IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

Hanmi Financial Corporation (NASDAQ:HAFC) released its first quarter 2025 earnings presentation on April 22, 2025, revealing stable financial performance with notable improvements in net interest margin and deposit growth. The Korean-American focused bank reported unchanged net income compared to the previous quarter while demonstrating progress in its strategic initiatives.

The stock responded positively to the earnings release, trading up 4.36% to $22.52 in the regular session, building on momentum from the previous quarter when the company exceeded EPS expectations.

Quarterly Performance Highlights

Hanmi reported net income of $17.7 million for Q1 2025, unchanged from the previous quarter, with diluted earnings per share of $0.58. The company achieved a return on average equity of 8.92% and return on average assets of 0.94%.

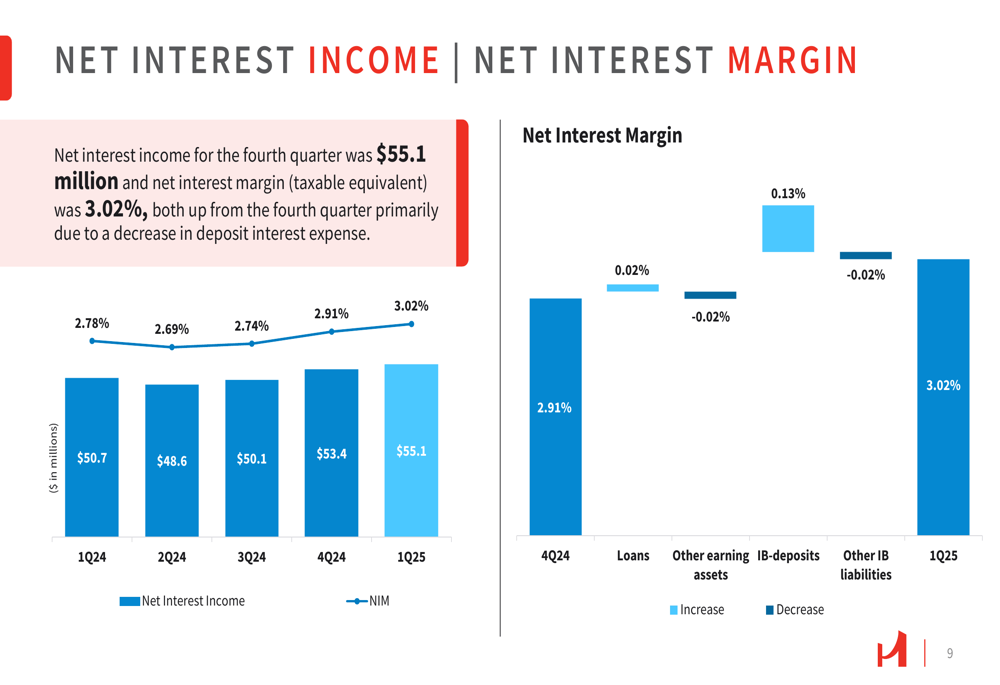

Net interest income increased to $55.1 million, up 3.1% from the prior quarter, driven by an 11 basis point improvement in net interest margin to 3.02%. This margin expansion came primarily from lower deposit costs, as the average cost of interest-bearing deposits decreased by 27 basis points to 3.69%.

As shown in the following chart tracking net interest income and margin trends over the past five quarters:

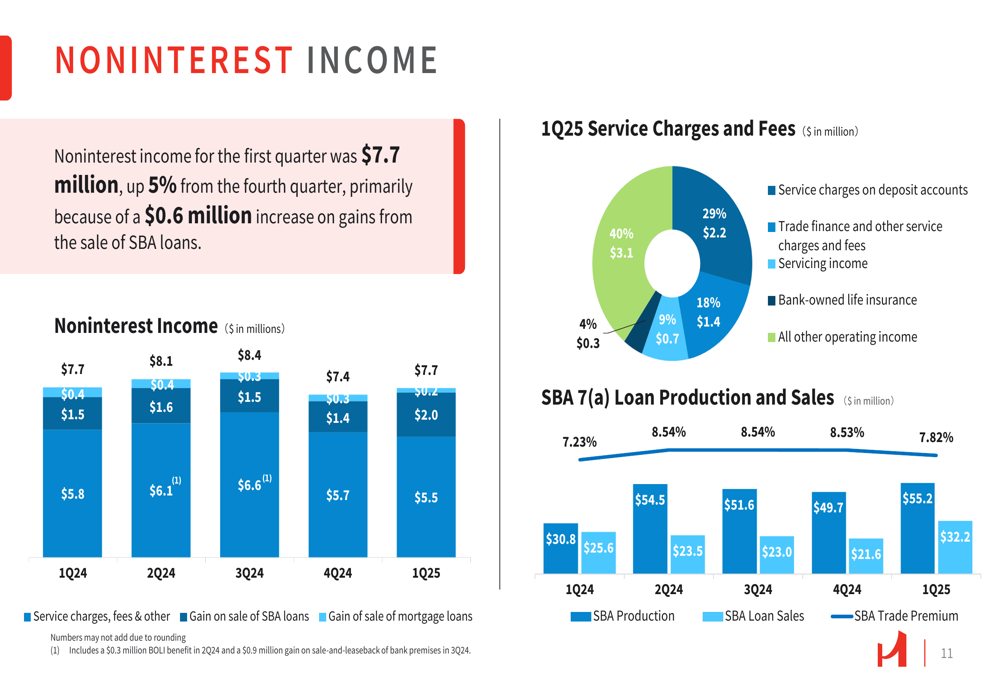

Noninterest income grew 5.0% quarter-over-quarter to $7.7 million, primarily due to a $0.6 million increase in gains from SBA (LON:SBA) loan sales. Noninterest expense increased slightly by 1.3% to $35.0 million, resulting in an efficiency ratio of 55.69%.

The following chart illustrates the composition of noninterest income across service charges, loan sale gains, and other revenue streams:

Loan and Deposit Trends

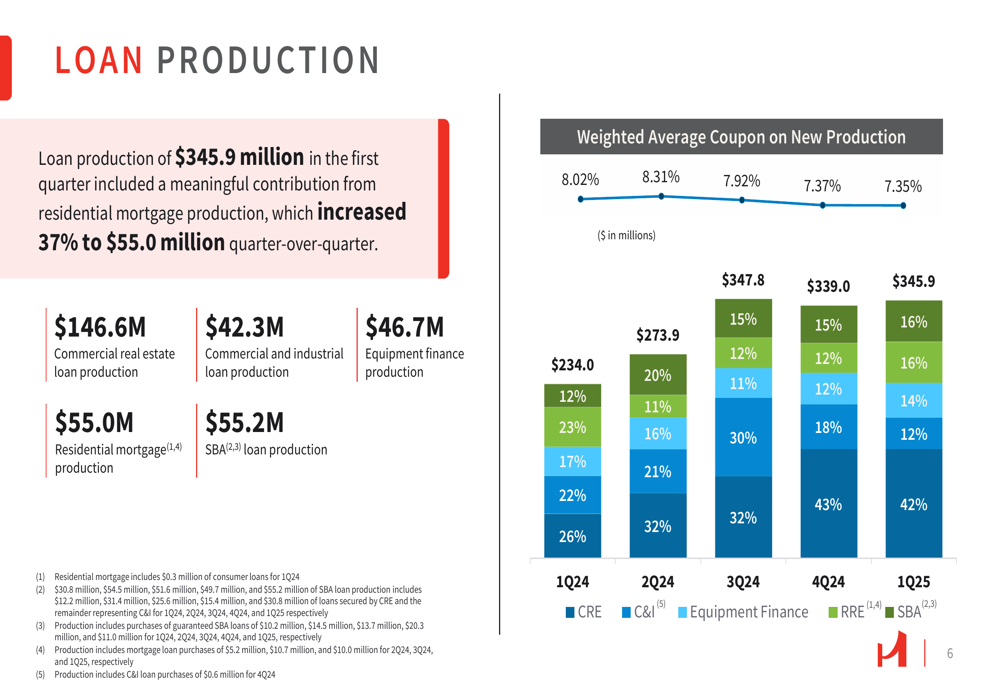

Hanmi’s loan portfolio grew modestly by 0.5% from the previous quarter to $6.28 billion. Loan production totaled $345.9 million in Q1 2025, with a weighted average coupon of 7.35%. Commercial real estate loans dominated production at 42%, followed by SBA loans at 16% and residential mortgages at 14%.

Notably, residential mortgage production increased 37% quarter-over-quarter to $55.0 million, demonstrating growth in this segment despite the higher interest rate environment.

The following chart details loan production by category over the past five quarters:

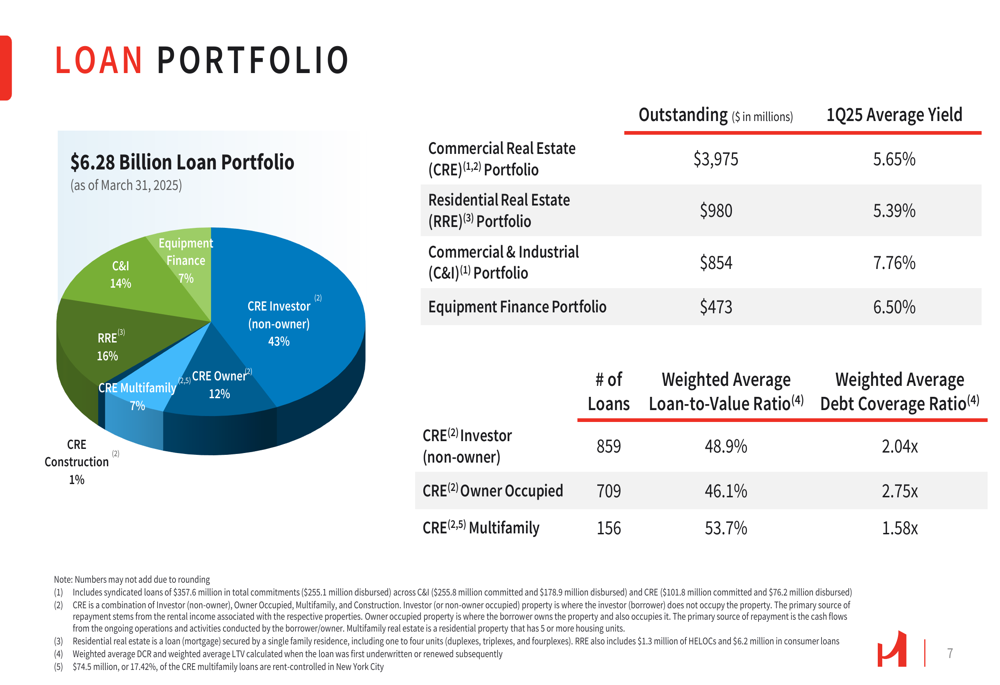

The loan portfolio remains diversified across multiple segments, with commercial real estate representing 63% of total loans, residential real estate 16%, commercial and industrial loans 14%, and equipment finance 7%. Within the CRE portfolio, investor (non-owner) properties represent the largest segment at 43% of total loans.

The following chart illustrates the composition of Hanmi’s loan portfolio:

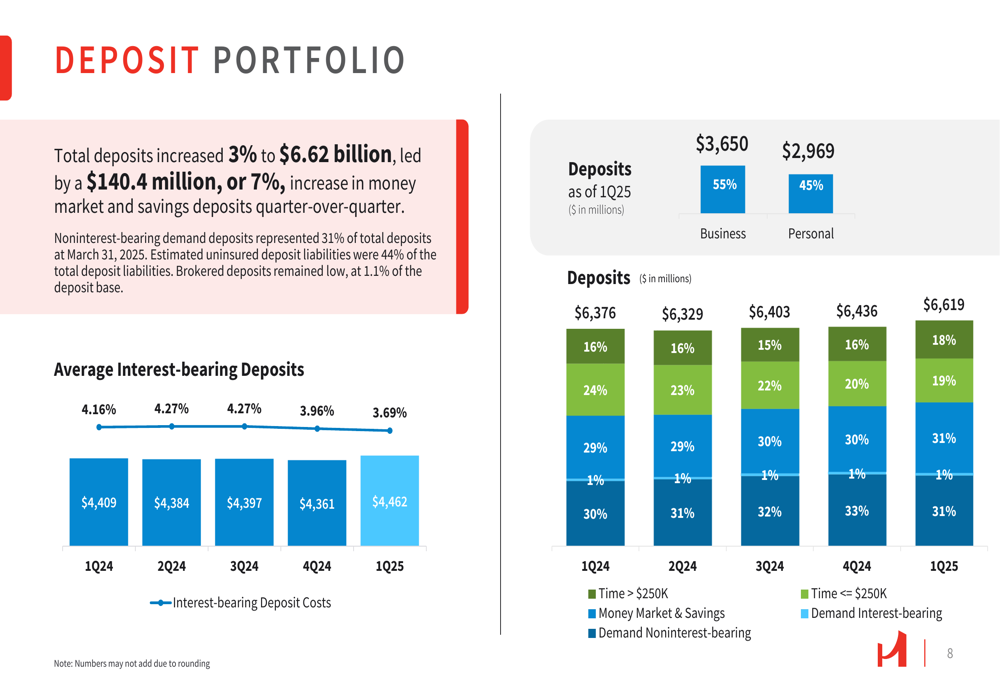

On the funding side, deposits increased 2.9% quarter-over-quarter to $6.62 billion. Noninterest-bearing demand deposits represented 31.2% of total deposits, providing a stable low-cost funding source. Business deposits accounted for 55% of total deposits, with personal deposits making up the remaining 45%.

The following chart shows deposit trends by type over the past five quarters:

Asset Quality and Capital Management

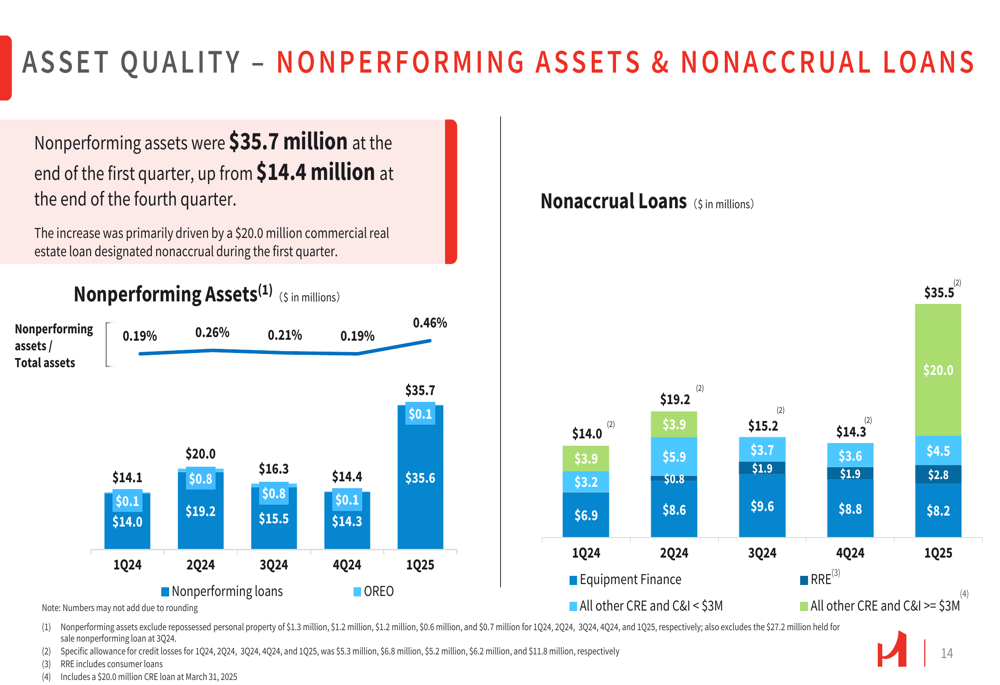

Hanmi maintained solid asset quality metrics in Q1 2025, with an allowance for credit losses of $70.6 million, representing 1.12% of total loans. The company recorded credit loss expense of $2.7 million, with net loan charge-offs to average loans of 0.13%.

However, the presentation noted a $20.8 million increase in classified loans, primarily driven by a $20.0 million nonaccrual commercial real estate loan. This development bears watching in future quarters but remains manageable within the context of the overall portfolio.

The following chart shows the trend in nonperforming assets and nonaccrual loans:

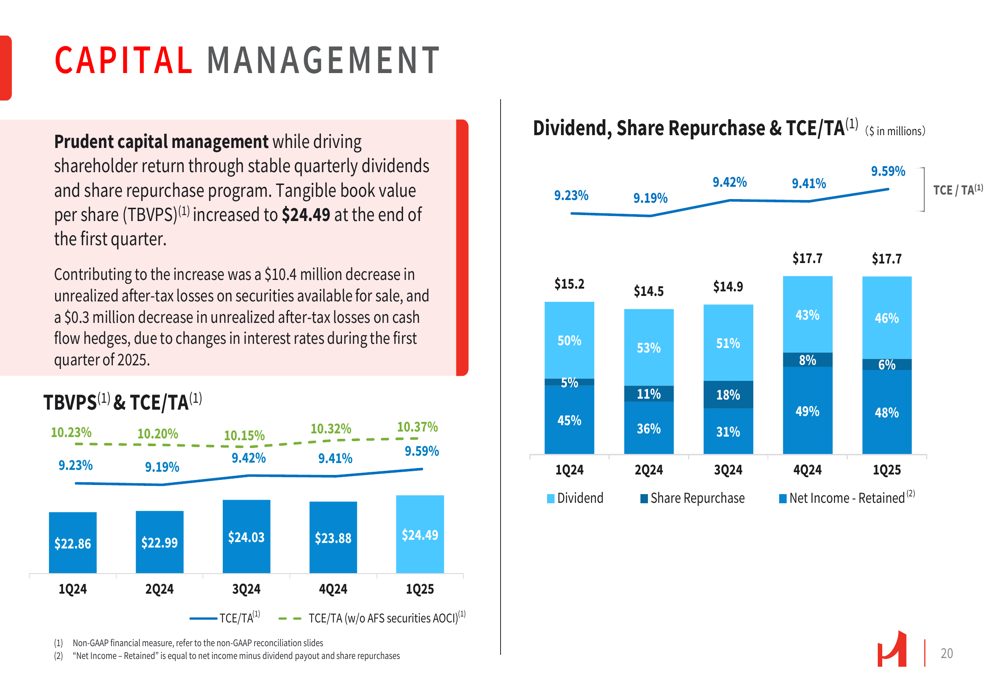

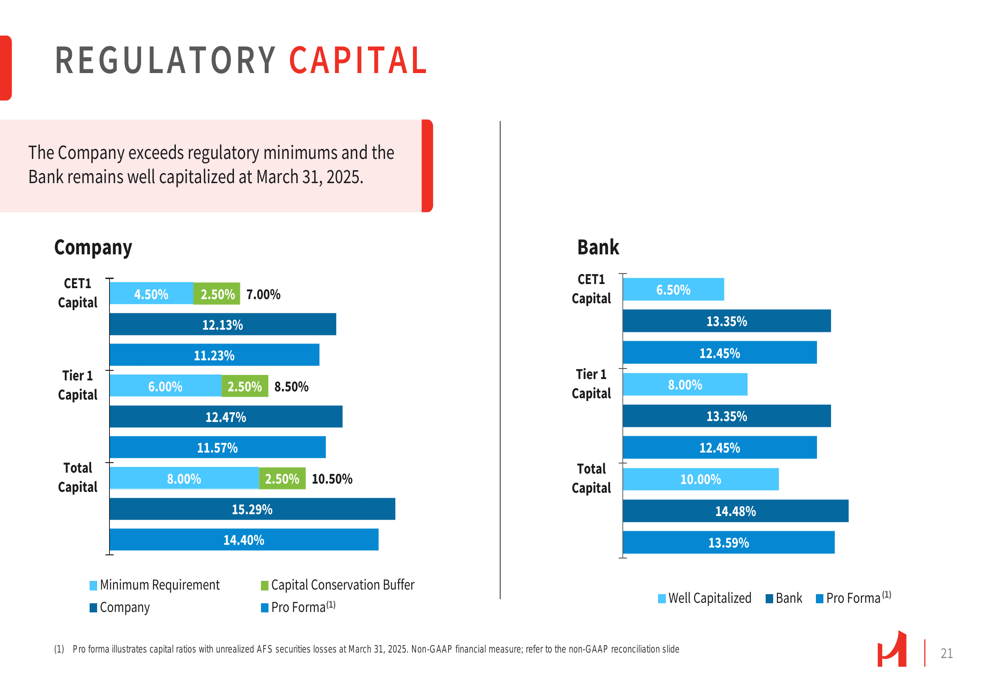

From a capital perspective, Hanmi maintained strong ratios with tangible common equity to tangible assets of 9.59%, common equity tier 1 capital ratio of 12.13%, and total risk-based capital ratio of 15.29%. These levels significantly exceed regulatory requirements for well-capitalized institutions.

Tangible book value per share increased to $24.49, continuing its steady upward trend as illustrated in the following capital management chart:

Strategic Initiatives

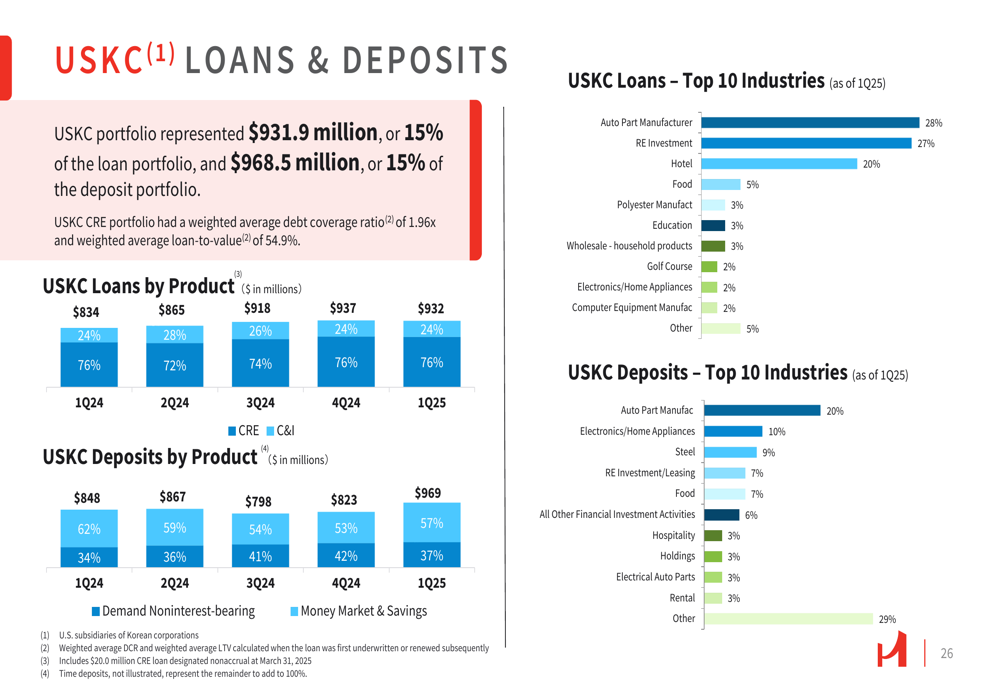

Hanmi continues to focus on its relationship-driven banking model with particular emphasis on the Korean-American market. The U.S.-Korea Corporate (USKC) portfolio represented $931.9 million or 15% of the loan portfolio and $968.5 million or 15% of the deposit portfolio.

This strategic focus aligns with comments from CEO Bonnie Lee during the Q4 2024 earnings call, where she highlighted the Corporate Korea initiative as a core growth strategy. The initiative grew the USKC loan portfolio by 23% in 2024, and the Q1 2025 results suggest continued momentum in this segment.

The following chart provides a breakdown of the USKC portfolio by product type:

Another strategic priority is portfolio diversification, particularly reducing the concentration in commercial real estate while growing commercial and industrial lending. While CRE still represents 63% of the total portfolio, the company continues to emphasize relationship-based C&I lending to create a more balanced portfolio over time.

Forward-Looking Statements

Building on guidance provided during the Q4 2024 earnings call, Hanmi appears on track to achieve its projected low-to-mid single-digit loan growth for 2025. The company’s focus on expanding C&I exposure while reducing CRE concentration as a percentage of the portfolio remains a key strategic priority.

The decreasing cost of interest-bearing deposits, combined with relatively stable loan yields, positions Hanmi to potentially see continued improvement in net interest margin if the Federal Reserve proceeds with expected rate cuts in 2025.

The company’s strong capital position, with regulatory ratios well above requirements, provides flexibility for continued organic growth, potential share repurchases, and dividend payments to shareholders.

Hanmi’s Q1 2025 results demonstrate the company’s ability to maintain stable performance while navigating the evolving interest rate environment. The focus on relationship banking, particularly within the Korean-American community, continues to provide a competitive advantage in deposit gathering and loan production. While commercial real estate exposure remains elevated, the company’s disciplined underwriting and strong credit metrics provide some reassurance against potential market volatility.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.