S&P 500 rises as health care, tech gain to overshadow Fed independence concerns

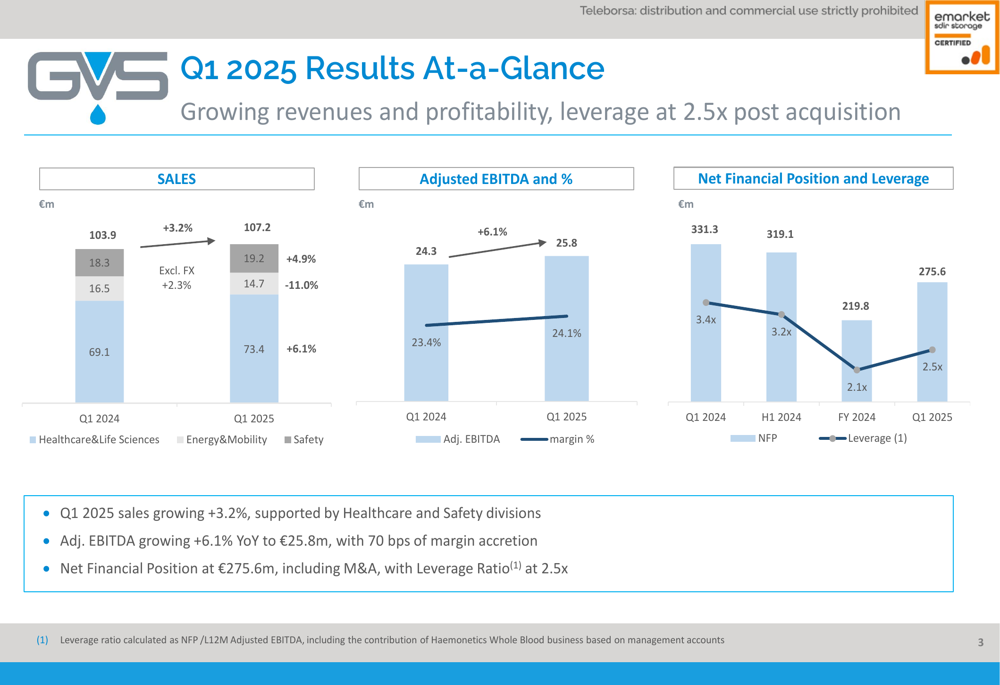

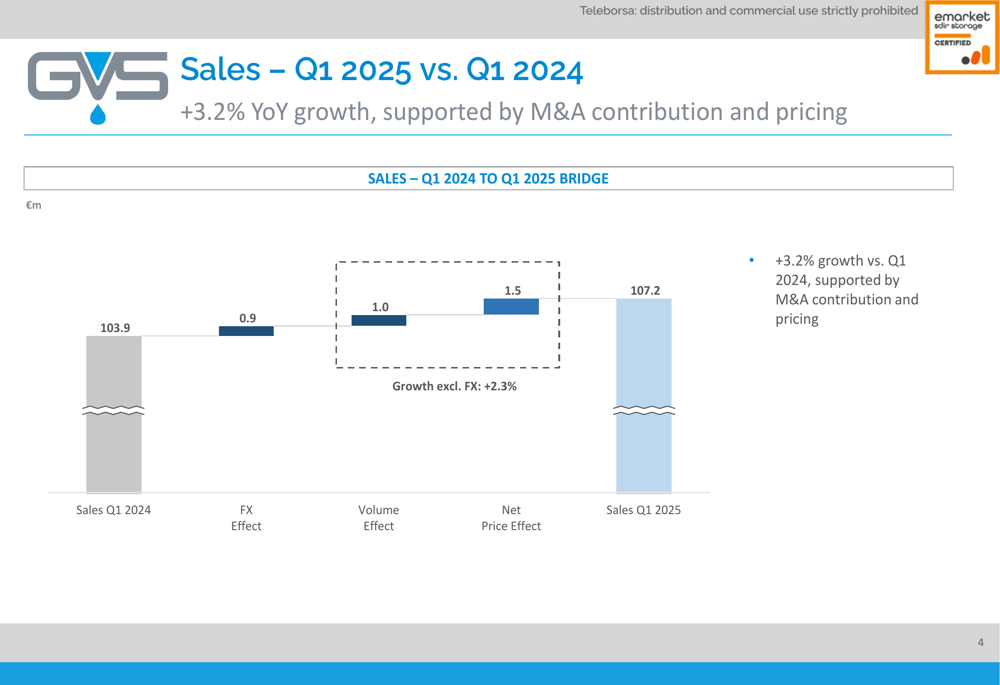

Italian filtration specialist GVS SpA (BIT:GVS) reported solid first-quarter 2025 results on May 15, showing sales growth of 3.2% year-over-year to €107.2 million, driven primarily by strong performance in its Healthcare & Life Sciences division and supported by recent acquisition activity.

Quarterly Performance Highlights

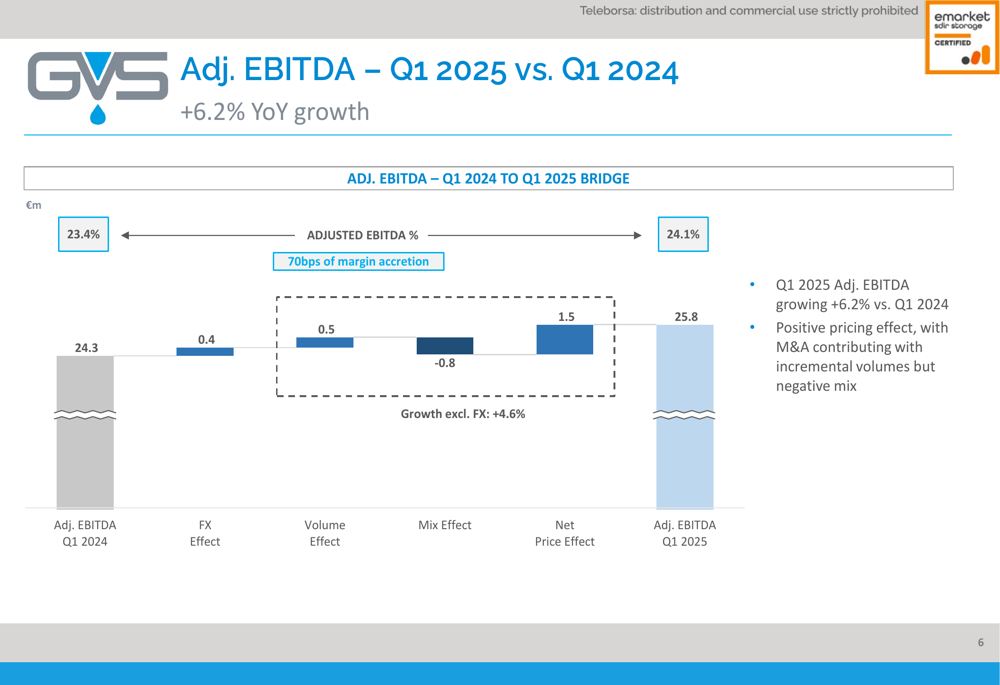

GVS delivered adjusted EBITDA of €25.8 million in Q1 2025, representing a 6.1% increase compared to the same period last year, with margins expanding by 70 basis points to 24.1%. When excluding foreign exchange impacts, adjusted net income grew by an impressive 21.6% to €12.0 million, improving the margin to 11.2% from 9.5% in Q1 2024.

"Q1 2025 sales growing +3.2%, supported by Healthcare and Safety divisions," the company noted in its presentation, highlighting the positive momentum in its core business segments.

As shown in the following chart detailing the quarterly performance metrics:

The company’s sales growth was supported by positive contributions from foreign exchange effects, volume increases, and favorable pricing, as illustrated in this sales bridge analysis:

Detailed Financial Analysis

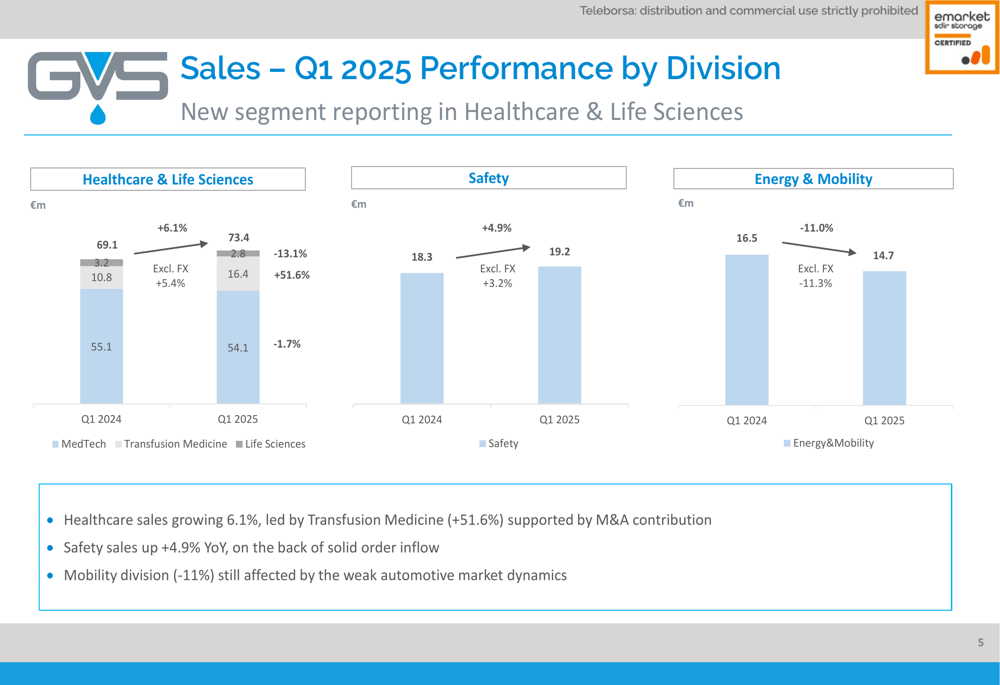

GVS’s performance varied significantly across its three business divisions. The Healthcare & Life Sciences division, which represents the largest portion of the company’s revenue, grew by 6.1% year-over-year to €73.4 million. This growth was primarily driven by the Transfusion Medicine segment, which surged 51.6% following the acquisition of Haemonetics (NYSE:HAE)’ Whole Blood business in January 2025.

The Safety division also performed well, with sales increasing by 4.9% to €19.2 million, supported by solid order inflow. However, the Energy & Mobility division continued to face challenges, with sales declining by 11.0% to €14.7 million due to persistent weakness in the automotive market.

The divisional performance breakdown is illustrated in the following chart:

The company’s adjusted EBITDA growth of 6.1% was driven by positive foreign exchange effects, volume increases, and favorable pricing, which more than offset negative mix effects:

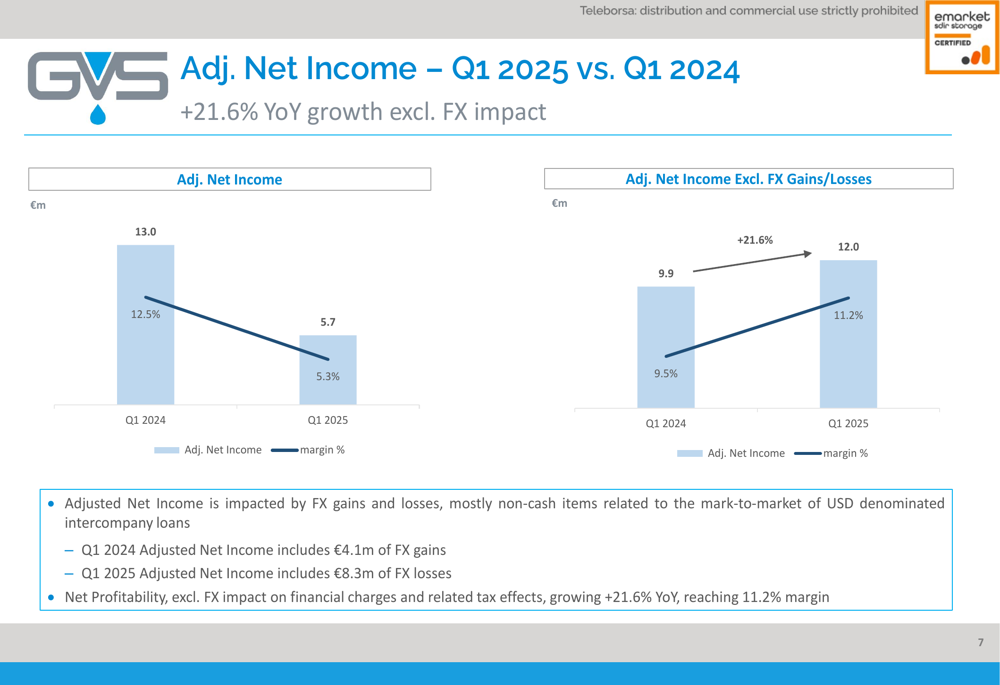

GVS’s adjusted net income showed divergent results depending on whether foreign exchange impacts were included. Including FX effects, adjusted net income declined to €5.7 million from €13.0 million in Q1 2024. However, excluding these impacts, adjusted net income grew by 21.6% to €12.0 million.

"Adjusted Net Income is impacted by FX gains and losses, mostly non-cash items related to the mark-to-market of USD denominated intercompany loans," the company explained, noting that Q1 2024 included €4.1 million of FX gains while Q1 2025 included €8.3 million of FX losses.

Strategic Initiatives & Forward-Looking Statements

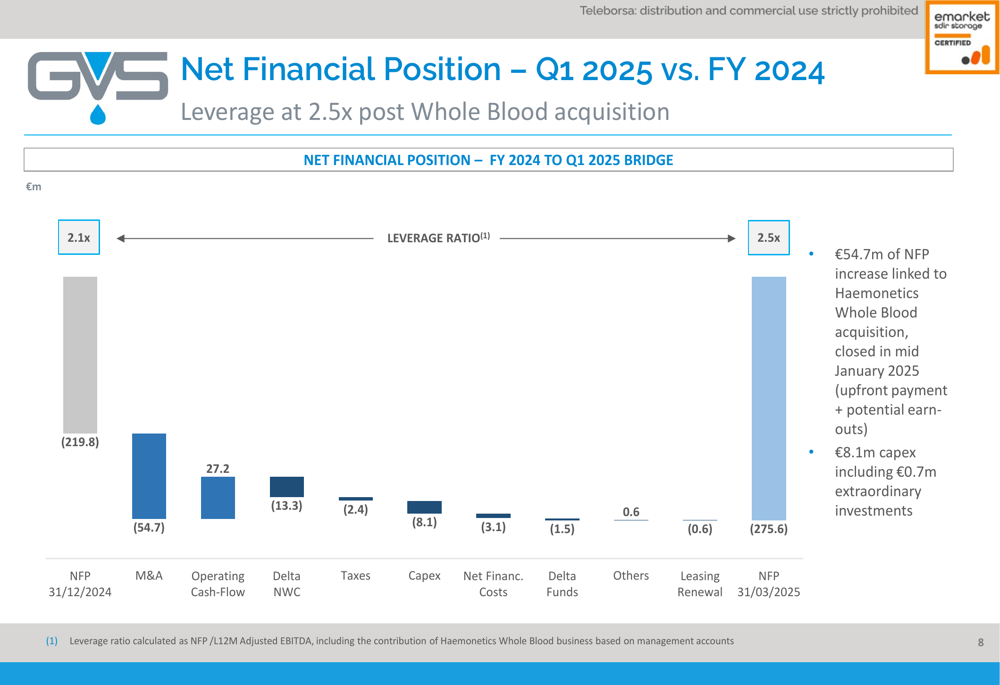

GVS’s net financial position stood at €275.6 million at the end of Q1 2025, compared to €219.8 million at the end of 2024. This increase was primarily due to the €54.7 million impact from the Haemonetics Whole Blood acquisition, which closed in mid-January 2025.

The company’s cash flow and financial position changes are detailed in this bridge chart:

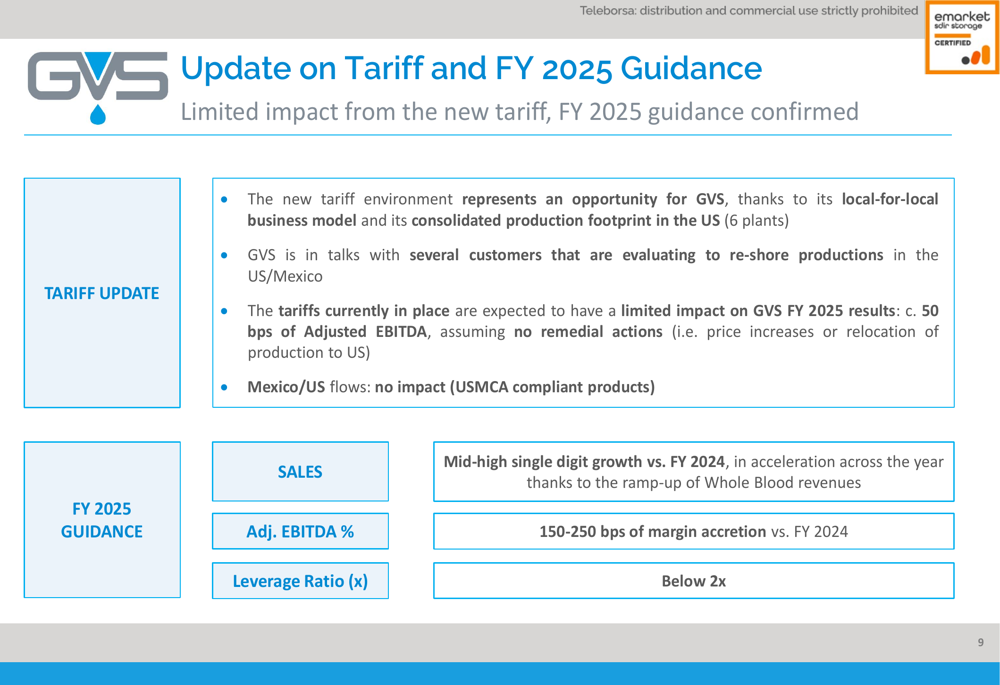

Looking ahead, GVS provided a positive outlook for the remainder of 2025, projecting mid-to-high single-digit sales growth compared to 2024, with acceleration expected throughout the year as the Whole Blood business ramps up. The company also anticipates 150-250 basis points of margin accretion and expects to reduce its leverage ratio to below 2x by year-end.

Notably, GVS views the evolving tariff environment as an opportunity rather than a threat, citing its local-for-local business model and established US manufacturing footprint with six plants. The company is in discussions with several customers considering reshoring production to the US or Mexico and expects current tariffs to have a limited impact of approximately 50 basis points on its 2025 adjusted EBITDA.

GVS shares rose 0.78% to €4.51 following the results announcement, continuing their recovery from the 52-week low of €3.83, though still well below the 52-week high of €7.52.

The Q1 2025 results show improvement from the company’s Q4 2024 performance, which had missed revenue expectations but demonstrated strong profitability growth. The continued strength in the Healthcare division and strategic positioning to benefit from reshoring trends suggest GVS is on track to meet its full-year guidance despite ongoing challenges in the automotive sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.