What happens to stocks if AI loses momentum?

Introduction & Market Context

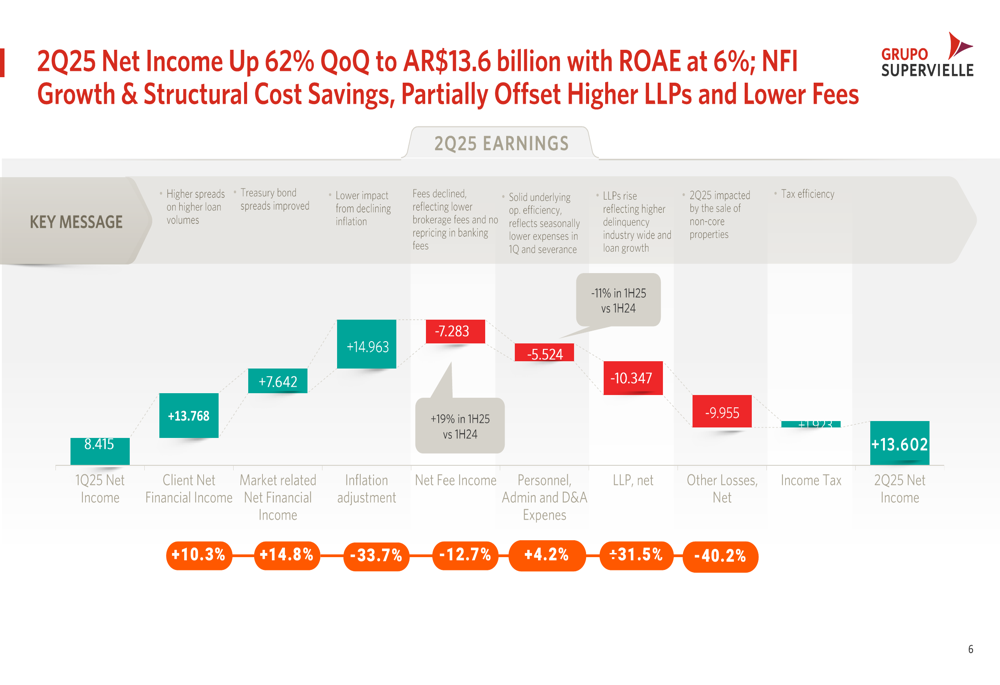

Grupo Supervielle SA (NYSE:SUPV) reported a 62% quarter-over-quarter increase in net income for Q2 2025, as the Argentine bank continues its strategic pivot from investments to lending. The results, presented on August 14, 2025, show the company navigating a complex macroeconomic environment marked by decelerating inflation and the successful lifting of foreign exchange restrictions for individuals.

The bank’s performance comes amid pre-electoral uncertainty in Argentina, though management noted that "structural macro and political conditions remain supportive." Grupo Supervielle shares closed at $10.92 on August 13, down 0.91% ahead of the results presentation, with the stock trading within a 52-week range of $6.75 to $19.75.

Quarterly Performance Highlights

Grupo Supervielle achieved a real-terms return on equity (ROE) of 6% in Q2 2025, supported by a solid net interest margin (NIM) of 21%, which expanded 160 basis points quarter-over-quarter. The bank’s loan book grew 14% compared to the previous quarter, outpacing the industry’s 11.2% growth rate.

As shown in the following quarterly net income analysis, several factors contributed to the 62% increase in profits:

The bank’s total deposit base increased 6% quarter-over-quarter and 42% year-over-year, with U.S. dollar deposits reaching record levels—up 16% from the previous quarter and 154% compared to the same period last year. This strong deposit growth provides a stable funding base for the bank’s expanding loan portfolio.

Operating efficiency also improved, with the bank reporting a year-to-date cost reduction of 13% and net fee income growth of 19% over the same period.

Strategic Shift to Lending

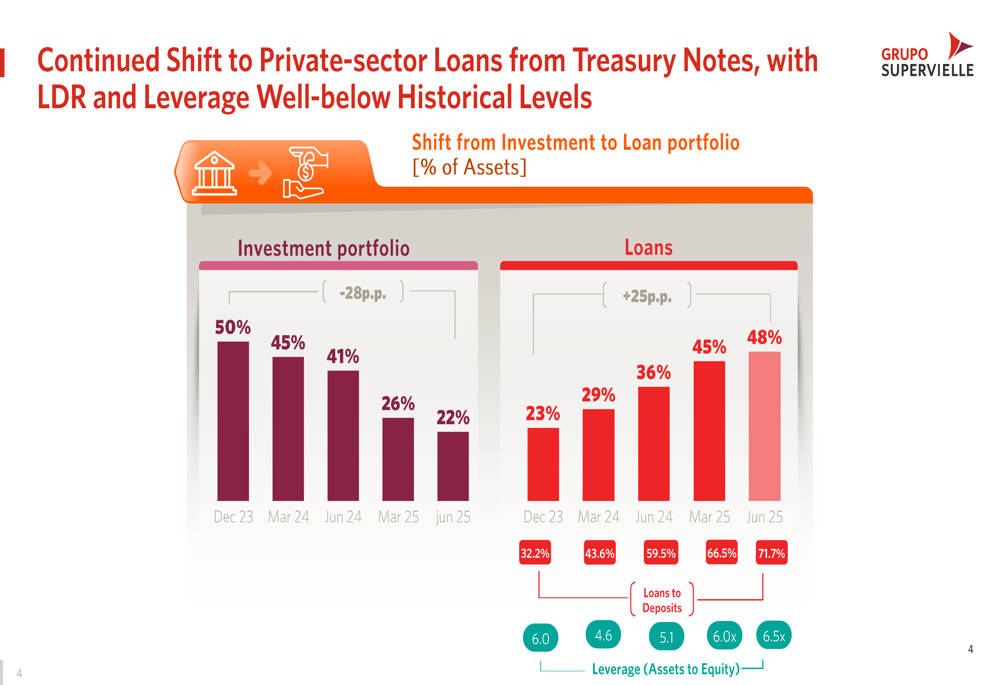

A cornerstone of Grupo Supervielle’s strategy has been the significant reallocation of assets from investments to loans. This pivot is clearly illustrated in the following chart:

The investment portfolio decreased from 50% of assets in December 2023 to just 22% in June 2025, while the loan portfolio increased from 23% to 48% during the same period. Consequently, the loans-to-deposits ratio rose dramatically from 32.2% to 71.7%, indicating more efficient use of the bank’s funding base.

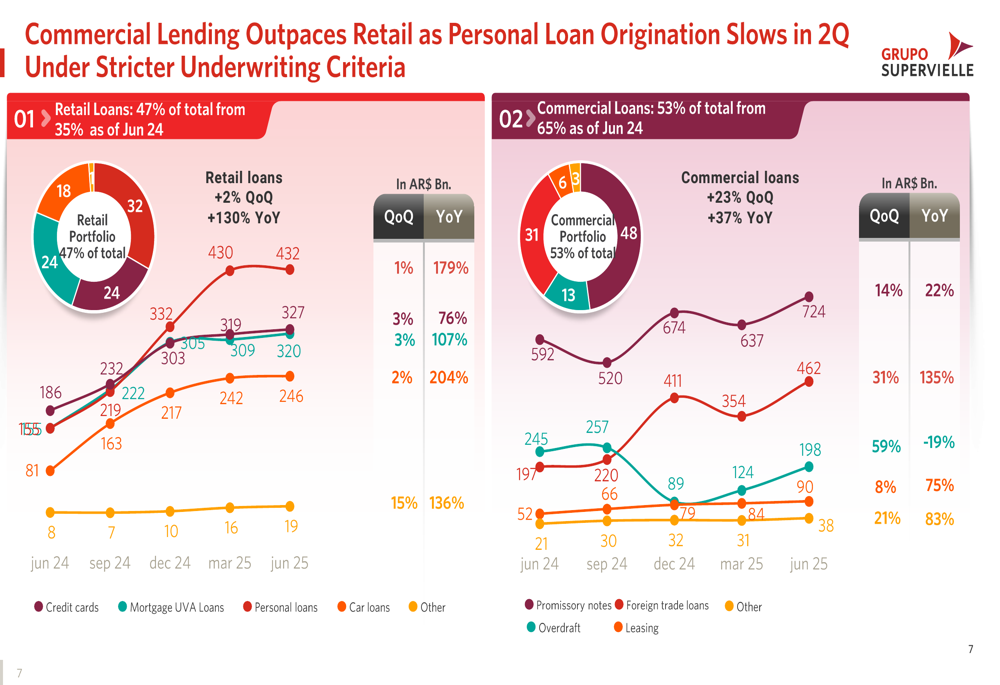

This strategic shift has been accompanied by a change in the composition of the loan portfolio itself. Commercial loans now represent 53% of total lending, growing 23% quarter-over-quarter and 37% year-over-year, primarily driven by promissory notes and foreign trade loans. Meanwhile, retail lending, which accounts for 47% of the portfolio, showed more modest growth of 2% quarter-over-quarter.

Asset Quality and Risk Management

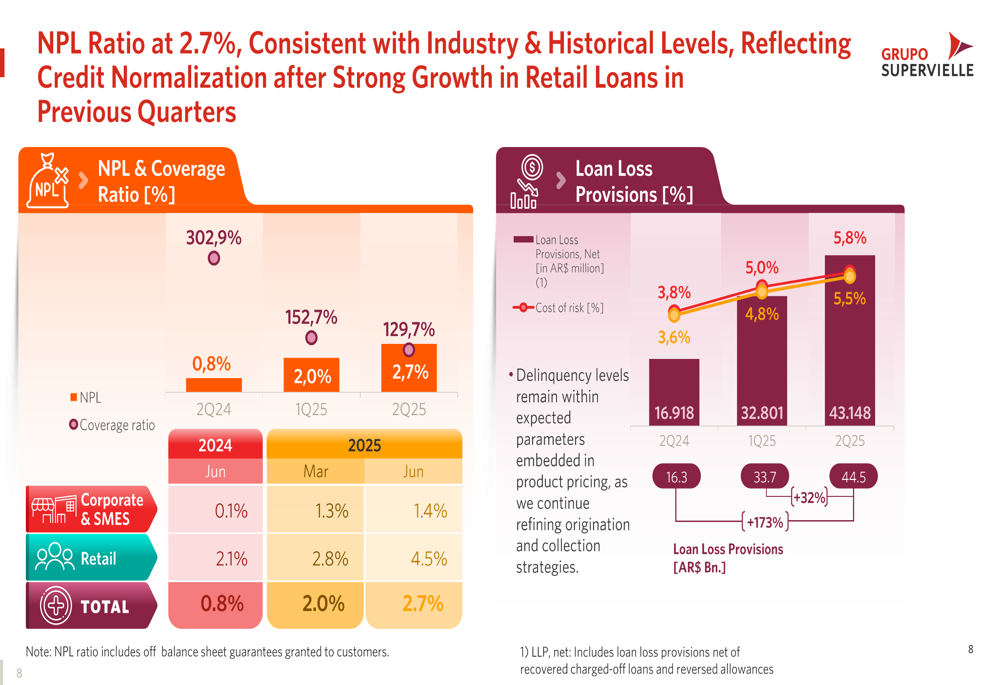

The rapid expansion of the loan book has been accompanied by some deterioration in asset quality metrics. The non-performing loan (NPL) ratio increased to 2.7% in Q2 2025, up from 2.0% in the previous quarter and 0.8% in the same period last year. Simultaneously, the coverage ratio declined to 129.7% from 152.7% in Q1 2025 and 302.9% a year earlier.

The following chart illustrates these trends in asset quality:

Loan loss provisions increased to 43.1 billion Argentine pesos in Q2 2025, up from 32.8 billion in the previous quarter. The cost of risk rose to 5.5%, compared to 4.8% in Q1 2025 and 3.6% a year earlier. Despite these increases, management stated that "delinquency levels are within expected parameters" given the rapid loan growth and broader industry trends.

Digital Innovation Initiatives

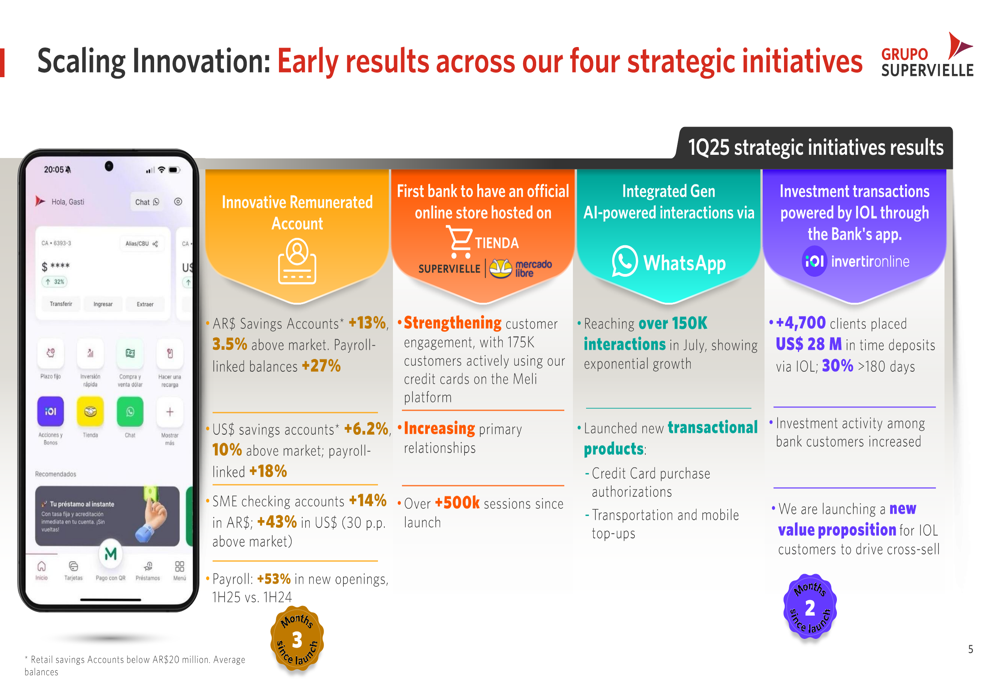

Grupo Supervielle highlighted four strategic digital initiatives that are showing promising early results. These innovations aim to enhance customer engagement and drive deposit and transaction growth.

The bank’s innovative remunerated account has helped increase Argentine peso savings accounts by 13% (3.5% above market) and U.S. dollar savings accounts by 6.2% (10% above market). The bank has also become the first in Argentina to establish an official online store on Mercado Libre, strengthening customer engagement with 175,000 customers actively using Supervielle credit cards on the platform.

As illustrated in the following slide, these digital initiatives are gaining significant traction:

The bank’s AI-powered WhatsApp interactions reached over 150,000 in July 2025, showing exponential growth. Additionally, investment transactions powered by IOL through the bank’s app have attracted 4,700 clients who placed $28 million in time deposits, with 30% of these deposits having terms exceeding 180 days.

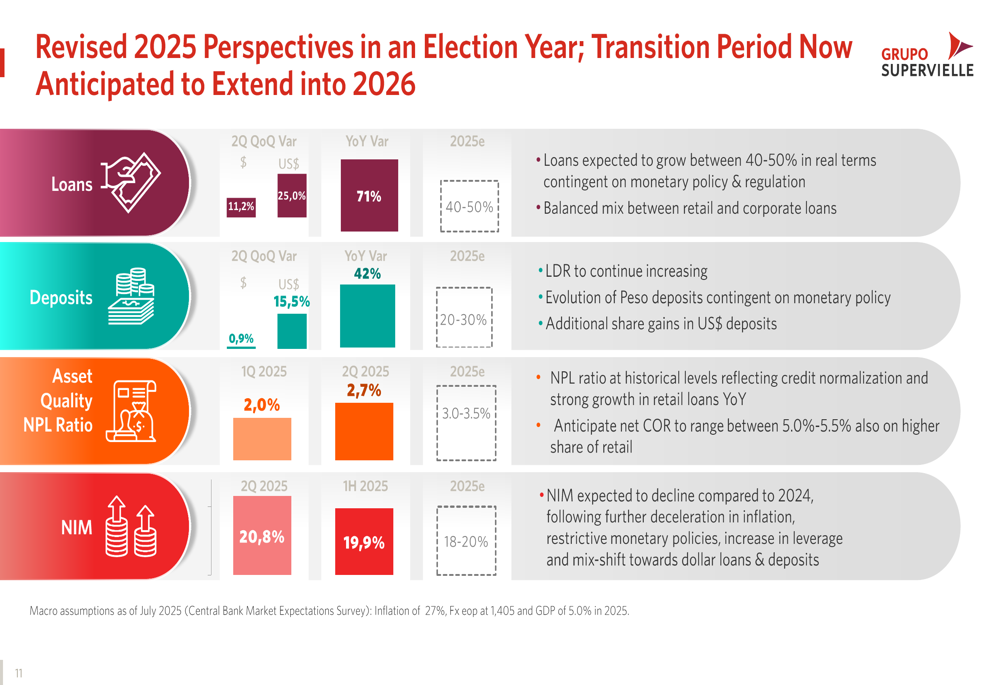

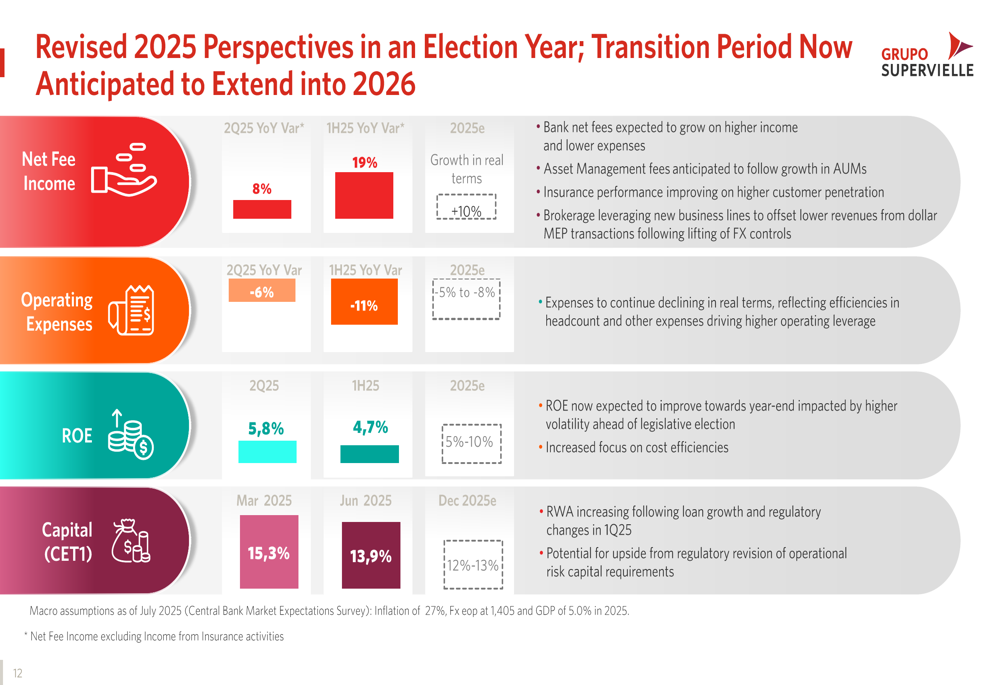

Forward-Looking Guidance

Grupo Supervielle provided revised guidance for 2025, noting that the transition period is now expected to extend into 2026. The bank anticipates loan growth of 40-50% in real terms for 2025, with deposits projected to increase by 20-30%.

The following chart details the bank’s expectations across key performance metrics:

Management expects the NPL ratio to rise to 3.0-3.5% by year-end, while maintaining a NIM of 18-20%. Operating expenses are projected to decline by 5-8% in real terms for the full year, supporting an expected ROE of 5-10%.

The CET1 capital ratio, which stood at 13.9% in June 2025 (down from 15.3% in March), is expected to end the year between 12-13% as risk-weighted assets increase following loan growth and regulatory changes implemented in Q1 2025.

As Grupo Supervielle continues its strategic transformation, management remains focused on balancing growth opportunities with prudent risk management in Argentina’s evolving economic landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.