Futures slip, bank earnings ahead, Powell to speak - what’s moving markets

Introduction & Market Context

Helios Technologies (NASDAQ:NYSE:HLIO) presented its first quarter 2025 earnings results on May 7, 2025, revealing a performance that exceeded management’s outlook despite year-over-year revenue declines. The company, which specializes in hydraulics and electronics solutions, continues to navigate challenging market conditions while implementing strategic initiatives to drive future growth.

The presentation comes amid significant stock pressure, with HLIO shares trading at $27.13, near the lower end of its 52-week range of $24.76 to $57.29. This represents a substantial decline from the $44.80 price reported after the company’s Q4 2024 earnings release, indicating ongoing investor concerns despite the better-than-expected quarterly results.

Quarterly Performance Highlights

Helios Technologies reported Q1 2025 net sales of $195 million, down 8% year-over-year but exceeding the high end of the company’s outlook by $5 million. Adjusted EBITDA margin came in at 17.3%, down 90 basis points from the prior year but 30 basis points above the high end of the outlook. Diluted non-GAAP EPS was $0.44, representing a 17% year-over-year decline but surpassing the current consensus by $0.08.

As shown in the following financial highlights chart, the company’s performance was stronger than expected despite the challenging environment:

The company emphasized that this marks the sixth consecutive quarter of meeting or exceeding quarterly outlook and the seventh consecutive quarter of debt reduction, demonstrating consistent execution in a difficult market environment.

Segment Analysis

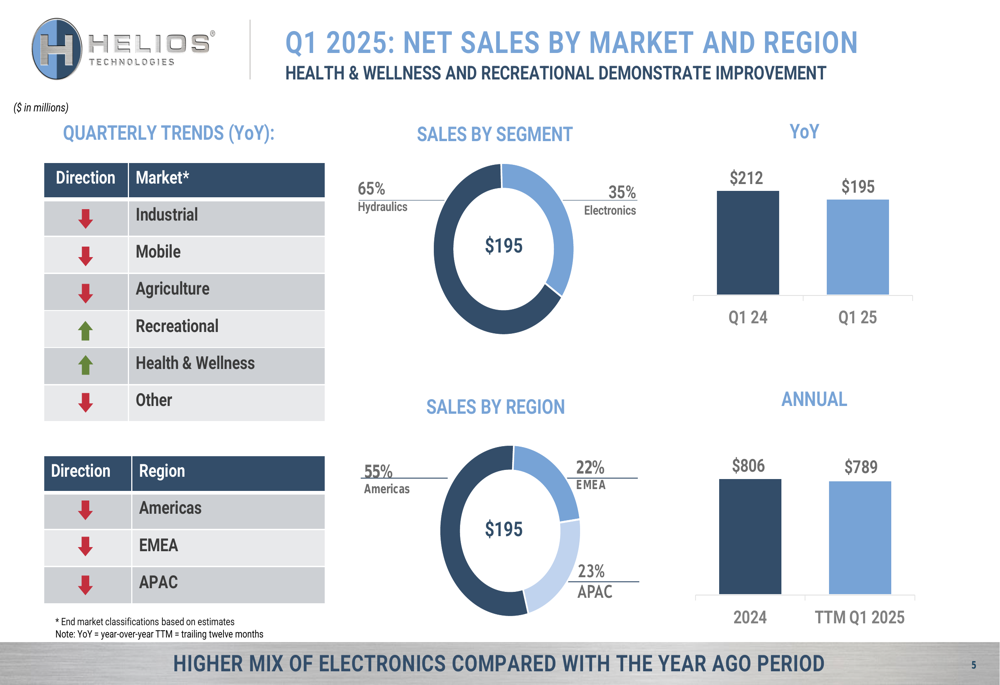

Helios Technologies’ performance revealed a tale of two segments, with Electronics showing resilience while Hydraulics faced more significant headwinds.

The Hydraulics segment, which accounted for 65% of total sales, reported revenue of $126.4 million, down 11% year-over-year. Gross profit declined 16% to $37.4 million, while operating income fell 20% to $17.4 million. The segment’s challenges were primarily driven by weakness in agriculture, mobile, and industrial markets.

In contrast, the Electronics segment, representing 35% of sales, showed modest growth with revenue increasing 1% year-over-year to $69.1 million. More impressively, operating income grew 13% to $8.0 million, demonstrating the segment’s ability to drive profitability improvements despite flat sales. The company noted that growth in Health & Wellness and Recreational markets mostly offset declines in other areas.

The following chart illustrates the company’s sales breakdown by market and region:

Geographically, the Americas accounted for 55% of total sales, while EMEA (Europe, Middle East, and Africa) and APAC (Asia-Pacific) represented 22% and 23%, respectively. The mix of electronics is higher compared to the year-ago period, reflecting the segment’s relative outperformance.

Cash Flow and Balance Sheet Strength

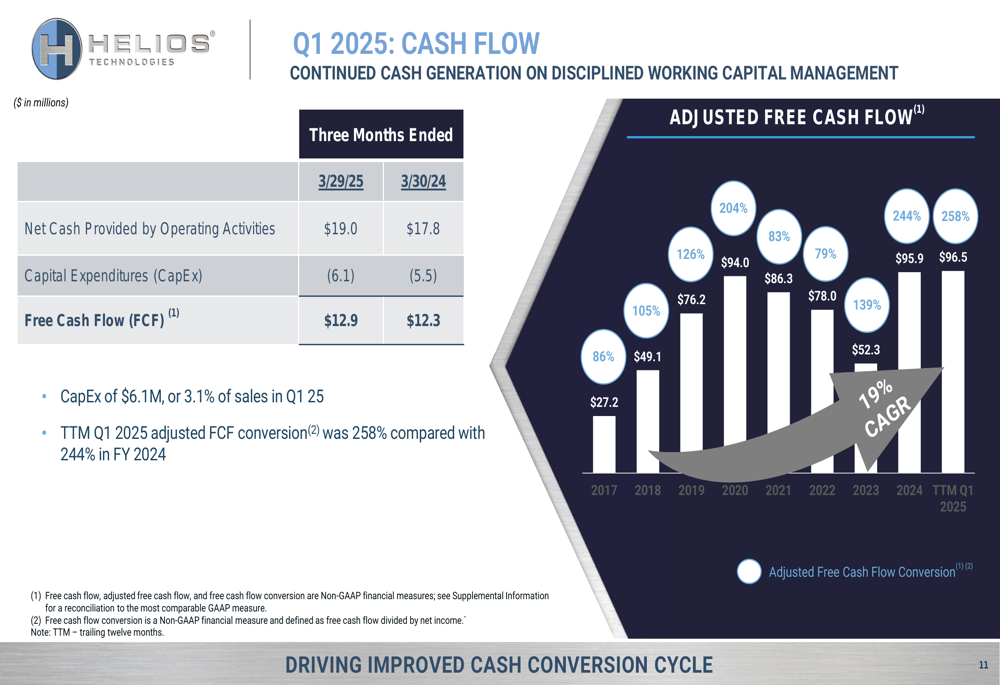

A notable bright spot in Helios Technologies’ Q1 2025 results was its strong cash generation. Net cash provided by operating activities increased to $19.0 million compared to $17.8 million in the prior year. After capital expenditures of $6.1 million, free cash flow reached $12.9 million, up from $12.3 million in Q1 2024.

The company’s trailing twelve months adjusted free cash flow conversion was impressive at 258%, compared with 244% in fiscal year 2024, as illustrated in the following chart:

On the balance sheet front, Helios Technologies reported total debt of $445 million and liquidity of $399 million, including $353 million in undrawn revolver capacity and $46 million in cash. The company’s net debt to adjusted EBITDA ratio stood at 2.7x. Management emphasized its near-term objective to continue using cash to pay down debt while maintaining dividend payments.

Tariff Impact and Mitigation Strategies

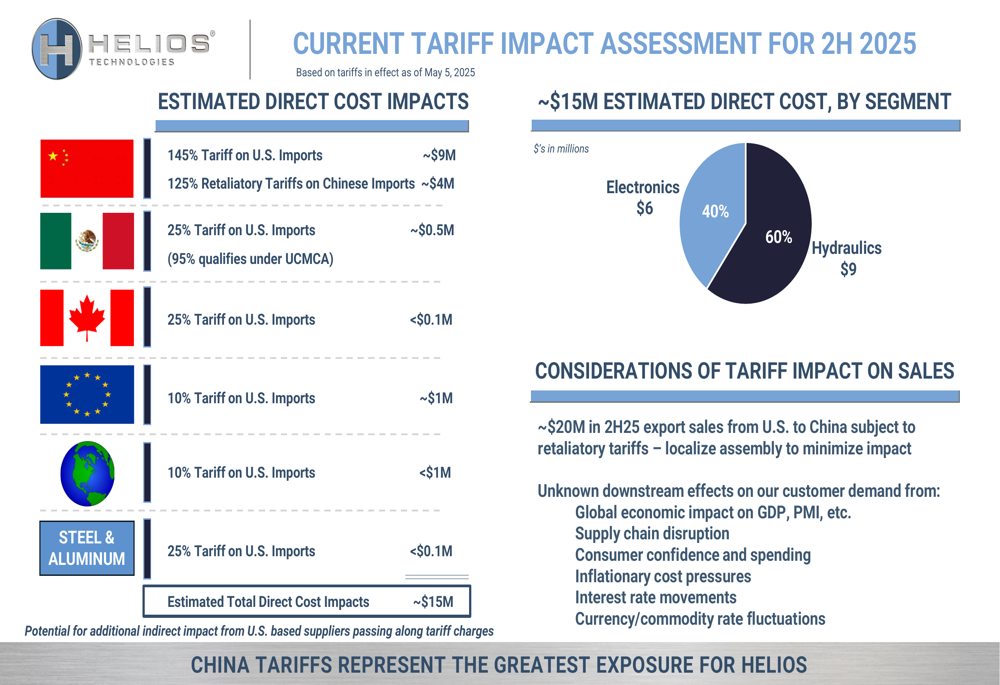

A significant portion of the presentation focused on the potential impact of tariffs in the second half of 2025, which represents a material risk to the company’s performance. Helios Technologies estimates a total direct cost impact of approximately $15 million, primarily from the 145% tariff on U.S. imports ($9 million) and 125% retaliatory tariffs on Chinese imports ($4 million).

The following chart details the company’s assessment of tariff impacts:

To address these challenges, management outlined a comprehensive set of mitigation strategies, including price increases, alternate sourcing, bonded warehouse utilization, local manufacturing, and offensive market strategies. The company emphasized that it is actively exploring and implementing these countermeasures to minimize the tariff exposure.

Forward Outlook and Guidance

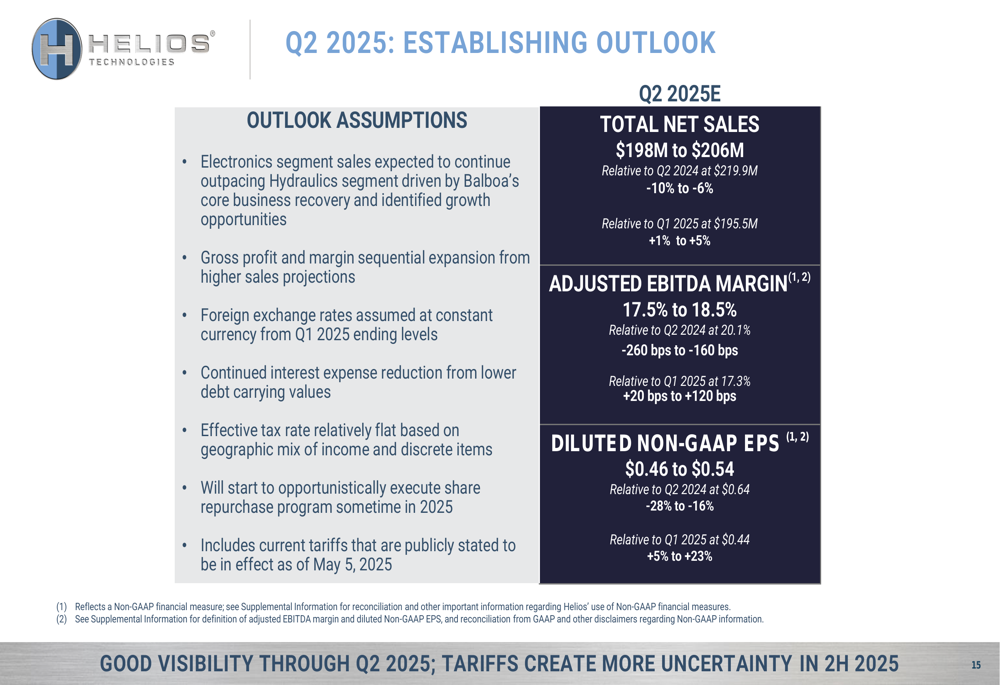

Looking ahead to Q2 2025, Helios Technologies provided an outlook that reflects ongoing market challenges but also demonstrates the company’s resilience. Management projects total net sales of $198 million to $206 million, representing a 10% to 6% decline compared to Q2 2024. Adjusted EBITDA margin is expected to range from 17.5% to 18.5%, down 260 to 160 basis points year-over-year, while diluted non-GAAP EPS is projected at $0.46 to $0.54, a 28% to 16% decline from the prior year.

The detailed Q2 2025 outlook is presented in the following slide:

By segment, the company expects continued challenges across both divisions in Q2 2025:

- Hydraulics: $129 - $134 million (-11% to -8% vs. Q2 2024)

- Electronics: $69 - $72 million (-7% to -3% vs. Q2 2024)

Management noted that while they have good visibility through Q2 2025, the tariff situation creates more uncertainty for the second half of the year. The company also indicated plans to opportunistically execute a share repurchase program sometime in 2025, suggesting confidence in its long-term prospects despite near-term headwinds.

For the full year, Helios Technologies is focusing on five key financial priorities: returning to growth, driving operating leverage, shortening the cash conversion cycle, reducing debt, and leveraging its strong foundation. The company aims to deliver profitable sales growth while improving its overall financial profile.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.