ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Hoist Finance AB (STO:HOFI) presented its Q1 2025 results on May 7, 2025, showcasing a 19% year-over-year increase in profit before tax amid continued portfolio growth and strong operational performance. The company’s stock closed at SEK 86.5 on May 6, 2025, down slightly by 0.29% ahead of the earnings presentation.

The European debt purchasing specialist continues to capitalize on growing NPL ratios in European banks and an active secondary market, while making progress toward achieving Specialised Debt Restructurer (SDR) status in 2026, which would provide significant regulatory benefits.

Quarterly Performance Highlights

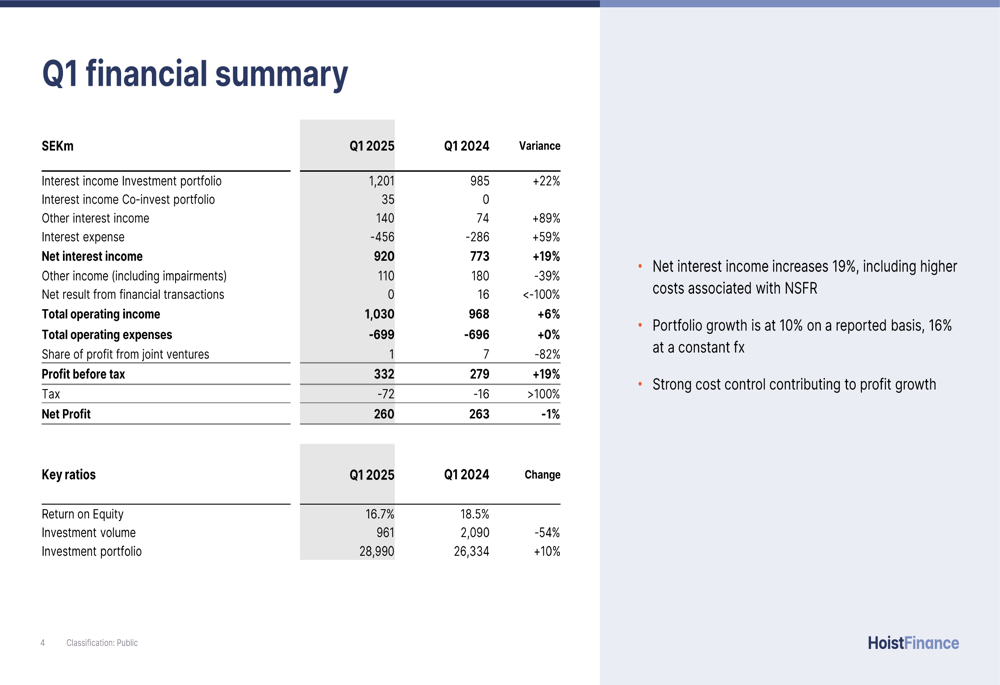

Hoist Finance reported profit before tax of SEK 332 million for Q1 2025, a 19% increase from SEK 279 million in the same quarter last year. Net interest income grew by 19% year-over-year, outpacing the 16% constant currency portfolio growth, demonstrating improved yield on investments.

As shown in the following financial summary:

Return on equity stood at 16.7% for the quarter, compared to 18.5% in Q1 2024. Despite the slight decline in ROE, the company maintained strong earnings per share of SEK 2.33. The total investment portfolio reached SEK 29.0 billion, representing a 10% increase on a reported basis and 16% at constant exchange rates.

The company’s collection performance remained strong at 103% across markets, though slightly below the 106% reported in Q1 2024. This performance, combined with tight cost control, contributed significantly to the profit growth.

Portfolio Growth and Diversification

Hoist Finance invested SEK 961 million in new portfolios during Q1 2025, with an additional SEK 1.3 billion in investments signed to close in Q2 and Q3. While the investment volume was lower than the SEK 2.1 billion reported in Q1 2024, management highlighted a strong pipeline for the remainder of the year.

The quarterly investment trend over recent years shows the company’s consistent approach to portfolio expansion:

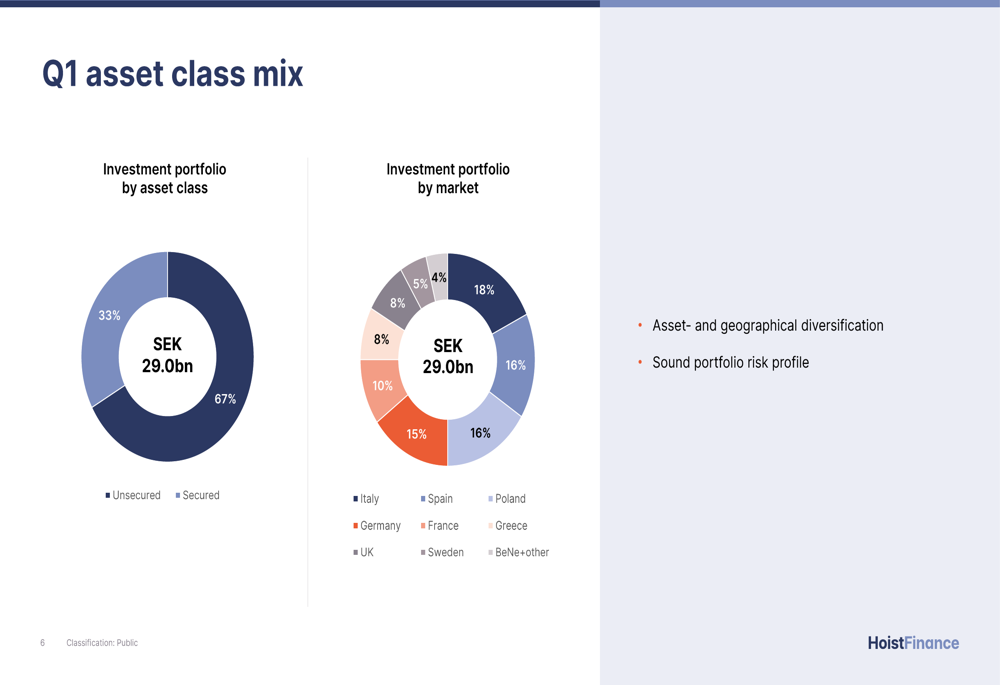

The company maintains a well-diversified portfolio both by asset class and geography. Secured assets represent 67% of the portfolio, with unsecured assets accounting for 33%. Geographically, the portfolio is spread across multiple European markets, with Italy (18%), Spain (16%), and Sweden (15%) representing the largest exposures.

As illustrated in the asset class and geographical distribution:

This diversification strategy helps mitigate risk while providing multiple avenues for growth across different market conditions.

Cost Control and Operational Efficiency

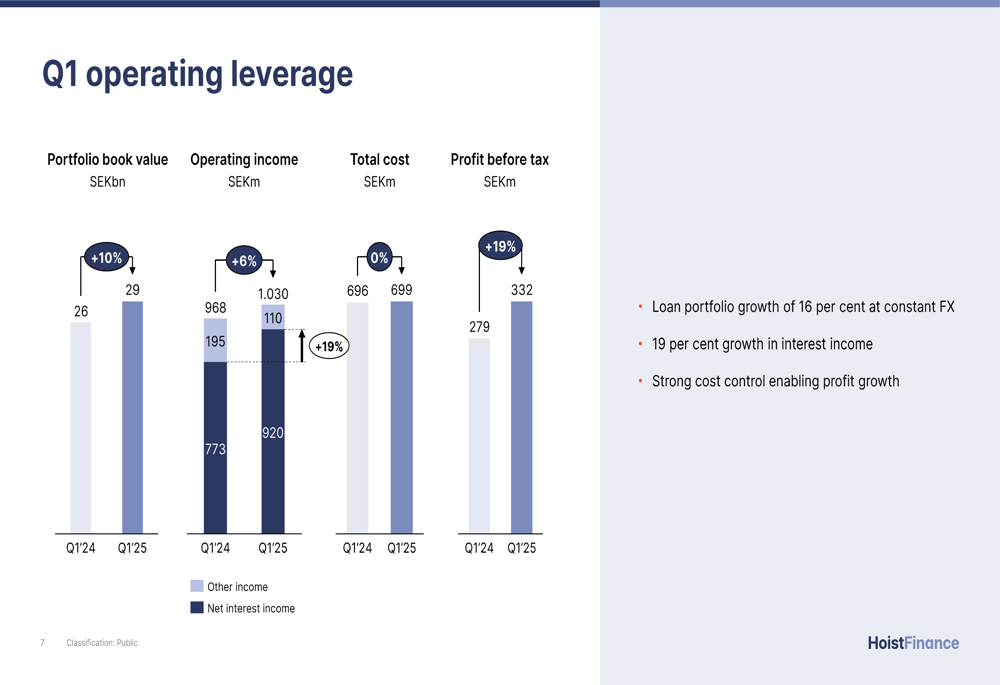

A key driver of Hoist Finance’s improved profitability has been its focus on operational efficiency and cost control. Despite inflationary pressures, total operating expenses remained flat year-over-year at SEK 699 million, compared to SEK 696 million in Q1 2024.

The company’s operating leverage is clearly demonstrated in the following comparison:

The company has achieved this cost discipline while growing its portfolio and revenues, resulting in expanding margins and higher profitability. Full-time equivalent (FTE) headcount decreased to 1,031 in Q1 2025 from 1,303 in Q1 2024, reflecting ongoing efficiency improvements.

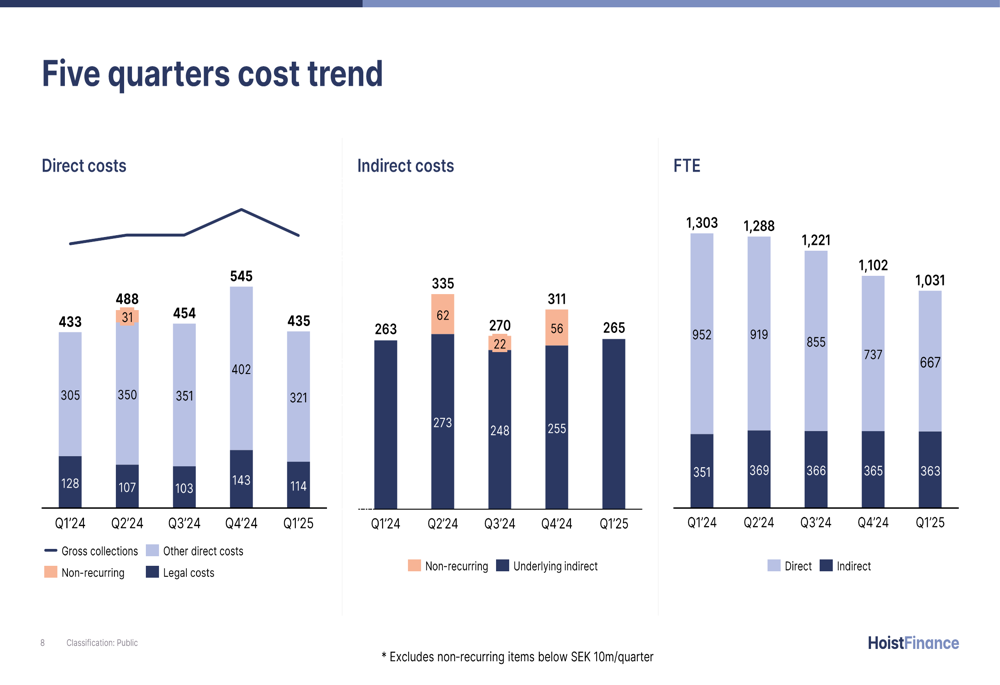

The five-quarter cost trend shows consistent management of both direct and indirect costs:

Capital Position and Funding

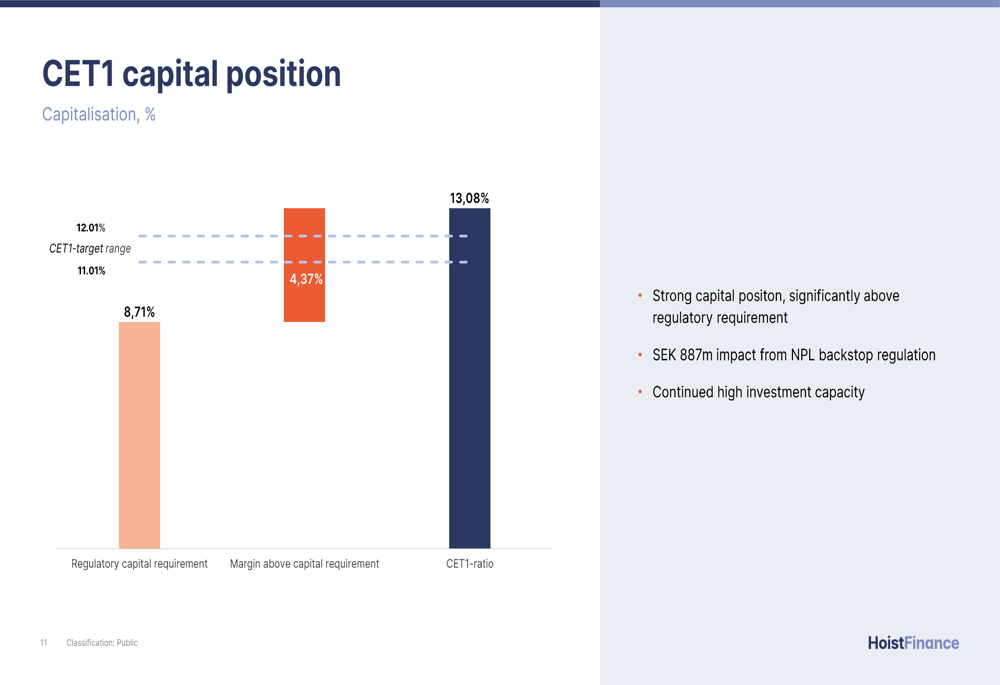

Hoist Finance maintains a strong capital position with a CET1 ratio of 13.08%, significantly above the regulatory requirement of 8.71%. This provides a comfortable buffer of 4.37 percentage points and ensures continued investment capacity.

The capital position is illustrated in the following chart:

On the funding side, the company issued SEK 750 million in senior preferred bonds over three years at STIBOR +155 basis points, and SEK 700 million in senior non-preferred bonds over five years at STIBOR + 250 basis points during the quarter. The company also redeemed EUR 40 million in AT1 instruments without issuing new ones.

Deposits continue to be the primary funding source, representing 81% of total funding, with an average cost of funding at 3.70% in Q1 2025, up from 2.84% in Q1 2023.

The company’s liquidity position remains exceptionally strong, with the Liquidity Coverage Ratio (LCR) at 1,567% and Net Stable Funding Ratio (NSFR) at 138%. The liquidity reserve expanded to SEK 27 billion by the end of Q1 2025.

Strategic Initiatives and Outlook

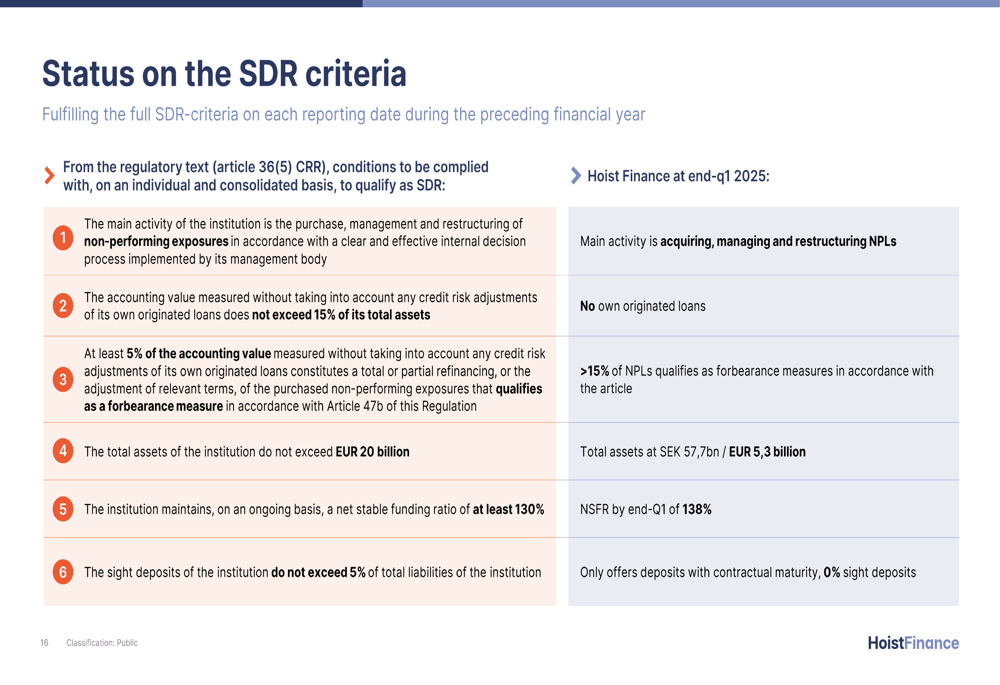

A significant strategic focus for Hoist Finance is achieving Specialised Debt Restructurer (SDR) status, which would provide regulatory benefits. The company reported that it now meets all the criteria as of Q1 2025 and is on track to qualify as an SDR in 2026.

The key SDR criteria and Hoist Finance’s status are summarized as follows:

Looking ahead, management highlighted several positive factors supporting continued growth:

- A strong investment pipeline for the year

- Growing NPL ratios in European banks and an active secondary market

- Increasing operational leverage

- Significant purchasing power and competitive funding costs

- Progress toward SDR status in 2026

CEO Harry Vranjes and CFO Magnus Söderlund presented the results, emphasizing the company’s balanced approach to growth, cost control, and portfolio diversification as key drivers of sustainable performance.

With its strong capital position, diversified portfolio, and operational efficiency, Hoist Finance appears well-positioned to capitalize on opportunities in the European NPL market while maintaining profitability in the quarters ahead.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.