Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

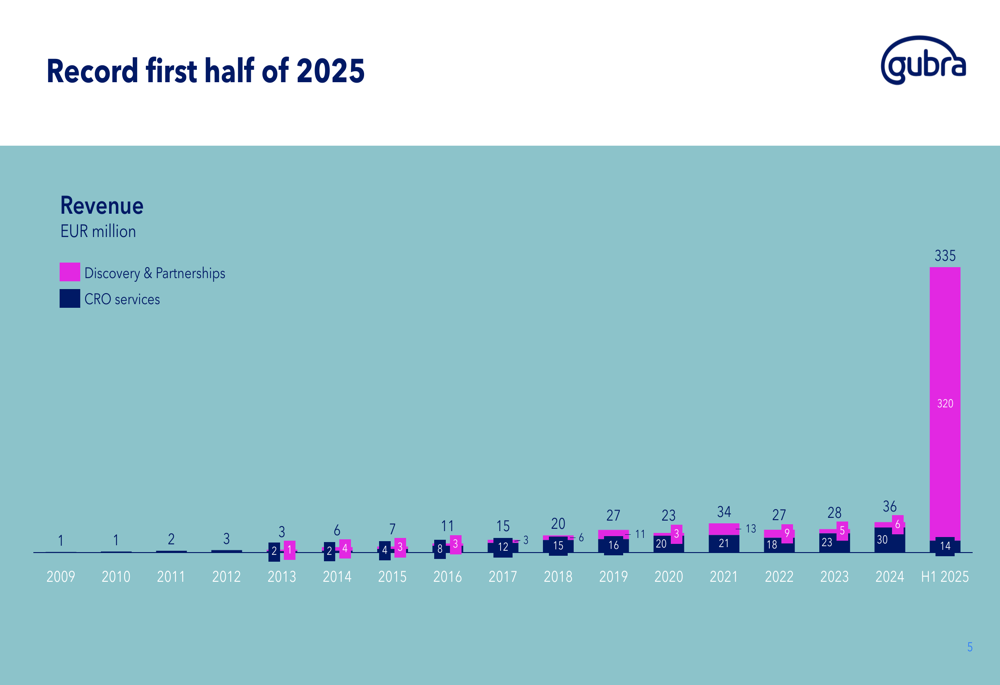

Gubra AS (NASDAQ:GUBRA) presented its first half 2025 results on August 21, 2025, revealing extraordinary financial performance primarily driven by a transformative licensing deal with AbbVie (NYSE:ABBV). The company, which specializes in peptide-based drug development with a focus on obesity treatments, reported record revenue of €335 million for H1 2025, compared to €36 million for the full year 2024.

The presentation, delivered by CEO Henrik Blou, CSO Louise S. Dalbøge, and CFO Kristian Borbos, highlighted the company’s strategic focus on developing innovative obesity treatments while maintaining its contract research organization (CRO) business. Gubra’s stock closed at 354.6 DKK on August 20, 2025, down slightly by 0.11%, but remains well above its 52-week low of 323.4 DKK.

As shown in the following revenue growth chart, Gubra’s H1 2025 results represent an unprecedented leap from historical performance:

Quarterly Performance Highlights

The most significant development in H1 2025 was the outlicensing of GUBamy (Amylin) to AbbVie for USD 2.2 billion, including USD 350 million upfront payment plus royalties. This deal fundamentally transformed Gubra’s financial position, enabling the company to announce an extraordinary dividend of DKK 1 billion to shareholders.

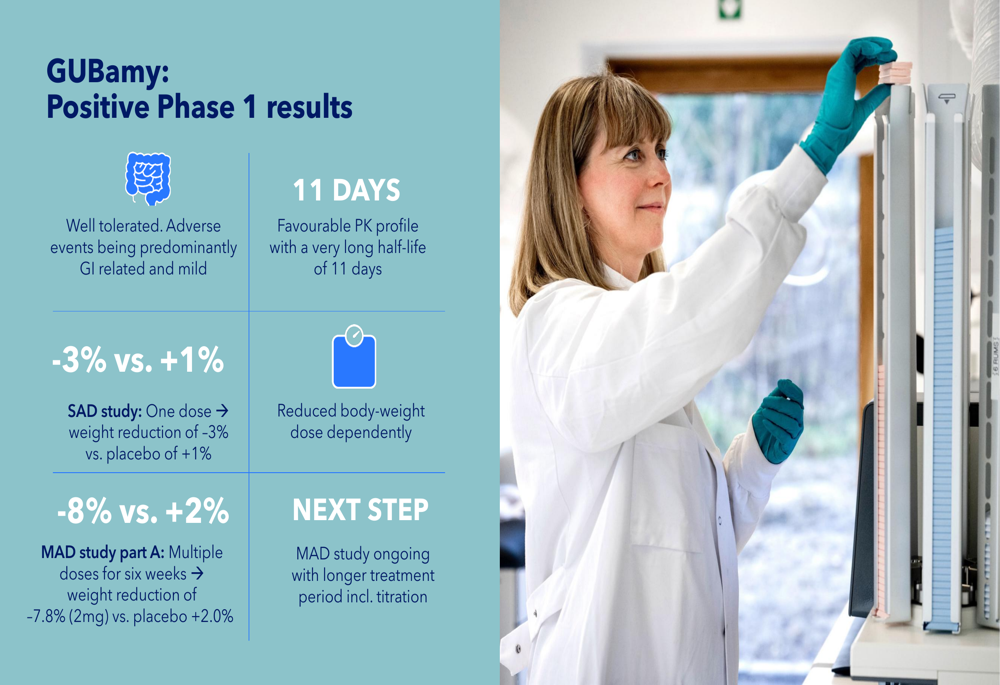

The presentation highlighted several key operational achievements for the first half of 2025, including strong clinical results for GUBamy and progress with UCN2, their innovative obesity treatment focused on healthy weight loss:

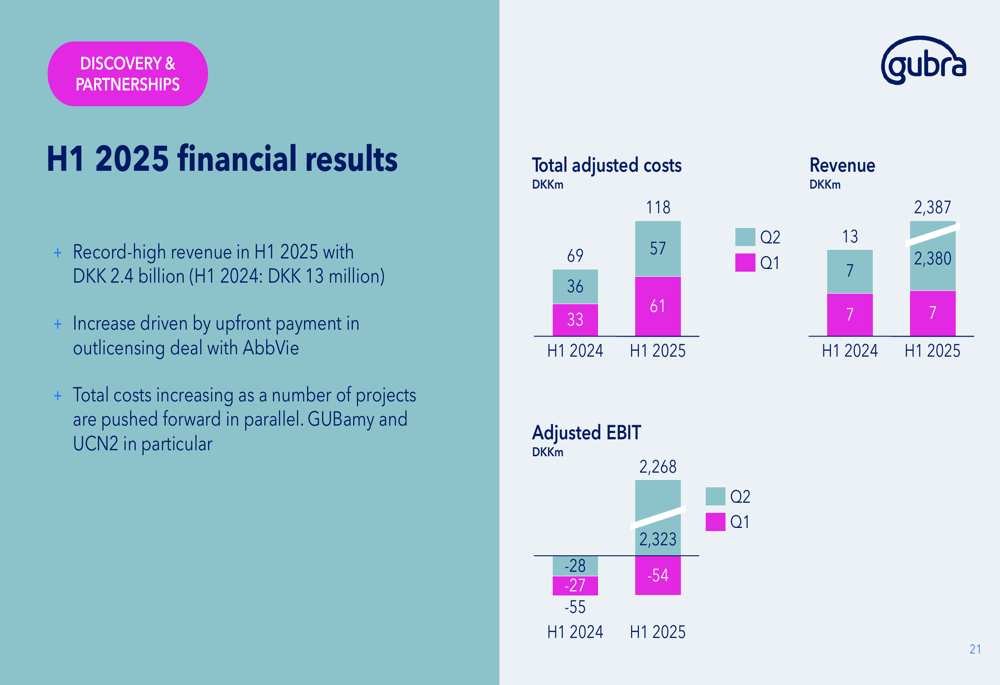

Financial results for the Discovery (NASDAQ:WBD) & Partnerships segment showed record-high revenue of DKK 2.4 billion in H1 2025, compared to just DKK 13 million in H1 2024, driven primarily by the AbbVie upfront payment:

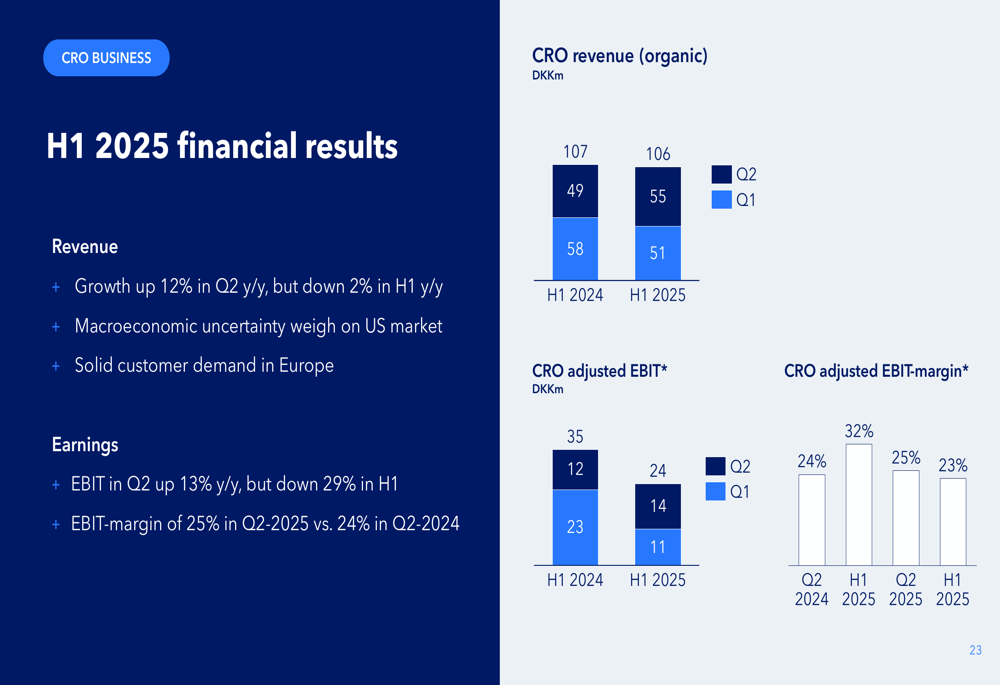

Meanwhile, the CRO business segment showed mixed results with revenue of DKK 106 million in H1 2025, slightly below the DKK 107 million reported in H1 2024. The company noted that macroeconomic uncertainty is weighing on the US market, though European customer demand remains solid:

Detailed Financial Analysis

Gubra’s historical growth trajectory shows a compound annual growth rate (CAGR) of 30% from 2009 to 2024, with the business divided between CRO services and Discovery & Partnerships. The H1 2025 results represent a dramatic acceleration of this growth, with Discovery & Partnerships contributing €320 million and CRO services adding €14 million to the total €335 million revenue.

The company’s adjusted EBIT for the Discovery & Partnerships segment reached DKK 2,268 million in Q2 2025 and DKK 2,323 million in Q1 2025, compared to negative figures in the corresponding periods of 2024. This remarkable turnaround reflects the transformative impact of the AbbVie deal.

For the CRO segment, adjusted EBIT margin declined from 32% in H1 2024 to 23% in H1 2025, reflecting increased costs and competitive pressures. The company has revised its outlook for this segment, now expecting revenue to be "slightly below 2024 revenue" compared to the previous guidance of 10-20% growth.

Strategic Initiatives

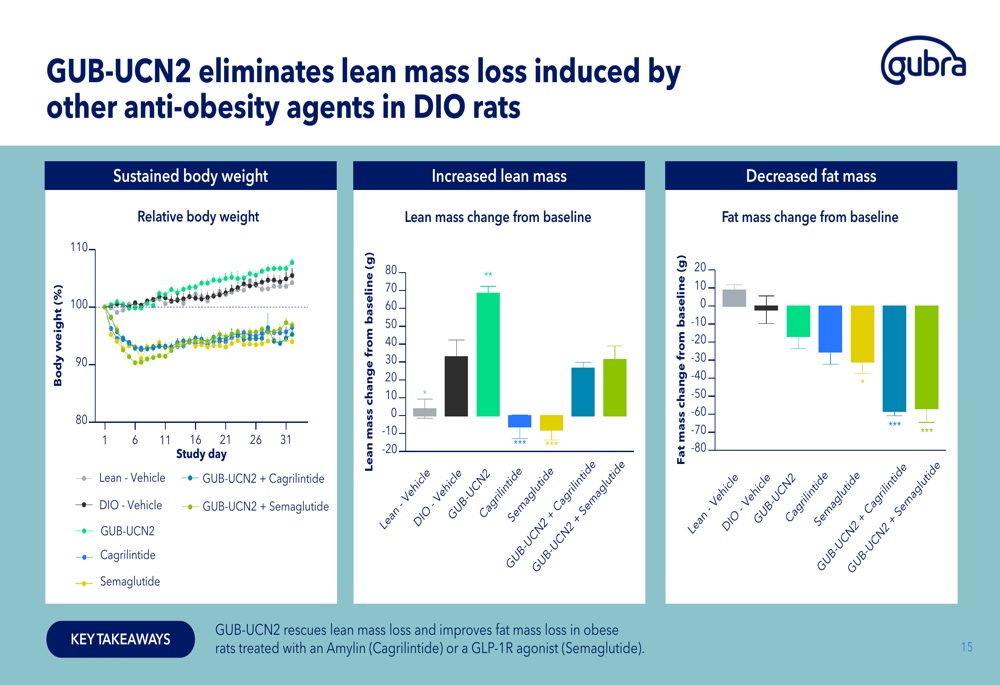

Gubra’s presentation emphasized its strategic focus on developing innovative obesity treatments, particularly highlighting its "healthy weight loss" approach. The company’s GUB-UCN2 program aims to address a key limitation of current obesity treatments by preventing lean mass loss while enhancing fat reduction.

As illustrated in the following chart, GUB-UCN2 has shown promising results in eliminating lean mass loss induced by other anti-obesity agents:

The company’s R&D pipeline includes several promising candidates across different development stages, with both partnered and internal programs. GUBamy (Amylin) for obesity, now partnered with AbbVie, represents the most advanced and commercially significant program.

The GUBamy Phase 1 results showed impressive weight reduction of -7.8% with the 2mg dose versus +2.0% for placebo in the Multiple Ascending Dose (MAD) study part A:

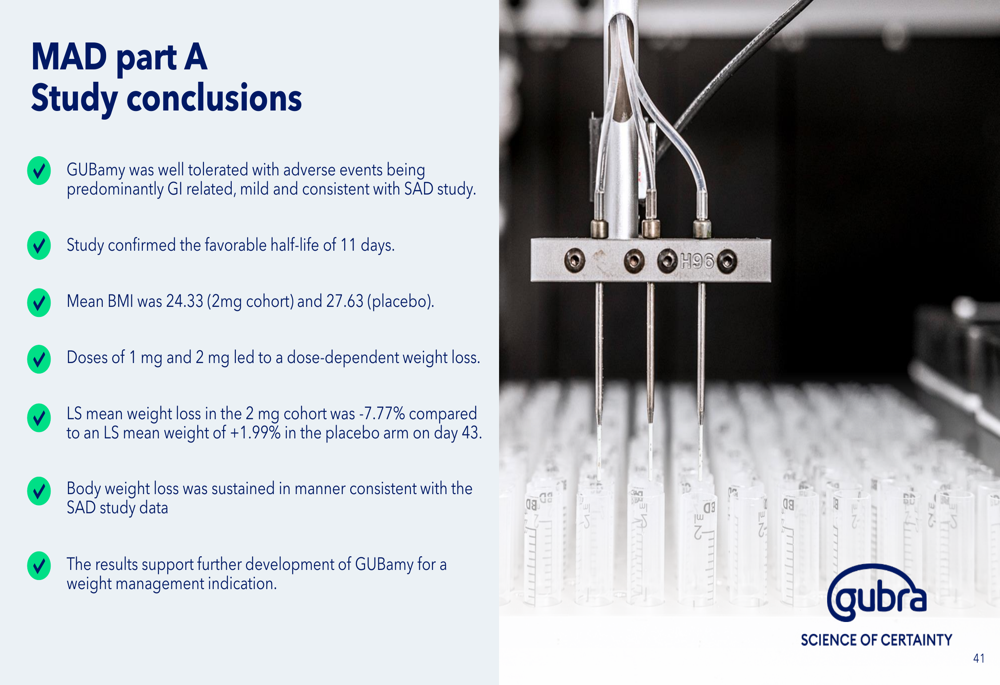

The MAD part A study conclusions further support GUBamy’s potential as a significant weight management treatment:

Forward-Looking Statements

Gubra has updated its financial outlook for 2025, maintaining its Discovery & Partnership segment cost guidance at DKK 230-250 million while revising the CRO segment expectations downward. The company now expects CRO revenue to be slightly below 2024 levels, with an EBIT margin around 20%.

The company also announced a CEO succession plan, with Markus Rohrwild set to take over as CEO from September 8, 2025.

Looking further ahead, Gubra outlined its strategic priorities and aspirations toward 2030, focusing on four key areas: Pipeline and Models, Tech Innovation, Core Research Engine, and ESG. The company aims to develop its pipeline beyond obesity, accelerate innovation through a "TechBio Lab," optimize its research operations, and promote environmental sustainability by investing 10% of pre-tax profit in environmental activities annually.

For GUB-UCN2, the company is planning to begin clinical Phase 1 testing in early 2026, with non-clinical toxicity programs currently ongoing. This timeline aligns with statements made in the Q1 2025 earnings call.

Analyst Perspectives

While the presentation did not include specific analyst commentary, the extraordinary financial results and promising clinical data for both GUBamy and GUB-UCN2 position Gubra favorably in the competitive obesity treatment market. The AbbVie partnership validates the company’s approach and provides substantial resources to advance its pipeline.

The slight decline in CRO business performance remains a concern, with macroeconomic uncertainty affecting the US market. However, this segment represents a much smaller portion of Gubra’s overall value following the transformative AbbVie deal.

The company’s strategic focus on "healthy weight loss" through GUB-UCN2 represents a differentiated approach in the increasingly crowded obesity treatment market, potentially addressing a significant unmet need by preserving lean mass while reducing fat mass.

With a strong cash position following the AbbVie deal and promising clinical data for its lead programs, Gubra appears well-positioned to execute its strategic priorities and deliver long-term value to shareholders, despite near-term challenges in its CRO business.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.