Figma Shares Indicated To Open $105/$110

Introduction & Market Context

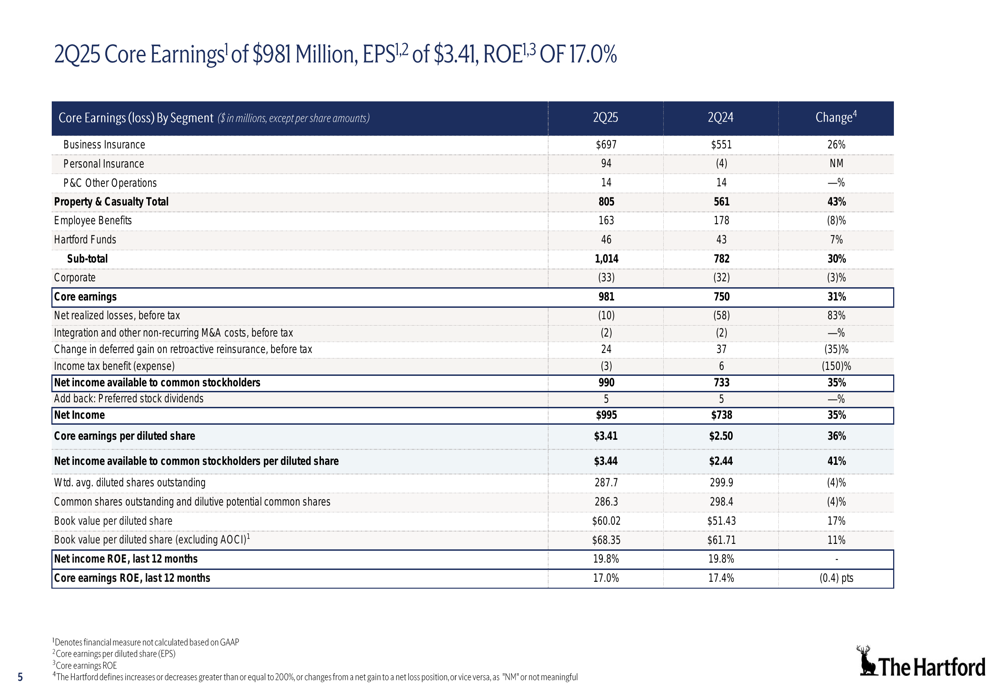

Hartford Financial Services Group (NYSE:HIG) released its second quarter 2025 financial results on July 28, 2025, showcasing significant improvement across key metrics. The presentation revealed a 31% year-over-year increase in core earnings to $981 million, with core earnings per diluted share rising 36% to $3.41.

The results mark a substantial recovery from the company’s Q1 2025 performance, when Hartford reported earnings per share of $2.20, slightly missing analyst expectations of $2.23. The stock, which experienced a 1.71% decline during the regular trading session, showed signs of recovery with a 0.2% increase in after-hours trading following the earnings release.

Quarterly Performance Highlights

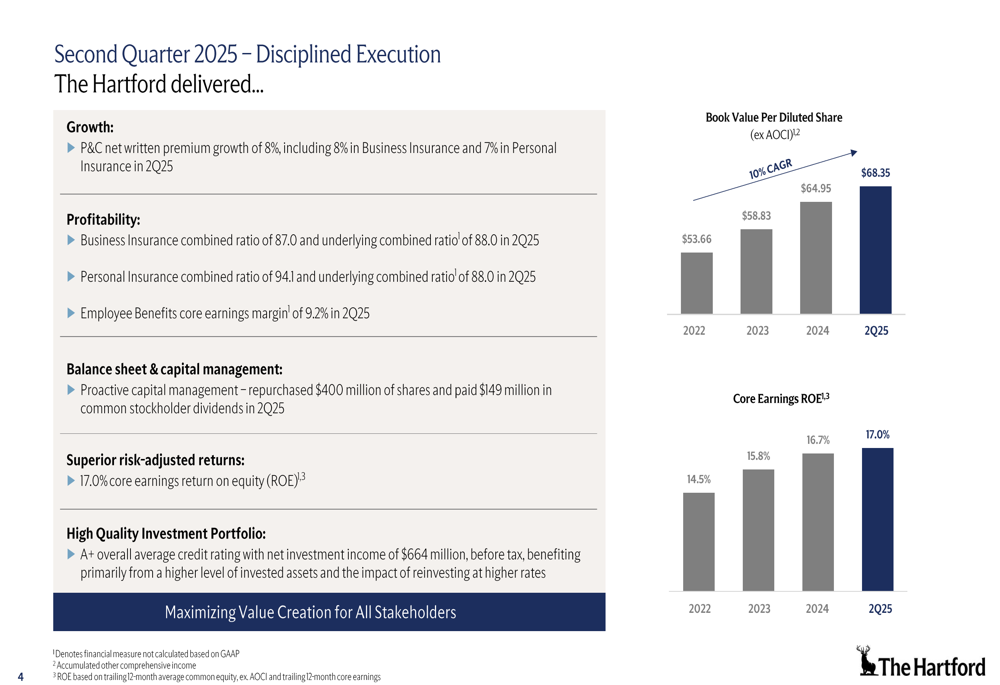

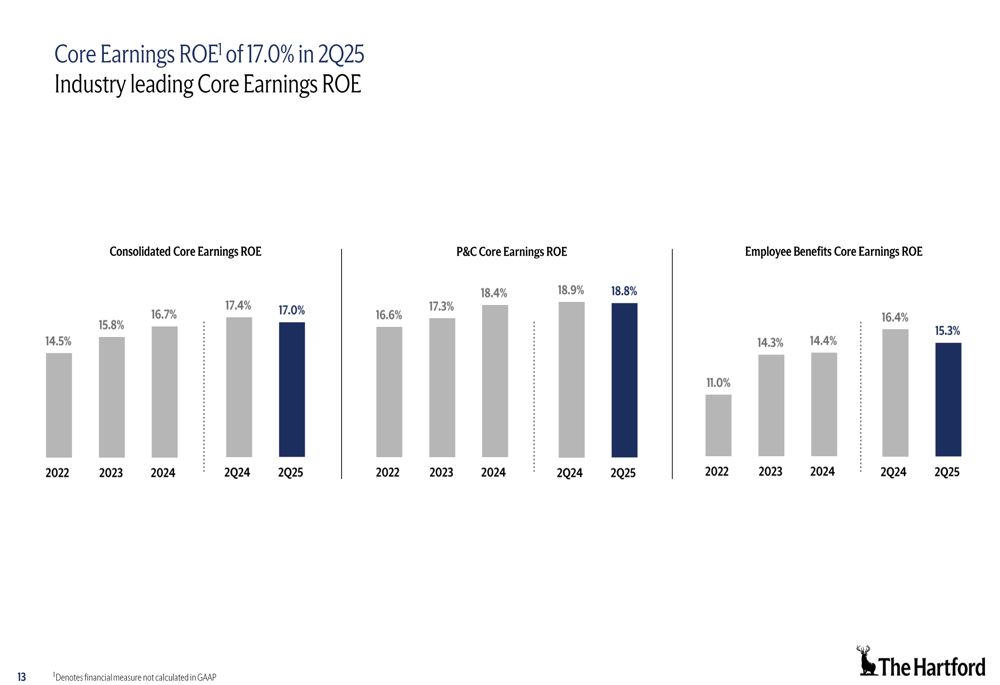

Hartford’s Q2 2025 results demonstrated strong execution across its diversified business segments, with Property & Casualty (P&C) written premiums growing 8% year-over-year to $4.8 billion. The company achieved an impressive core earnings return on equity (ROE) of 17.0%, maintaining its upward trajectory from 14.5% in 2022.

As shown in the following comprehensive performance summary:

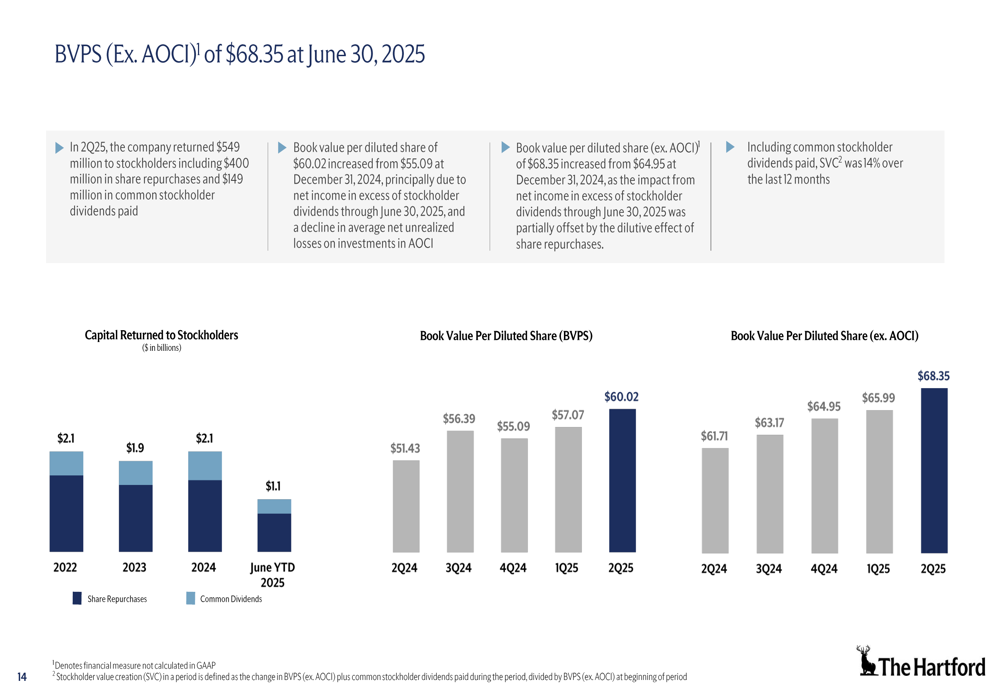

The company’s book value per diluted share (excluding AOCI) reached $68.35, continuing its steady growth from $53.66 in 2022. Combined ratios improved significantly across segments, with the overall P&C combined ratio decreasing by 5.0 points to 88.6.

A detailed breakdown of core earnings by segment reveals the substantial year-over-year improvement:

Segment Analysis

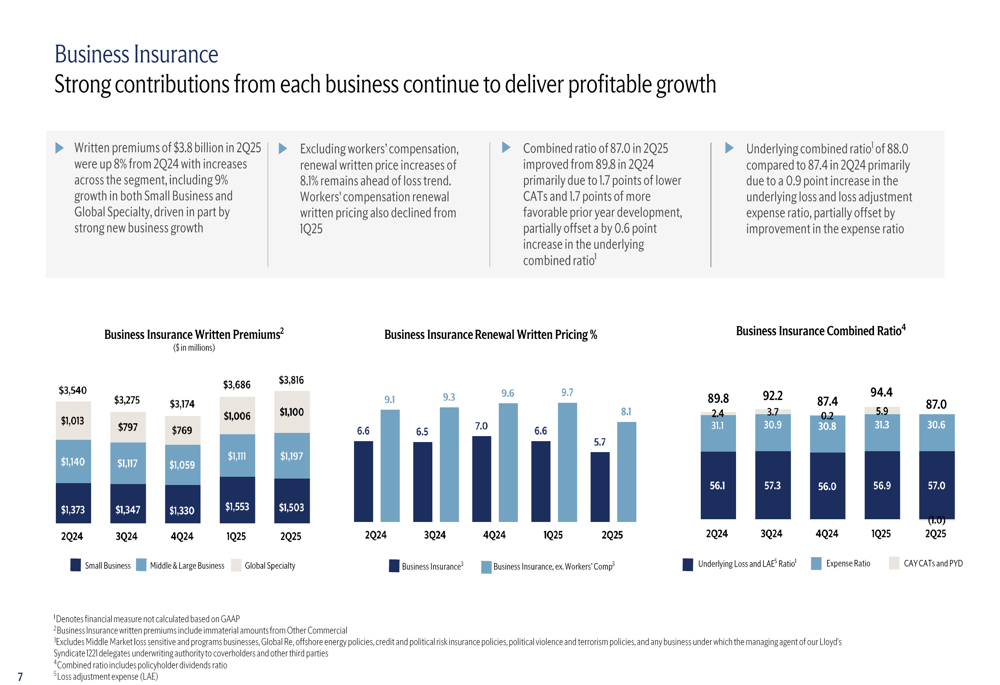

Business Insurance, Hartford’s largest segment representing 55% of revenue, delivered particularly strong results with core earnings of $697 million, a 26% increase from Q2 2024. Written premiums grew 8% to $3.8 billion, while the combined ratio improved by 2.8 points to 87.0.

The following chart illustrates Business Insurance performance metrics:

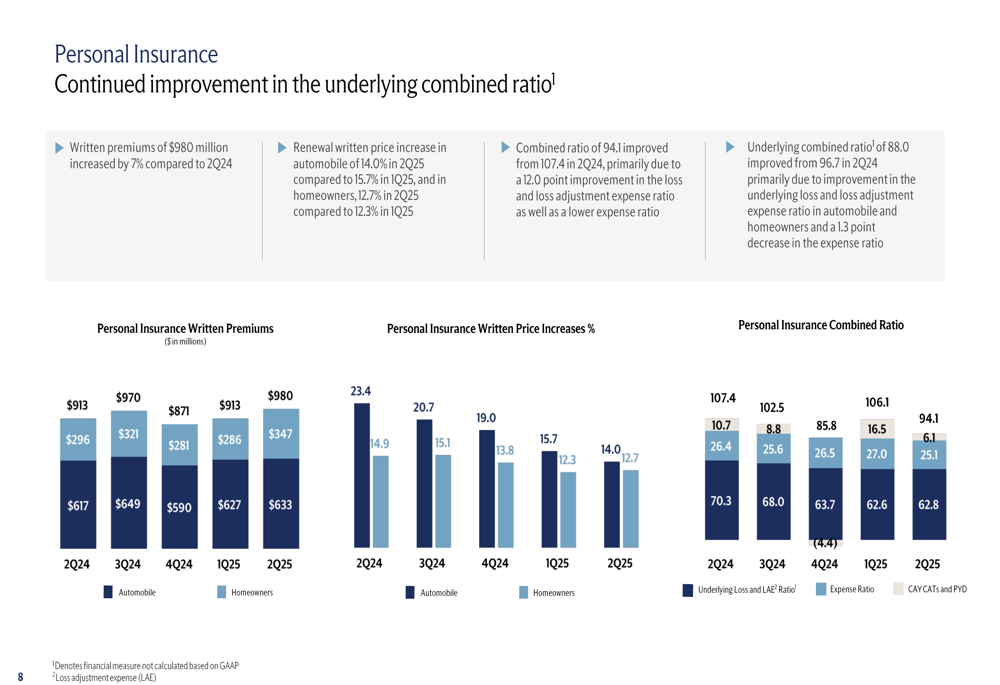

Personal Insurance showed the most dramatic improvement among all segments, with a combined ratio of 94.1, representing a 13.3 point improvement from Q2 2024. This marks a significant turnaround from Q1 2025, when the segment reported just $6 million in earnings due to catastrophe losses, including $325 million from California wildfires.

The Personal Insurance recovery is detailed in this segment breakdown:

Employee Benefits maintained strong performance with a core earnings margin of 9.2%, exceeding the company’s long-term target despite an 8% year-over-year decline in core earnings to $163 million. Fully insured ongoing premiums remained flat compared to Q2 2024.

Investment Portfolio Performance

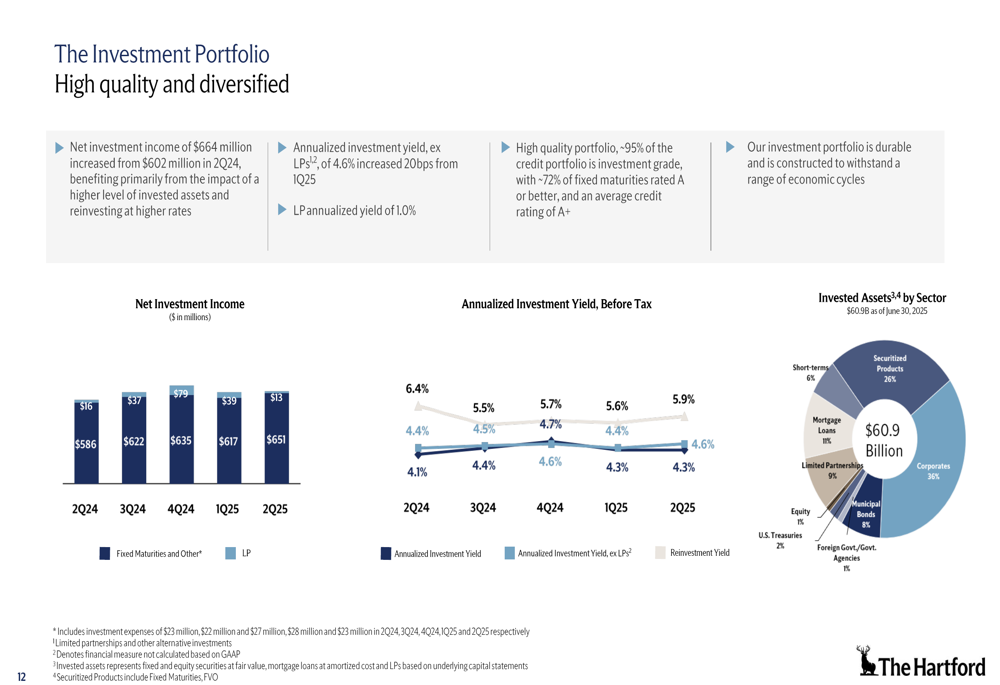

Hartford’s investment portfolio continues to demonstrate high quality and diversification, with net investment income increasing to $664 million from $602 million in Q2 2024. The annualized investment yield, excluding limited partnerships, rose to 4.6%, a 20 basis point increase from Q1 2025.

The portfolio maintains an A+ average credit rating, with approximately 95% of the credit portfolio rated as investment grade and roughly 72% of fixed maturities rated A or better, as illustrated in the following chart:

Capital Management & Shareholder Returns

Hartford maintained its commitment to returning capital to shareholders, distributing $549 million in Q2 2025 through $400 million in share repurchases and $149 million in common stockholder dividends. This approach has contributed to the steady growth in book value per diluted share.

The following chart details Hartford’s capital return strategy and book value performance:

The company’s disciplined capital management has supported its industry-leading core earnings ROE of 17.0%, as demonstrated in this comparative analysis:

Forward-Looking Statements

Hartford enters the second half of 2025 with strong momentum across its diversified business segments. The company’s focus on disciplined underwriting and pricing is evident in the renewal written price increases: 8.1% in Business Insurance (excluding workers’ compensation), 14.0% in automobile, and 12.7% in homeowners.

The significant improvement in Personal Insurance suggests that Hartford is successfully addressing the challenges faced in Q1 2025. With a high-quality investment portfolio and consistent capital return strategy, the company appears well-positioned to maintain its strong performance through the remainder of 2025.

Investors should note that while Hartford’s presentation highlights numerous positive developments, the company continues to operate in a dynamic insurance market with ongoing challenges including climate-related catastrophe risks, competitive pricing pressures in workers’ compensation, and broader economic uncertainties that could impact future results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.