Five things to watch in markets in the week ahead

Introduction & Market Context

Grupo Catalana Occidente (BME:GCO) presented its first quarter 2025 results on April 30, showing solid performance across all business segments despite mixed global economic conditions. The results come shortly after INOC, S.A. announced a voluntary public tender offer for 100% of GCO’s shares on March 27, 2025.

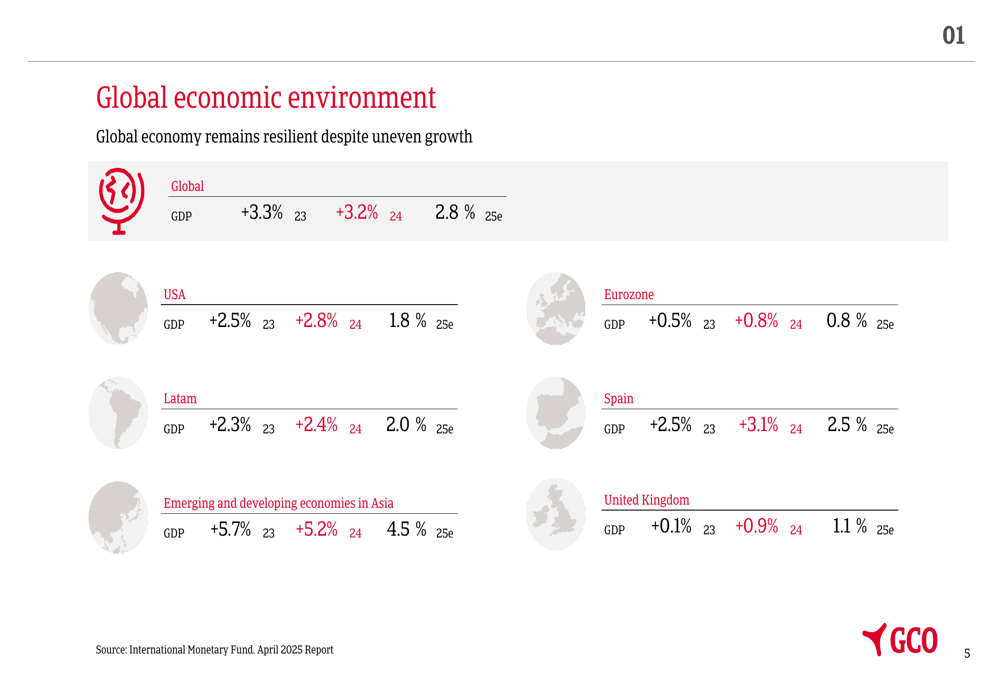

The global economic environment remains varied, with projected 2024 GDP growth of 3.2% globally and 3.1% in Spain, according to IMF data cited in the presentation. The Spanish insurance sector showed strong momentum, with overall premium growth of 6.8% in Q1 2025.

As shown in the following chart of global economic projections:

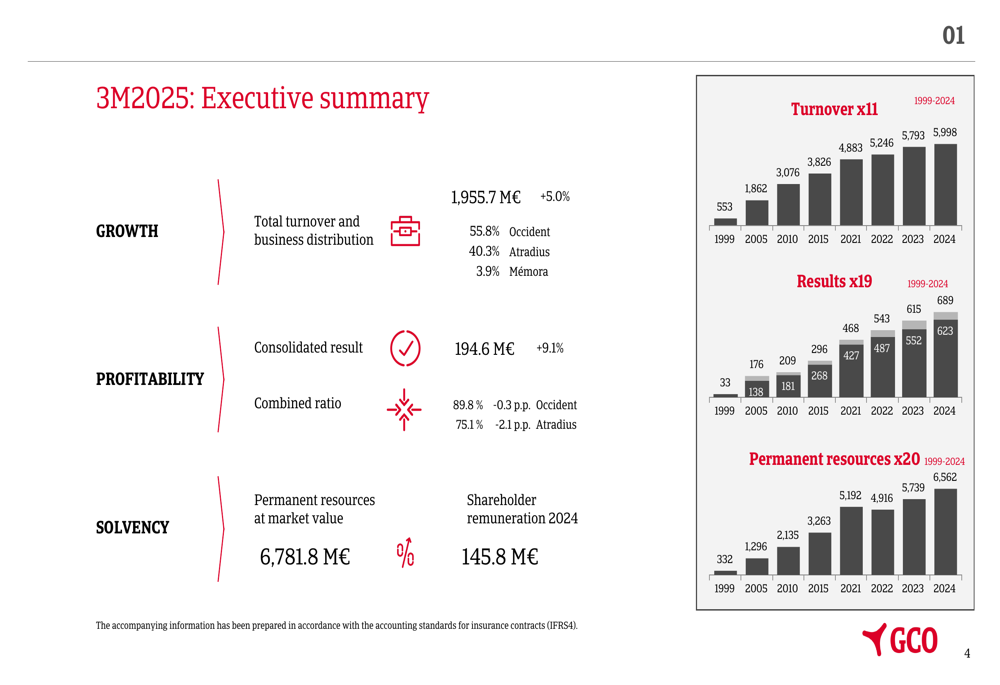

Executive Summary

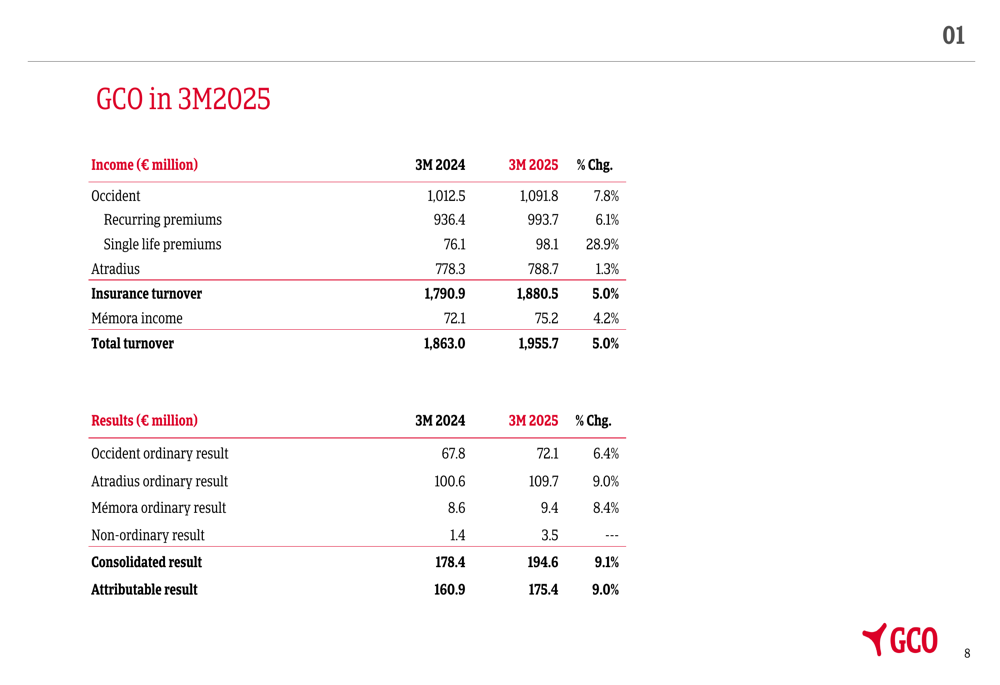

GCO reported total turnover of €1,955.7 million for Q1 2025, representing a 5.0% increase compared to the same period last year. The consolidated result reached €194.6 million, up 9.1% year-over-year, while the attributable result grew by 9.0% to €175.4 million.

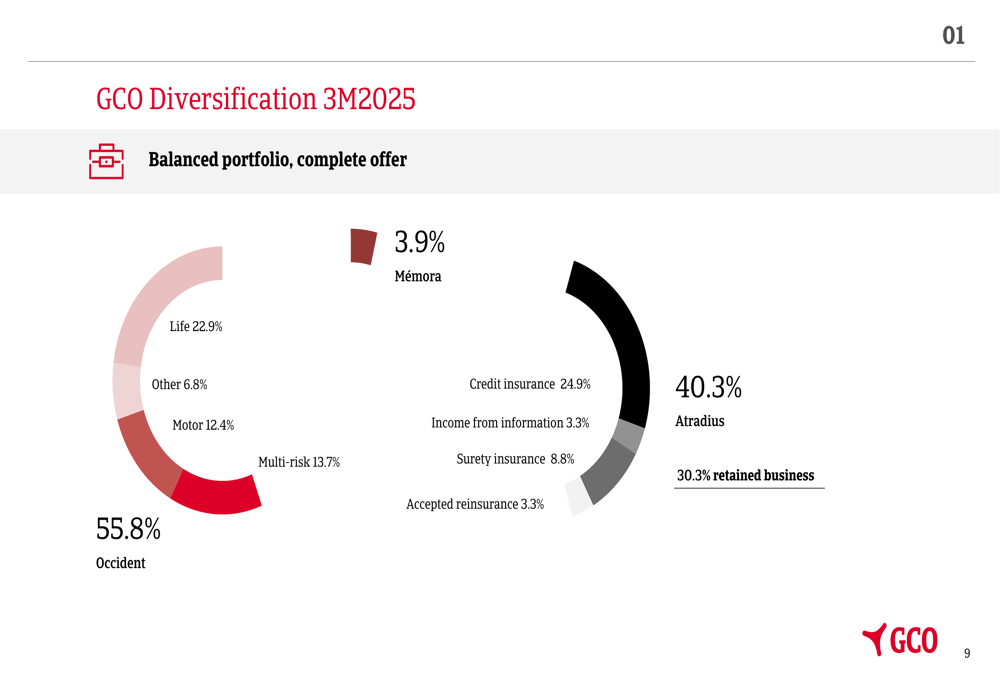

The company’s business remains well-diversified, with Occident (traditional insurance) representing 55.8% of turnover, Atradius (credit insurance) accounting for 40.3%, and Mémora (funeral services) contributing 3.9%.

The following chart provides an overview of the company’s key performance metrics:

Quarterly Performance Highlights

GCO’s performance in Q1 2025 was characterized by growth across all business segments. The company achieved improved combined ratios in both its traditional insurance business (Occident) at 89.8% (-0.3 percentage points) and credit insurance operations (Atradius) at 75.1% (-2.1 percentage points), indicating enhanced underwriting profitability.

The breakdown of income and results by business segment illustrates the balanced contribution to overall performance:

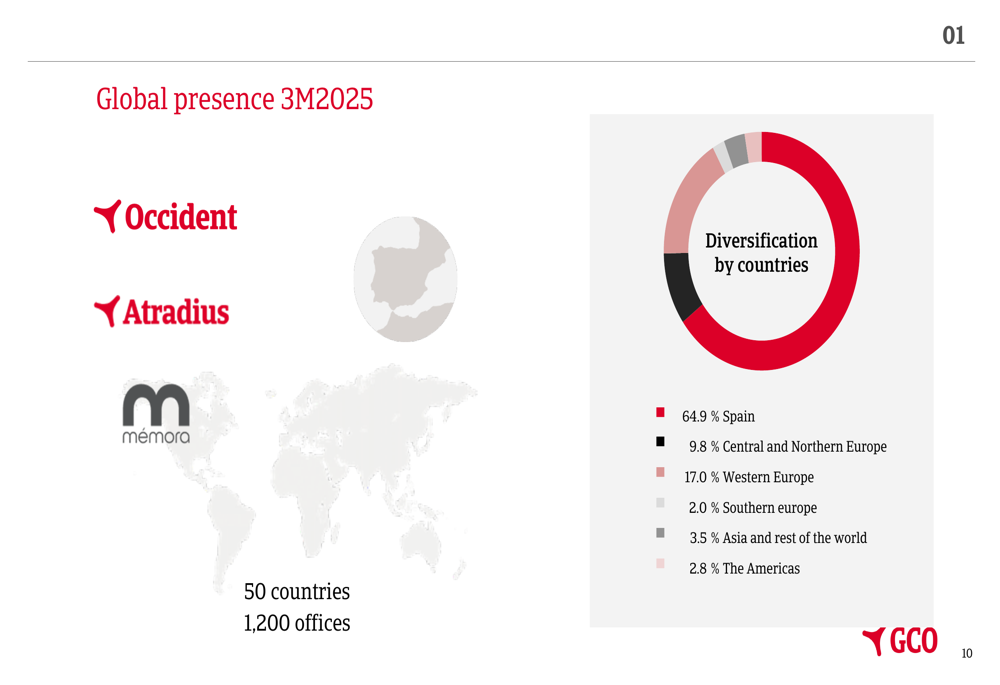

The company maintains a diversified portfolio across various insurance lines, providing resilience against sector-specific challenges. As shown in the following chart of GCO’s portfolio diversification:

GCO’s global footprint spans 50 countries with 1,200 offices, though Spain remains its core market, accounting for 64.9% of operations. The company’s geographical diversification is illustrated below:

Segment Performance

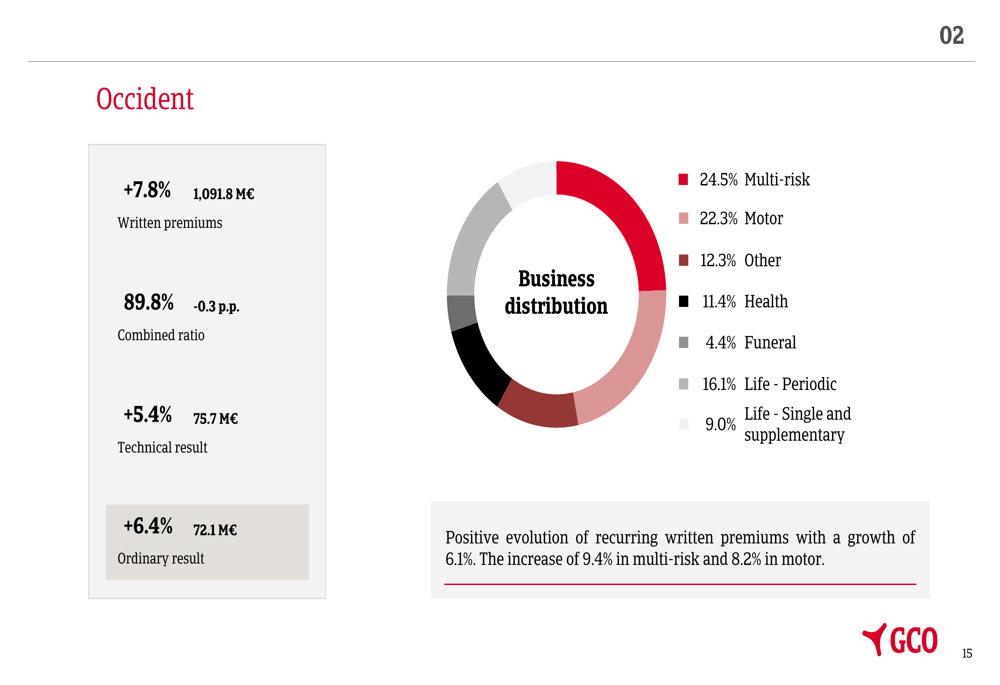

Occident (Traditional Insurance)

Occident, GCO’s traditional insurance segment, reported written premiums of €1,091.8 million, a 7.8% increase compared to Q1 2024. The segment achieved a combined ratio of 89.8%, an improvement of 0.3 percentage points year-over-year. The technical result grew by 5.4% to €75.7 million, while the ordinary result increased by 6.4% to €72.1 million.

Growth was particularly strong in multi-risk (+9.4%) and motor insurance (+8.2%), reflecting successful pricing strategies and market expansion. The following chart details Occident’s performance and business distribution:

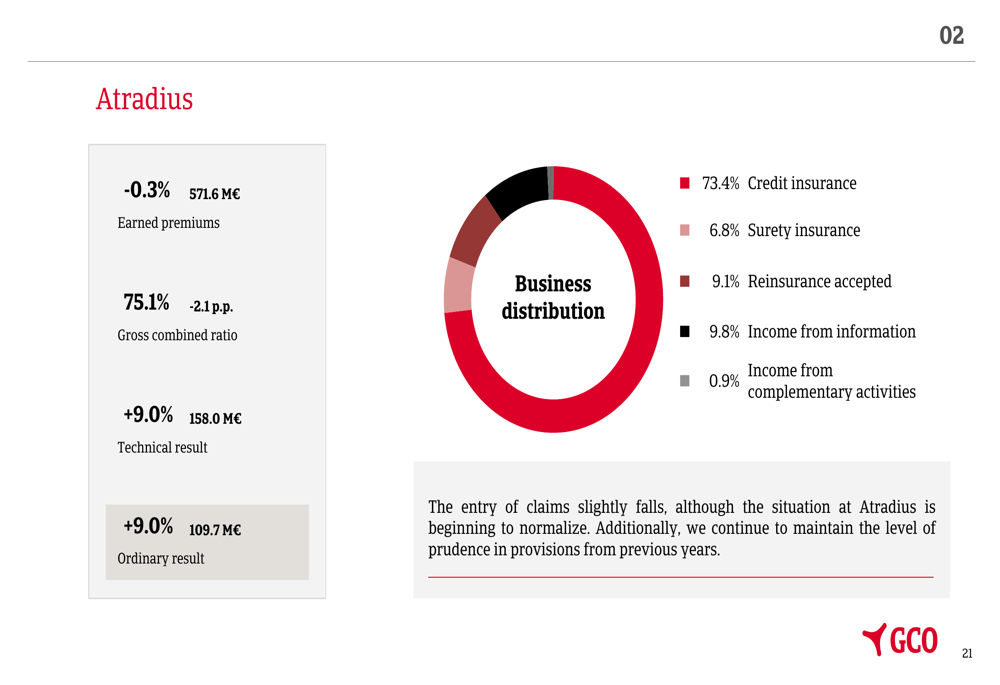

Atradius (Credit Insurance)

Atradius, the group’s credit insurance arm, reported earned premiums of €571.6 million, a slight decrease of 0.3% compared to Q1 2024. Despite this, the segment achieved a gross combined ratio of 75.1%, an improvement of 2.1 percentage points, demonstrating enhanced underwriting efficiency. The technical result and ordinary result both increased by 9.0% to €158.0 million and €109.7 million, respectively.

The following chart shows Atradius’s business distribution and key performance metrics:

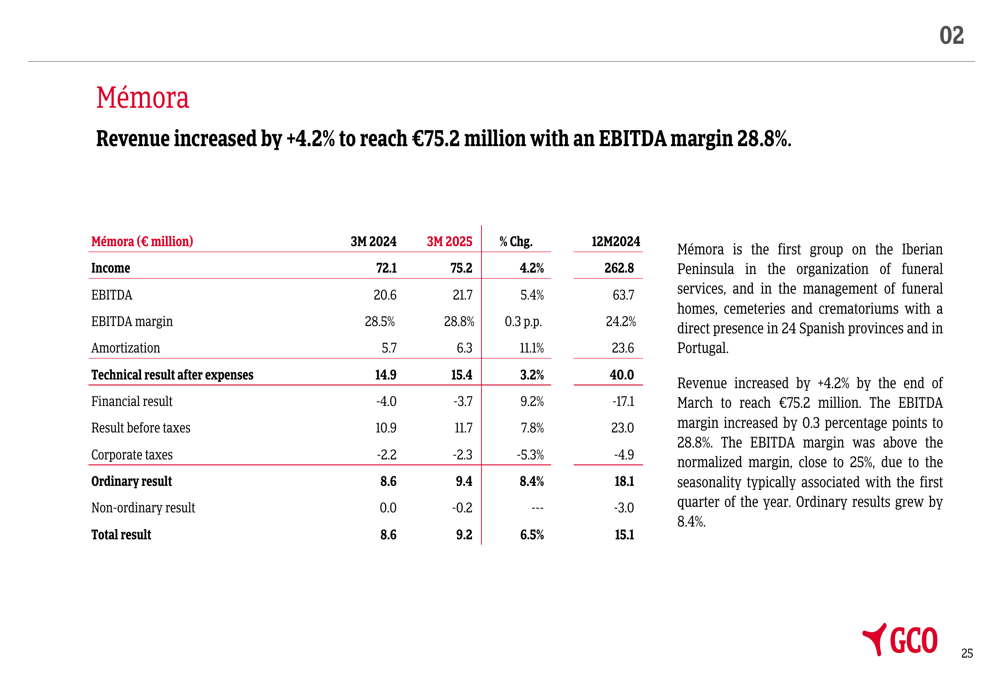

Mémora (Funeral Services)

Mémora, GCO’s funeral services segment, reported revenue of €75.2 million, representing a 4.2% increase compared to Q1 2024. The segment achieved an EBITDA of €21.7 million (+5.4%) with an improved EBITDA margin of 28.8% (+0.3 percentage points). The ordinary result grew by 8.4% to €9.4 million.

The following table details Mémora’s financial performance:

Financial Strength and Investments

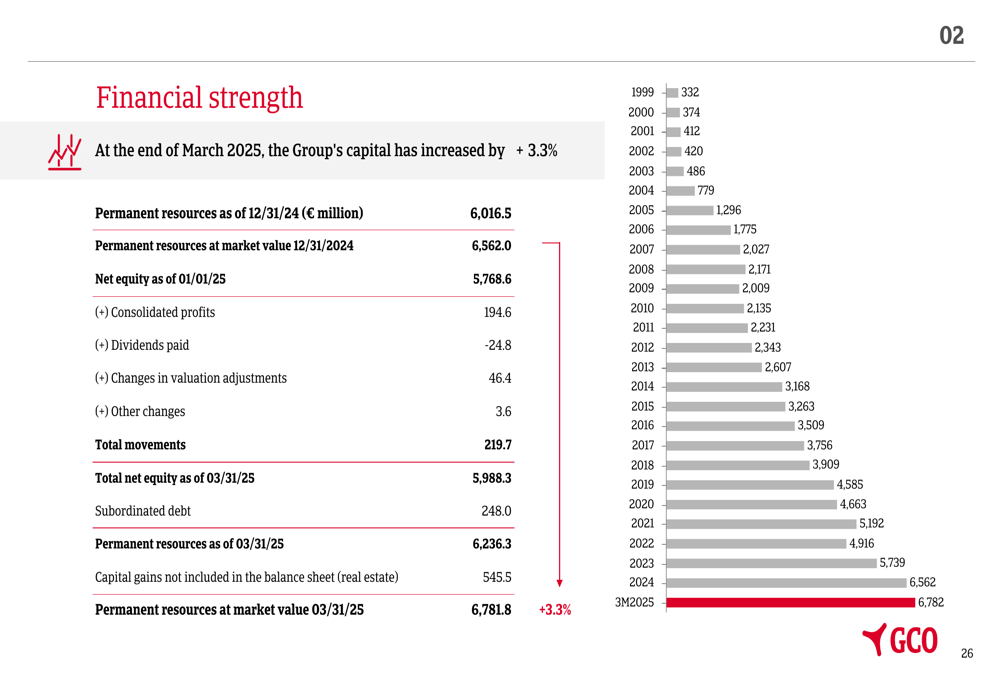

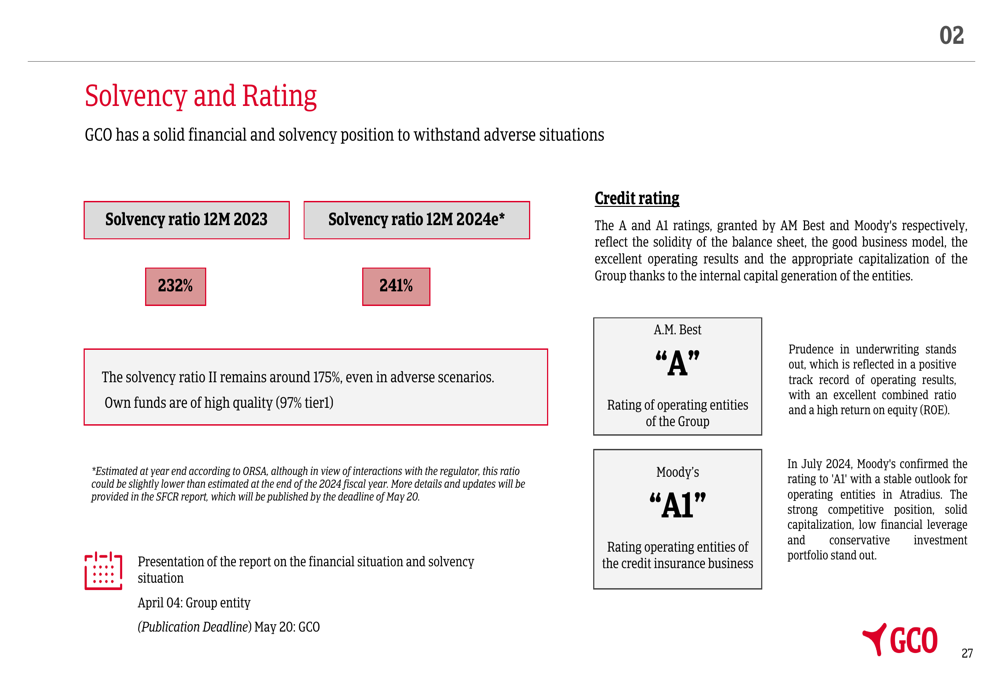

GCO continues to maintain a strong financial position, with permanent resources at market value reaching €6,781.8 million as of March 31, 2025, a 3.3% increase from year-end 2024. The company’s estimated solvency ratio for 2024 stands at 241%, up from 232% in 2023, significantly above regulatory requirements.

The following chart illustrates the evolution of the company’s permanent resources:

The company’s strong financial position is further reflected in its credit ratings, with an "A" rating from A.M. Best and an "A1" rating from Moody’s:

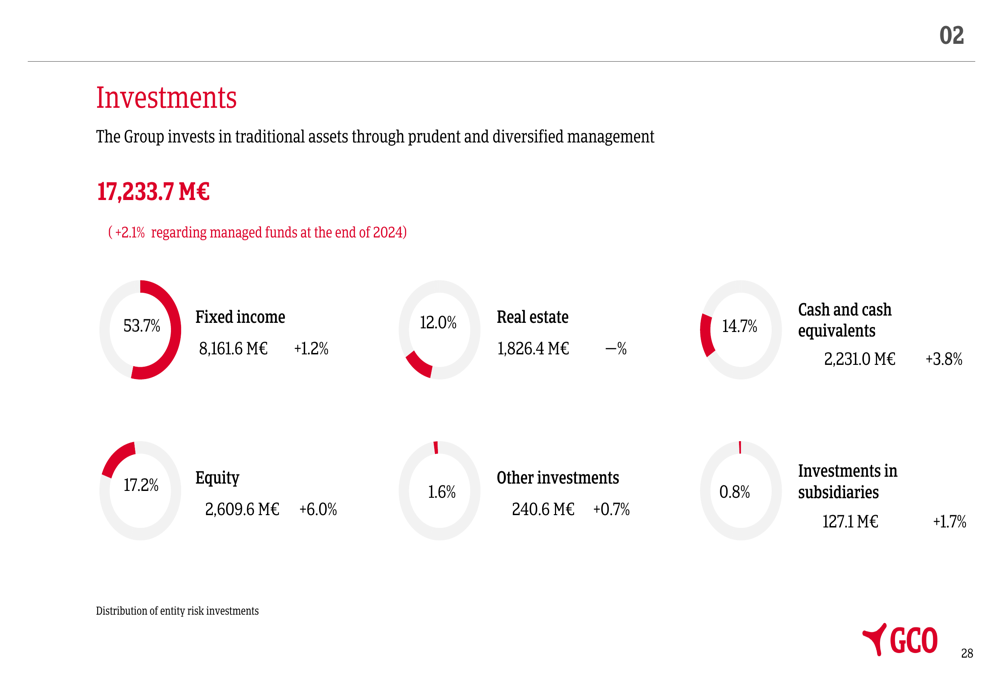

GCO’s investment portfolio totaled €17,233.7 million as of March 31, 2025, a 2.1% increase compared to year-end 2024. The portfolio remains conservatively positioned, with 53.7% allocated to fixed income and 14.7% to cash and cash equivalents. The following chart provides a breakdown of the investment portfolio:

Dividend Growth and Shareholder Value

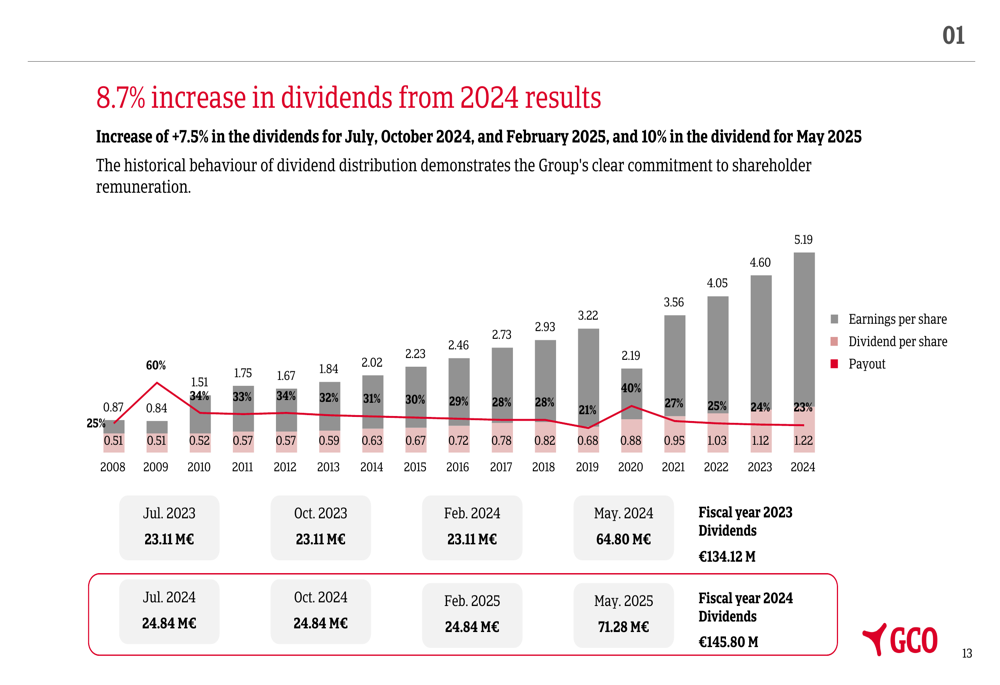

GCO announced an 8.7% increase in dividends from 2024 results, with total dividends for the fiscal year 2024 amounting to €145.80 million. The dividend will be distributed in four payments: July 2024 (€24.84 million), October 2024 (€24.84 million), February 2025 (€24.84 million), and May 2025 (€71.28 million).

The company’s shares ended March 2025 at €49.0 per share, delivering a year-to-date return of 36.63%, significantly outperforming both the IBEX 35 (+13.29%) and the EuroStoxx Insurance index (+7.20%).

The following chart details the dividend distribution plan:

Forward-Looking Statements

Looking ahead, GCO aims to continue its growth trajectory while maintaining underwriting discipline across all business segments. The company remains focused on implementing its Sustainability Master Plan 2024-2026, structured around four pillars: good governance, sustainable business, social commitment, and environmental responsibility.

The most significant development for GCO’s future is the voluntary public tender offer announced by INOC, S.A. on March 27, 2025, for 100% of GCO’s shares. While the presentation did not provide extensive details on the offer, this development could potentially lead to significant changes in the company’s ownership structure and strategic direction in the coming months.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.