Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

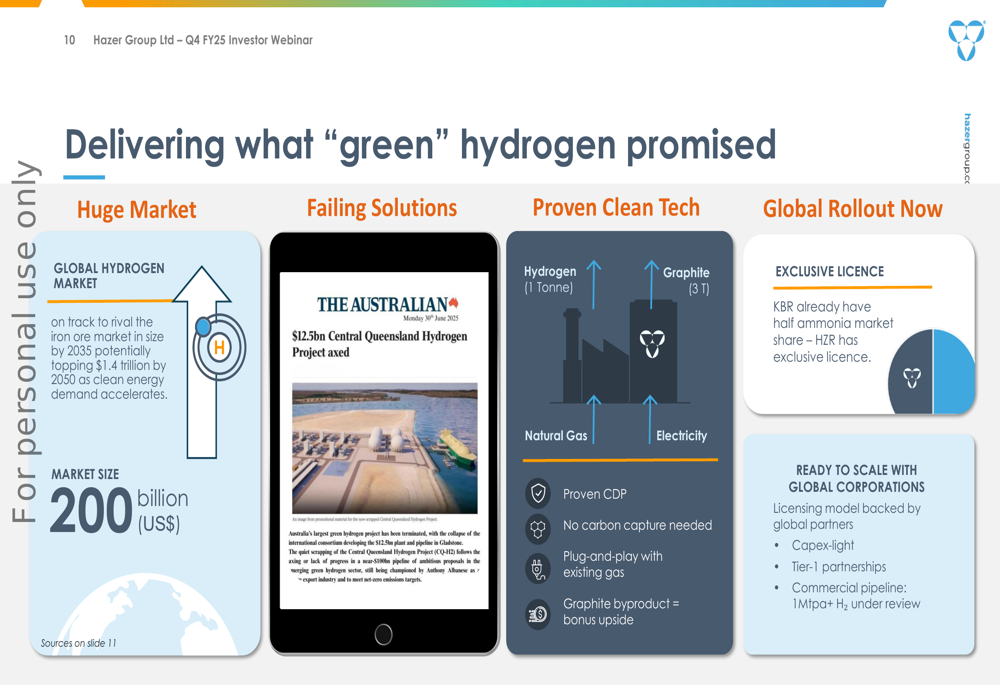

Hazer Group Ltd (ASX:HZR) presented its Q4 FY25 Investor Webinar on July 24, 2025, highlighting strategic partnerships and commercialization efforts in the clean hydrogen space. The company positions itself at the forefront of the global hydrogen market, which currently stands at 97 million tonnes per annum (MTPA) with a market size of US$200 billion, and is projected to grow significantly in coming decades.

The presentation comes as Hazer’s stock has experienced volatility, with the share price closing at A$0.36 on July 23, 2025, down 5.26% for the day but showing a 14.29% return over the previous week according to recent market data.

As shown in the following slide, Hazer’s technology aims to disrupt the traditional hydrogen production market by offering a cleaner alternative to Steam Methane Reforming (SMR), which currently accounts for approximately 95% of global hydrogen production:

Strategic Initiatives

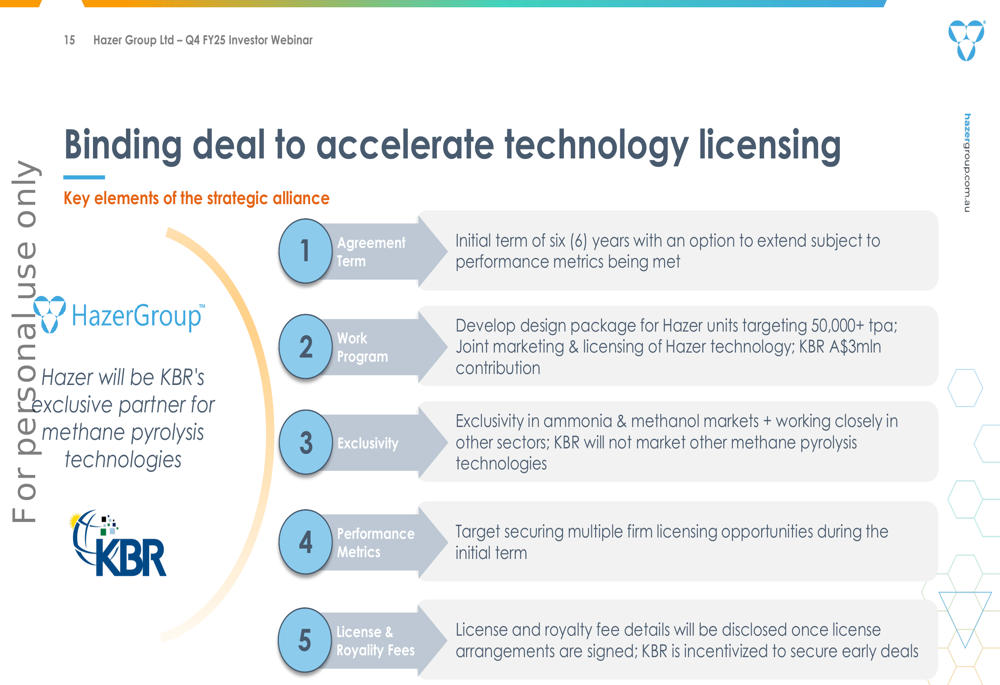

The cornerstone of Hazer’s Q4 update was its global partnership with KBR (NYSE:KBR), a major engineering firm with significant market share in ammonia production. This binding deal, structured as a six-year agreement with extension options, aims to accelerate technology licensing and commercialization.

The partnership includes developing design packages for Hazer units targeting 50,000+ tonnes per annum (tpa) capacity, joint marketing efforts, and a A$3 million contribution from KBR. The agreement grants KBR exclusivity in ammonia and methanol markets while preventing them from marketing competing methane pyrolysis technologies.

The strategic alliance is illustrated in the following slide:

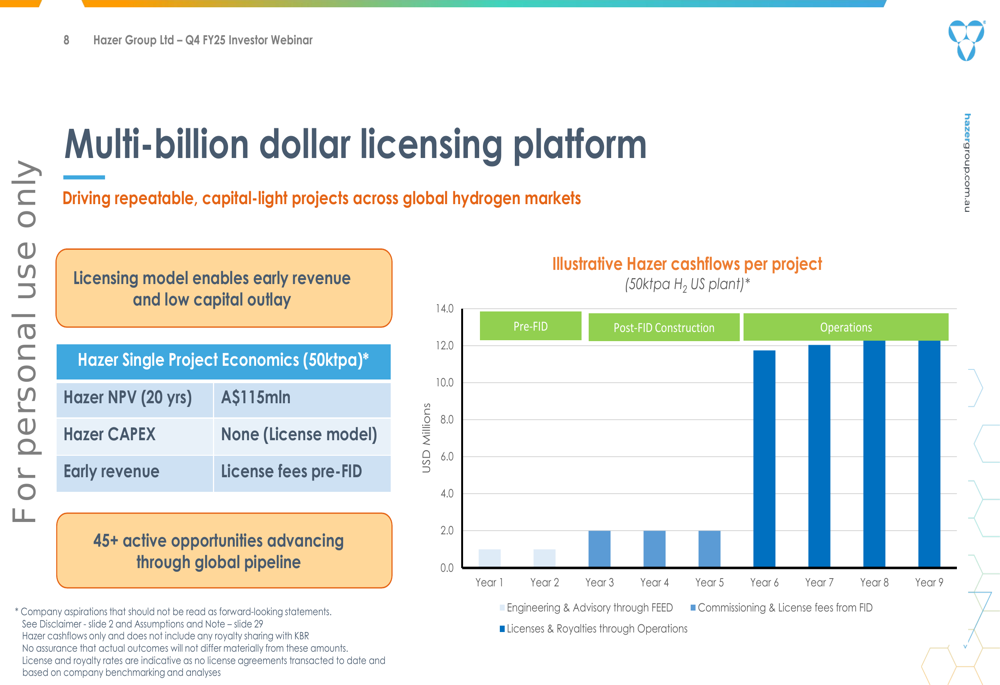

Hazer is implementing a capital-light licensing model rather than building and operating plants directly. This approach enables early revenue through license fees and ongoing royalties with minimal capital expenditure. According to the company’s projections, a single 50,000 tpa hydrogen project could generate an NPV of A$115 million over 20 years.

The company’s licensing economics are detailed in this slide:

Quarterly Performance Highlights

During Q4 FY25, Hazer strengthened its financial position with a A$10.7 million capital raise, bringing its total funding position to over A$16 million. This aligns with the company’s Q1 2025 earnings report, which showed a cash position of A$10.3 million and liquidity of A$12.5 million with no debt.

The quarter also saw progress in intellectual property protection with two new patents secured in Southeast Asia, adding to patents previously obtained in Japan and the US. The company completed its Commercial Demonstration Plant (CDP) test program, which has proven the technology’s readiness for commercial deployment.

Key highlights from the quarter are summarized in the following slide:

Competitive Industry Position

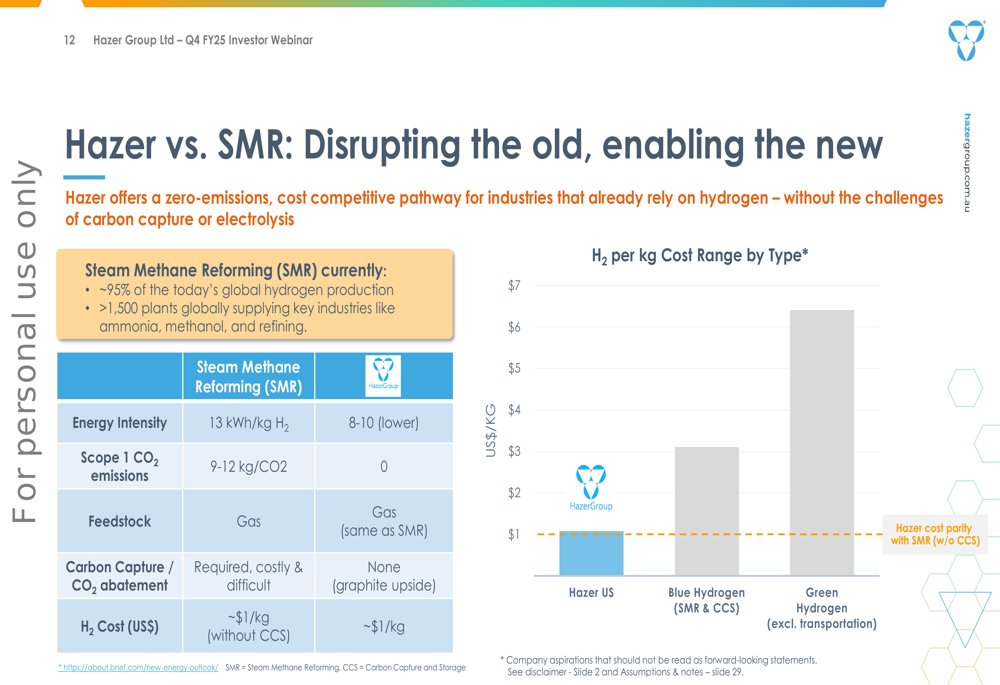

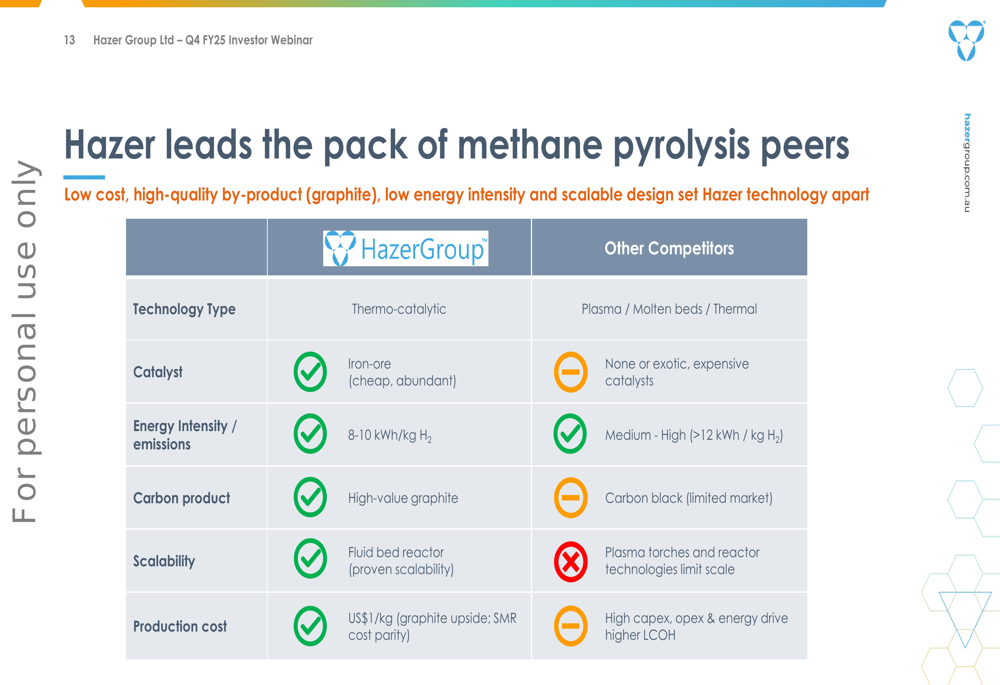

Hazer’s methane pyrolysis technology offers several advantages over traditional hydrogen production methods. Compared to Steam Methane Reforming (SMR), Hazer claims lower energy intensity (8-10 kWh/kg H₂ vs. 13 kWh/kg H₂), zero Scope 1 CO₂ emissions (vs. 9-12 kg CO₂), and cost parity at approximately US$1/kg without requiring carbon capture.

The company also positions itself ahead of other methane pyrolysis competitors by using iron-ore catalyst (described as cheap and abundant), producing high-value graphite rather than carbon black, and employing fluid bed reactor technology with proven scalability.

This competitive positioning is detailed in the following comparison:

Hazer also claims leadership among methane pyrolysis peers:

Forward-Looking Statements

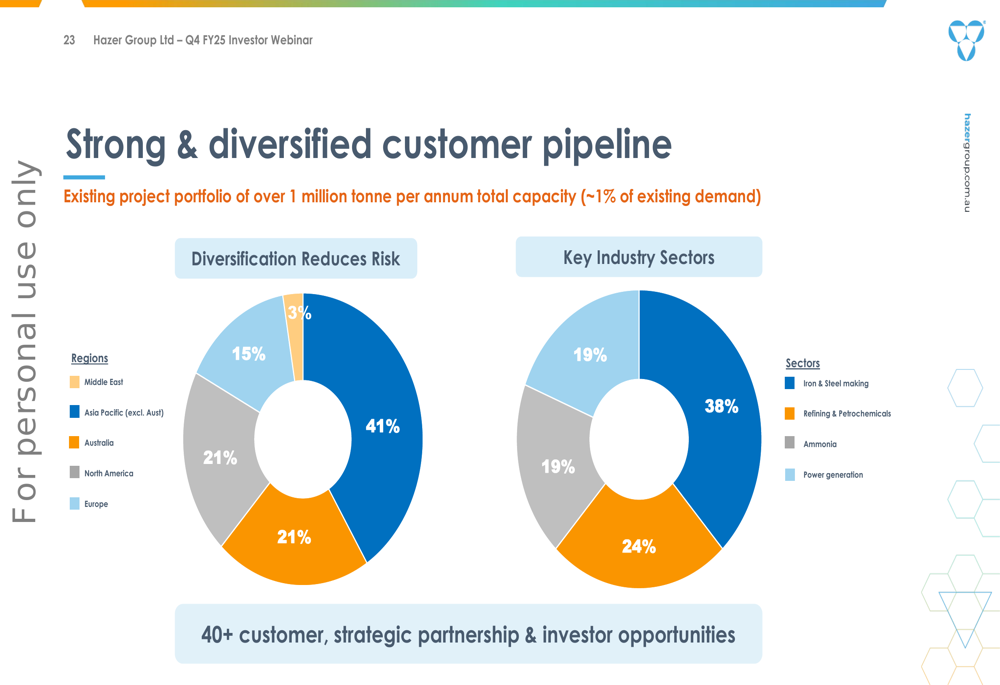

Hazer’s sales pipeline spans multiple regions and sectors, with 45+ active global leads representing potential hydrogen capacity of 1.2 MTPA, or approximately 1% of the current global market. The pipeline includes engagements with oil and gas majors, petrochemical companies, ammonia producers, sustainable aviation fuel manufacturers, and steelmakers.

The company’s customer diversification is illustrated in the following slide:

A significant additional value stream comes from Hazer’s graphite byproduct. The company produces approximately 3 tonnes of graphite for each tonne of hydrogen, potentially generating A$45 million in annual revenue from a single 50,000 tpa hydrogen project (assuming 150,000 tpa of graphite at A$300/tonne).

This opportunity is particularly relevant given recent market developments:

For 2025, Hazer has outlined six strategic priorities focused on accelerating process scale-up, unlocking graphite value, progressing existing commercial projects, and securing new strategic partnerships. The company aims to target 10 projects over the next decade, focusing on industries such as oil and gas, refining, petrochemicals, and steel.

Investment Perspective

While Hazer presents an optimistic outlook in its investor webinar, analysts note the company is burning through cash reserves as it transitions from technology development to commercialization. With a market capitalization of A$47.49 million and a current ratio of 5.53, the company appears financially stable in the short term, though the pace of commercial adoption will be critical.

The company summarizes its investment case as follows:

The success of Hazer’s strategy hinges on the execution of its KBR partnership, the rate of adoption for its technology in commercial projects, and its ability to monetize graphite byproducts. While the company has made significant progress in proving its technology and establishing strategic partnerships, investors should monitor the timeline for converting the pipeline of opportunities into revenue-generating projects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.