Gold prices steady as traders assess Fed rate outlook after soft US data

Introduction & Market Context

Specialty auto insurer Hagerty Inc. (NYSE:HGTY) delivered strong second-quarter results, continuing its momentum from earlier in the year. The company’s Q2 2025 investor presentation revealed substantial growth across key metrics, with total revenue increasing 18% year-over-year to $688 million. The strong performance prompted management to raise its full-year 2025 guidance.

Hagerty’s stock closed at $10.02 on August 1, 2025, down 1.38% for the day, but has shown resilience with a 52-week range of $8.03 to $12.35. The company’s Q2 results build on its impressive Q1 performance, which saw the stock surge 9.46% following the earnings announcement.

Quarterly Performance Highlights

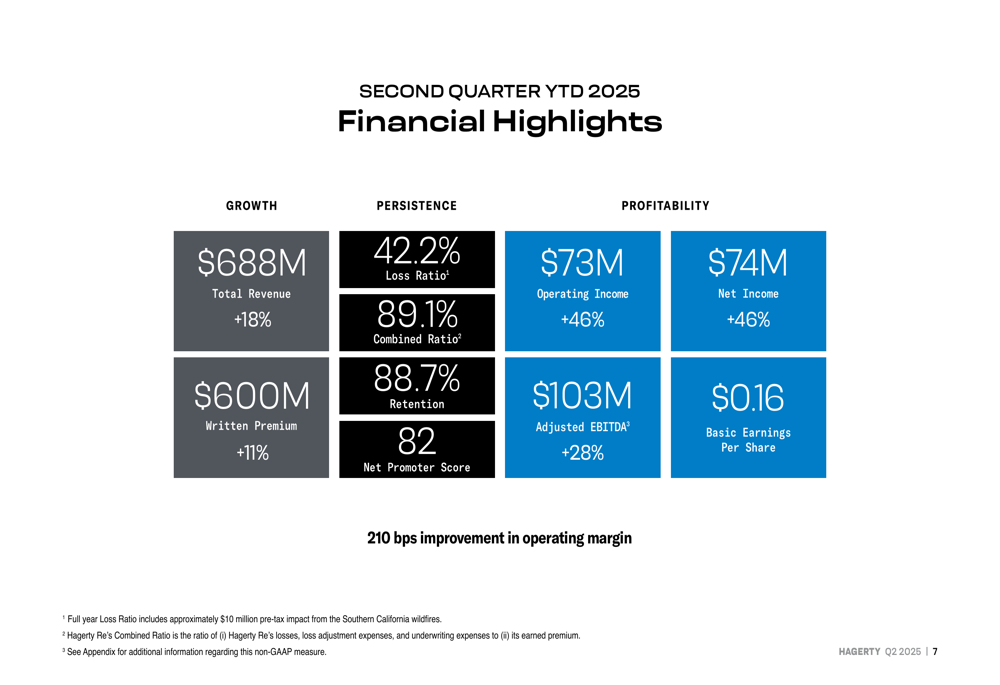

Hagerty reported significant improvements across all key financial metrics for Q2 YTD 2025. The company achieved 18% total revenue growth to $688 million, driven by 12% growth in commission and fee revenue and 68% growth in membership, marketplace, and other revenue. Written premium grew by 11% to $600 million.

Profitability metrics showed even stronger improvement, with operating income increasing 46% to $73 million and net income rising 46% to $74 million. The company also improved its operating margin by 210 basis points and reported adjusted EBITDA of $103 million, up 28% year-over-year.

As shown in the following financial highlights chart:

The company’s insurance operations continued to demonstrate industry-leading performance with a loss ratio of 42.2% and a combined ratio of 89.1%. Customer metrics remained strong with a retention rate of 88.7% and an impressive Net Promoter Score of 82, indicating high customer satisfaction.

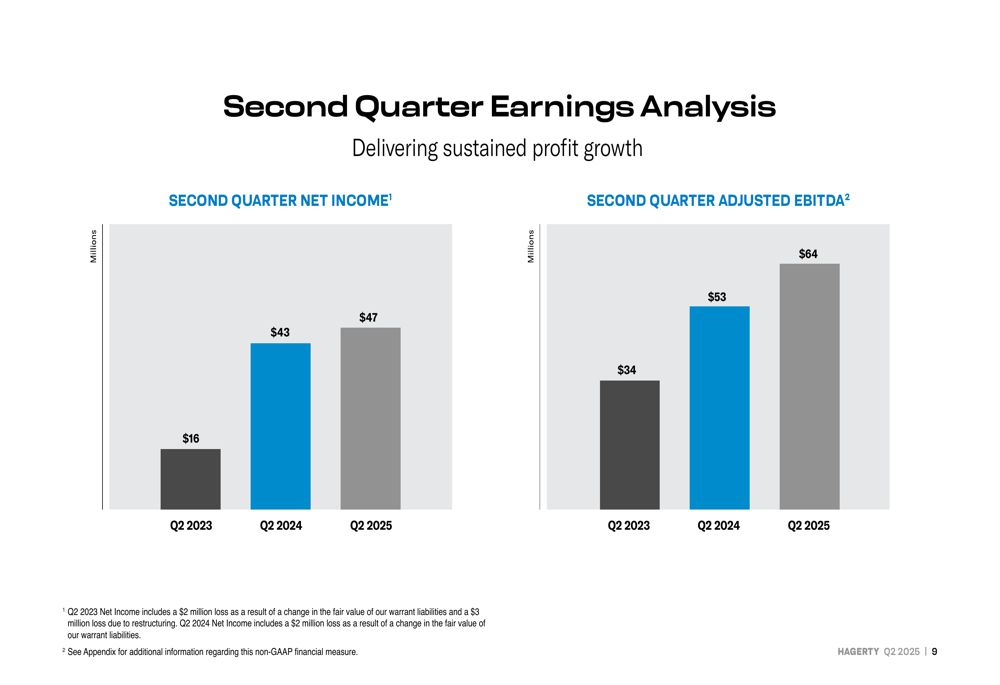

Looking at quarterly earnings trends, Hagerty has shown consistent improvement in both net income and adjusted EBITDA over the past three years:

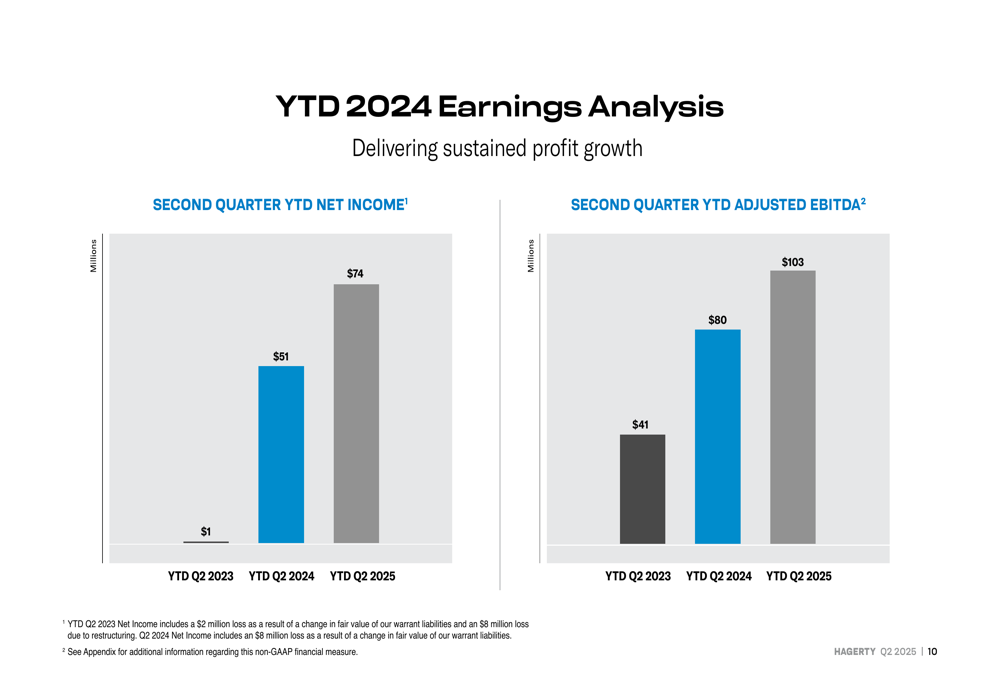

The year-to-date performance is even more impressive when viewed over a three-year period, showing substantial growth from the modest $1 million net income in YTD Q2 2023:

Strategic Initiatives

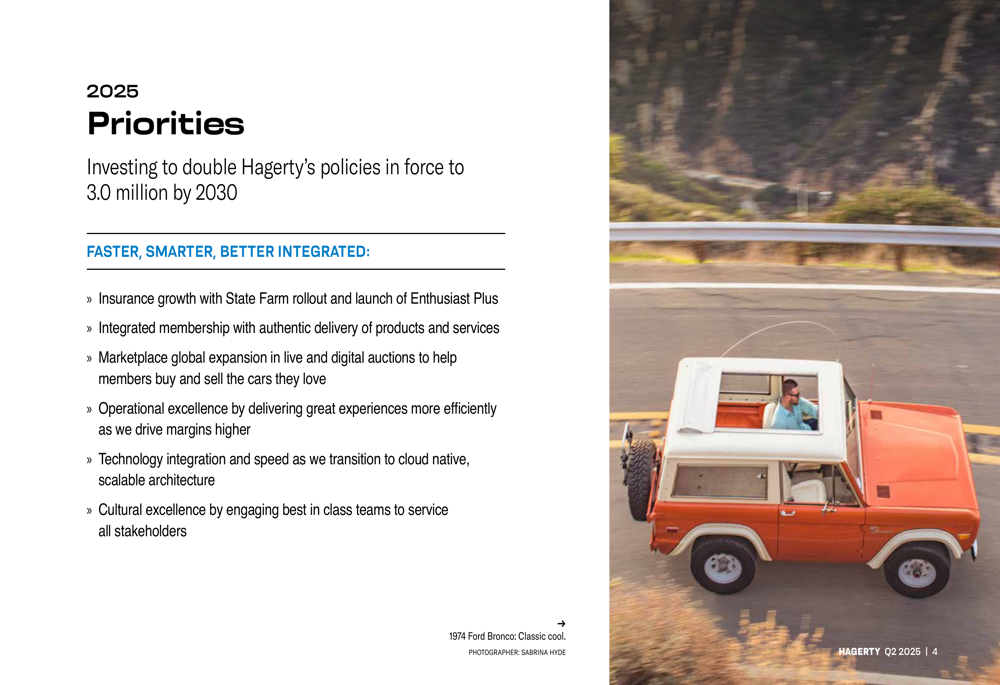

Hagerty outlined its strategic priorities for 2025, focusing on its goal to double policies in force to 3.0 million by 2030. The company is pursuing several initiatives under the theme "Faster, Smarter, Better Integrated":

A key component of Hagerty’s strategy is investing in technology infrastructure to support growth and improve efficiency. In July 2025, the company launched Enthusiast+, a new insurance product on the Duck Creek platform. This initiative is part of Hagerty’s efforts to address challenges with its aging IT infrastructure, which has impacted operational efficiency and scalability.

The company acknowledged that near-term redundant systems will result in higher operating and software expenses, but expects technology spend to moderate as a percentage of revenue in 2026 as these investments yield operational improvements.

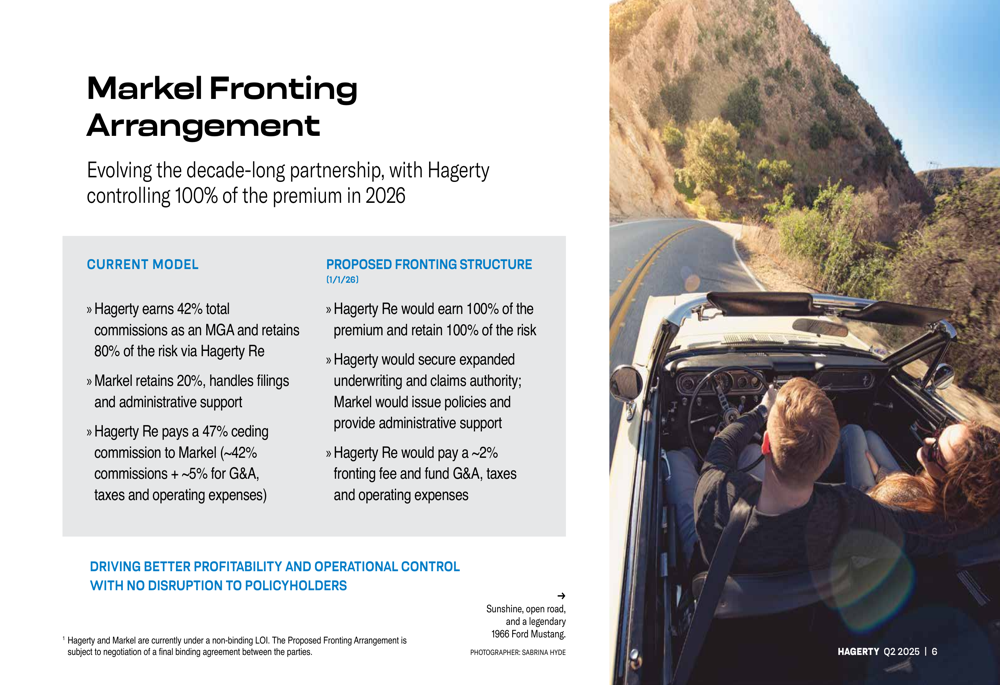

Markel (NYSE:MKL) Partnership Evolution

One of the most significant strategic developments announced is Hagerty’s non-binding letter of intent with Markel for a new fronting arrangement effective January 1, 2026. Under this proposed structure, Hagerty would control 100% of the premium, compared to the current model where Hagerty earns 42% total commissions as an MGA and retains 80% of the risk via Hagerty Re.

The following slide illustrates the current and proposed structures:

This arrangement is expected to drive better profitability and operational control with no disruption to policyholders. Under the new structure, Hagerty Re would pay a ~2% fronting fee to Markel instead of the current 47% ceding commission, significantly improving economics for Hagerty.

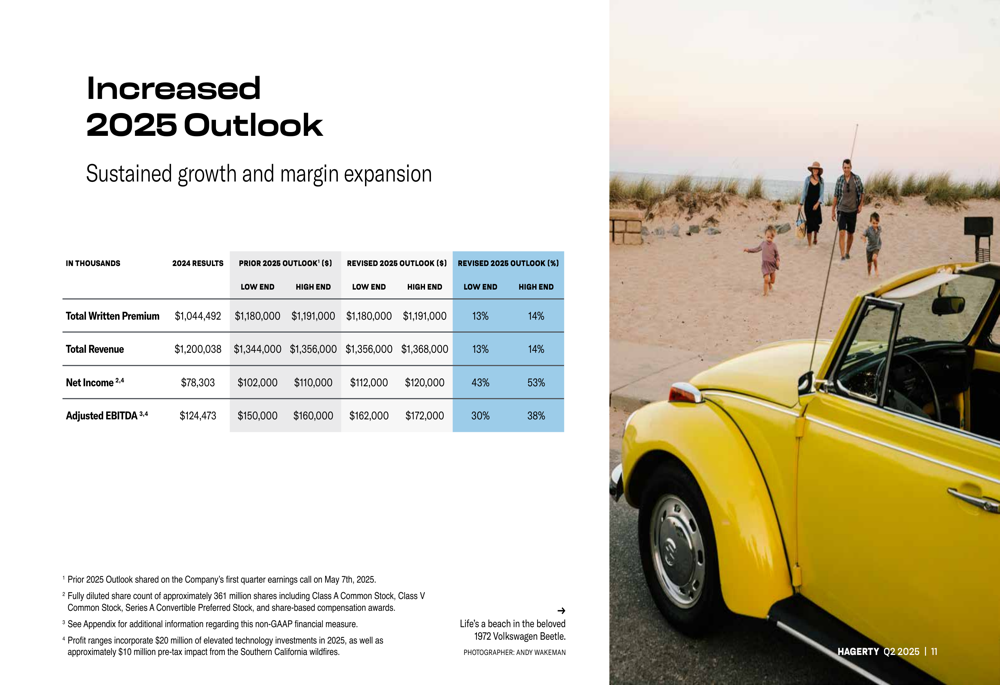

Increased 2025 Outlook

Based on the strong first-half performance, Hagerty increased its full-year 2025 guidance across all key metrics:

The revised outlook projects total revenue of $1.356-1.368 billion, representing 13-14% growth over 2024. Net income is expected to reach $112-120 million, a 43-53% increase, while adjusted EBITDA is projected at $162-172 million, up 30-38% from 2024.

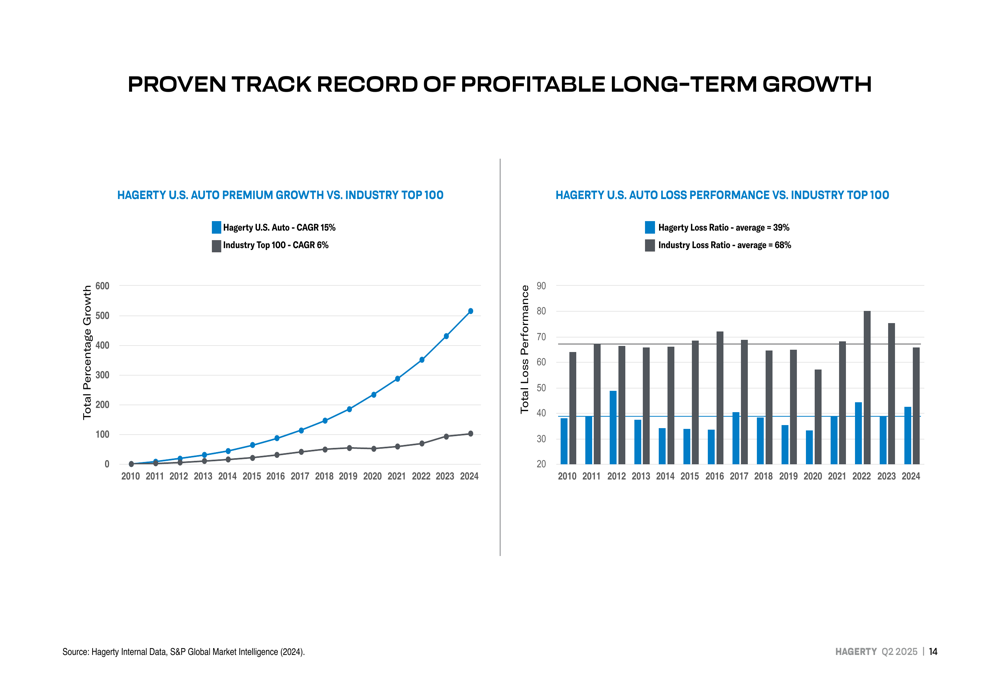

Long-term Growth Strategy

Hagerty’s long-term strategy is built on its proven track record of outperforming the broader auto insurance industry. The company has achieved a 15% CAGR in U.S. auto premium growth compared to the industry average of 6%, while maintaining a significantly better loss ratio (39% vs. industry average of 68%).

As shown in the following comparative analysis:

The company sees substantial growth opportunity in its addressable market of 46.5 million vehicles, where it currently has only 6.7% overall penetration. While Hagerty has achieved 14.4% penetration in the pre-1981 vehicle market, its penetration in the larger post-1980 enthusiast vehicle market is only 3.1%, representing a significant growth opportunity.

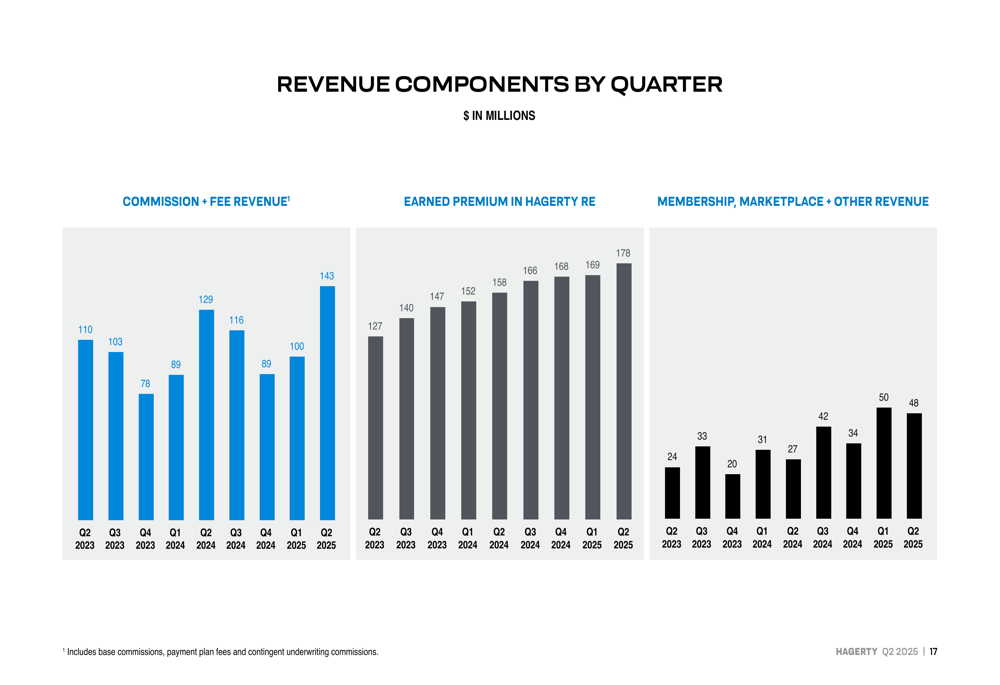

Hagerty’s revenue diversification strategy is also showing results, with marketplace revenue growing 232% in Q2 YTD 2025. The company’s quarterly revenue components show the increasing contribution from membership, marketplace, and other revenue streams:

With its strong financial performance, strategic initiatives, and large addressable market, Hagerty appears well-positioned to achieve its goal of doubling policies in force to 3 million by 2030, while continuing to deliver strong financial results for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.