US stock futures dip as Trump’s firing of Cook sparks Fed independence fears

Introduction & Market Context

Helix Energy Solutions Group Inc (NYSE:HLX) presented its first quarter 2025 results on April 24, revealing a return to profitability despite ongoing industry challenges. The offshore energy services provider reported a modest profit of $0.02 per share, exceeding analyst expectations of a $0.0081 loss, though revenue fell short of forecasts.

The company’s stock dropped 3.1% in after-hours trading following the announcement, closing at $6.61, as investors reacted to the revenue miss and reduced full-year outlook. Helix currently trades well below its 52-week high of $13.05, reflecting broader challenges in the energy services sector.

Quarterly Performance Highlights

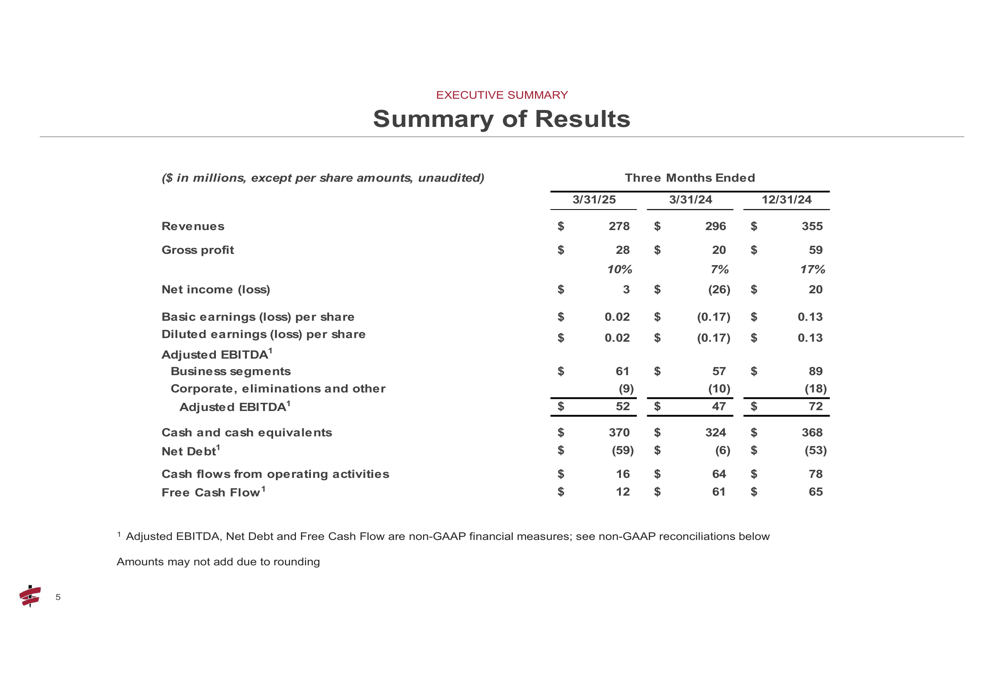

Helix reported Q1 2025 revenue of $278 million, down from $296 million in the same period last year and $355 million in Q4 2024. Despite the revenue decline, the company achieved net income of $3 million, a significant improvement from the $26 million loss recorded in Q1 2024.

As shown in the following financial summary, the company maintained a 10% gross profit margin, up from 7% in the year-ago quarter:

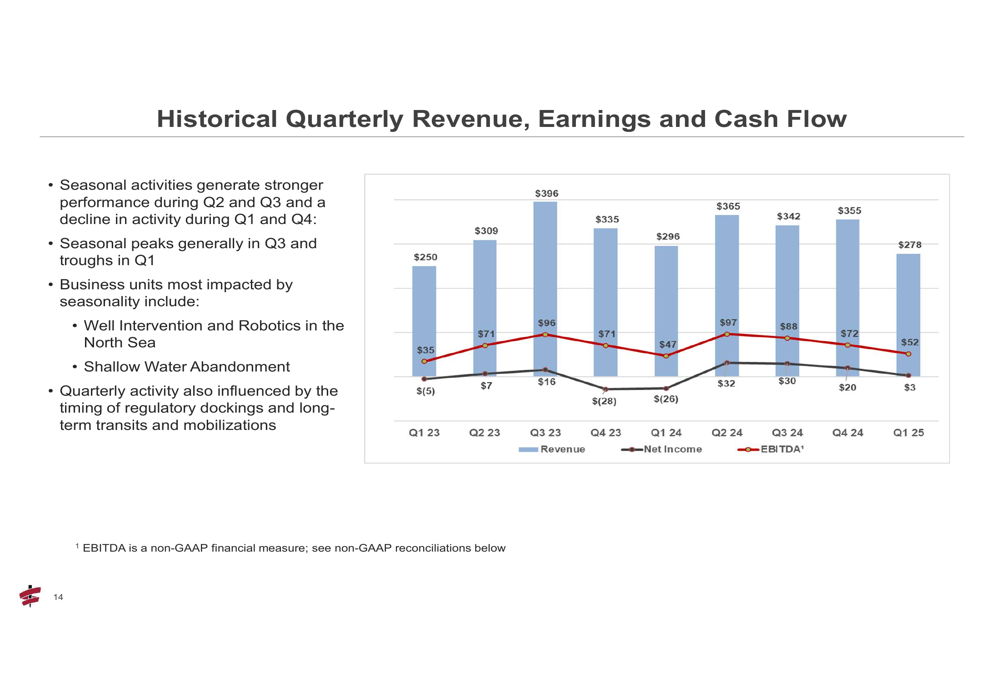

Adjusted EBITDA reached $52 million, representing a 10.6% increase from $47 million in Q1 2024, though down from $72 million in the previous quarter. This sequential decline aligns with the company’s typical seasonal pattern, where Q1 and Q4 generally show lower activity levels compared to mid-year peaks.

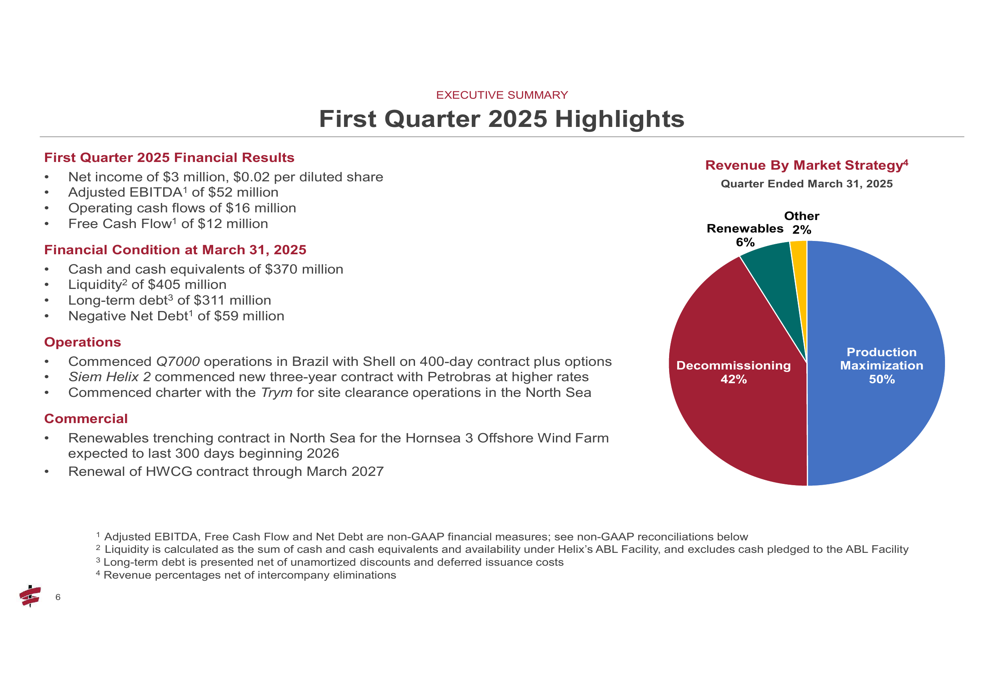

The company’s revenue mix demonstrates its strategic focus areas, with production maximization and decommissioning work accounting for 92% of total revenue:

Detailed Financial Analysis

Segment performance varied significantly across Helix’s business units. Well Intervention, the company’s largest segment, generated $198 million in revenue with a 12% gross profit margin. Robotics delivered $51 million with a 16% margin, while Shallow Water Abandonment struggled with a 69% negative gross margin on $17 million in revenue.

Utilization rates showed mixed results across the fleet. In Well Intervention, Gulf of America vessels maintained high utilization (98%), while North Sea assets operated at just 17% utilization. The Q7000 vessel commenced operations in Brazil in late March under a 400-day contract with Shell, while the Siem Helix 2 began a new contract with Petrobras in January.

The company’s historical quarterly performance illustrates both seasonal patterns and year-over-year improvements:

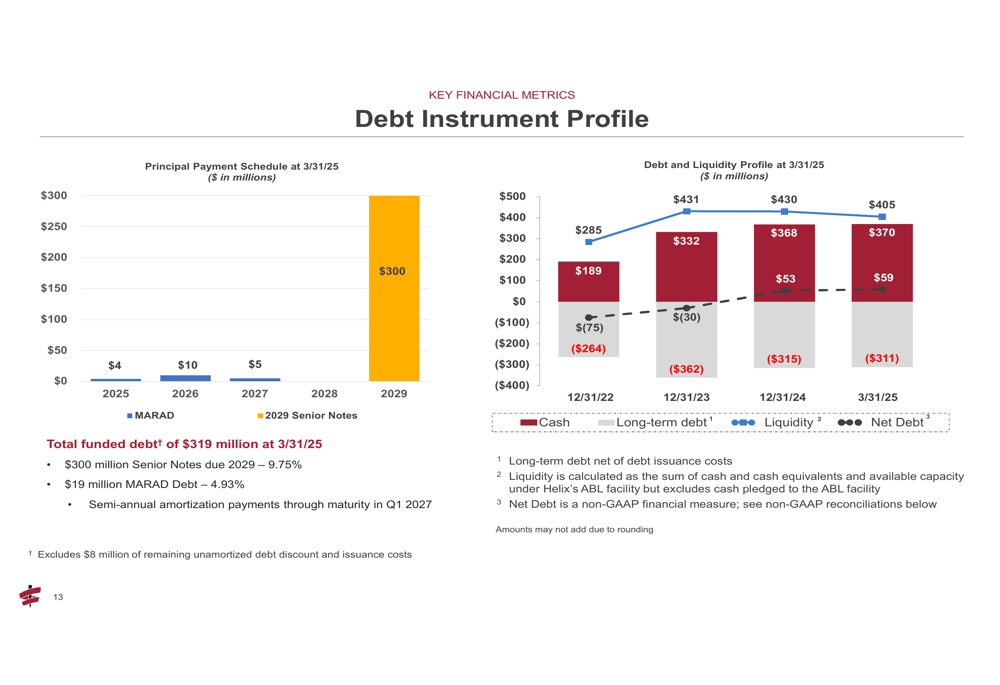

Helix maintained a strong balance sheet with $370 million in cash and cash equivalents as of March 31, 2025, up from $324 million a year earlier. The company’s net debt position improved to negative $59 million, indicating more cash than debt on the balance sheet.

The debt profile shows no significant maturities until 2029, providing financial flexibility:

Strategic Initiatives & Outlook

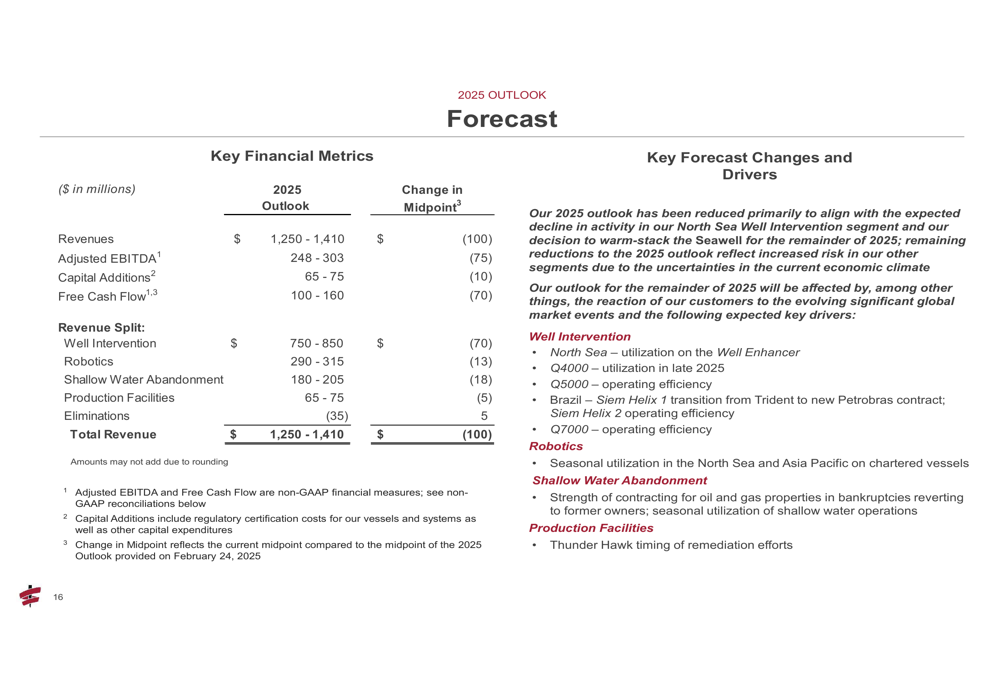

Helix has reduced its 2025 outlook, primarily due to expected decline in North Sea Well Intervention activity and the decision to warm-stack the Seawell vessel for the remainder of the year. The revised forecast projects:

CEO Owen Kratz noted during the earnings call, "Helix is resilient and with significant backlog and robust balance sheet, we’re well positioned to weather the storm." He also mentioned the company’s strategic decision regarding the Seawell vessel, stating, "We’re stacking the Seawell potentially for all of 2025 and potentially repurposing her to another region."

The company faces several challenges, including weakness in the North Sea market due to regulatory issues, potential impacts from US tariff hikes and OPEC production increases, and lower oil prices currently in the low $60s.

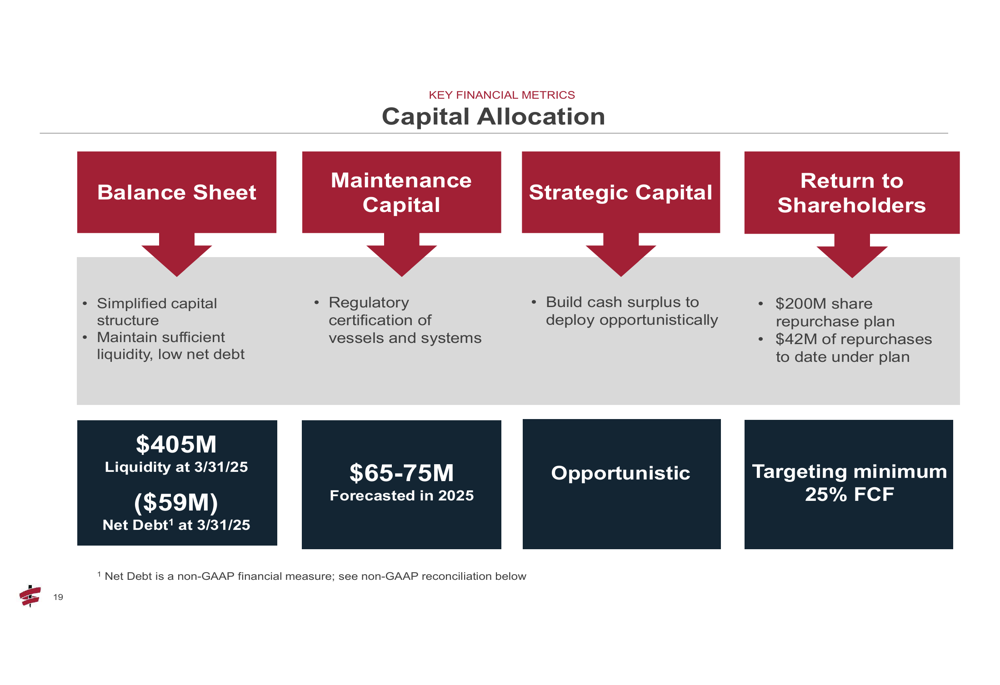

Capital Allocation & Balance Sheet Strength

Helix’s capital allocation strategy balances maintaining balance sheet strength, funding necessary maintenance capital, pursuing strategic opportunities, and returning value to shareholders:

The company has implemented a $200 million share repurchase plan, with $42 million of repurchases completed to date. Management has committed to allocating a minimum of 25% of free cash flow to shareholder returns.

Capital expenditures for 2025 are projected between $65-75 million, including $26 million for regulatory certification costs. Free cash flow generation is expected to reach $100-160 million for the full year, despite the reduced outlook.

Helix maintains its core purpose of enabling energy transition through maximizing existing reserves, lowering decommissioning costs, and supporting offshore renewables and wind farms. With approximately $1.4 billion in backlog and $455 million in liquidity, the company appears well-positioned to navigate the current challenging market environment while maintaining its strategic focus on long-term growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.