Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

Harmony Biosciences Holdings (NASDAQ:HRMY) presented its Q1 2025 financial results and business update on May 6, 2025, highlighting continued revenue growth and pipeline advancement. The company, which specializes in treatments for sleep-wake disorders and other central nervous system conditions, reported strong financial performance while maintaining its full-year guidance.

The presentation comes as Harmony (JO:HARJ)’s stock has shown volatility, with a 1.19% decline in the previous session to $29.96, but a notable 5.11% gain in pre-market trading. The company’s shares have traded between $26.47 and $41.61 over the past 52 weeks, reflecting both challenges and opportunities in the specialty pharmaceutical space.

Quarterly Performance Highlights

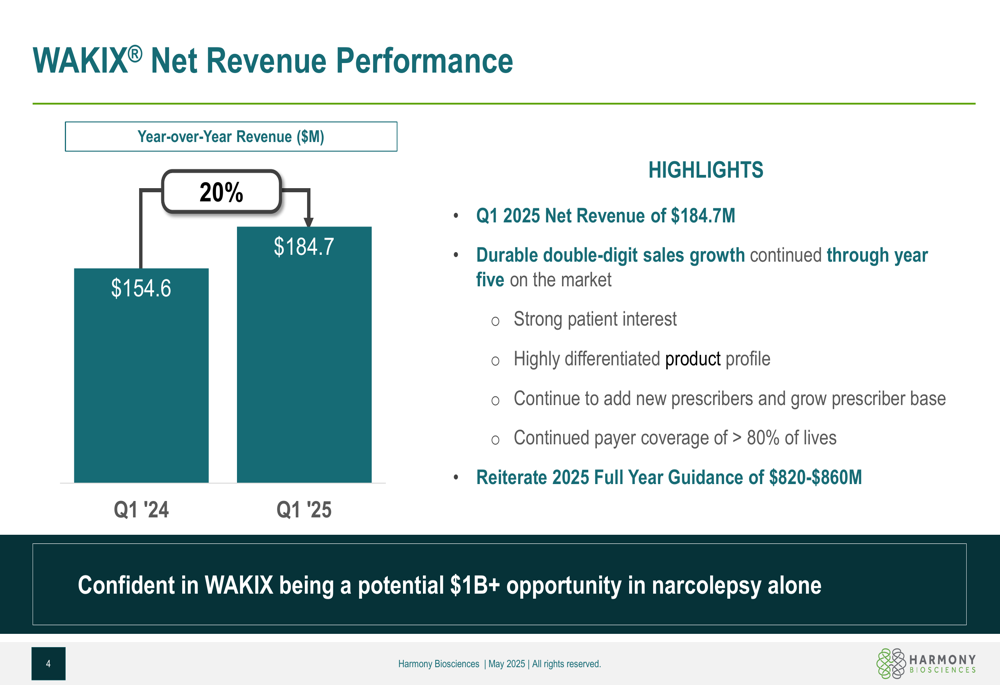

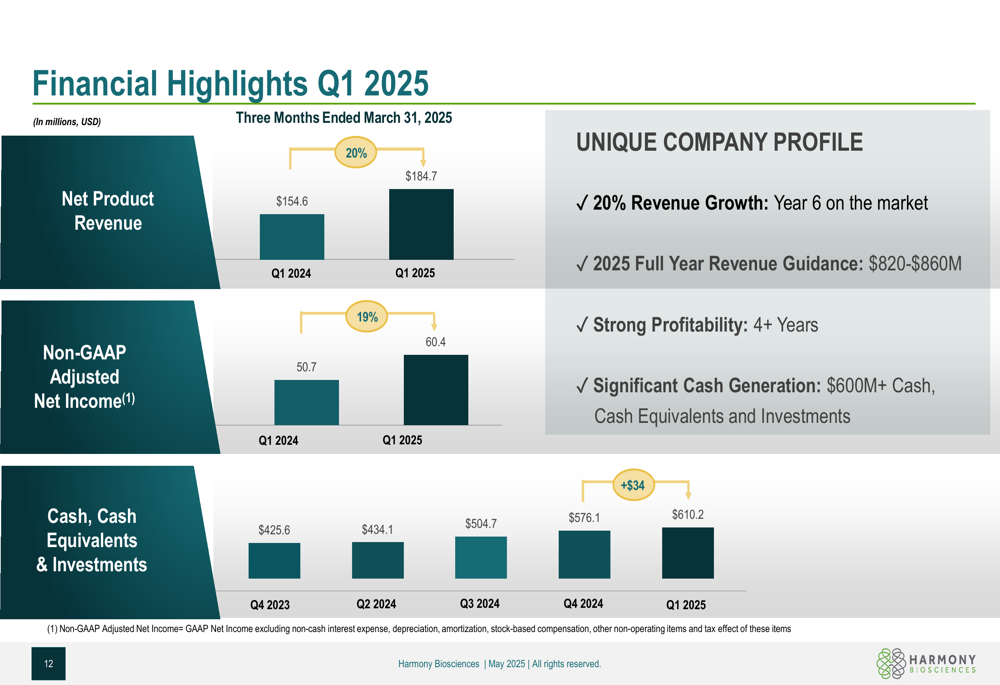

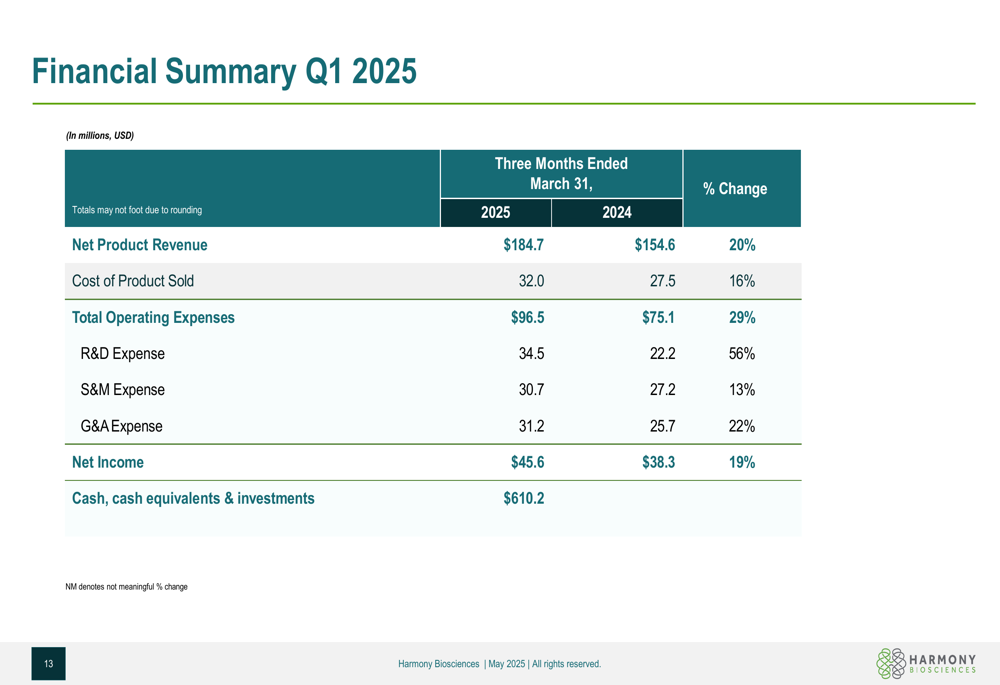

Harmony Biosciences reported Q1 2025 net product revenue of $184.7 million, representing a 20% increase compared to $154.6 million in Q1 2024. This growth demonstrates the continued commercial success of WAKIX, the company’s flagship narcolepsy treatment, now in its sixth year on the market.

As shown in the following chart of quarterly revenue performance:

The company highlighted several factors contributing to WAKIX’s sustained growth, including strong patient interest, a highly differentiated product profile, continued expansion of the prescriber base, and maintained payer coverage exceeding 80% of lives. Management expressed confidence in WAKIX becoming a potential $1 billion-plus opportunity in narcolepsy alone.

Pipeline Development and Upcoming Catalysts

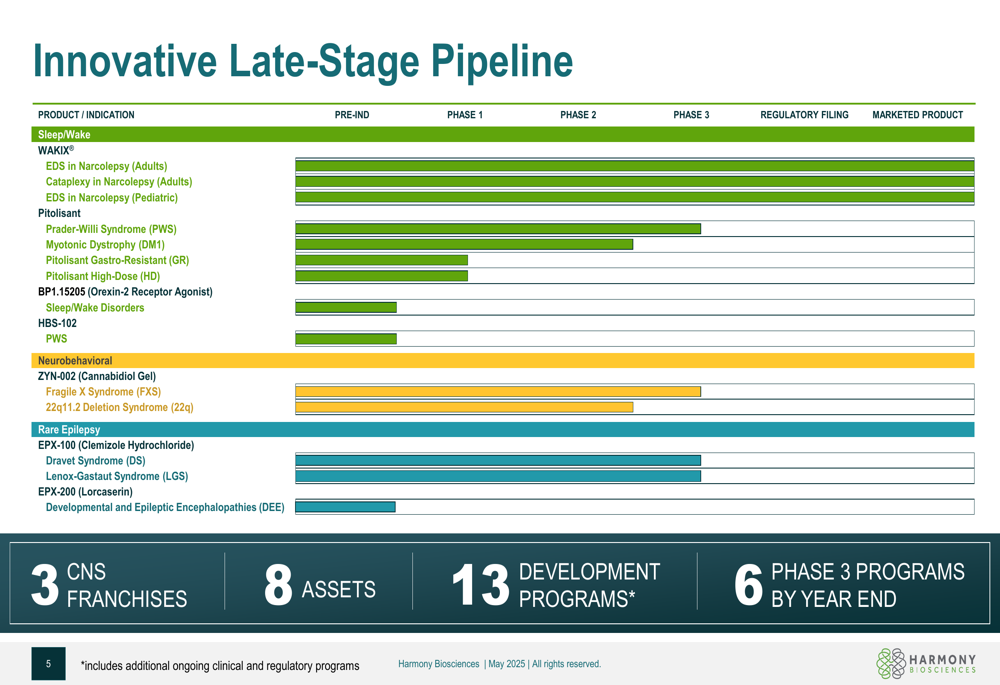

Harmony’s presentation emphasized its expanding late-stage pipeline across three CNS franchises: sleep-wake disorders, neurobehavioral conditions, and epilepsy. The company currently has four ongoing Phase 3 registrational trials and expects to have up to six by year-end.

The comprehensive pipeline overview illustrates the breadth of Harmony’s development programs:

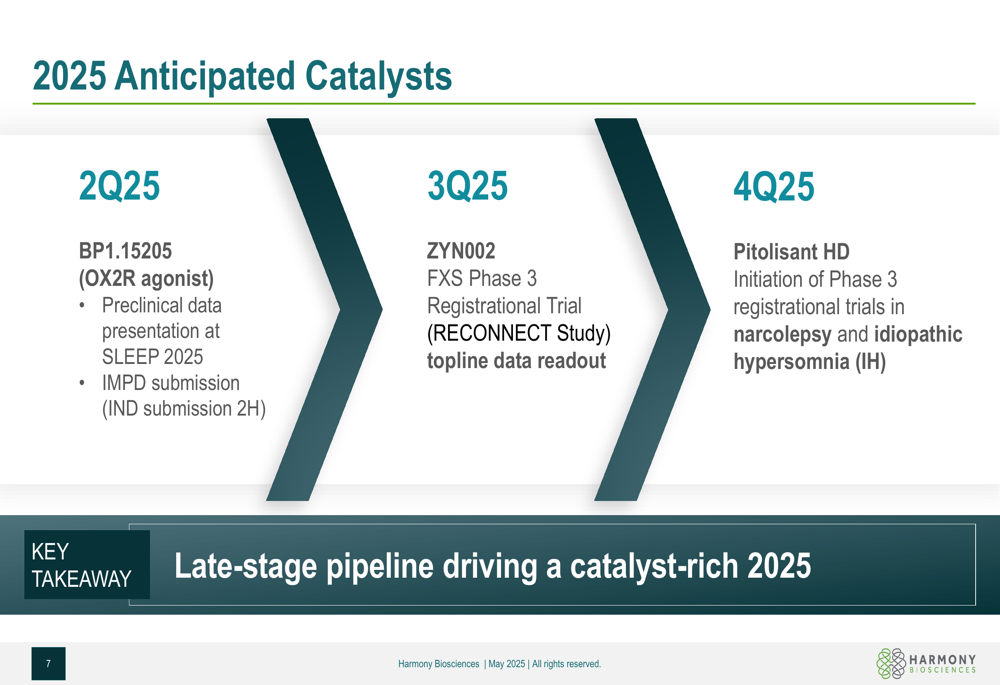

The company highlighted several key catalysts expected throughout 2025, creating multiple potential value-driving events across the year:

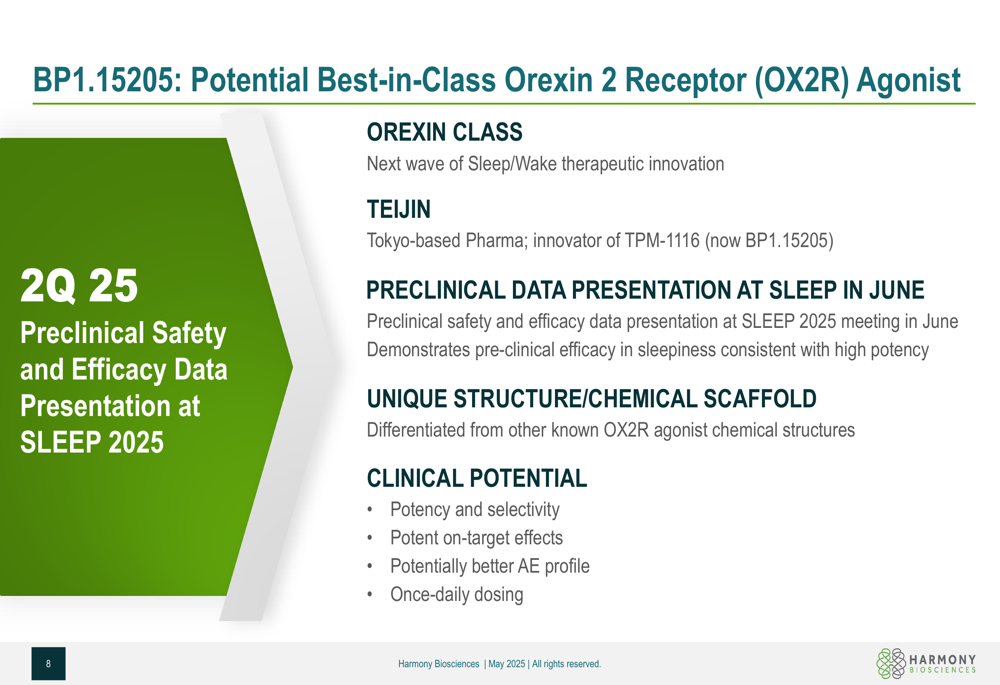

Among the most anticipated developments is the advancement of BP1.15205, described as a potential best-in-class Orexin 2 Receptor (OX2R) agonist. Preclinical data for this compound will be presented at the SLEEP 2025 conference in June.

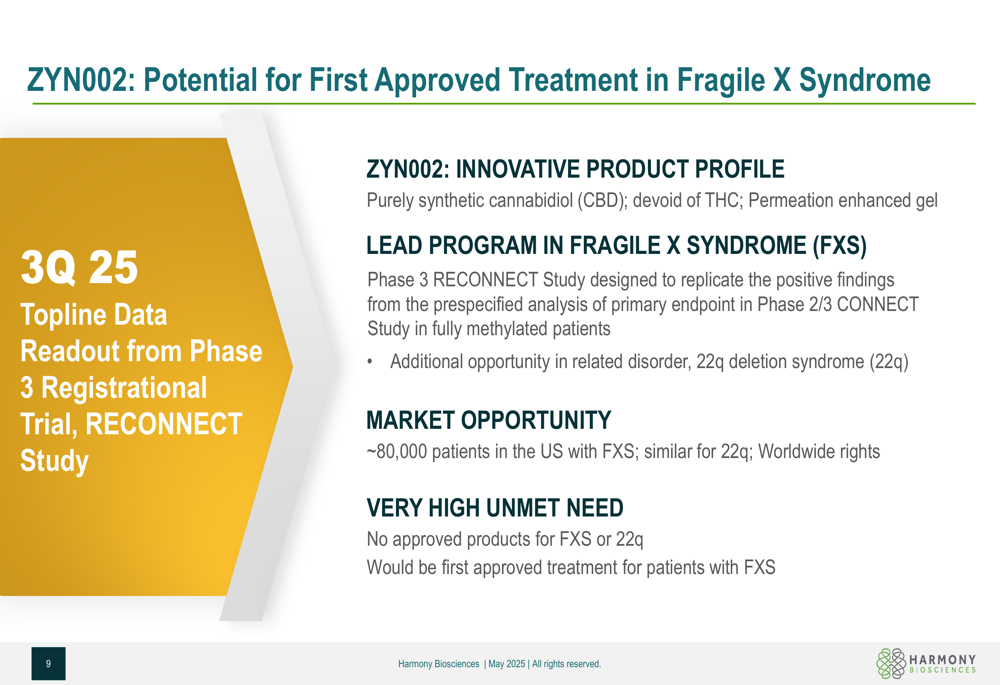

Another significant near-term catalyst is the topline data readout from ZYN002’s Phase 3 RECONNECT trial in Fragile X Syndrome, expected in Q3 2025. If successful, this would position Harmony to potentially deliver the first approved treatment for this condition.

Financial Analysis

Harmony’s financial results demonstrate both strong revenue growth and profitability, with non-GAAP adjusted net income reaching $60.4 million in Q1 2025, a 19% increase from $50.7 million in Q1 2024.

The company’s financial highlights showcase its solid performance metrics:

The detailed financial summary reveals increased investments in research and development, with R&D expenses rising 56% year-over-year to $34.5 million, reflecting the company’s commitment to advancing its pipeline. Sales and marketing expenses increased 13% to $30.7 million, while G&A expenses rose 22% to $31.2 million.

Notably, Harmony maintains a strong balance sheet with $610.2 million in cash, cash equivalents, and investments. This represents an increase from the $576.1 million reported at the end of Q4 2024, demonstrating continued cash generation despite increased investments in pipeline development.

Strategic Outlook

Harmony Biosciences reiterated its 2025 full-year revenue guidance of $820-$860 million, consistent with the outlook provided in its Q4 2024 earnings report. The company emphasized its unique profile as a profitable biotech with over four years of profitability and self-funding capabilities.

Management highlighted the strategic importance of the late-stage pipeline in driving future growth, with potential new product launches and label expansions creating multiple opportunities beyond the current WAKIX franchise. The company’s focus on U.S.-centric operations allows for efficient commercialization without the complexities of global market entry.

For Pitolisant HD, Harmony plans to initiate Phase 3 registrational trials in narcolepsy and idiopathic hypersomnia in Q4 2025, with topline data anticipated in 2027 and potential FDA approval targeted for 2028. The company has filed utility patents that could extend the pitolisant franchise into the 2040s, providing long-term market protection.

Overall, Harmony Biosciences appears well-positioned to leverage its commercial success with WAKIX while advancing multiple pipeline candidates that could significantly expand its market presence in neurological disorders with high unmet needs.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.