Stock market today: S&P 500 falls as government shutdown, trade jitters persist

Introduction & Market Context

HighPeak Energy (NYSE:HPK) presented its second quarter 2025 results on August 12, revealing a strategic shift toward operational efficiency and financial stability amid challenging market conditions. The Midland Basin pure play reported decreased production compared to the previous quarter, while highlighting debt management initiatives and cost-cutting measures.

The company’s stock closed at $8.76 on August 11, down 3.77% for the day, but gained 2.74% in after-hours trading following the presentation. Currently trading well below its 52-week high of $16.56, HighPeak faces the industry-wide challenge of balancing production growth with financial discipline in a volatile commodity price environment.

Quarterly Performance Highlights

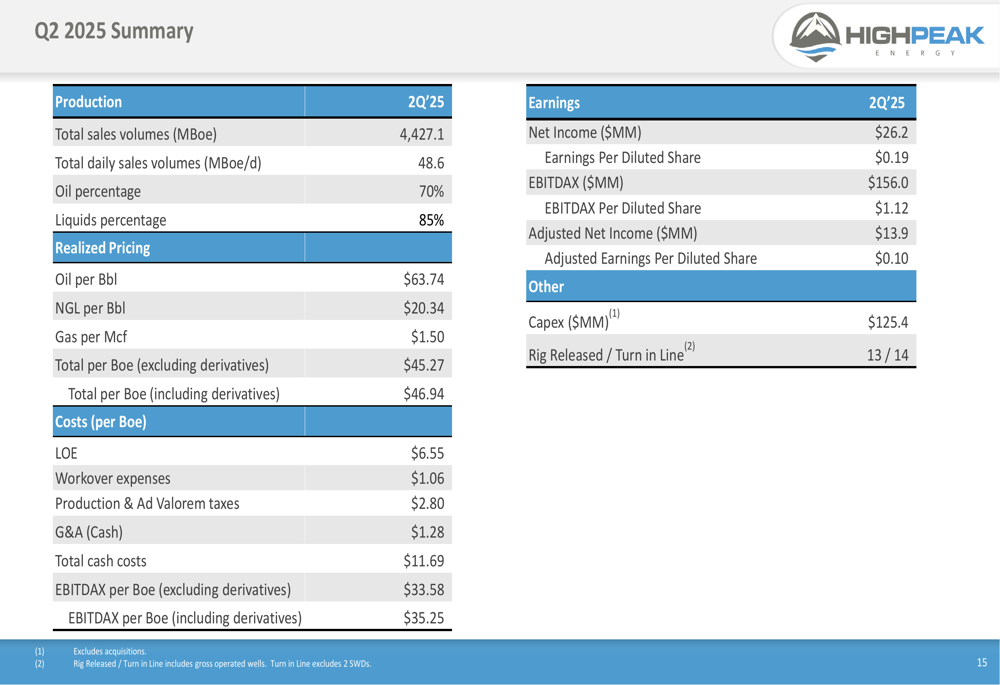

HighPeak reported Q2 2025 production of 48.6 MBoe/d, representing a 8.3% decrease from the 53,000 BOE/d achieved in Q1. Oil comprised 70% of total production, with liquids accounting for 85%. Despite the production decline, the company maintained strong operational efficiency with Q2 unhedged EBITDAX per BOE of $33.58.

The company posted Q2 net income of $26.2 million, translating to earnings per diluted share of $0.19, down from $0.31 in Q1. EBITDAX for the quarter reached $156 million, a significant decrease from nearly $200 million in the previous quarter.

As shown in the following comprehensive financial summary:

HighPeak’s realized pricing for the quarter averaged $63.74 per barrel for oil, $20.34 per barrel for NGLs, and $1.50 per Mcf for natural gas, resulting in a total realized price of $45.27 per BOE excluding derivatives. Total (EPA:TTEF) cash costs were contained at $11.69 per BOE, helping to maintain margins despite challenging commodity prices.

Financial Position and Debt Management

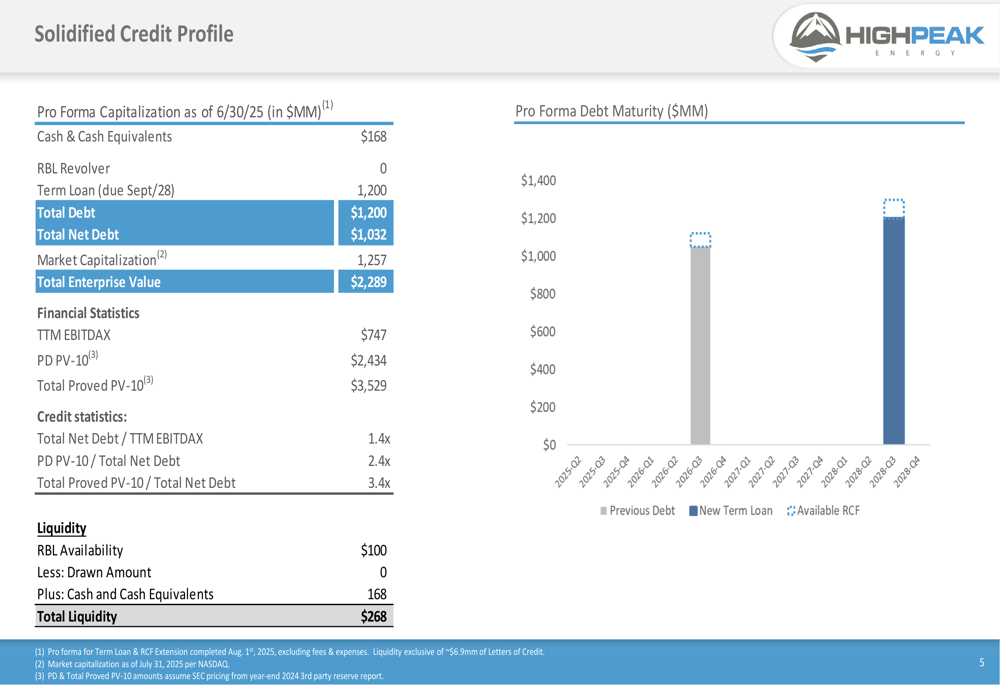

A key focus of HighPeak’s presentation was its strengthened financial position. The company has extended its Term Loan and Revolving Credit Facility maturities to September 2028, while upsizing the Term Loan to $1.2 billion to provide additional liquidity. The company also secured a deferral of Term Loan amortization payments until September 2026.

The company’s credit profile as of June 30, 2025, shows a total net debt of $1,032 million against a total enterprise value of $2,289 million. With a total net debt to trailing twelve months EBITDAX ratio of 1.4x, HighPeak maintains a relatively conservative leverage position compared to many peers in the sector.

The following slide illustrates the company’s improved debt maturity profile and key credit statistics:

HighPeak highlighted that the extension fees were "significantly less than other financing options" and that the floating interest rate structure provides "optionality in face of anticipated declines" in interest rates. Total liquidity stood at $268 million, consisting of $168 million in cash and $100 million in available revolving credit facility capacity.

Operational Efficiency Initiatives

HighPeak emphasized several operational efficiency initiatives aimed at reducing costs and improving returns. The company highlighted its Lorin Pad Simulfrac operation in May 2025, which completed wells at 4,500 ft/day using 80% recycled fluids. This approach reportedly saved approximately $400,000 per well and decreased completion costs by 3-5%.

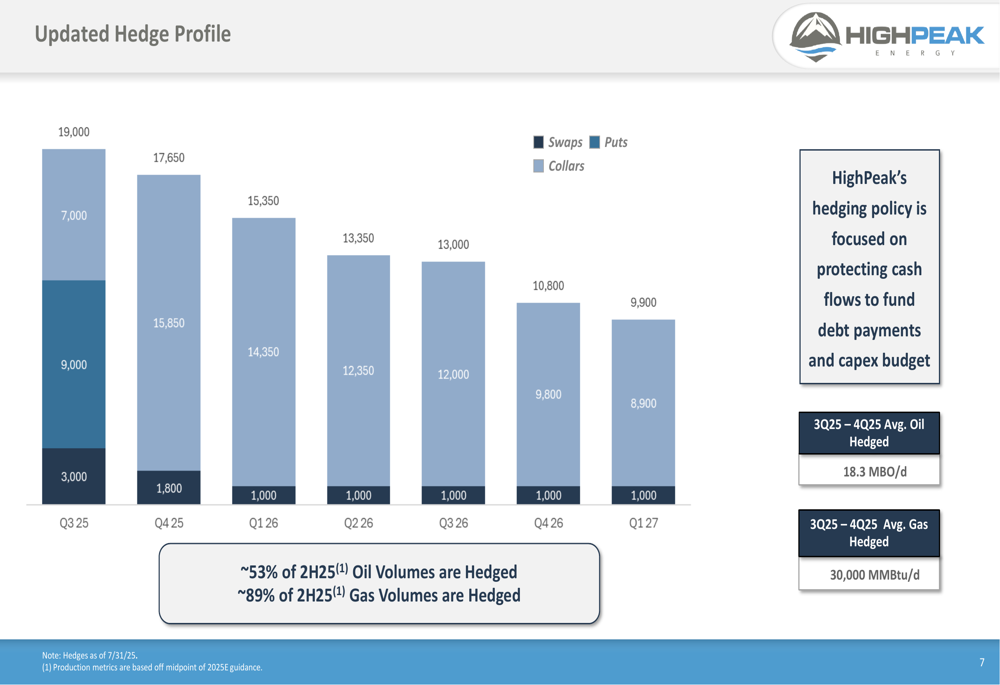

The company’s updated hedge profile shows a strategic approach to risk management, with approximately 53% of second-half 2025 oil volumes and 89% of gas volumes hedged. The hedging strategy is focused on protecting cash flows to fund debt payments and capital expenditures.

The following chart details HighPeak’s hedge positions through early 2027:

The company also reported progress on its solar energy initiative, which generated savings of $809,487 and reduced CO₂ emissions by 4,616 metric tons from June through December 2024.

Development Strategy and Outlook

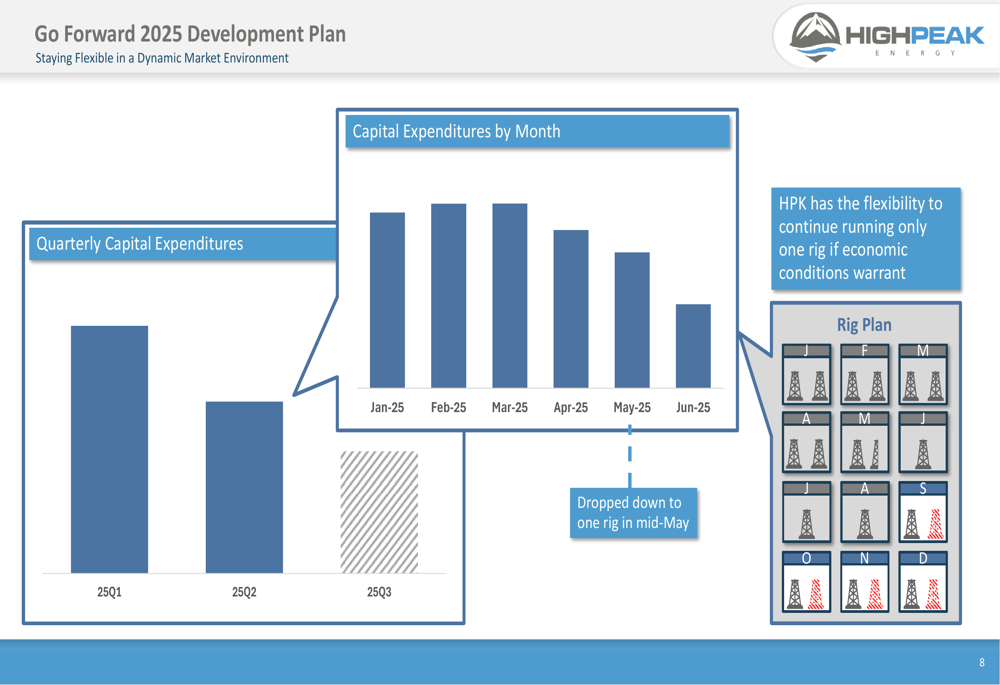

HighPeak has adjusted its development strategy in response to market conditions, reducing its rig count to one in mid-May 2025. The company’s capital expenditure trend shows a significant decrease from Q1 to Q2, with further reductions forecast for Q3.

The following development plan illustrates the company’s flexible approach to capital allocation:

Despite the reduced activity level, HighPeak continues to highlight its inventory of over 1,000 drilling locations with breakeven costs below $50 per barrel. The company reported encouraging results from its Middle Spraberry wells, with the first well producing cumulative oil of 170 MBbl in less than a year, potentially delineating over 200 additional Middle Spraberry locations.

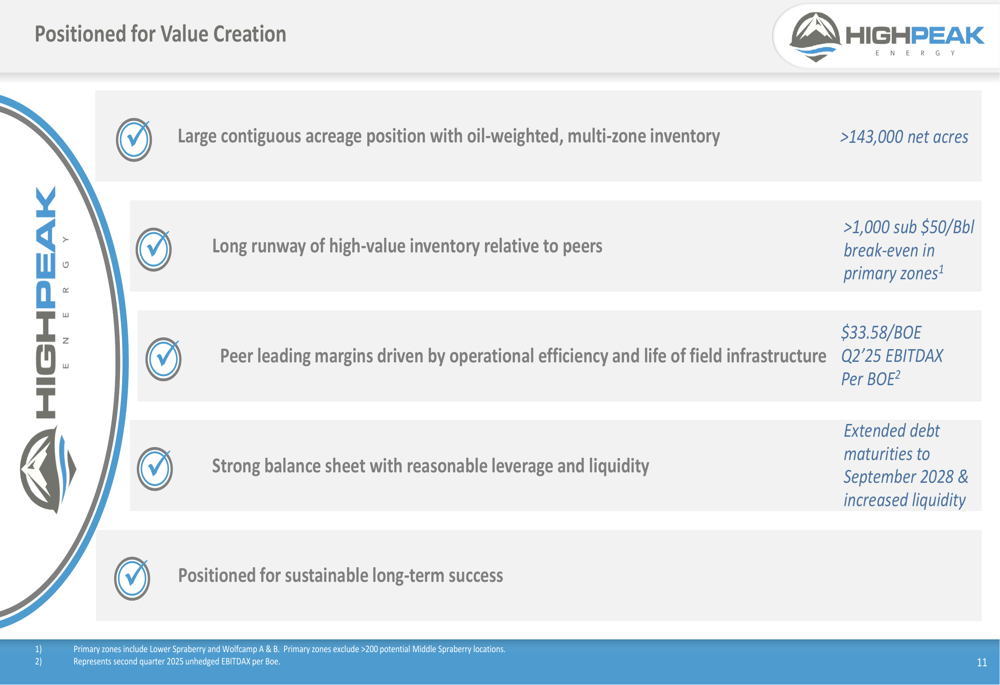

HighPeak’s positioning for value creation centers on its large contiguous acreage position (over 143,000 net acres), long runway of high-value inventory, peer-leading margins, and strengthened balance sheet:

The company’s cautious approach to development, combined with its focus on operational efficiency and financial discipline, suggests HighPeak is prioritizing sustainability over growth in the current market environment. This represents a notable shift from the more aggressive growth posture indicated in previous quarters, reflecting adaptation to evolving market conditions and investor preferences for capital discipline in the energy sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.