U.S. stocks steady; Cook’s dismissal, Nvidia earnings in spotlight

Introduction & Market Context

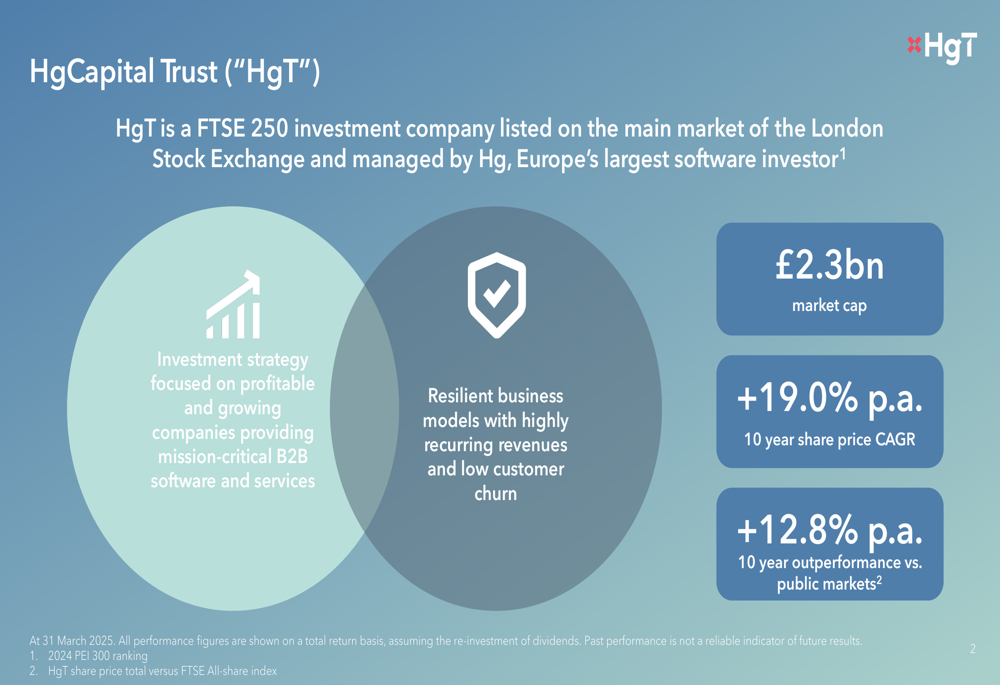

HgCapital Trust plc (LON:HGT), a FTSE 250 investment company providing listed access to private software businesses, presented its Q1 2025 update on May 8, highlighting continued strong underlying performance despite valuation headwinds.

The trust, which offers retail investors exposure to Hg’s portfolio of private equity investments in software and services businesses, maintains its focus on companies with highly recurring revenue models and mission-critical products. This strategy has delivered substantial long-term outperformance, though recent periods have seen challenges from multiple compression.

As shown in the following overview of HgCapital Trust’s positioning and performance metrics:

Executive Summary

HgT reported net assets of £2.4 billion as of March 31, 2025, with a NAV per share of 531.3p and share price of 506.0p. The trust’s long-term performance remains impressive, with a 10-year share price CAGR of 19.0% p.a., outperforming the FTSE All-Share Index by 12.8% p.a. over the same period.

However, year-to-date performance has lagged the benchmark, with share price declining 5.5% and NAV per share falling 2.0%, compared to the FTSE All-Share Index’s 4.5% gain. This underperformance reflects broader valuation pressures in the technology sector despite strong underlying business fundamentals.

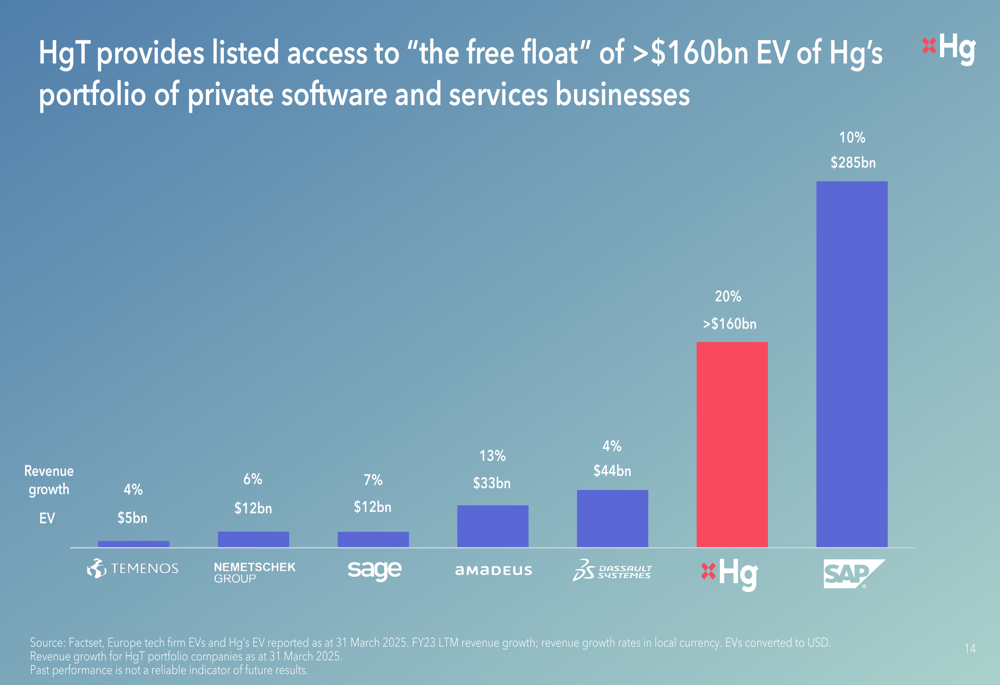

The trust is managed by Hg, Europe’s largest software investor with approximately $85 billion in assets under management and a portfolio enterprise value exceeding $160 billion. Hg’s investment focus remains on business-critical software with subscription or repeat revenue models, high margins, and fragmented customer bases.

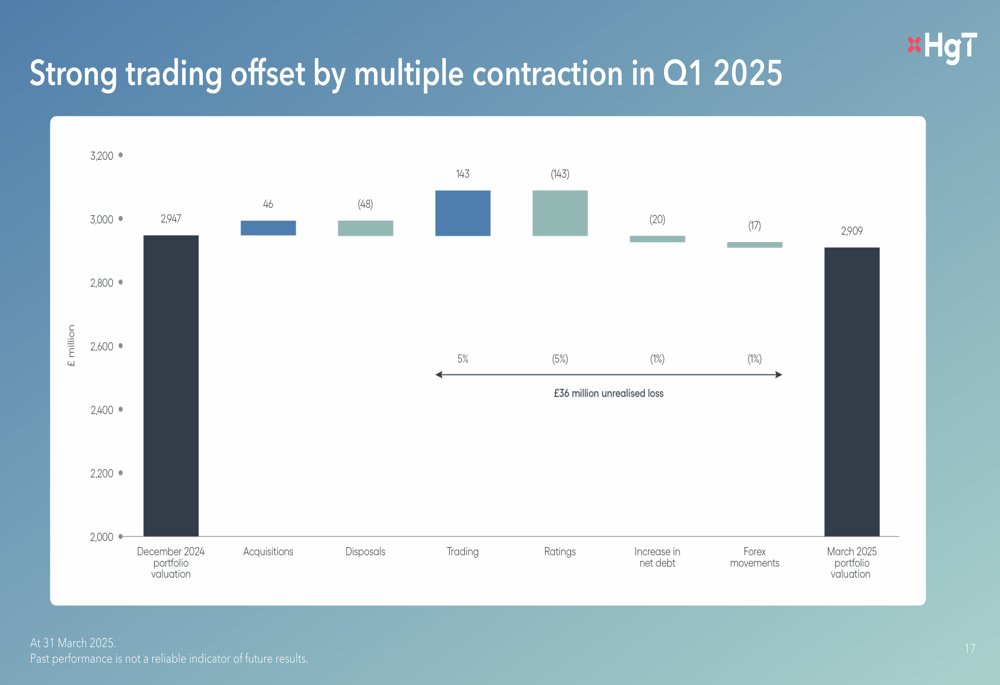

Quarterly Performance Highlights

The Q1 2025 results revealed a pattern of strong underlying business performance offset by valuation headwinds. As illustrated in the following waterfall chart, trading performance contributed positively with £143 million in gains, but this was completely offset by a £143 million negative impact from ratings (multiple contraction):

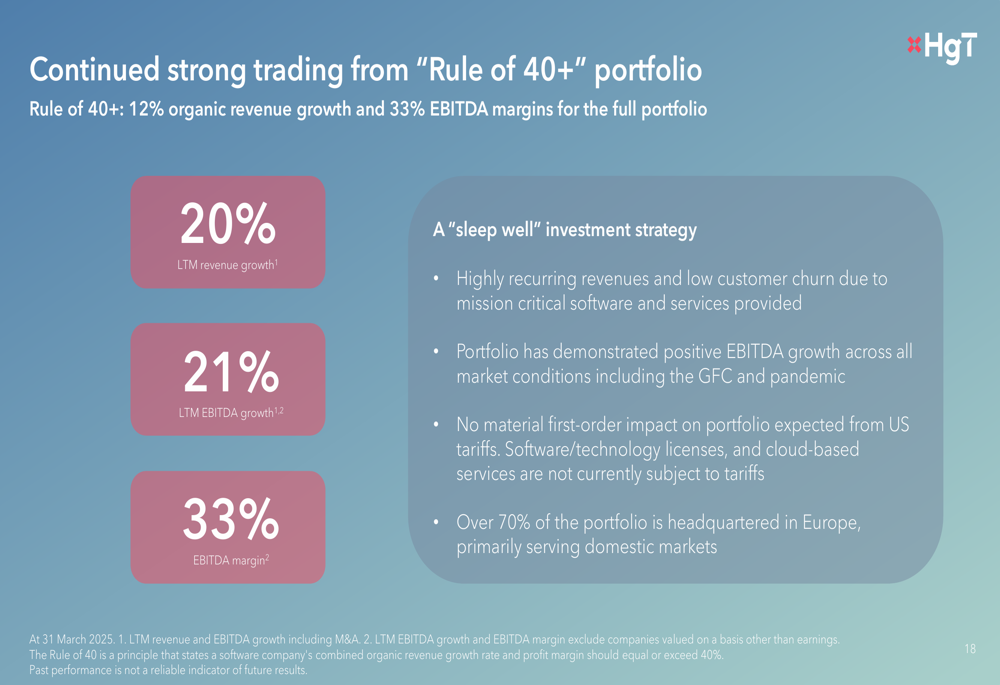

Despite these valuation challenges, the portfolio companies continue to demonstrate robust operational metrics, with 20% LTM revenue growth, 21% LTM EBITDA growth, and 33% EBITDA margins. The portfolio maintains what Hg calls a "Rule of 40+" profile, combining 12% organic revenue growth with 33% EBITDA margins.

The following slide highlights the strong trading performance of the portfolio:

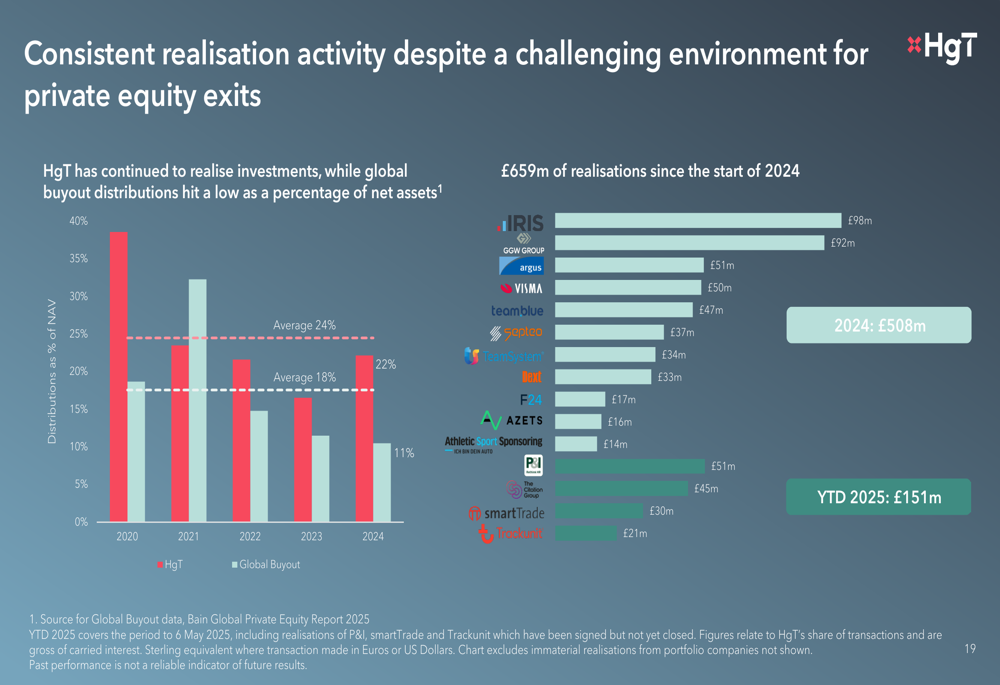

HgT has maintained consistent realisation activity despite the challenging environment for private equity exits. Since the start of 2024, the trust has realized £659 million from investments, including £151 million in 2025 year-to-date. Significant exits include IRIS (£98m), GGW GROUP (£92m), and Argus (£51m).

The following chart illustrates HgT’s realisation activity:

Simultaneously, Hg has continued to invest selectively, deploying £606 million in 2024 (including £109 million of co-investment) and £278 million year-to-date in 2025 (including £17 million of co-investment). Co-investment has increased to 10% of the portfolio in Q1 2025, up from 5% at the start of 2024, with a medium-term target of 10-15%.

Strategic Initiatives

During Q1 2025, HgT committed $1 billion to Hg Saturn 4, to be invested over the next three to four years. This commitment aligns with the trust’s strategy of providing investors with access to private software companies that are staying private longer and growing significantly before considering public listings.

The trust highlights that Europe’s fragmented market structure provides particular opportunities in the private software space, with over 50% of the top 40 European software companies remaining private, compared to less than 20% in the US.

As illustrated in the following slide, HgT provides listed access to a substantial portfolio of private software businesses with enterprise value exceeding $160 billion and revenue growth outpacing many public software companies:

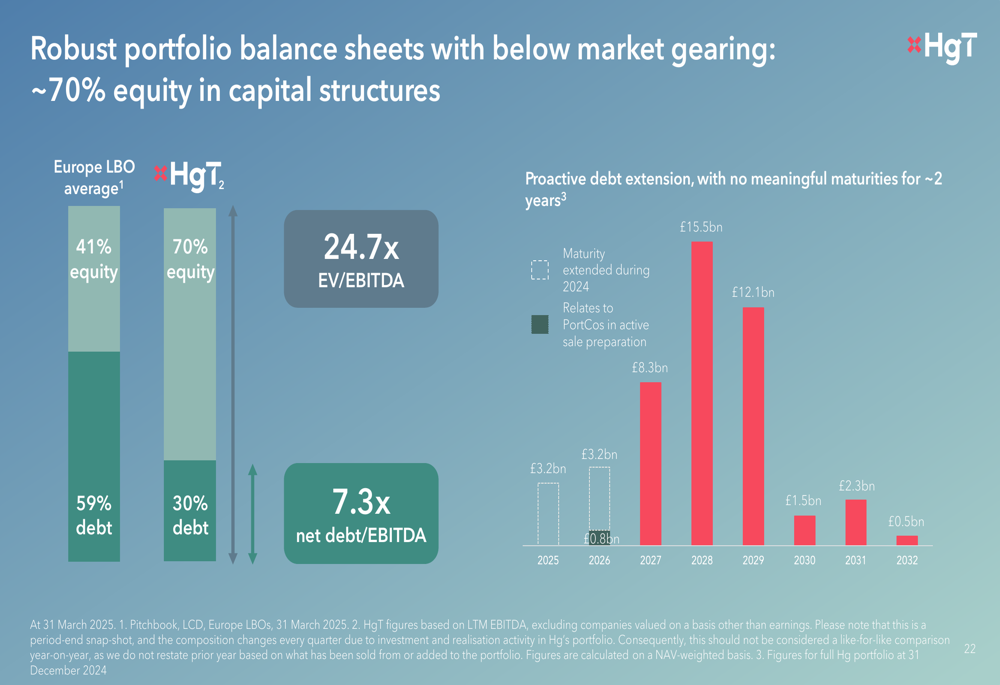

The portfolio maintains robust balance sheets with below-market leverage. The average net debt to EBITDA ratio stands at 7.3x, significantly lower than the European LBO average of 24.7x. Additionally, the capital structures feature approximately 70% equity, compared to the European LBO average of 41%.

The following chart illustrates this conservative approach to leverage:

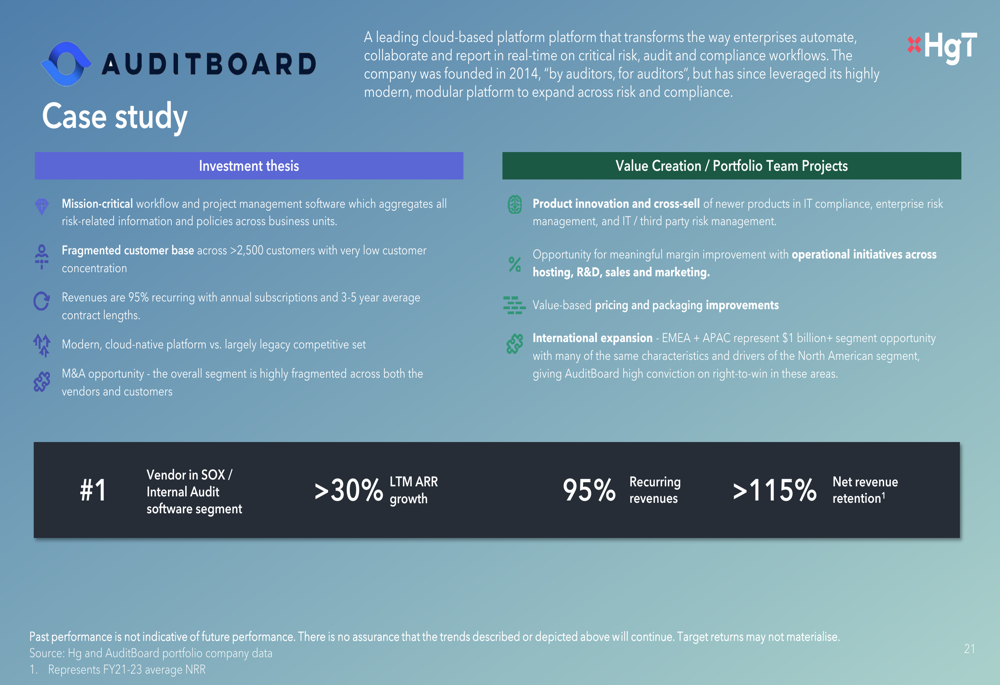

HgT also highlighted a case study of AuditBoard, a leading cloud-based platform for risk, audit, and compliance workflows. The company demonstrates the trust’s investment thesis with over 30% LTM ARR growth, 95% recurring revenues, and greater than 115% net revenue retention:

Forward-Looking Statements

Looking ahead, HgT expects continued resilient trading performance underpinned by the mission-critical nature of its portfolio companies’ products and services. Management does not anticipate any material first-order impact on the portfolio from US tariffs, noting that over 70% of the portfolio is headquartered in Europe, primarily serving domestic markets.

While the exit market remains challenging, the trust continues to prioritize returning cash to investors. HgT maintains a robust balance sheet to support future investment activity, with £375 million in undrawn credit facilities and £68 million in cash and cash equivalents as of March 31, 2025.

Management remains optimistic about the long-term investment opportunity, particularly as businesses seek to automate workflows to improve productivity and manage rising labor costs. The trust points to demographic trends showing a long-term decline in working-age population that is expected to drive up labor costs and increase software adoption.

Despite recent valuation headwinds, HgCapital Trust’s long-term performance metrics and focus on resilient business models with recurring revenue streams position it to potentially continue delivering value to investors as the digital transformation of businesses accelerates.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.