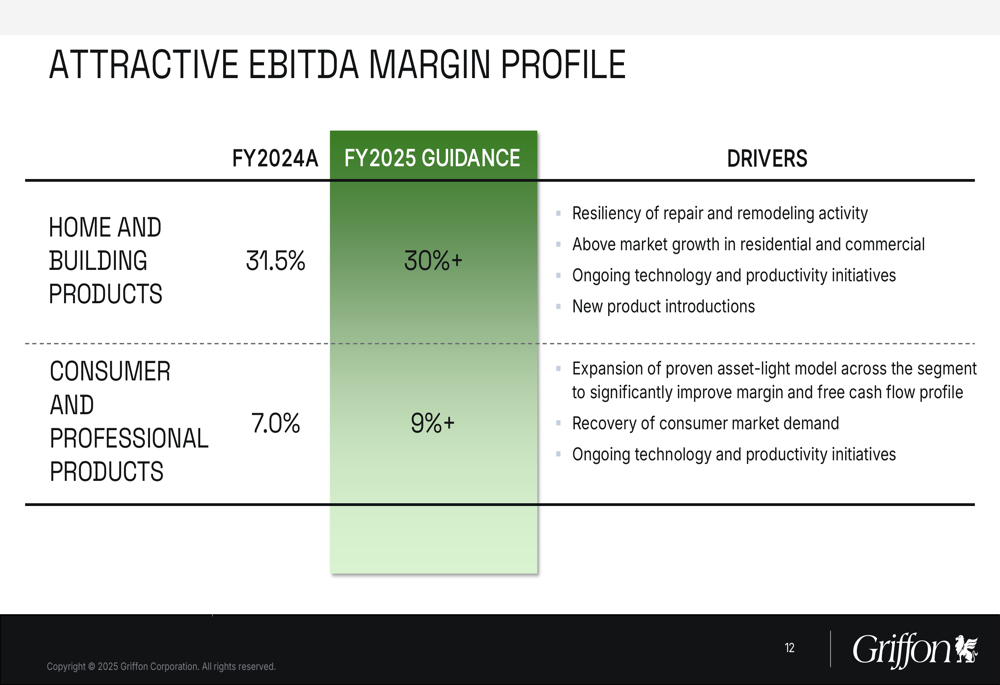

For FY2025, the company projects continued strong margins, with HBP expected to maintain 30%+ EBITDA margins and CPP targeting 9%+ EBITDA margins. However, the Q3 earnings call revealed more cautious guidance, with full-year revenue expectations reduced to $2.5 billion while maintaining EBITDA guidance of $575-600 million.

The company’s margin profile and drivers are detailed below:

CEO Ron Kramer emphasized during the Q3 earnings call the company’s commitment to its global sourcing model despite challenges, stating, "We have the best brands, and we’re committed to our global sourcing asset-light model." He also highlighted expectations of generating over $1 billion in free cash flow over the next two fiscal years.

Detailed Financial Analysis

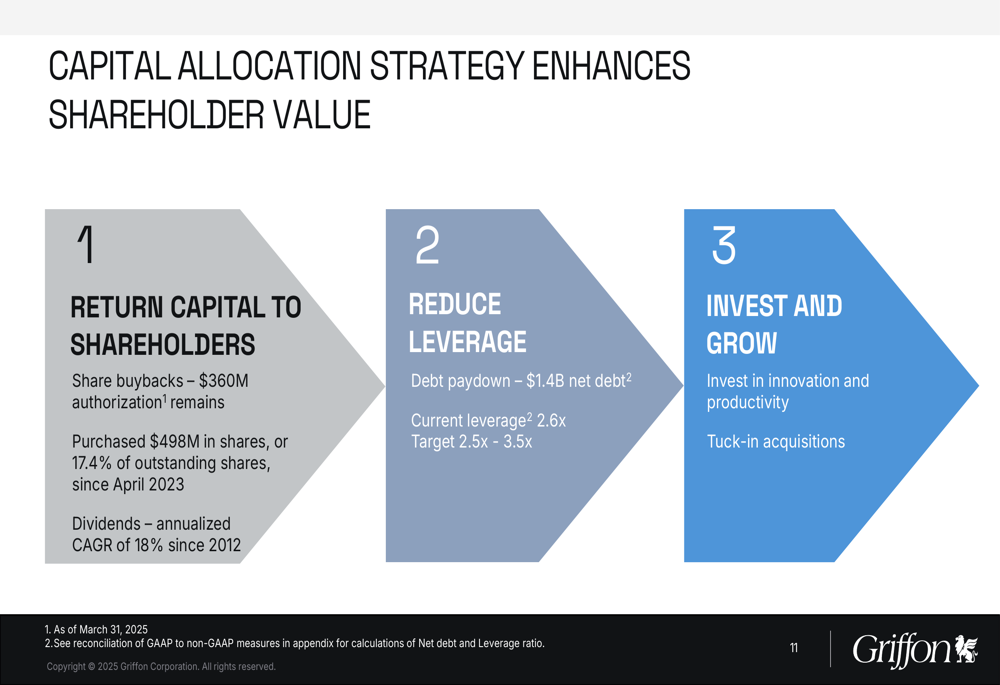

Griffon’s capital allocation strategy focuses on three key areas: returning capital to shareholders, reducing leverage, and investing for growth. The company has an active share repurchase program with $360 million remaining authorization, having purchased $498 million in shares since April 2023. Dividends have grown at an 18% CAGR since 2012.

The company has reduced net debt to $1.4 billion with a leverage ratio of 2.6x, within its target range of 2.5x-3.5x. Investment priorities include innovation, productivity improvements, and tuck-in acquisitions to complement organic growth.

This capital allocation approach is illustrated in the following slide:

Despite the optimistic presentation, Griffon faces several challenges highlighted in the Q3 earnings call, including tariffs and geopolitical tensions affecting supply chains, weak consumer demand in key segments, and macroeconomic pressures from inflation and interest rates. The Consumer and Professional Products segment appears particularly vulnerable to these headwinds.

The 13.75% stock decline following Q3 results suggests investors are concerned about the company’s ability to navigate these challenges while maintaining its financial targets. However, with a P/E ratio of 16.25 and strong operational cash flow, Griffon may present value for investors who believe in the company’s long-term strategy and brand strength.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.