Crispr Therapeutics shares tumble after significant earnings miss

Howard Hughes Holdings Inc (NYSE:HHH) revealed a major strategic shift in its first quarter 2025 presentation, highlighting a transformative $900 million investment from Pershing Square that will reshape the company into a diversified holding company. The presentation, released on May 8, 2025, details strong performance across all segments and outlines the company’s evolving business model under returning Executive Chairman Bill Ackman.

Executive Summary

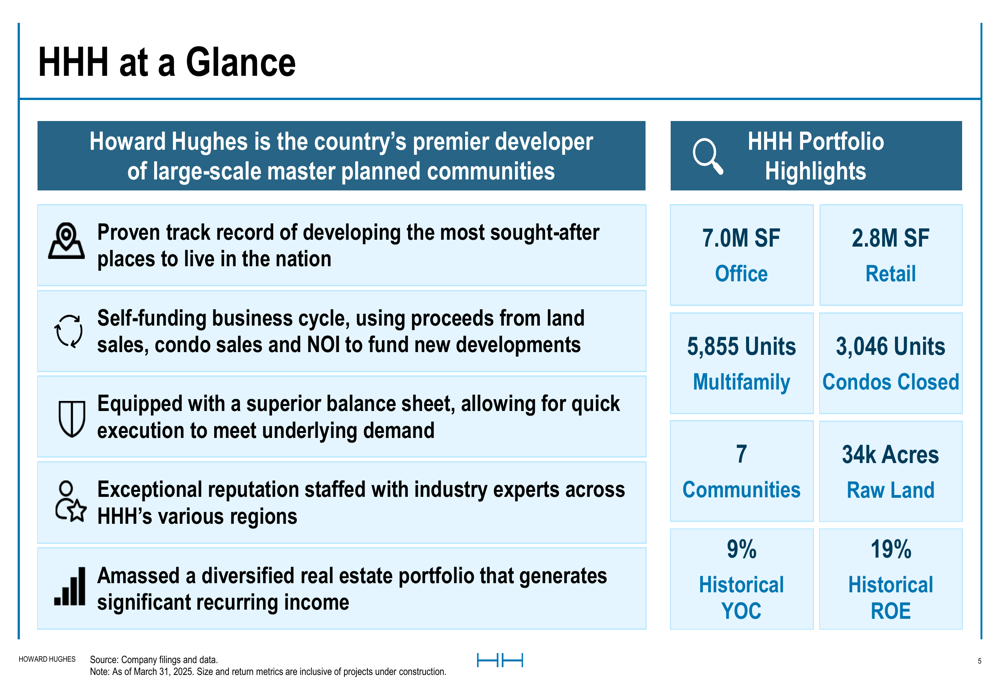

Howard Hughes reported robust financial performance across its three core segments. The company’s Master Planned Communities (MPC) segment generated $349 million in earnings before taxes (EBT) for 2024, while Strategic Developments delivered $211 million in Adjusted Condo Gross Profit. The Operating Assets segment produced $257 million in net operating income (NOI), with expectations to reach $353 million at stabilization.

The presentation follows HHH’s Q4 2024 earnings report, where the company posted revenue of $983.59 million, exceeding forecasts of $933.43 million, despite an EPS miss of $3.25 against expectations of $3.69. The company’s stock has shown resilience, trading at $68.70 as of the latest close.

As shown in the following comprehensive overview of HHH’s business model and portfolio:

Strategic Transformation

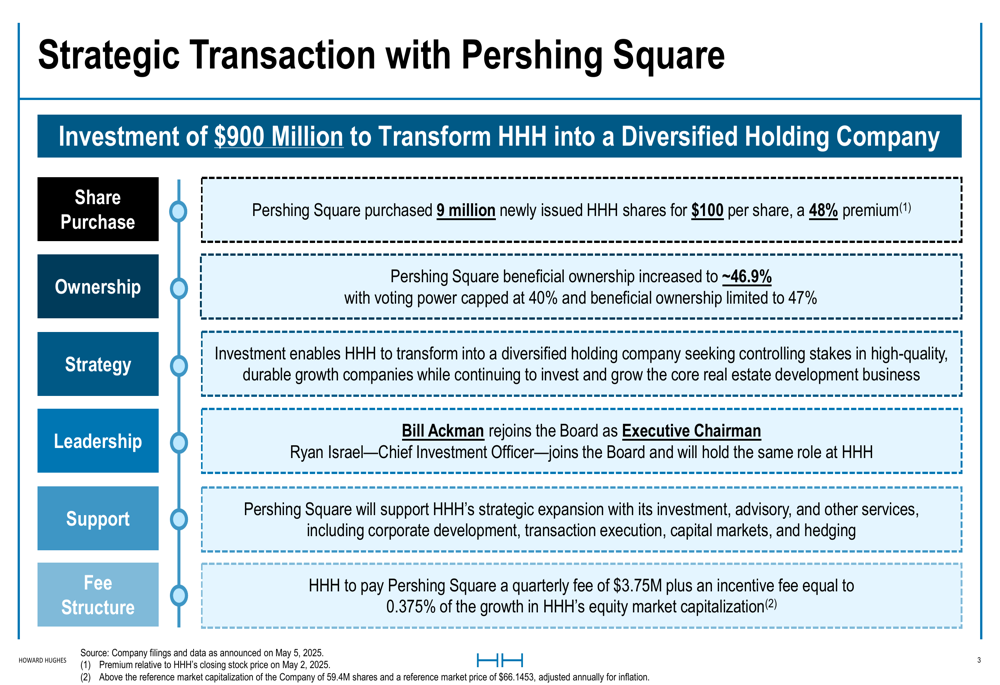

The most significant development highlighted in the presentation is Pershing Square’s $900 million investment, which has fundamentally altered HHH’s corporate structure and future direction. The transaction involved Pershing Square purchasing 9 million newly issued HHH shares at $100 per share—a substantial 48% premium to market price—increasing Pershing Square’s beneficial ownership to approximately 46.9% with voting power capped at 40%.

The investment brings Bill Ackman back to HHH as Executive Chairman, with Ryan Israel joining as Chief Investment Officer. The transaction establishes a new fee structure where HHH will pay Pershing Square a quarterly fee of $3.75 million plus an incentive fee.

The following slide details the key aspects of this transformative transaction:

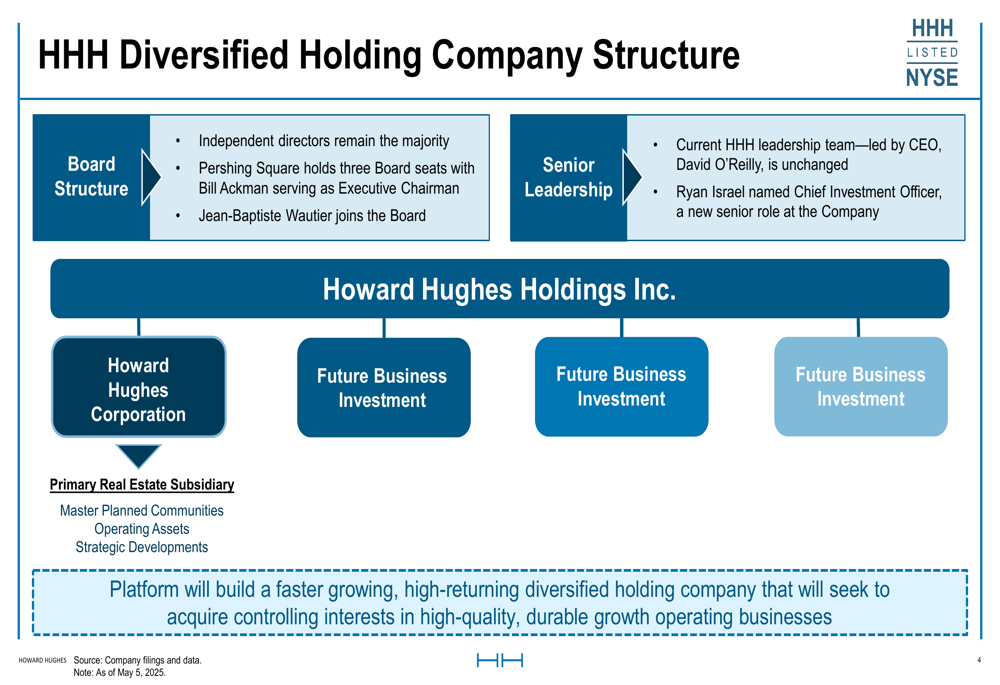

The reorganization creates a new holding company structure that maintains the existing Howard Hughes Corporation as a subsidiary focused on real estate operations while enabling the parent company to pursue broader investment opportunities:

Competitive Advantages and Business Model

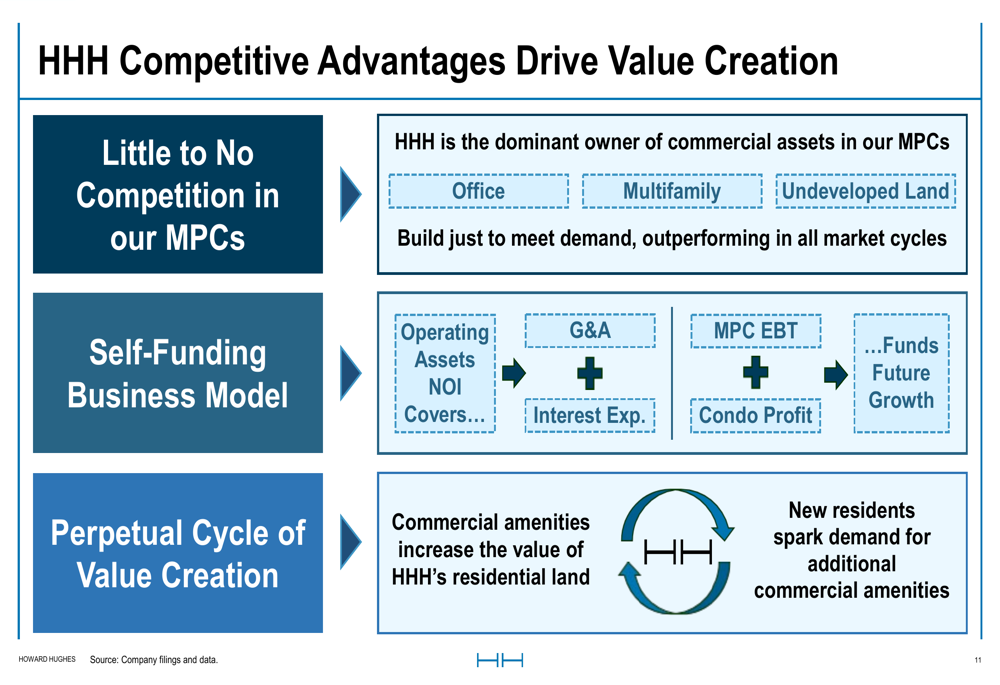

HHH’s presentation emphasizes its unique self-funding business model and competitive advantages in the master-planned community space. The company highlighted its position as the dominant owner of commercial assets within its MPCs, allowing it to build according to demand with minimal competition.

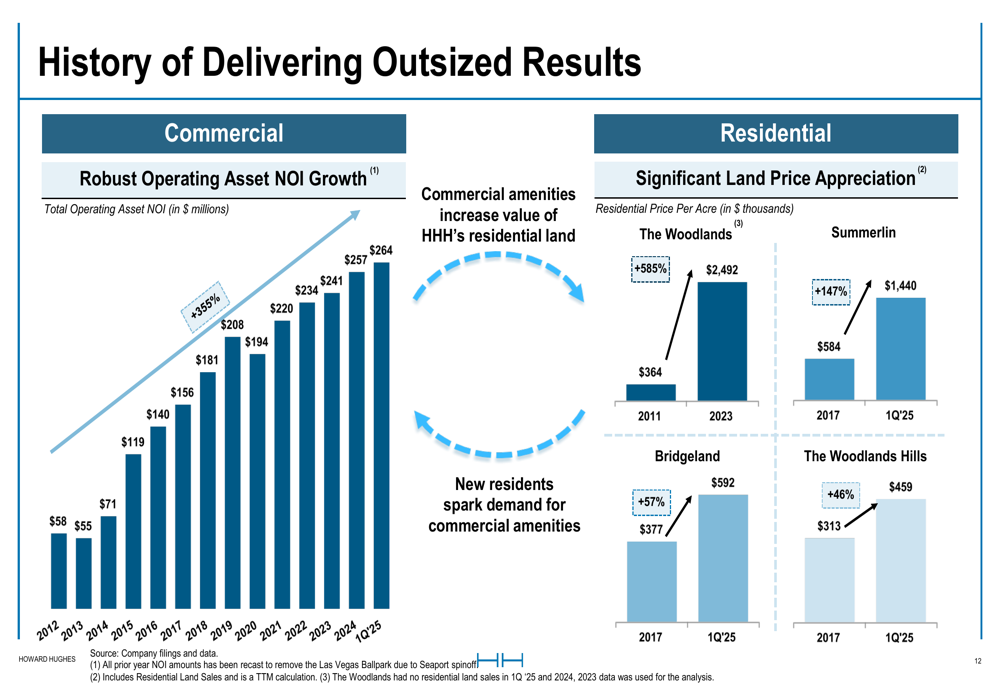

The company’s business model creates a perpetual cycle of value creation, where commercial amenities increase residential land values, and new residents drive demand for additional commercial development. Operating Assets NOI covers general and administrative expenses and interest expenses, while MPC earnings and condo profits fund future growth.

As illustrated in this key business model slide:

This model has delivered strong historical results, with significant land price appreciation across communities and substantial NOI growth from $55 million in 2012 to $264 million in 1Q 2025:

Financial Performance and Outlook

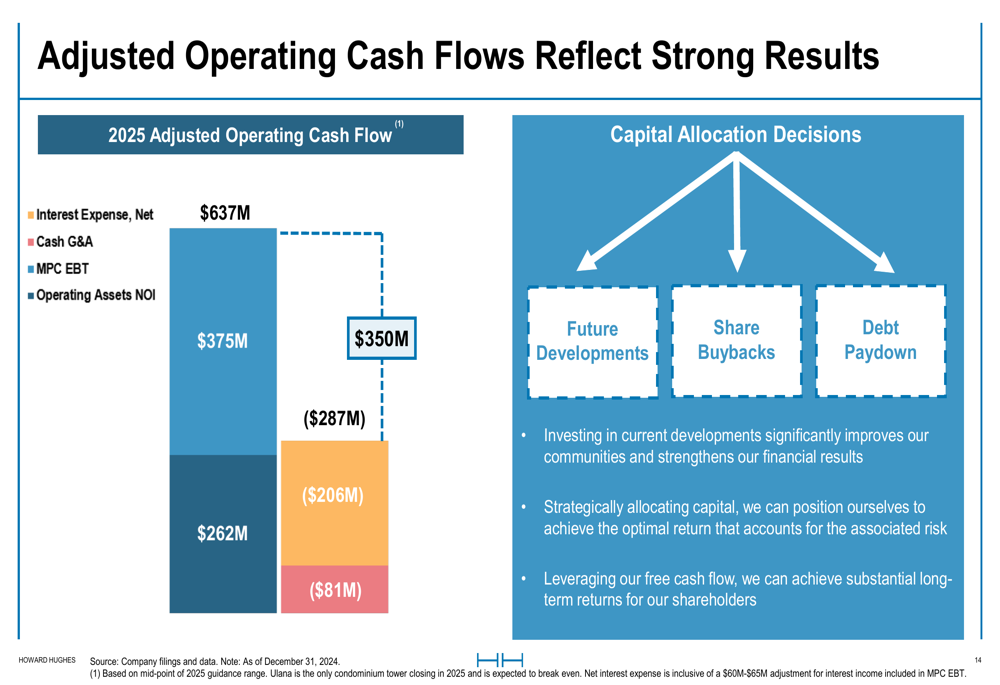

The presentation details HHH’s strong financial position, with 2025 Adjusted Operating Cash Flow showing positive contributions from MPC EBT ($350M) and Operating Assets NOI ($637M), offset by Interest Expense ($81M) and Cash G&A ($206M):

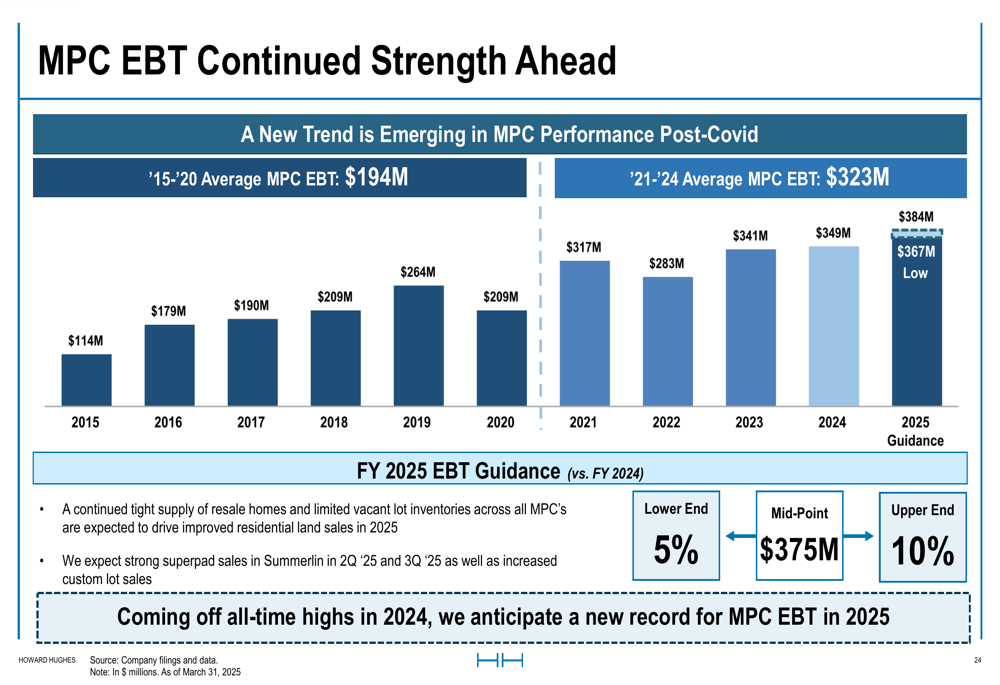

The company’s MPC segment continues to show strength, with guidance for 2025 projecting 5-10% growth from 2024 levels, targeting a mid-point of $375 million:

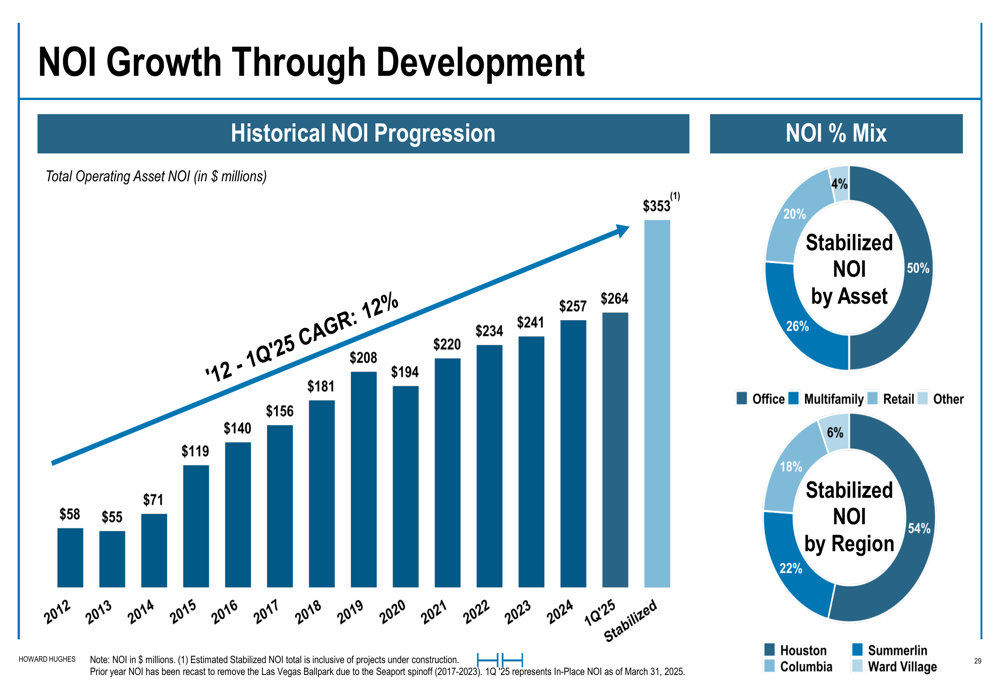

HHH’s commercial real estate portfolio is diversified across office, multifamily, and retail assets, with $264 million of in-place NOI expected to grow to $353 million at stabilization:

The company has demonstrated consistent NOI growth through development, with a clear trajectory toward higher stabilized NOI:

Segment Performance

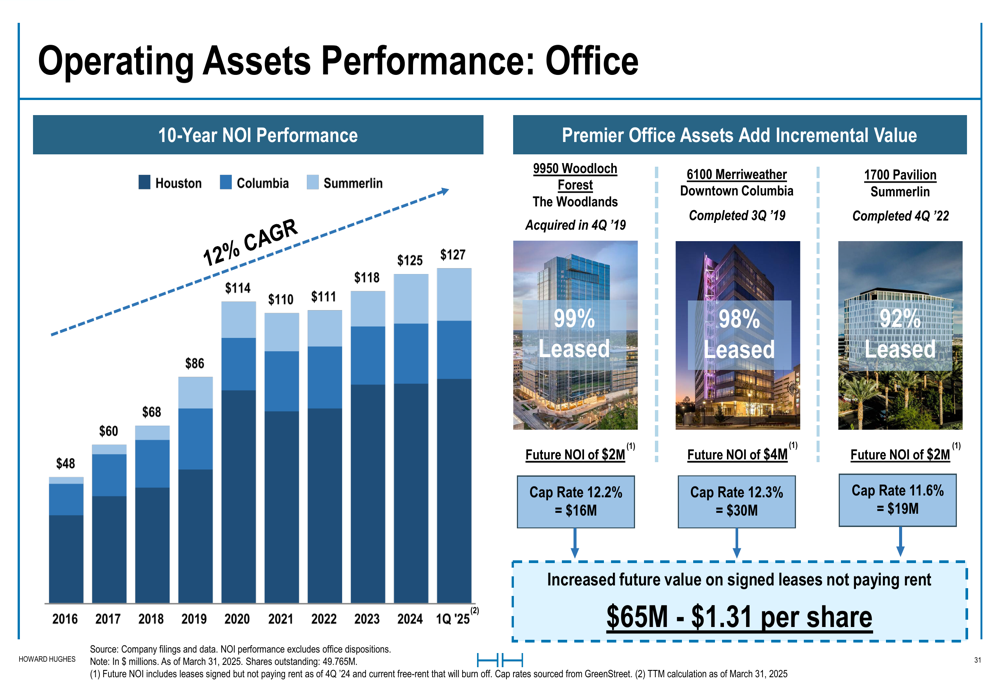

The presentation provides detailed breakdowns of each operating segment’s performance. The Office portfolio, comprising 7.0 million square feet with an 88% stabilized leased percentage, shows strong 10-year NOI performance and highlights premier assets adding incremental value:

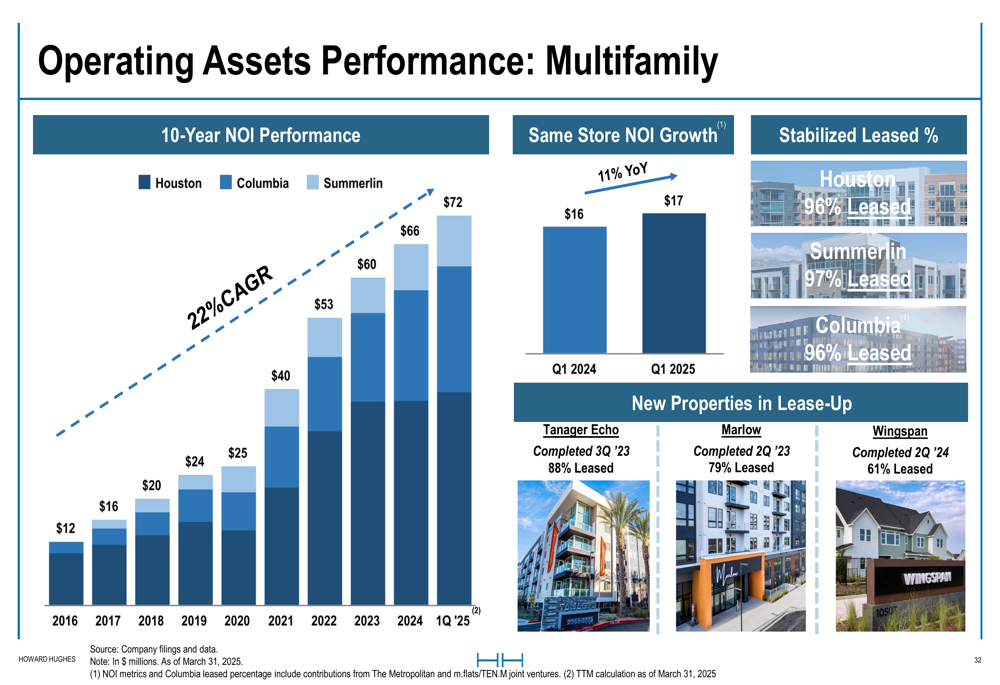

The Multifamily portfolio, with 5,855 units and a 96% stabilized leased percentage, demonstrates robust same-store NOI growth of 11% year-over-year:

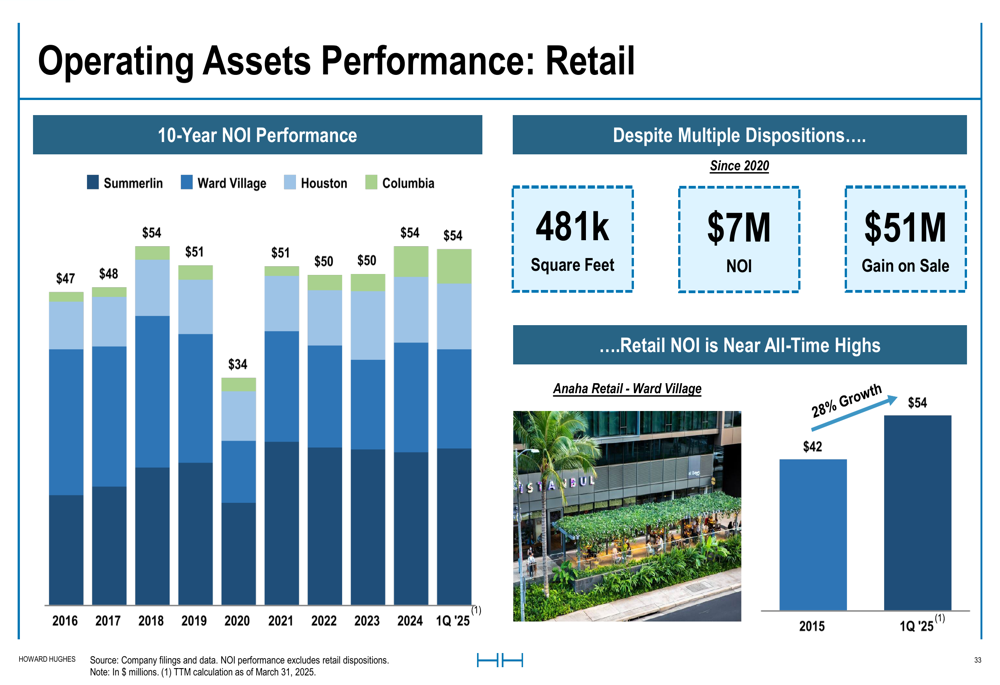

The Retail segment, encompassing 2.8 million square feet with a 96% stabilized leased percentage, has maintained strong NOI performance despite multiple dispositions:

The company has achieved transformational leasing success across several premier office assets:

Market Position and Future Development

HHH’s presentation emphasizes its strategic positioning in low-cost, low-tax, pro-business regions including Houston, Las Vegas, and Phoenix. The company’s master-planned communities consistently receive recognition and awards, with superior demographics compared to surrounding metropolitan areas.

The company holds approximately 34,000 acres for future development, providing a substantial runway for growth. This land bank, combined with the company’s self-funding business model and strong balance sheet (94% of debt fixed or swapped/capped, with 81% due in 2027 or later), positions HHH for continued expansion.

In the Ward Village condo development, HHH projects total revenue of $6.3 billion with gross profit margins of 25-30%, demonstrating the potential of its development pipeline.

Forward-Looking Statements

Looking ahead, HHH projects continued growth across all segments for 2025. The company’s guidance includes 5-10% growth in MPC EBT, targeting $375 million, and Operating Asset NOI reaching $262 million. The transformation into a diversified holding company under Pershing Square’s influence represents a significant strategic shift that could expand HHH’s investment horizons beyond its traditional real estate focus.

This strategic evolution comes at a time when HHH has demonstrated strong operational performance, as evidenced by its Q4 2024 revenue beat and positive market reception. The company’s presentation suggests confidence in its ability to leverage its strong real estate foundation while pursuing new growth opportunities under its revised corporate structure.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.