What happens to stocks if AI loses momentum?

Introduction & Market Context

HomeStreet Inc (NASDAQ:HMST) released its first quarter 2025 presentation on April 28, showing signs of gradual improvement amid ongoing financial challenges. The Seattle-based bank, with $7.8 billion in total assets, continues to navigate a complex interest rate environment while implementing its profitability plan.

The presentation comes as HomeStreet’s stock trades at $13.36, well above its 52-week low of $8.41 but still below its high of $16.10. The bank’s first quarter results reflect both persistent headwinds and emerging positive trends as it works toward a return to profitability.

Quarterly Performance Highlights

HomeStreet reported a net loss of $4.5 million, or $0.24 per share, for Q1 2025. On a core basis, which excludes certain non-recurring items, the net loss was $2.9 million, or $0.15 per share. Notably, while the parent company posted a loss, HomeStreet Bank itself achieved net income of $1.1 million for the quarter.

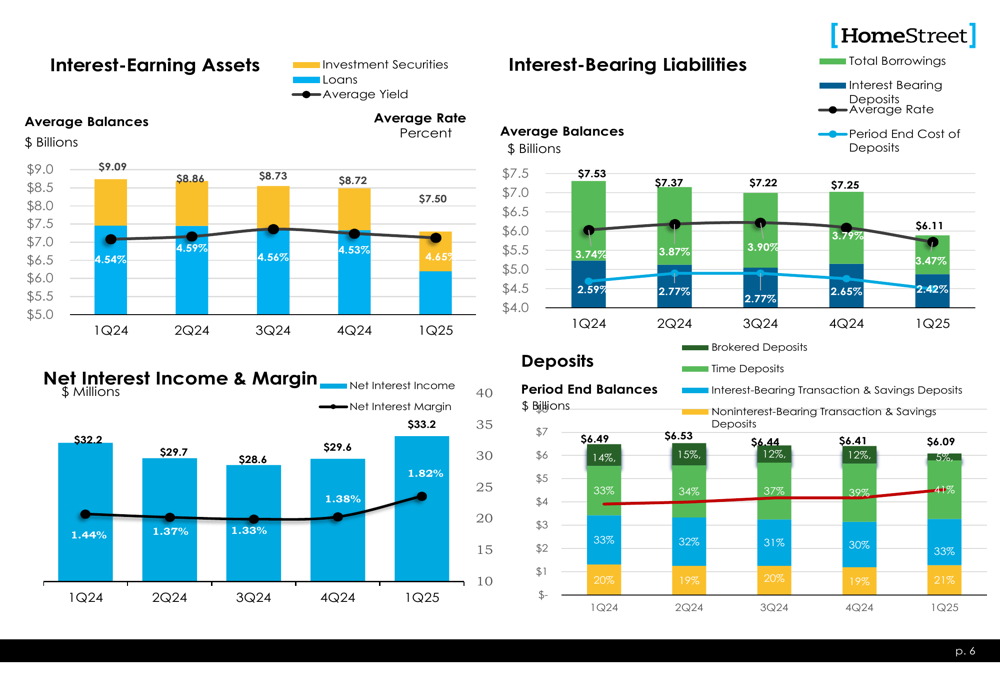

The bank’s net interest margin improved to 1.82%, a significant increase from the 1.38% reported in Q4 2024. This improvement reflects the company’s efforts to reprice loans and manage its balance sheet more effectively.

As shown in the following chart of interest-earning assets and liabilities, the average rate on interest-earning assets increased to 4.65% in Q1 2025 from 4.54% in Q1 2024, while the average rate on interest-bearing liabilities decreased to 3.47% from 3.74% over the same period:

Deposit growth was another bright spot, with total deposits increasing by $131 million from December 31, 2024, to March 31, 2025. Average deposits were $42 million higher in Q1 2025 compared to Q4 2024, excluding broker deposits.

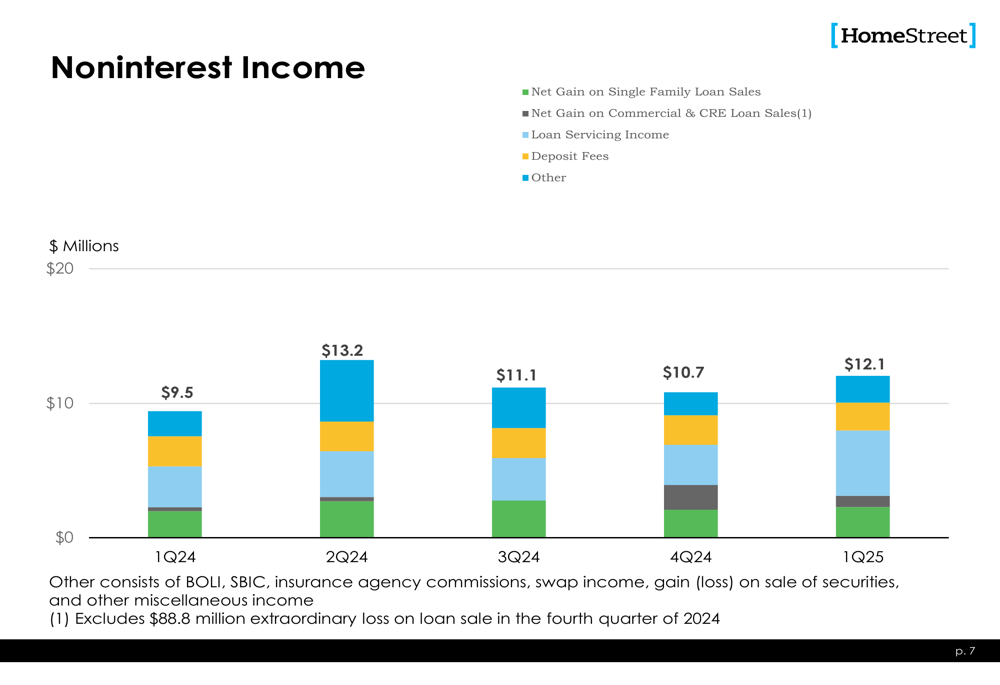

Noninterest income rose to $12.1 million in Q1 2025, up from $9.5 million in the same quarter last year, as illustrated in this breakdown:

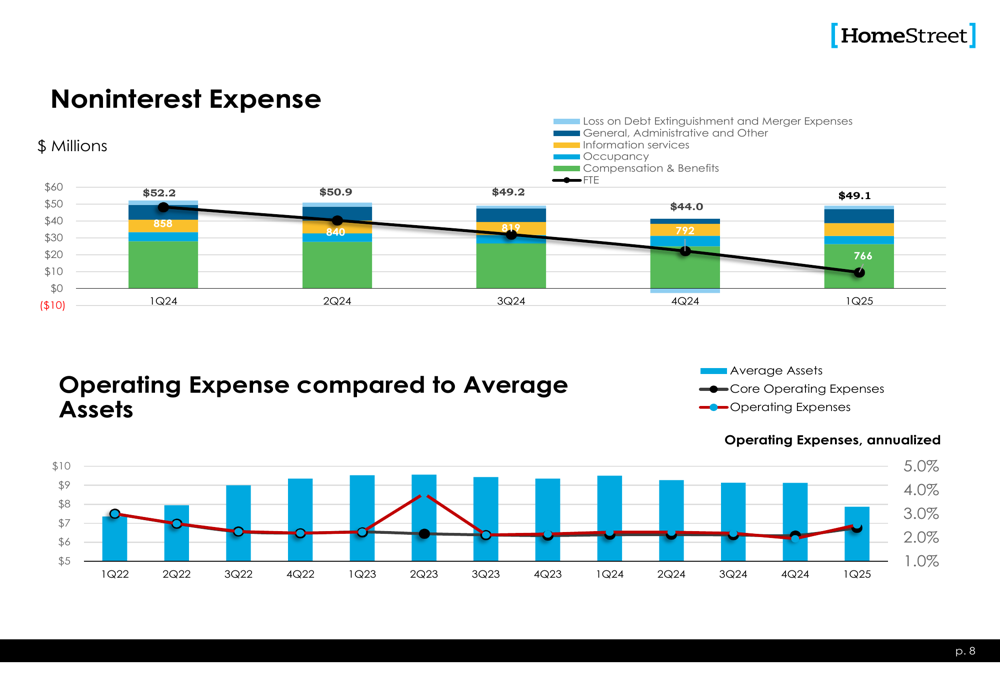

Meanwhile, noninterest expenses totaled $49.1 million for the quarter, down from $52.2 million in Q1 2024, demonstrating the company’s ongoing cost control efforts:

Merger Announcement

The most significant development revealed in the presentation was HomeStreet’s merger agreement with Mechanics Bank. The transaction is expected to close in the third quarter of 2025, though specific financial terms were not disclosed in the presentation materials.

This strategic move comes as HomeStreet continues to implement its profitability plan, with expectations of returning to core profitability in 2025. The merger could provide additional scale and resources to strengthen the combined entity’s competitive position in the western United States.

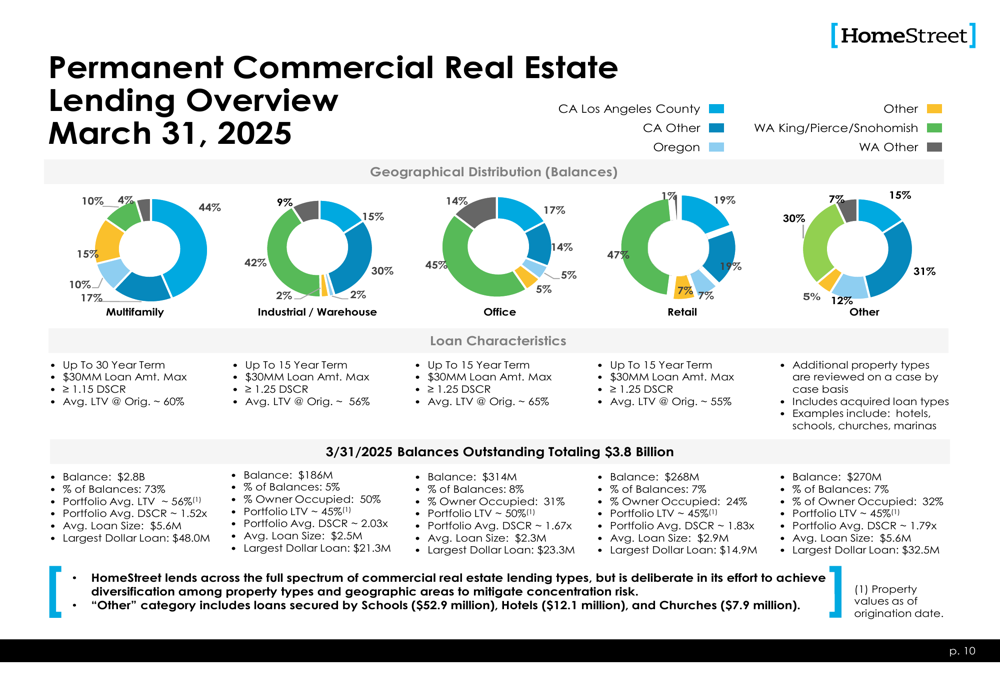

Loan Portfolio and Geographic Focus

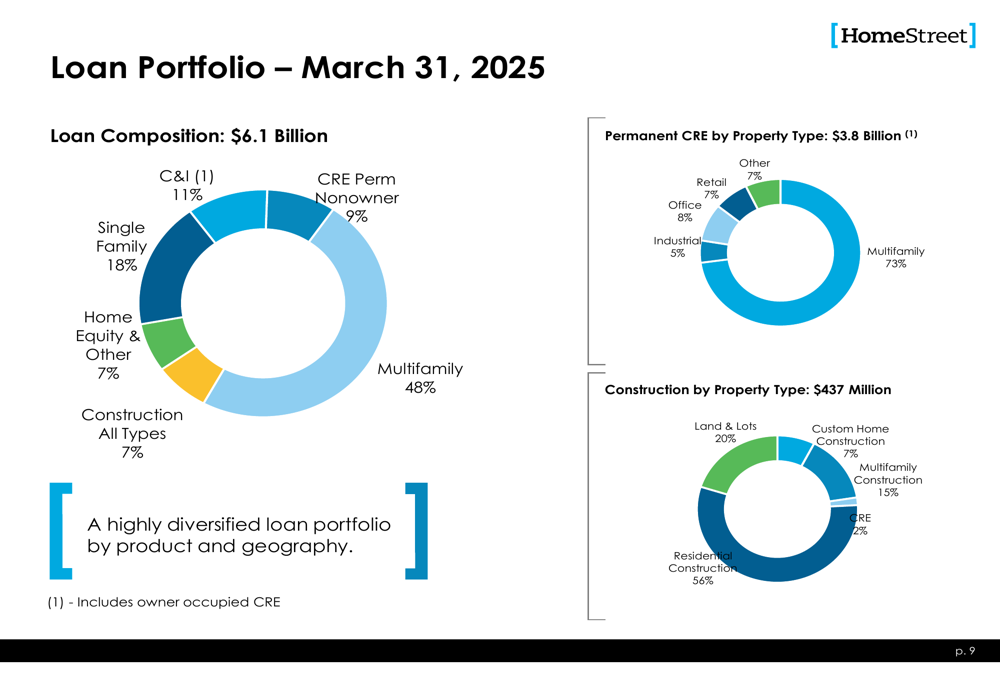

HomeStreet maintains a diversified loan portfolio with a strong emphasis on multifamily lending, which comprises 48% of its $6.1 billion loan portfolio. Single-family loans represent 18%, commercial and industrial (C&I) loans account for 11%, and commercial real estate (CRE) permanent non-owner occupied properties make up 9%.

The following chart illustrates the bank’s loan portfolio composition as of March 31, 2025:

Geographically, HomeStreet operates throughout the western United States, with 56 retail deposit branches, 3 primary stand-alone lending centers, and 1 primary stand-alone insurance office. Its market focus includes Seattle/Puget Sound, Southern California, Portland, the Hawaiian Islands, and Idaho/Utah for single-family construction lending.

The bank’s permanent commercial real estate lending is distributed across these regions, with detailed loan characteristics shown below:

Liquidity and Deposit Base

HomeStreet emphasized its strong liquidity position and diversified deposit base. As of March 31, 2025, uninsured deposits totaled $542 million, representing just 9% of total deposits—a relatively low level that reduces potential volatility.

The bank’s top ten customers account for only 4.9% of total deposit balances, reflecting a well-diversified customer base. The average balance of noninterest-bearing consumer deposit accounts was $8,000, while the average balance of noninterest-bearing business deposit accounts was $63,000.

HomeStreet reported on-balance sheet liquidity of 19% as of March 31, 2025. Additionally, available contingent liquidity borrowing sources totaled $5.5 billion, equivalent to 91% of total deposits, providing substantial financial flexibility.

The bank continues to attract new deposit clients, with its branch system adding 91 new business customers and commercial banking adding 21 new customers in Q1 2025.

Forward-Looking Statements

Looking ahead, HomeStreet expects to return to core profitability in 2025, consistent with previous guidance that projected a return to profitability in the first half of the year. The merger with Mechanics Bank represents a significant strategic shift that could accelerate this timeline.

The bank’s book value per share stood at $21.18 as of March 31, 2025, with tangible book value per share at $20.83. These figures provide a baseline for evaluating the company’s progress as it works to improve financial performance.

HomeStreet also highlighted its customer satisfaction metrics, noting a Net Promoter Score of 53 in 2024—exceeding the banking industry benchmark for the ninth consecutive year. This strong customer loyalty could prove valuable as the bank navigates its merger and continues its recovery efforts.

As interest rates potentially stabilize and the bank’s profitability initiatives take hold, HomeStreet appears positioned to build on the modest improvements seen in Q1 2025, though challenges clearly remain as evidenced by the continued net loss at the parent company level.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.