Trump meets Zelenskiy, says Putin wants war to end, mulls trilateral talks

Introduction & Market Context

Harvard Bioscience (NASDAQ:HBIO) released its Q1 2025 earnings presentation on May 12, 2025, revealing continued challenges across its business segments amid persistent headwinds in academic research funding. The company’s stock has faced significant pressure, trading at $0.333 in after-hours trading, up 5.71% following the earnings release but still near its 52-week low of $0.29, reflecting ongoing investor concerns about the company’s performance trajectory.

The life sciences equipment provider continues to navigate a difficult market environment, with uncertainty surrounding National Institutes of Health (NIH) funding and China tariff situations impacting its customer base. These challenges have prompted the company to emphasize cost management while focusing on new product commercialization opportunities.

Quarterly Performance Highlights

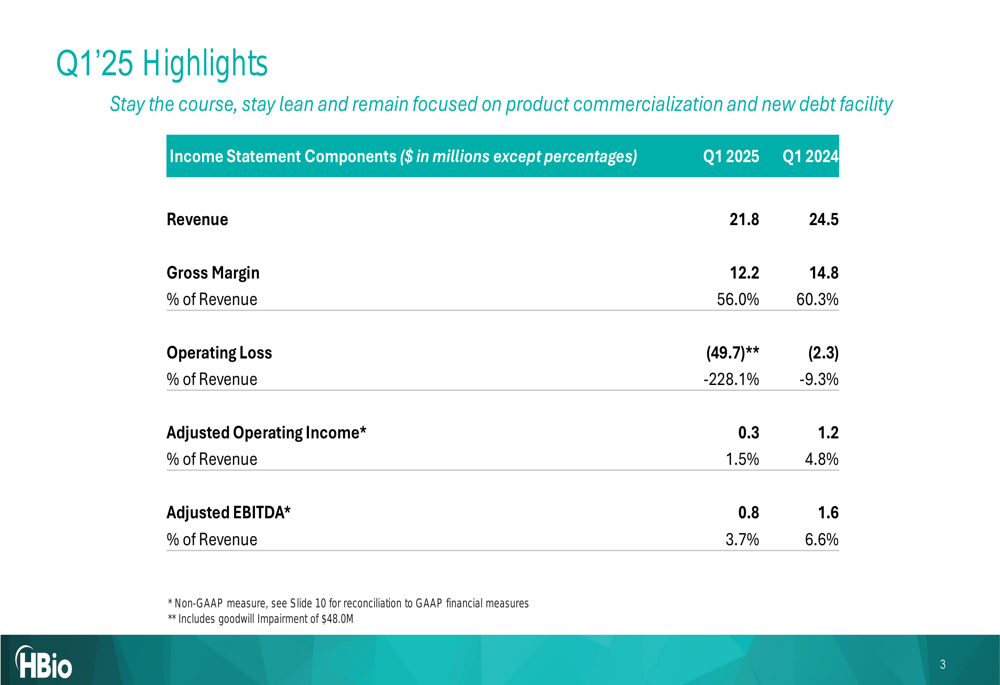

Harvard Bioscience reported Q1 2025 revenue of $21.8 million, representing a decline from $24.5 million in the same period last year. The company’s gross margin also contracted to 56.0% from 60.3% in Q1 2024, resulting in gross margin dollars of $12.2 million compared to $14.8 million in the prior-year period.

As shown in the following financial highlights table from the presentation:

The most significant impact on the company’s results came from a $48.0 million goodwill impairment charge, which drove operating loss to $49.7 million, compared to a $2.3 million loss in Q1 2024. On an adjusted basis, which excludes the impairment and other non-recurring items, operating income was $0.3 million, down from $1.2 million in the prior year.

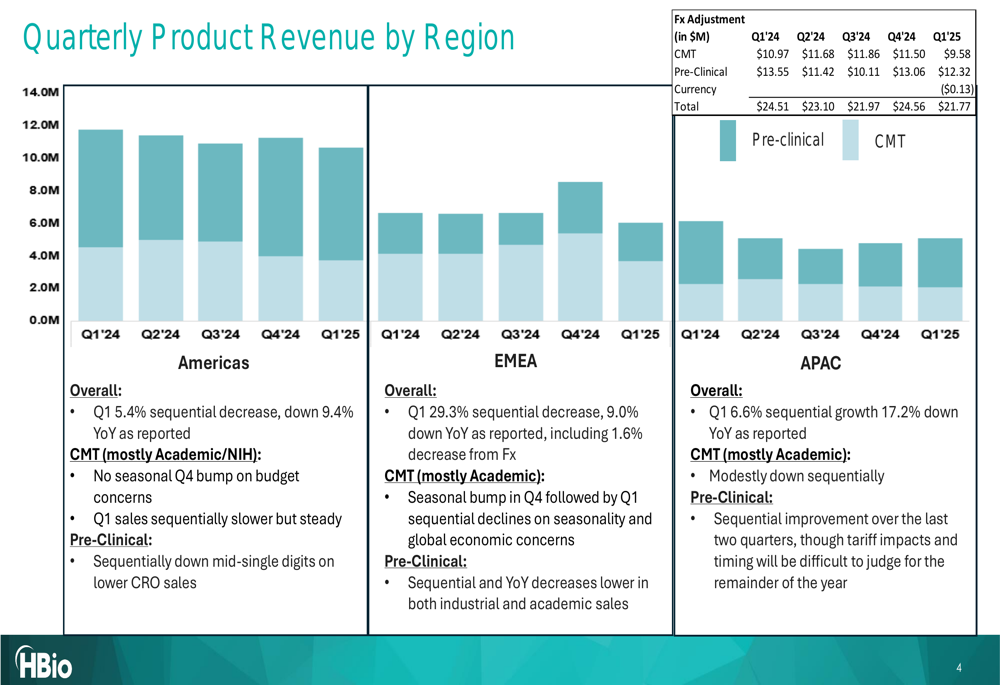

Regional performance showed weakness across most markets. The Americas region experienced a 9.4% year-over-year decline, while EMEA (Europe, Middle East, and Africa) saw a 9.0% decrease, with currency effects accounting for 1.6% of that decline. The APAC (Asia-Pacific) region posted the steepest drop at 17.2% year-over-year.

The following regional breakdown illustrates these trends:

Detailed Financial Analysis

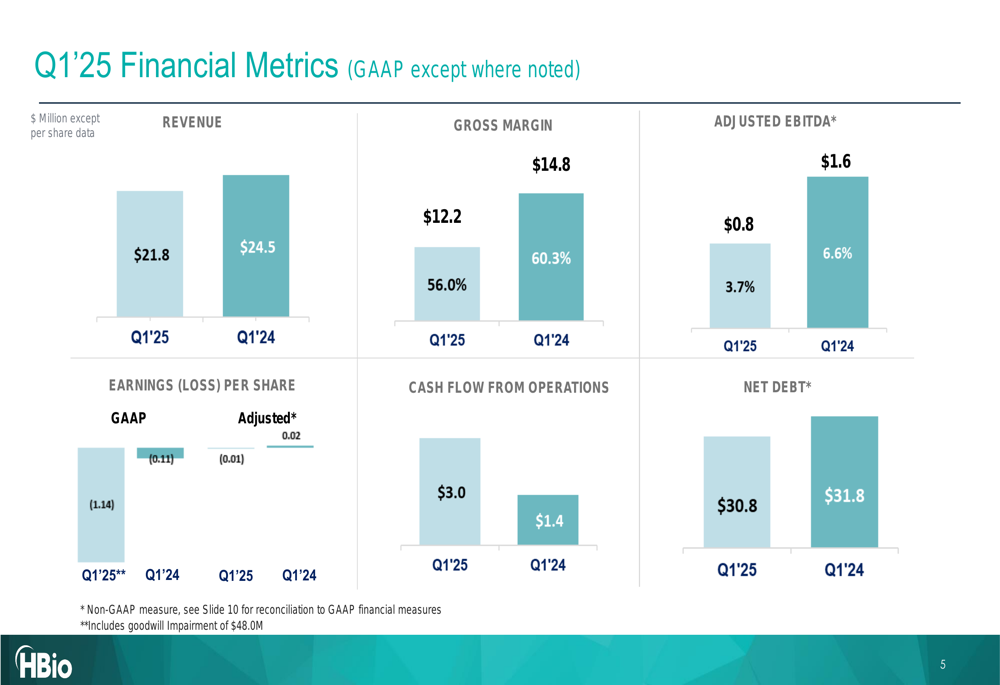

Despite the revenue challenges, Harvard Bioscience demonstrated some positive financial metrics. Cash flow from operations improved to $3.0 million in Q1 2025, up from $1.4 million in Q1 2024, suggesting effective working capital management. The company also reduced its net debt position slightly to $30.8 million from $31.8 million a year earlier.

The comprehensive financial metrics comparison is illustrated below:

Adjusted EBITDA, a key measure of operational performance, declined to $0.8 million (3.7% of revenue) in Q1 2025 from $1.6 million (6.6% of revenue) in Q1 2024. The company’s GAAP earnings per share was significantly impacted by the goodwill impairment, resulting in a loss of $1.14 per share compared to a loss of $0.11 per share in the prior-year period. On an adjusted basis, the loss was $0.01 per share, down from earnings of $0.02 per share in Q1 2024.

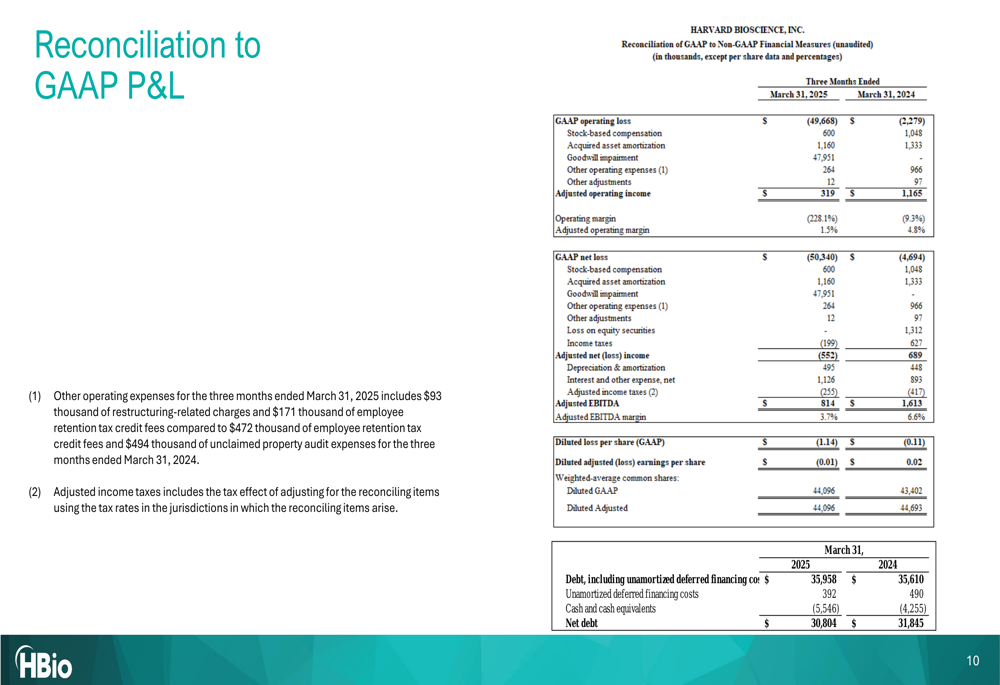

The reconciliation between GAAP and non-GAAP measures provides additional context for understanding the company’s underlying performance:

Strategic Initiatives

Harvard Bioscience is pursuing several strategic initiatives to address its current challenges and position for future growth. The company’s presentation emphasized a commitment to "stay the course, stay lean and remain focused on product commercialization and new debt facility."

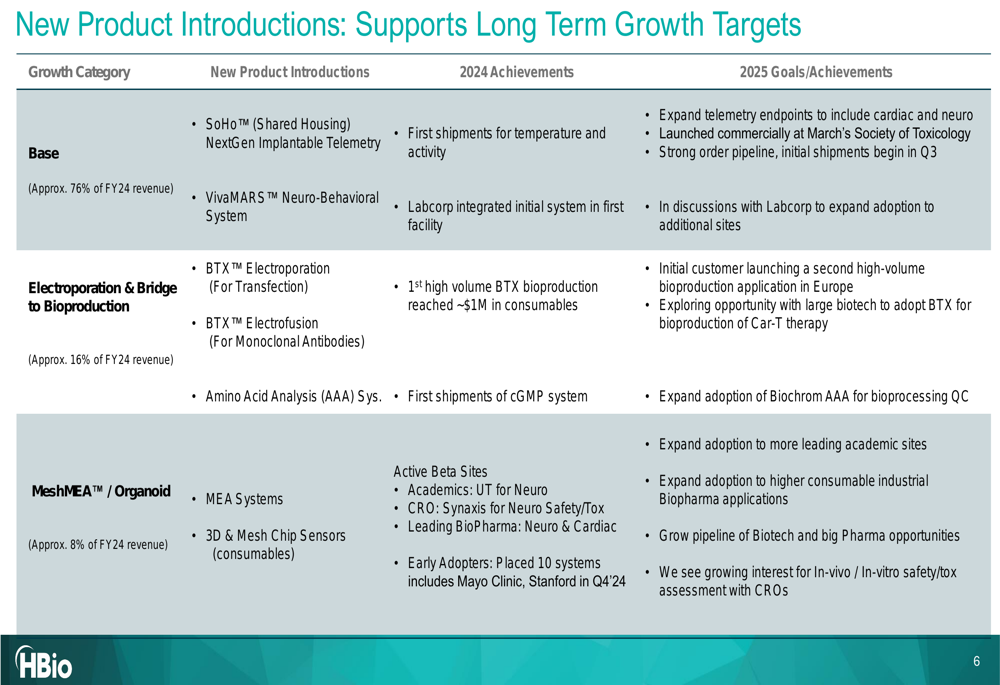

The company has outlined its product development strategy across three growth categories that represented different portions of its fiscal year 2024 revenue: Base (76%), Electroporation & Bridge to Bioproduction (16%), and MeshMEAT™/Organoid (8%). Each category has specific new product introductions and goals for 2025.

The following slide details these product initiatives:

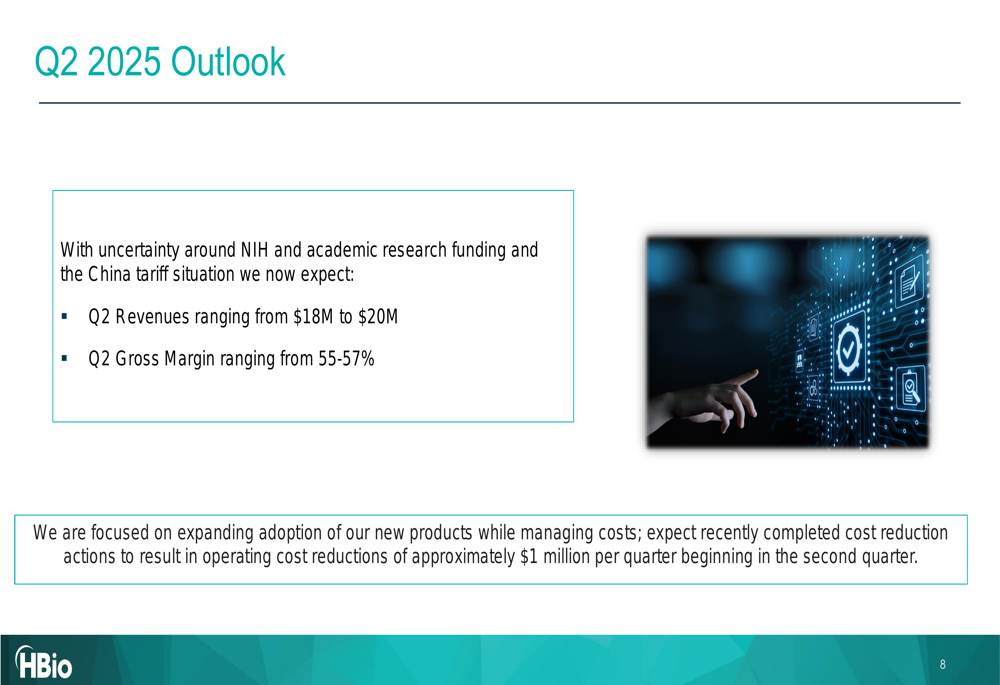

Management has also implemented cost reduction actions expected to deliver approximately $1 million in quarterly operating cost savings beginning in Q2 2025. These measures align with CEO Jim Green’s previous comments about managing the cost structure to maintain profitability regardless of revenue levels.

Forward-Looking Statements

Looking ahead to Q2 2025, Harvard Bioscience provided revenue guidance of $18-20 million, which represents a sequential decline from Q1 2025 and reflects continued caution about market conditions. The company expects gross margins to range between 55-57%, consistent with Q1 2025 levels.

The Q2 outlook is summarized in the following slide:

The company continues to focus on expanding adoption of its new products while managing costs carefully. The guidance takes into account ongoing uncertainty surrounding NIH and academic research funding, as well as the potential impact of China tariff situations.

Harvard Bioscience also noted its focus on a new debt facility, which according to previous earnings information, is expected to carry interest rates between 10-12%. This refinancing is planned to be completed by June 2025 and will be a critical factor in the company’s financial flexibility going forward.

While facing significant headwinds, the company’s strategic focus on new product opportunities in areas like CAR T therapy and organoid research represents potential growth drivers that could help offset challenges in its traditional academic and research markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.