Gold prices dip as hawkish Fed minutes weigh ahead of Jackson Hole

Introduction & Market Context

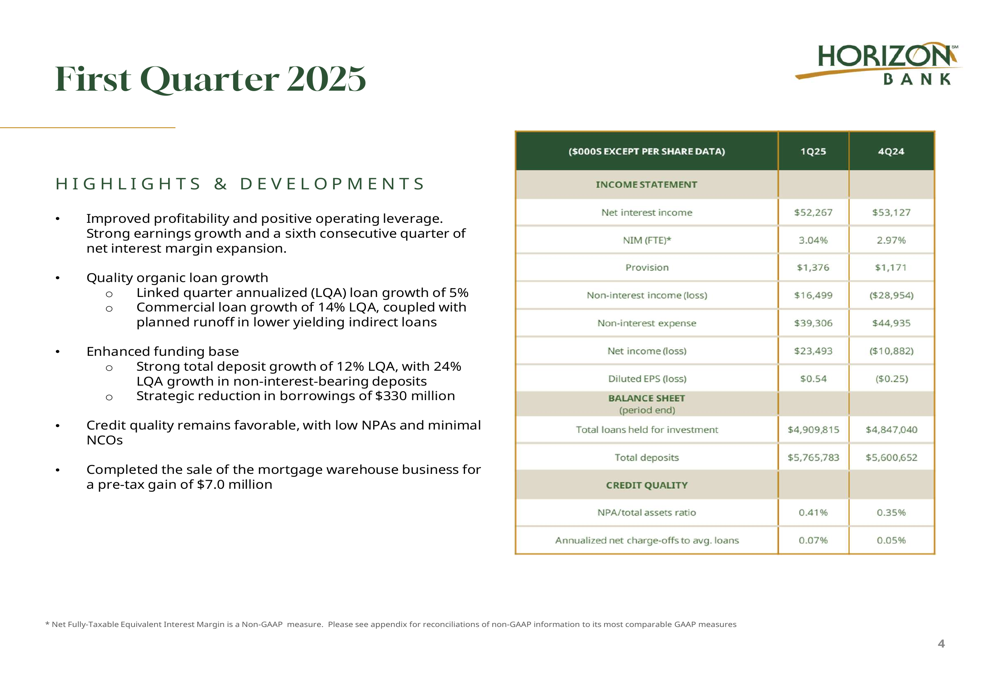

Horizon Bancorp (NASDAQ:HBNC) released its first quarter 2025 earnings presentation on April 24, showing a significant turnaround with a return to profitability after posting a loss in the previous quarter. The bank reported earnings per share of $0.54, a stark improvement from the $0.25 loss per share in Q4 2024.

Despite the positive results, Horizon’s stock was trading down 6.21% in premarket activity at $13.30, suggesting investors may have concerns about some aspects of the results or forward guidance.

Quarterly Performance Highlights

Horizon reported net income of $23.49 million for Q1 2025, compared to a loss of $10.88 million in Q4 2024. The quarter’s results were boosted by a $7.0 million pre-tax gain from the sale of the company’s mortgage warehouse business, a strategic move that had been previously announced.

Net interest income came in at $52.27 million, slightly down from $53.13 million in the previous quarter, while non-interest income improved dramatically to $16.50 million compared to a loss of $28.95 million in Q4 2024.

As shown in the following chart of quarterly highlights and key financial metrics:

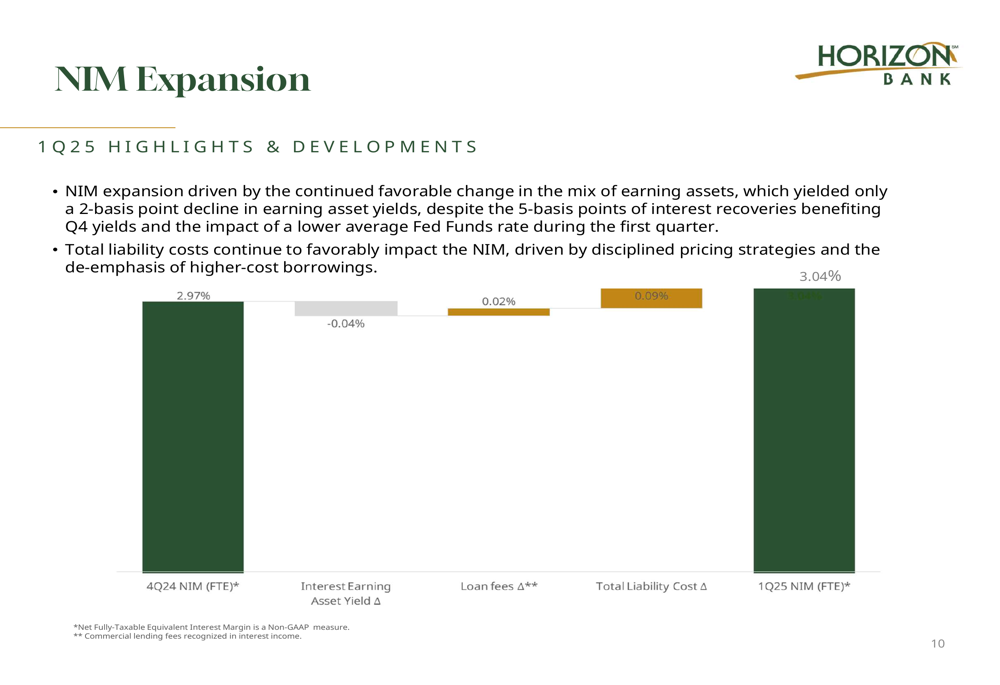

The bank’s net interest margin (NIM) expanded to 3.04% from 2.97% in the previous quarter, driven by favorable changes in earning asset mix and disciplined liability pricing. This improvement came despite ongoing industry challenges with funding costs.

Loan Portfolio Strategy

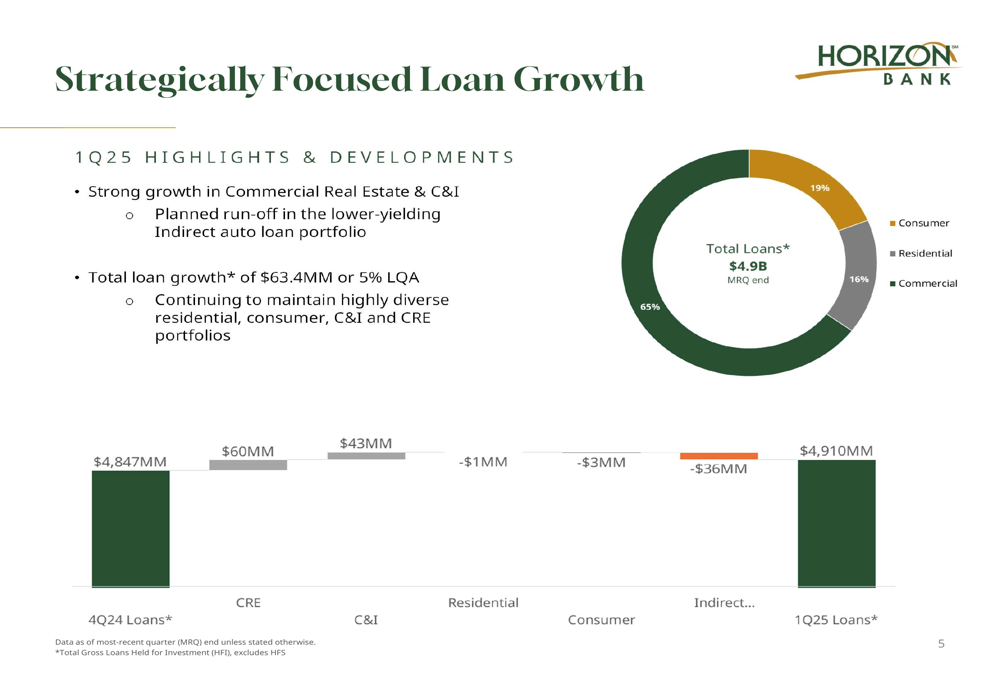

Horizon’s strategic focus on commercial lending is evident in its Q1 results, with total loans held for investment growing by $63.4 million or 5% on a linked quarter annualized basis. This growth was primarily driven by commercial real estate and C&I loans, which increased by $60 million and $43 million respectively, while the bank continued its planned reduction of lower-yielding indirect auto loans.

The company’s loan portfolio mix now stands at 65% commercial, 19% consumer, and 16% residential, highlighting its strategic shift toward higher-yielding commercial relationships.

The following chart illustrates Horizon’s loan growth strategy and portfolio composition:

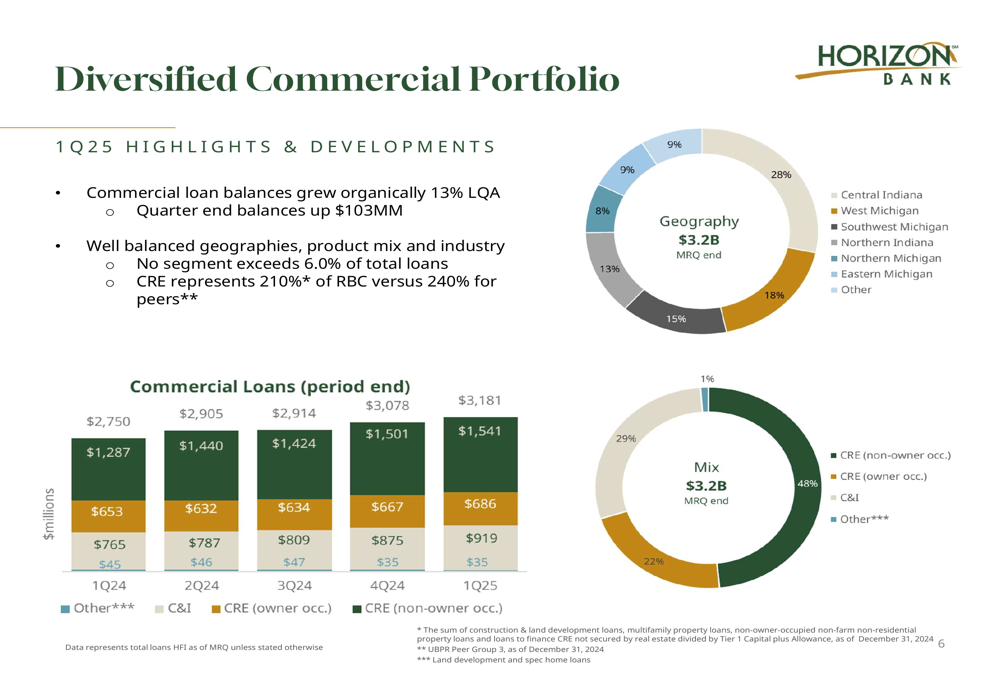

Commercial loan balances grew organically at a 13% annualized rate, with quarter-end balances up $103 million. The commercial portfolio is well-diversified across geographies and industries, with Central Indiana (28%), West Michigan (18%), and Southwest Michigan (15%) representing the largest regional concentrations.

The bank’s commercial mix is weighted toward CRE, with non-owner occupied at 48% and owner-occupied at 29%, while C&I loans make up 22% of the commercial portfolio.

Deposit and Funding Improvements

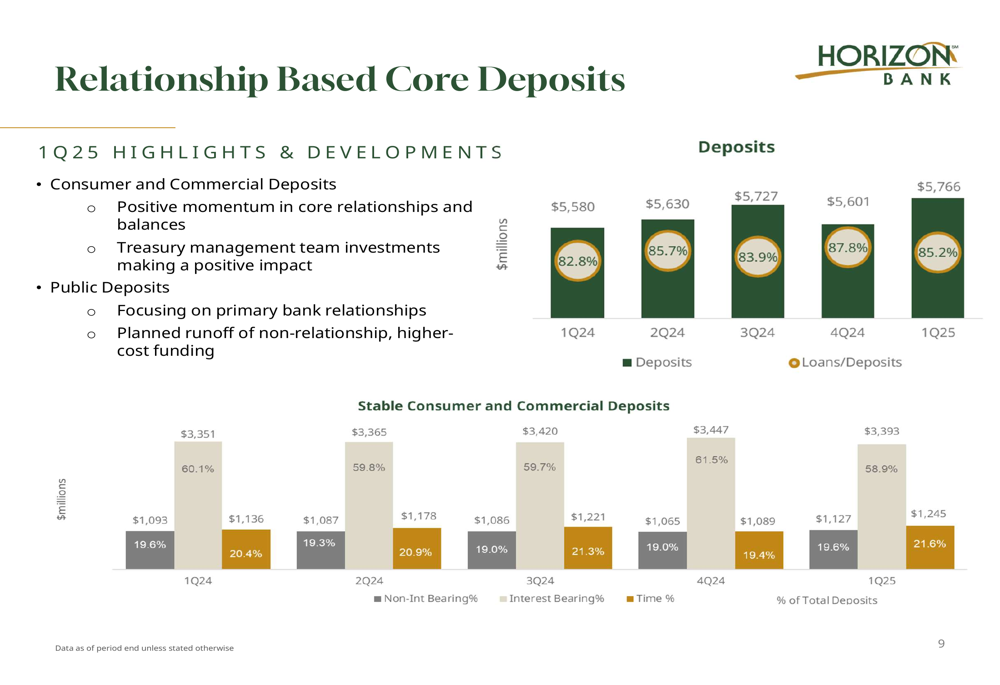

Horizon’s deposit base showed positive momentum in Q1 2025, with total deposits increasing to $5.77 billion from $5.60 billion in Q4 2024. This growth helped improve the loan-to-deposit ratio to 85.2% from 87.8% in the previous quarter, enhancing the bank’s liquidity position.

The company emphasized its focus on relationship-based core deposits, noting that its treasury management team investments are making a positive impact. The presentation highlighted the bank’s strategy of focusing on primary bank relationships while planning for runoff of non-relationship, higher-cost funding.

The following chart shows the trend in deposits and loan-to-deposit ratios:

Net interest margin expansion was a key highlight of the quarter, with the NIM increasing by 7 basis points to 3.04%. This improvement was primarily driven by disciplined pricing strategies and the de-emphasis of higher-cost borrowings, which contributed 9 basis points to the NIM expansion.

The drivers of NIM expansion are illustrated in this chart:

Capital Position and Asset Quality

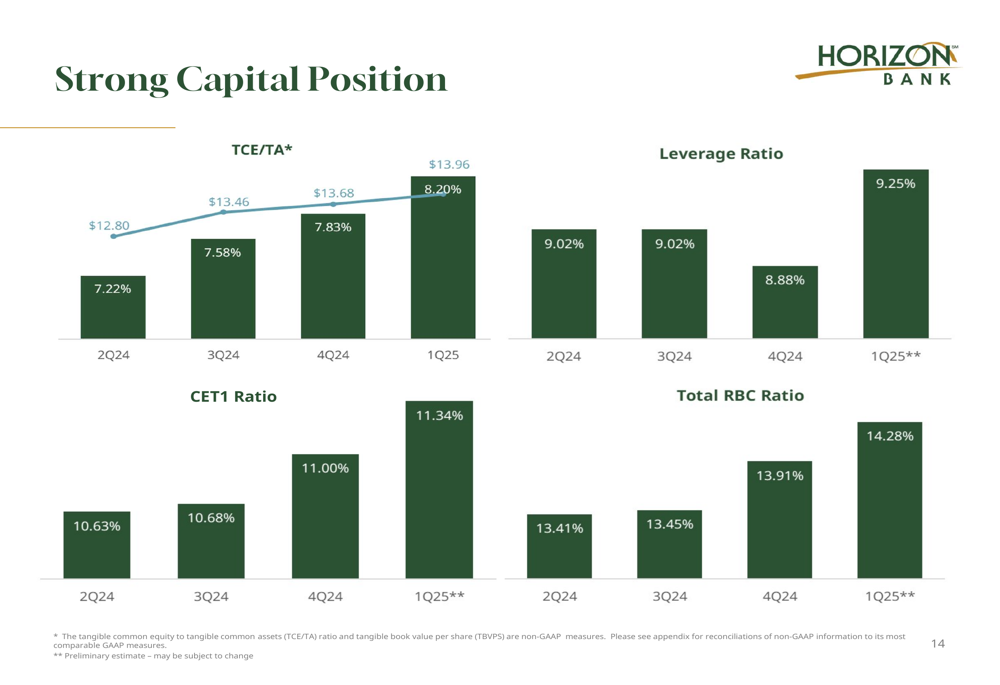

Horizon maintained strong capital ratios in Q1 2025, with the tangible common equity to tangible assets ratio improving to 8.20% from 7.83% in Q4 2024. The CET1 ratio increased to 11.34% from 11.00%, while the total risk-based capital ratio rose to 14.28% from 13.91%.

The following chart demonstrates Horizon’s strengthening capital position:

Asset quality metrics showed some modest deterioration, with non-performing loans increasing to $30.4 million (0.62% of total loans) from $27.0 million (0.56%) in Q4 2024. Net charge-offs remained low at 0.07% of average loans, up slightly from 0.05% in the previous quarter. The allowance for credit losses remained stable at 1.07% of total loans.

Forward Guidance and Outlook

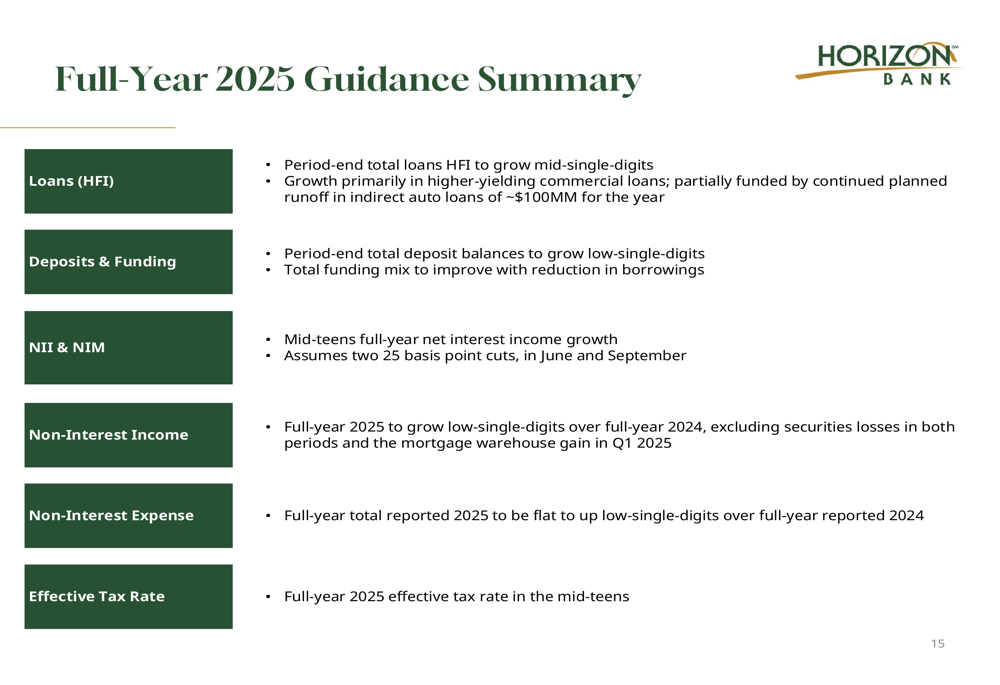

Looking ahead, Horizon provided optimistic guidance for full-year 2025, projecting mid-single-digit loan growth primarily in higher-yielding commercial loans, partially funded by continued planned runoff in indirect auto loans of approximately $100 million for the year.

The bank expects mid-teens full-year net interest income growth, assuming two 25 basis point rate cuts in June and September. Non-interest income is projected to grow at a low-single-digit rate over full-year 2024, excluding securities losses and the mortgage warehouse gain.

The comprehensive guidance for 2025 is outlined in this summary:

Management emphasized the bank’s focus on its core strengths, including its presence in attractive Midwestern markets, high-quality loan growth, tenured deposit base, and lean operating culture. These factors position Horizon to continue its recovery and growth trajectory throughout 2025.

This represents a significant turnaround from the challenges faced in Q3 2024, when the bank reported a substantial earnings miss that led to a stock decline. The Q1 2025 results suggest that management’s strategic initiatives, including the sale of the mortgage warehouse business and focus on commercial lending, are beginning to yield positive results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.