China chip stocks fall as US considers allowing Nvidia H200 sales

Introduction & Market Context

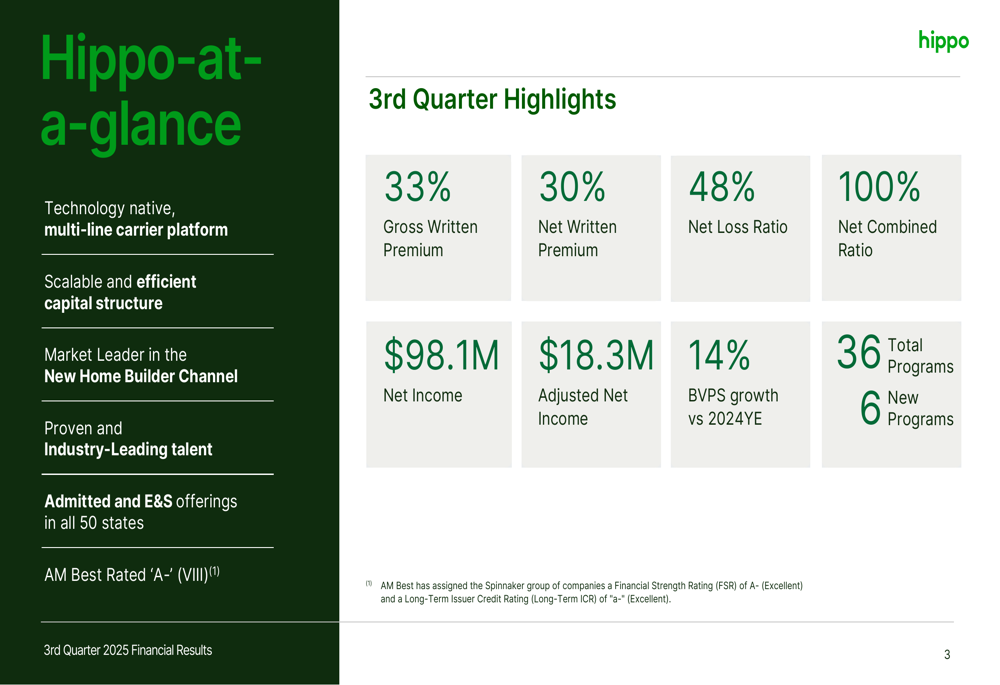

Hippo Holdings Inc. (NYSE:HIPO) presented its third-quarter 2025 financial results on November 5, showcasing significant premium growth and a substantial improvement in profitability. The technology-focused insurer's shares rose 2.34% to $36.73 in regular trading following the announcement, with premarket activity showing gains of 2.4%.

The results come amid a period of strategic transformation for Hippo, which has been diversifying its insurance offerings beyond its core homeowners business while maintaining its technology-native approach to underwriting and customer service.

Quarterly Performance Highlights

Hippo reported impressive growth metrics for Q3 2025, with gross written premiums increasing 33% year-over-year and net written premiums rising 30%. The company achieved a net income of $98.1 million, a dramatic improvement from the $8.5 million loss in the same quarter last year.

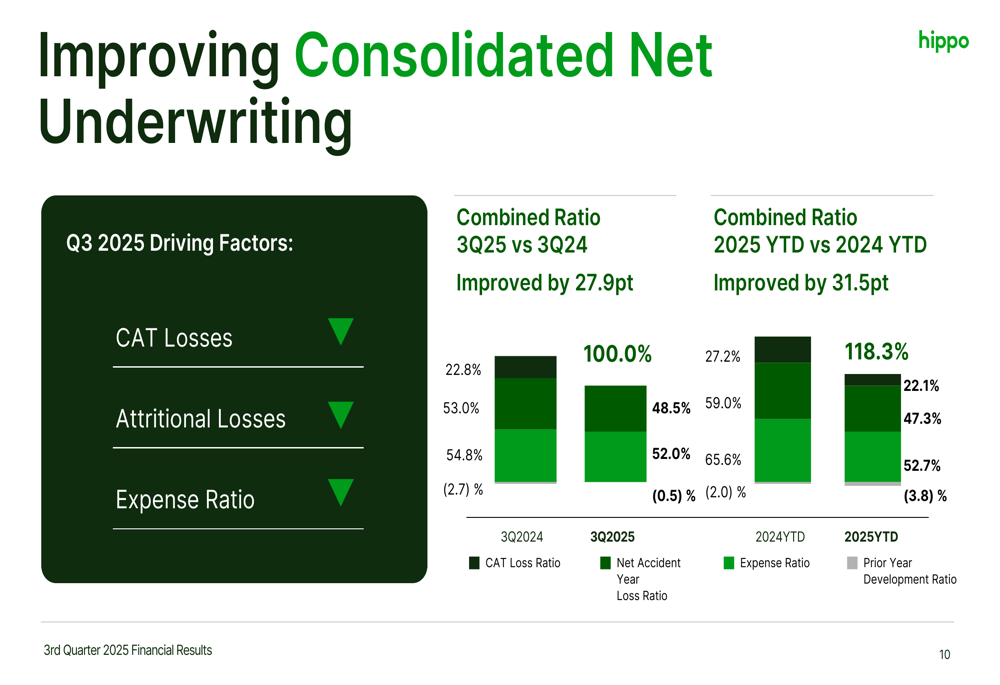

The insurer's underwriting performance showed substantial improvement, with the net loss ratio decreasing to 48% and the combined ratio reaching 100%, representing a 27.9 percentage point improvement compared to Q3 2024.

As shown in the following comprehensive overview of Hippo's third-quarter performance:

Adjusted net income reached $18.3 million, compared to a $1.3 million loss in the prior-year period. This improvement reflects the company's focus on disciplined underwriting and portfolio optimization.

Strategic Initiatives and Diversification

A key element of Hippo's strategy has been diversifying beyond its original homeowners insurance focus. The company reported $80 million in gross written premium growth in its Commercial Multi-Peril (CMP) and Casualty lines, representing a 130% increase over Q3 2024.

In June 2025, Hippo completed an organizational restructuring and sold its homebuilder distribution network for a net gain of $91 million, contributing significantly to the quarter's profitability. The company has also begun integrating Westwood Insurance Agency, with the first policies bound in October 2025.

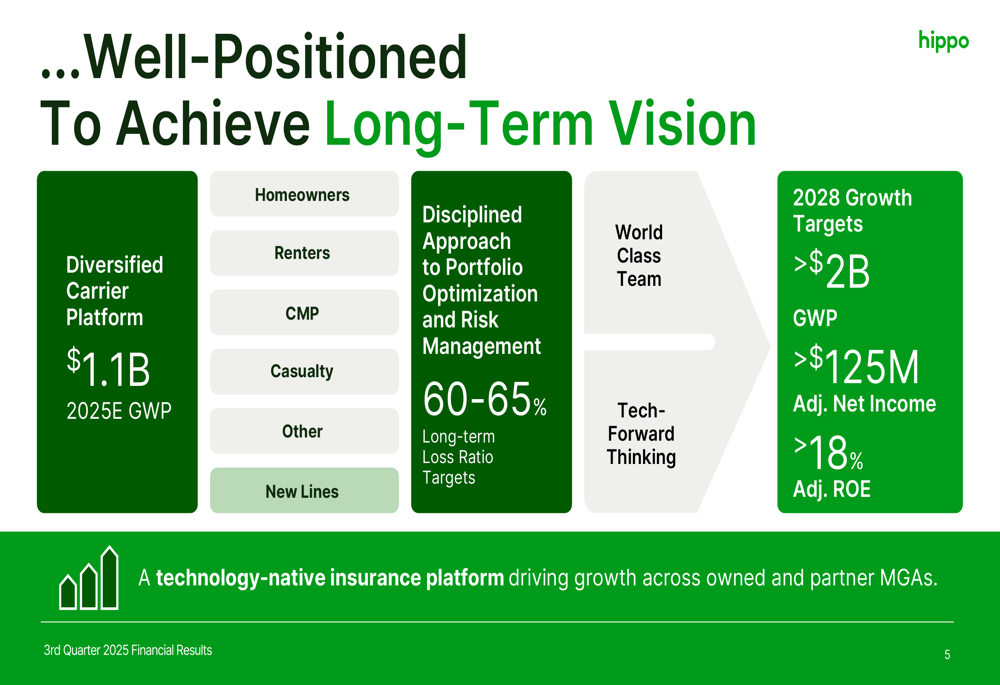

The company's strategic vision and long-term targets are illustrated in this slide:

Hippo has also strengthened its leadership team with key appointments, including Robin Gordon as Chief Data Officer and the addition of Laura Hay and Susan Holliday to its board of directors, bringing expertise from MetLife, KPMG International, and Swiss Re, respectively.

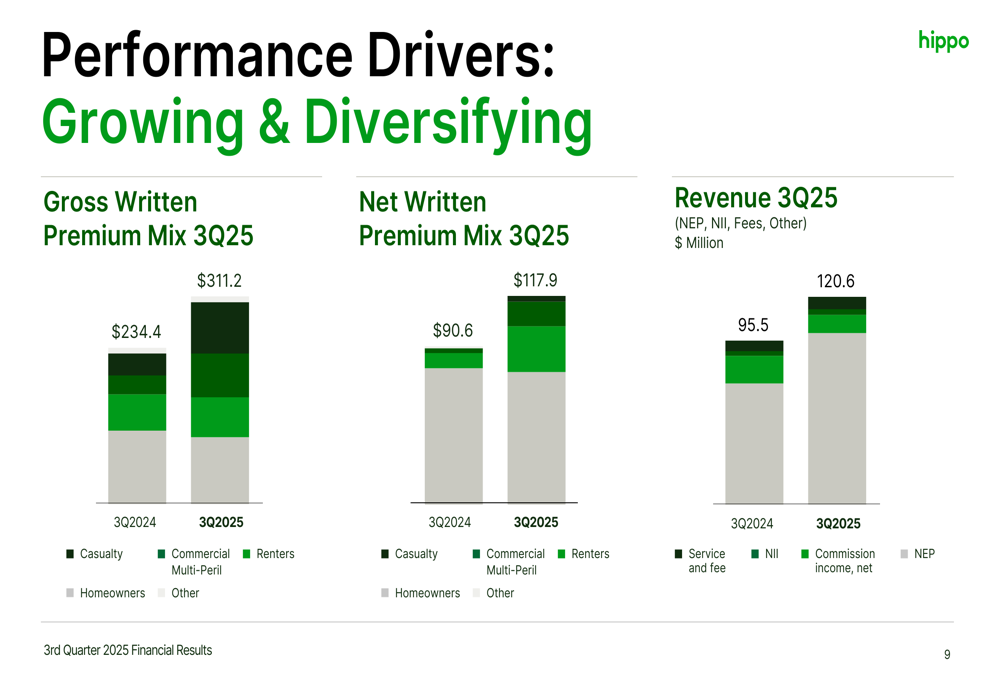

Detailed Financial Analysis

The diversification of Hippo's premium mix is evident in the breakdown of its revenue streams, showing growth across multiple lines of business:

Hippo's underwriting performance has shown consistent improvement, with the combined ratio reaching 100% in Q3 2025, down from 127.9% in Q3 2024. This improvement was driven by reductions in catastrophe losses, attritional losses, and expense ratio.

The following chart illustrates the components of Hippo's improved underwriting performance:

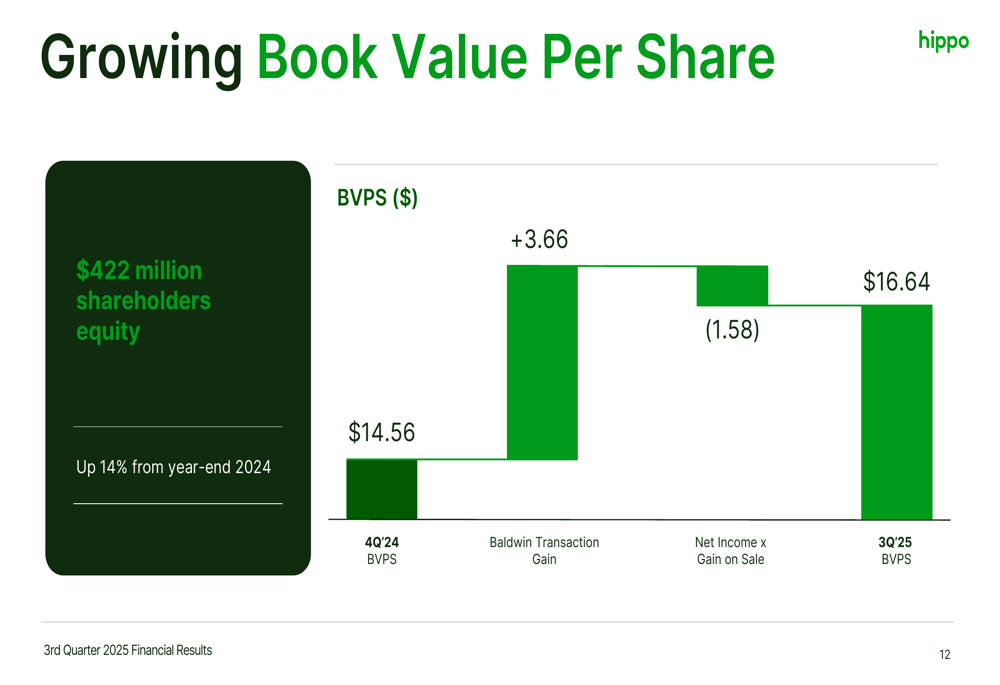

The company's book value per share grew to $16.64, a 14% increase from $14.56 at the end of 2024. This growth was primarily driven by the Baldwin transaction gain of $3.66 per share, partially offset by other factors:

Forward-Looking Statements

Hippo provided guidance for the full year 2025, projecting gross written premiums between $1.09 billion and $1.11 billion and revenue between $465 million and $468 million. The company expects a net loss ratio of 63-64% and adjusted net income between $10 million and $14 million.

Looking further ahead, Hippo has set ambitious targets for 2028, including:

- Gross written premiums exceeding $2 billion

- Adjusted net income above $125 million

- Adjusted return on equity greater than 18%

These targets are outlined in the company's long-term value projection:

CEO Rick McCathron emphasized the company's commitment to leveraging its technology-native platform to drive growth during the earnings call, stating, "We are doubling down on what we do best: building a technology-native insurance platform that drives profitable growth."

Market Reaction and Analyst Perspectives

Investors responded positively to Hippo's results, with the stock rising 2.34% in regular trading to $36.73, building on premarket gains of 2.4%. The stock has traded between $19.92 and $38.98 over the past 52 weeks, with the current price representing significant recovery from its lows.

During the Q&A session, analysts inquired about Hippo's growth strategy in the casualty line and its approach to the homeowners market. The company addressed potential capital allocation strategies, emphasizing its strong cash position and focus on strategic investments to support its ambitious growth targets.

With its improved financial performance, strategic diversification, and clear long-term vision, Hippo appears well-positioned to continue its growth trajectory while maintaining disciplined underwriting practices in the competitive insurance market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.