TSX futures inch lower after index closes at new all-time high

Introduction & Market Context

Italian filtration specialist GVS SpA presented its H1 2025 results on August 7, 2025, highlighting improved profitability metrics despite modest overall sales growth. The company’s stock traded at €4.98 on presentation day, showing minimal movement (-0.1%) as investors digested the mixed results against the backdrop of previous quarters’ performance.

GVS, which manufactures filtration solutions for healthcare, automotive, and safety applications, reported its highest EBITDA margin since Q4 2021, suggesting a recovery trajectory following its Q1 2025 earnings miss that had previously triggered a nearly 5% stock decline.

Executive Summary

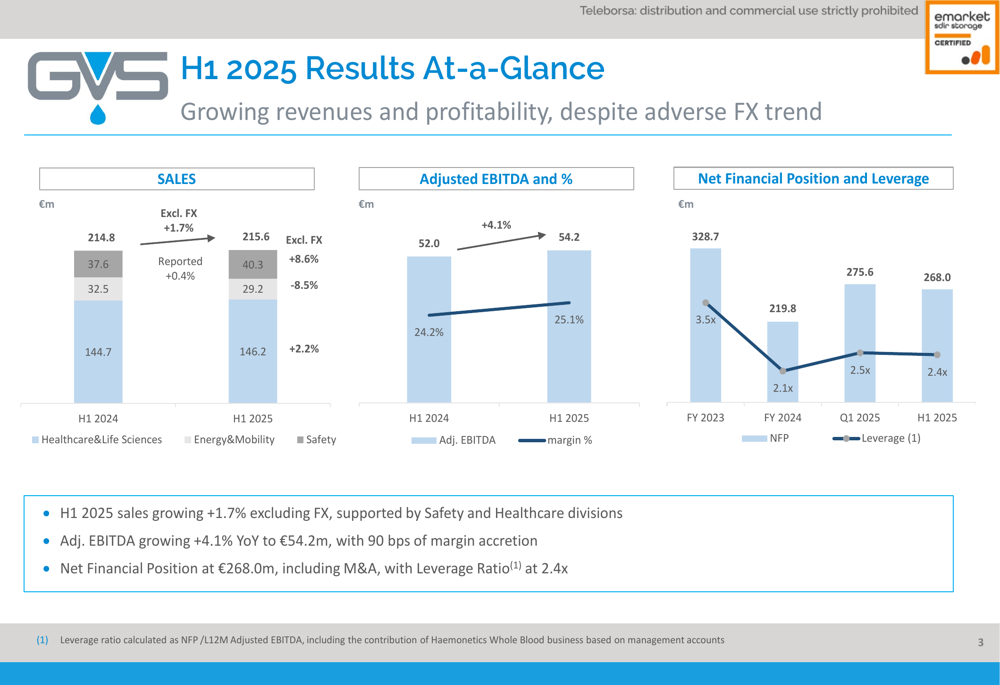

GVS reported H1 2025 sales of €215.6 million, representing a modest 1.7% year-over-year growth excluding currency effects. Despite the limited top-line expansion, the company achieved notable profitability improvements, with adjusted EBITDA reaching €54.2 million, up 4.1% compared to H1 2024, and EBITDA margin expanding by 90 basis points to 25.1%.

As shown in the following comprehensive financial overview, the company’s performance varied significantly across its three main divisions, with Healthcare & Life Sciences and Safety showing growth while the Mobility segment faced headwinds:

Particularly noteworthy was the Q2 2025 adjusted EBITDA margin of 26.2%, representing a 120 basis point improvement over Q2 2024 and marking the highest profitability level since Q4 2021. Adjusted net income excluding foreign exchange impacts increased by 16.2% to €26.2 million, with margin expanding from 10.5% to 12.1%.

Detailed Financial Analysis

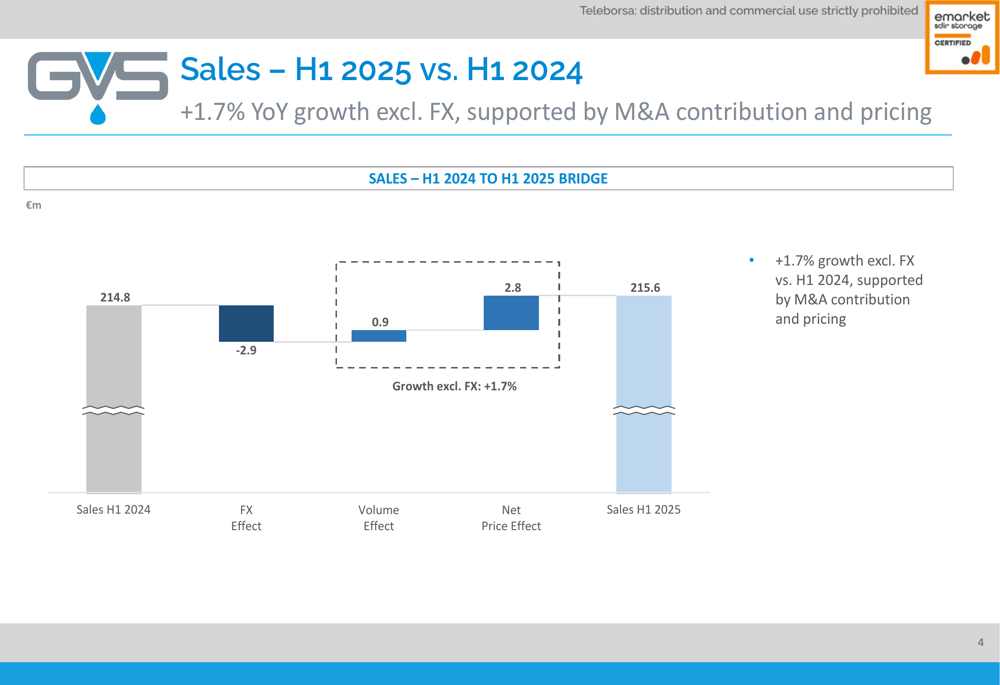

GVS’s overall sales growth of 1.7% (excluding FX) was driven by positive pricing effects of €2.8 million, which offset modest volume increases of €0.9 million. Currency effects negatively impacted reported sales by €2.9 million.

The following bridge analysis illustrates the components contributing to the sales performance:

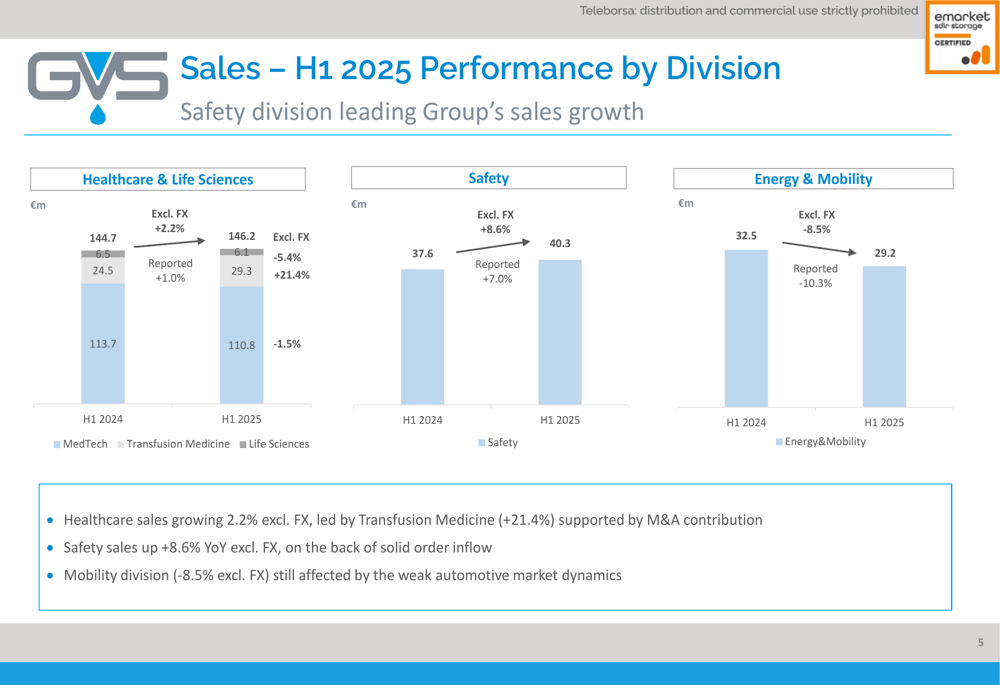

Divisional performance revealed significant variations. The Healthcare & Life Sciences division, which accounts for approximately 68% of total sales, grew by 2.2% excluding currency effects to €146.2 million. The Safety division demonstrated the strongest growth at 8.6% excluding FX, reaching €40.3 million. However, the Mobility division declined by 8.5% to €29.2 million, continuing to face challenges from weak automotive market conditions.

This divisional breakdown is clearly illustrated in the following chart:

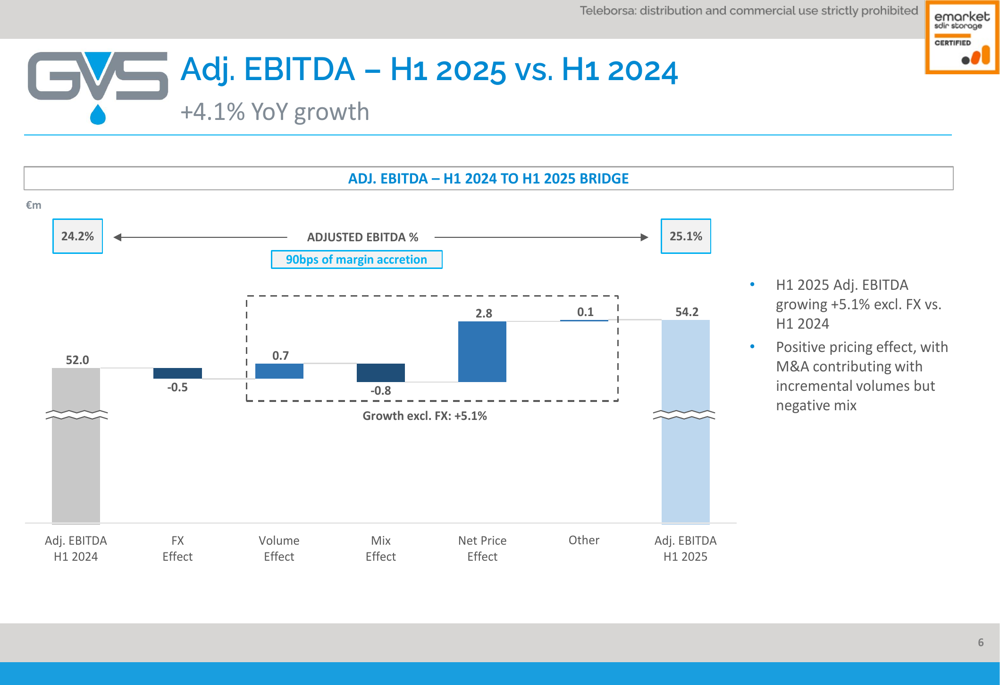

The company’s adjusted EBITDA improvement was primarily driven by favorable pricing effects of €2.8 million, which more than offset negative mix impacts of €0.8 million. Volume contributed a modest €0.7 million to EBITDA growth, while currency effects reduced EBITDA by €0.5 million.

The following waterfall chart details these profitability drivers:

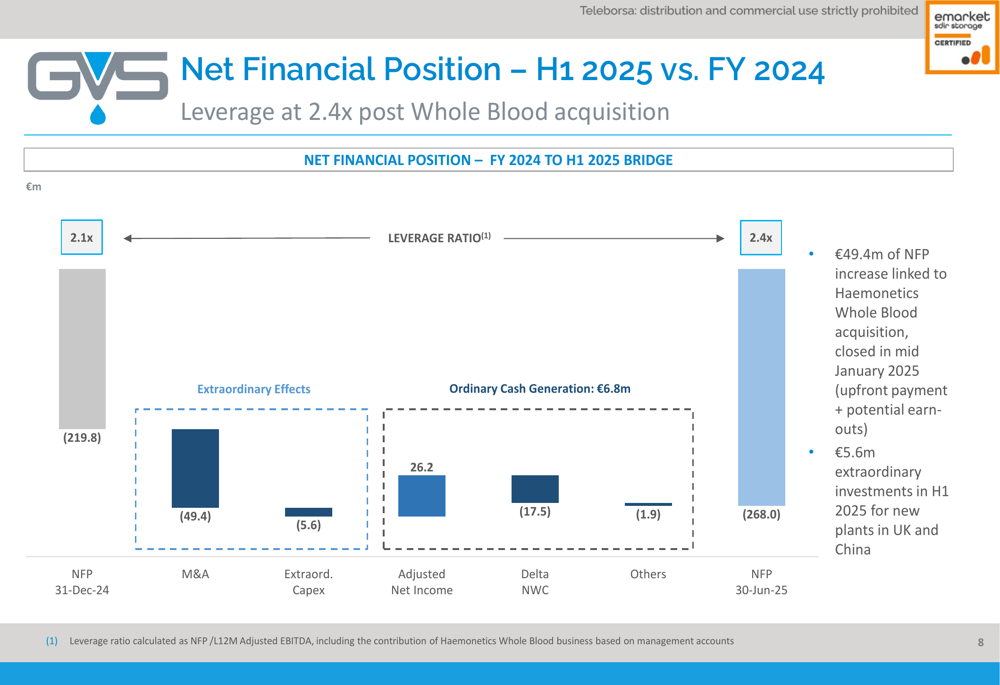

GVS’s net financial position stood at €268.0 million as of June 2025, with a leverage ratio of 2.4x. This represents an increase from the FY 2024 position of €219.8 million (2.1x leverage), primarily due to the €49.4 million impact of the Haemonetics (NYSE:HAE) Whole Blood acquisition and €5.6 million in extraordinary capital expenditures for new plants in the UK and China.

The following chart illustrates the evolution of the company’s financial position:

Strategic Initiatives

GVS’s H1 2025 performance reflects its ongoing strategic initiatives, particularly the integration of the Haemonetics Whole Blood business. Management highlighted that the production transfer from Haemonetics to GVS plants is progressing as planned, with the acquisition expected to contribute meaningfully to future results.

The company also reported significant investments in new manufacturing facilities in the UK and China, representing €5.6 million in extraordinary capital expenditures during the first half. These investments align with GVS’s geographic expansion strategy and efforts to optimize its production footprint.

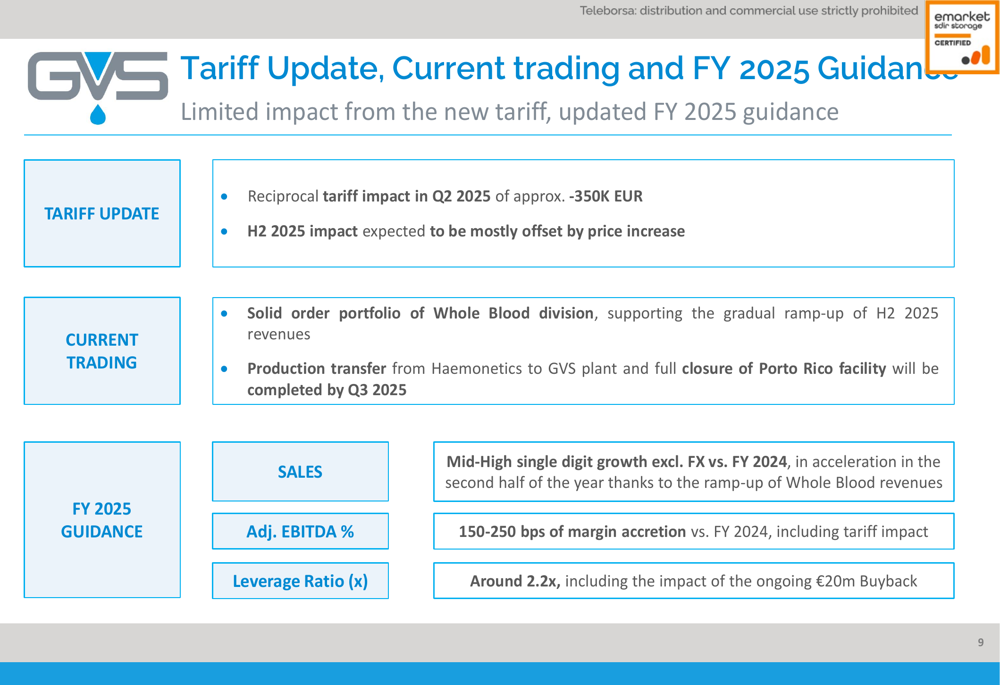

Additionally, GVS noted that reciprocal tariff impacts in Q2 2025 amounted to approximately €350,000, but management expects the H2 2025 impact to be largely offset by price increases, as outlined in the following guidance slide:

Forward-Looking Statements

Despite the mixed H1 2025 results, GVS maintained its full-year guidance, projecting mid-to-high single-digit growth excluding currency effects compared to FY 2024. Management anticipates margin accretion of 150-250 basis points and expects the leverage ratio to improve to approximately 2.2x by year-end.

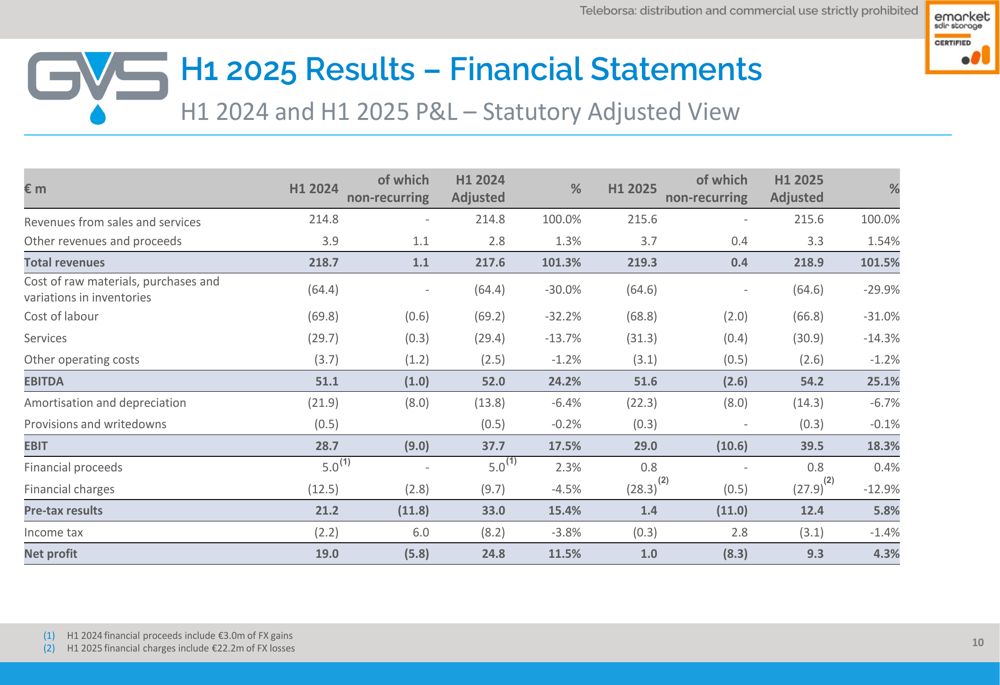

The company’s comprehensive financial statements provide additional context for evaluating its performance trajectory and future prospects:

GVS appears to be navigating a challenging market environment by focusing on profitability improvements and strategic acquisitions, while working to address weakness in its Mobility segment. The company’s ability to expand margins despite modest sales growth suggests effective cost management and pricing strategies, though investors will likely continue monitoring its progress in reducing leverage and accelerating organic growth in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.