Trump meets Zelenskiy, says Putin wants war to end, mulls trilateral talks

Introduction & Market Context

Grove Collaborative Holdings Inc (NYSE:GROV) presented its second quarter 2025 financial results on August 7, 2025, highlighting the company’s ongoing transformation efforts amid challenging market conditions. The sustainable consumer products company continues to navigate a strategic shift from its environmental-focused origins to a broader health and wellness positioning.

The presentation comes as Grove’s stock trades near $1.29, down 2.27% on the day and significantly below its 52-week high of $1.95. The company is working to stabilize its business after several quarters of revenue declines, with a focus on sequential improvement and eventual return to year-over-year growth.

Quarterly Performance Highlights

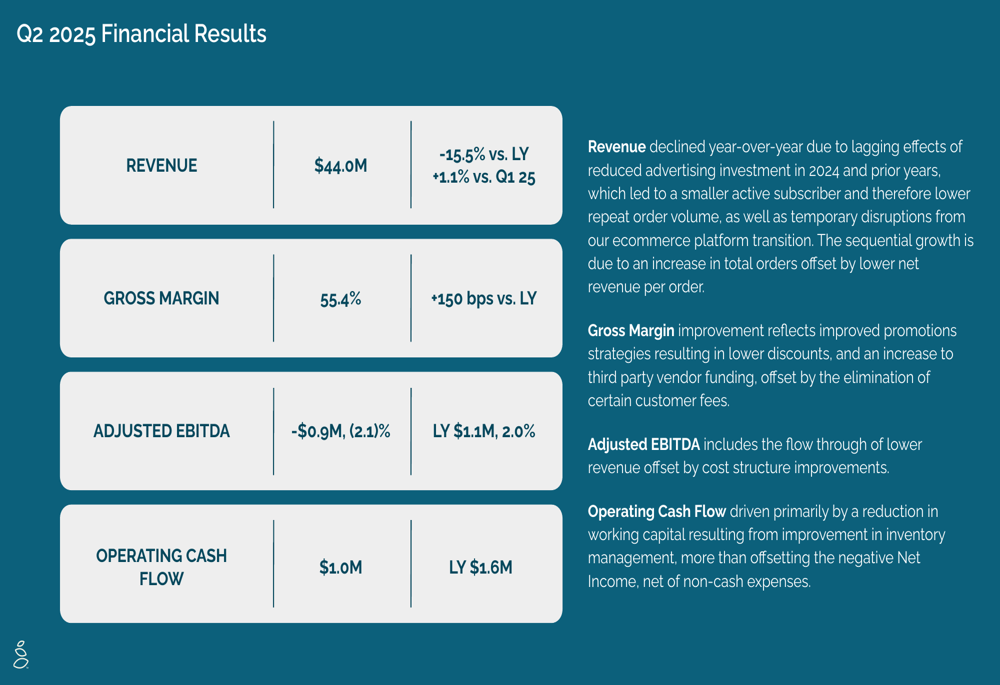

Grove reported Q2 2025 revenue of $44.0 million, representing a 15.5% decline year-over-year but a modest 1.1% sequential increase from Q1 2025. The company achieved a gross margin of 55.4%, improving 150 basis points compared to the same period last year.

As shown in the following financial results summary:

Adjusted EBITDA for the quarter was negative $0.9 million (-2.1%), compared to positive $1.1 million (2.0%) in the prior year period. Despite the EBITDA decline, the company maintained positive operating cash flow of $1.0 million, though this was down from $1.6 million in Q2 2024.

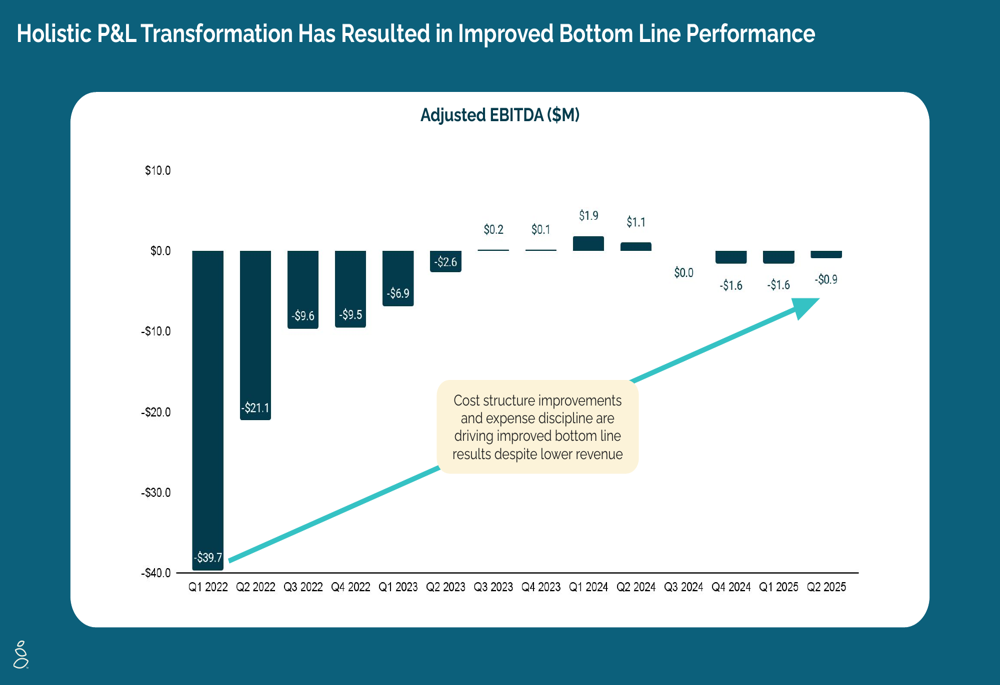

The company’s holistic P&L transformation has shown significant improvement over a multi-year period, as illustrated in this chart of quarterly Adjusted EBITDA performance:

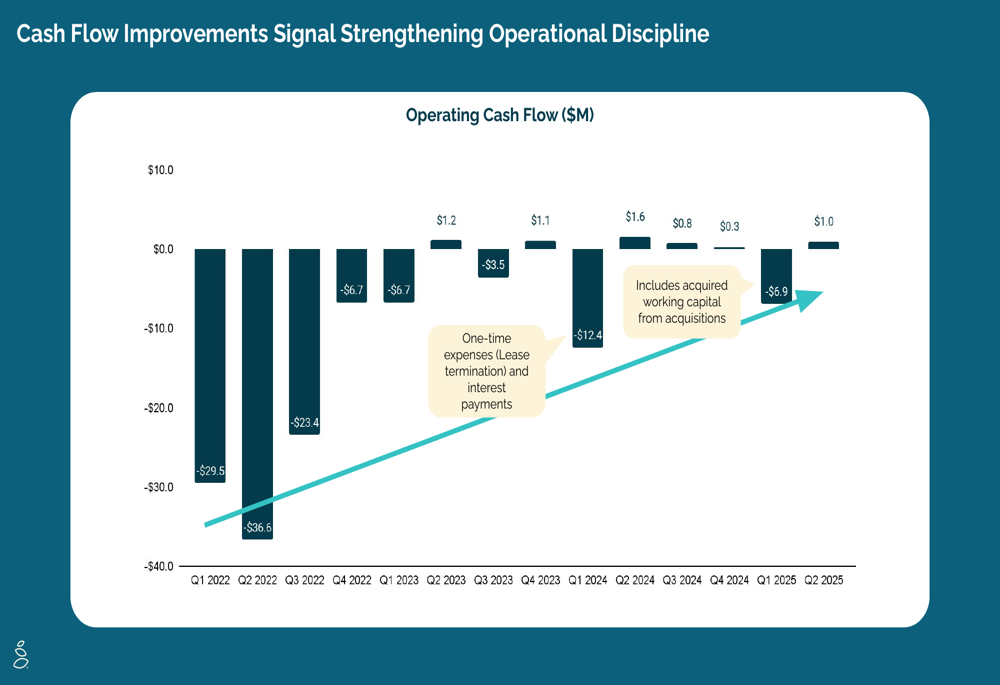

Similarly, Grove’s cash flow has demonstrated a trend toward operational discipline, with consistent positive operating cash flow in recent quarters:

Transformation Strategy

Grove’s presentation emphasized its strategic pivot from focusing primarily on environmental sustainability to a dual emphasis on both environmental and human health. This shift aims to better serve what the company identifies as 57 million conscientious consumers seeking healthier, planet-friendly products.

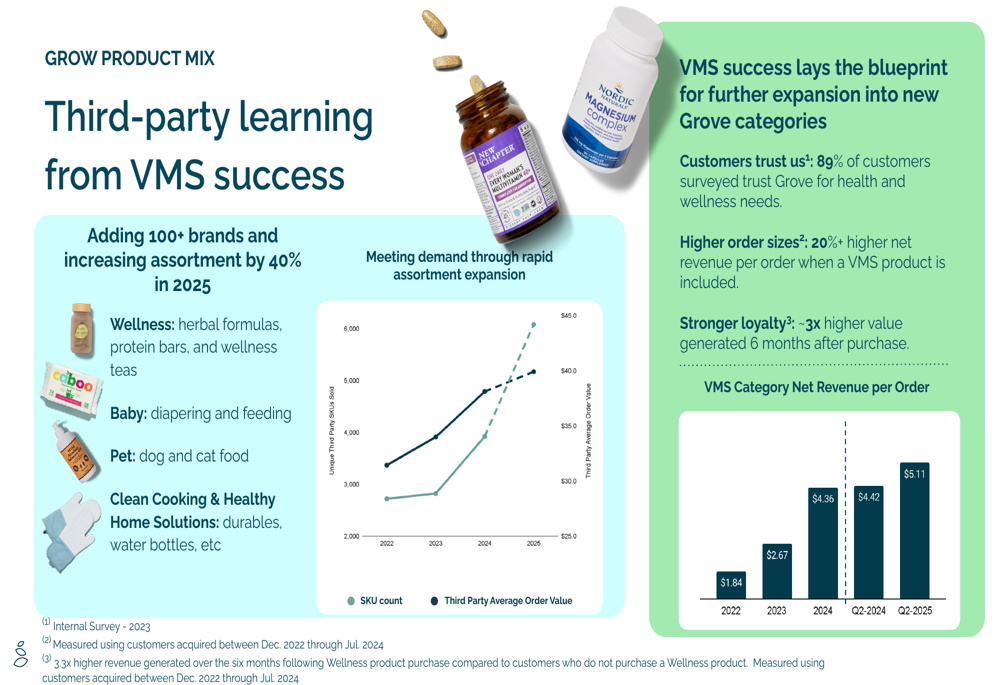

A key component of this strategy is the expansion into vitamins, minerals, and supplements (VMS) and other wellness categories. The company reported strong results from this initiative, with VMS customers demonstrating 20% higher order sizes and three times higher value generated after six months compared to non-VMS customers.

As shown in the following chart, Grove is experiencing growth in its VMS category with increasing SKU count and average order value:

The company plans to add over 100 brands and increase its assortment by 40% in 2025, expanding into herbal formulas, protein bars, baby products, pet products, and clean cooking solutions.

Financial Improvements

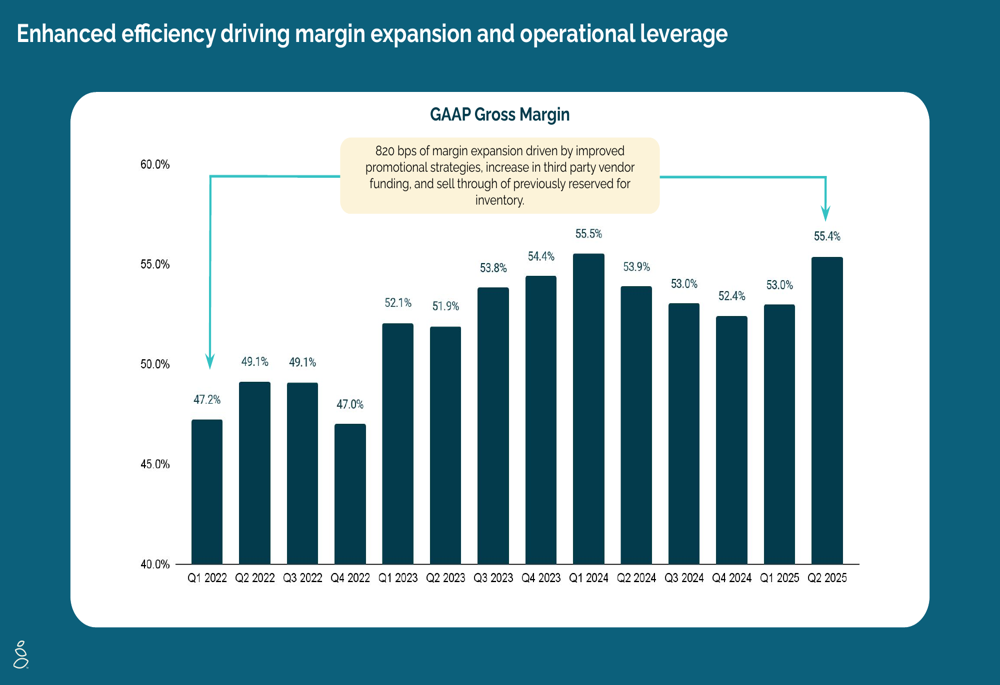

Despite revenue challenges, Grove highlighted several financial improvements, including significant gross margin expansion and debt reduction. The company has achieved approximately 820 basis points of margin expansion since Q1 2022:

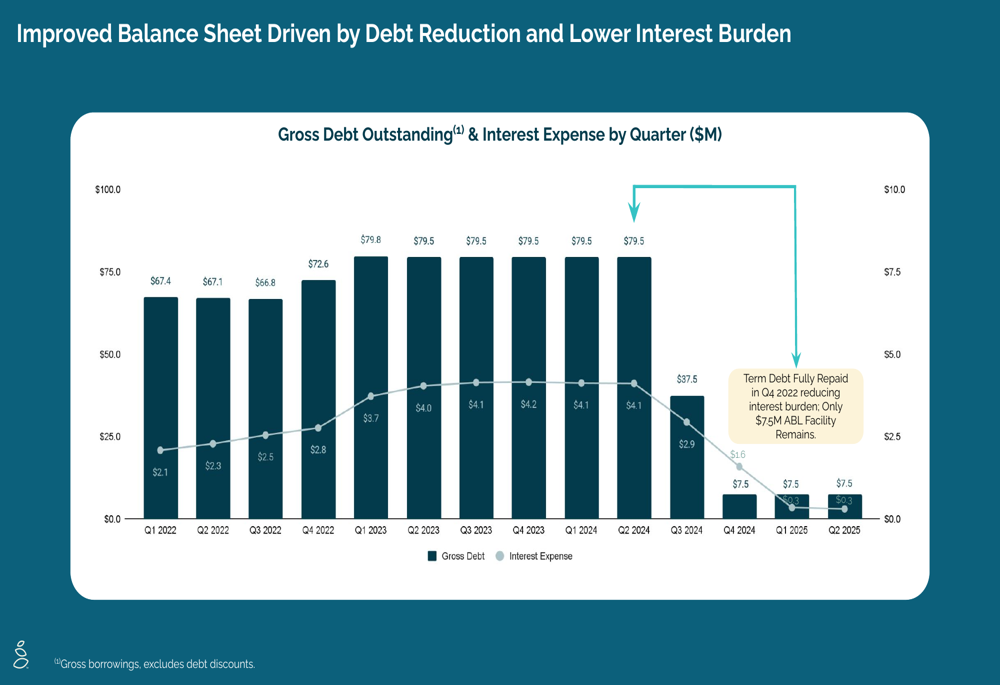

Additionally, Grove has substantially reduced its debt burden, with only a $7.5 million ABL facility remaining. This debt reduction has lowered the company’s interest expense considerably:

The company’s balance sheet as of June 30, 2025, showed $14.0 million in cash, though this represents a significant decrease from the $24.3 million reported at the end of Q4 2024, reflecting ongoing cash burn despite improvements in operating cash flow.

Forward Guidance

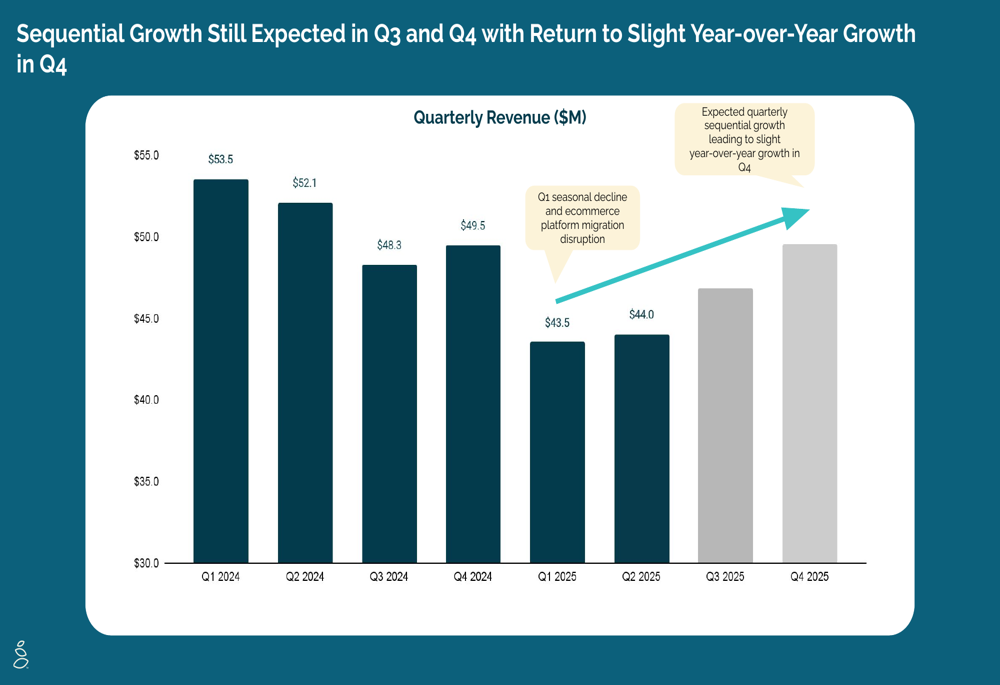

Grove expects sequential revenue growth to continue in Q3 and Q4 2025, with a return to slight year-over-year growth projected for the fourth quarter:

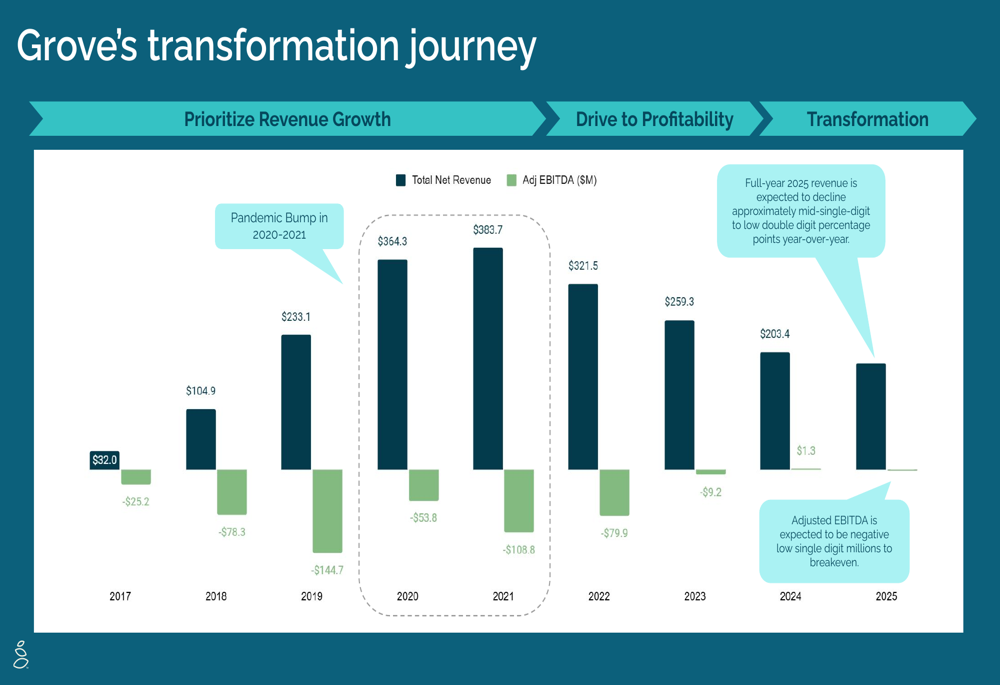

For the full year 2025, the company provided revised guidance, expecting revenue to decline by approximately mid-single digit to low double-digit percentage points year-over-year. Adjusted EBITDA is projected to range from negative low single-digit millions to breakeven:

The company’s multi-year transformation journey shows the historical context for these projections, with 2025 representing a stabilization period following significant revenue declines since the pandemic peak:

Challenges and Outlook

While Grove’s presentation emphasized positive developments in its transformation strategy, the company continues to face significant challenges. The sequential revenue growth in Q2 (+1.1%) marks a modest improvement, but the 15.5% year-over-year decline highlights ongoing difficulties in maintaining its customer base.

The shift from a subscription-only model to an open shopping experience represents a fundamental business model change that aims to expand the company’s reach but has initially resulted in revenue contraction. The company’s focus on higher-margin products and categories is designed to offset some of this volume decline.

Grove’s cash position has deteriorated significantly over the past year, decreasing from $24.3 million at the end of Q4 2024 to $14.0 million by June 30, 2025. This reduction in financial flexibility could constrain the company’s ability to invest in growth initiatives if positive cash flow is not sustained.

As Grove continues its transformation efforts, investors will be watching closely for signs that the sequential growth trend can accelerate and eventually translate into year-over-year growth, particularly in the fourth quarter as projected by management.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.