Robinhood shares gain on Q2 beat, as user and crypto growth accelerate

Hubbell Inc (NYSE:HUBB) shares declined 2.58% in premarket trading despite reporting double-digit earnings growth and raising its full-year outlook during its second quarter 2025 earnings presentation on July 29. The electrical and power components manufacturer delivered 11% growth in adjusted earnings per share, driven by strong datacenter demand and robust grid infrastructure performance.

Quarterly Performance Highlights

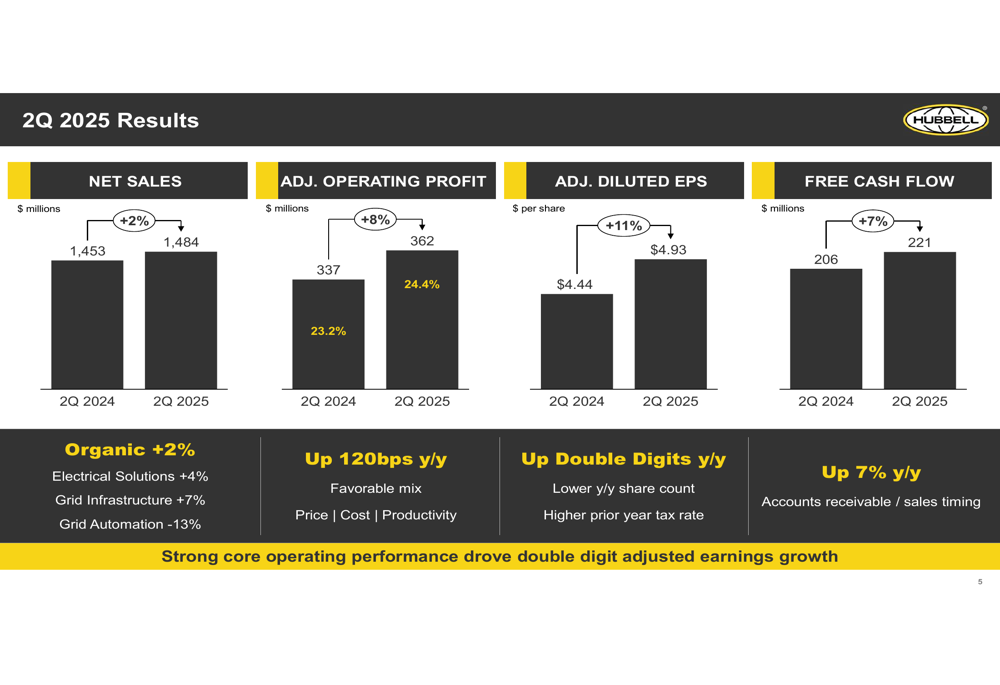

Hubbell reported solid financial results for the second quarter of 2025, with adjusted earnings per share growing 11% year-over-year to $4.93, exceeding the $4.44 reported in Q2 2024. This represents a significant improvement from Q1 2025, when the company missed earnings expectations with an EPS of $3.50 against a forecast of $3.72.

Net sales increased 2% to $1.48 billion, while adjusted operating profit rose 8% to $362 million. Free cash flow generation remained strong at $221 million, up 7% from the prior year.

As shown in the following chart of quarterly financial performance:

The company’s organic growth of 2% was driven by a mixed performance across segments, with Electrical Solutions growing 4% and Grid Infrastructure increasing 7%, partially offset by a 13% decline in Grid Automation. Favorable mix contributed 120 basis points to year-over-year margin improvement.

Segment Analysis

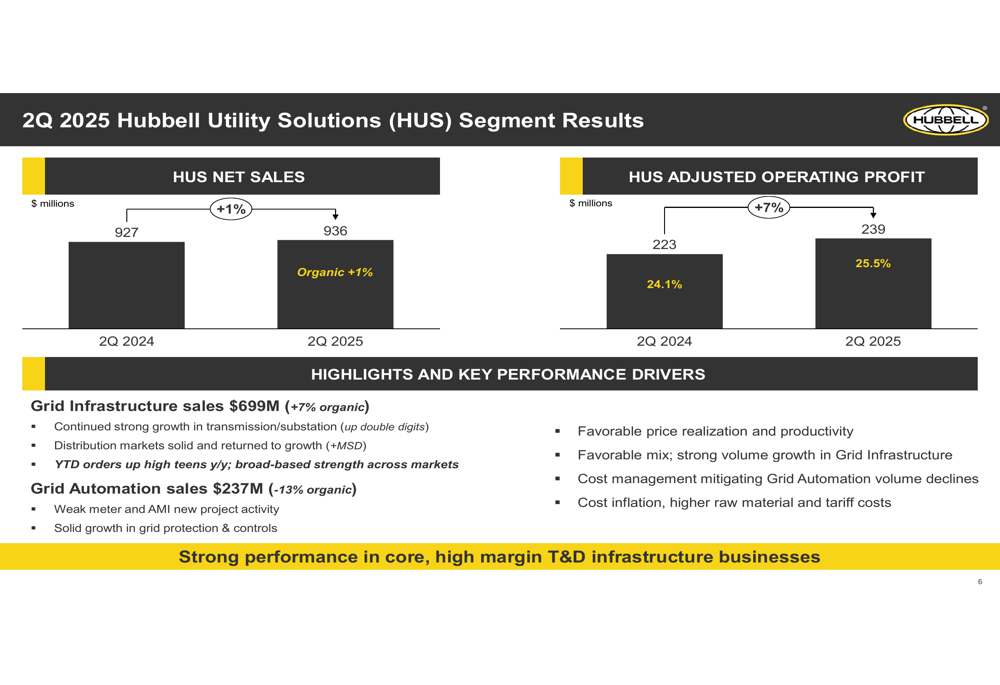

Hubbell’s Utility Solutions (HUS) segment, which represents approximately 63% of total sales, reported a modest 1% increase in net sales to $936 million. However, adjusted operating profit for this segment grew 7% to $239 million, resulting in an operating margin of 25.5%.

The following chart illustrates the HUS segment performance:

Within the HUS segment, Grid Infrastructure sales reached $699 million, representing 7% organic growth, with distribution markets returning to growth at mid-single digits. Year-to-date orders showed impressive growth, up high teens year-over-year with broad-based strength across markets. However, Grid Automation sales declined 13% organically to $237 million.

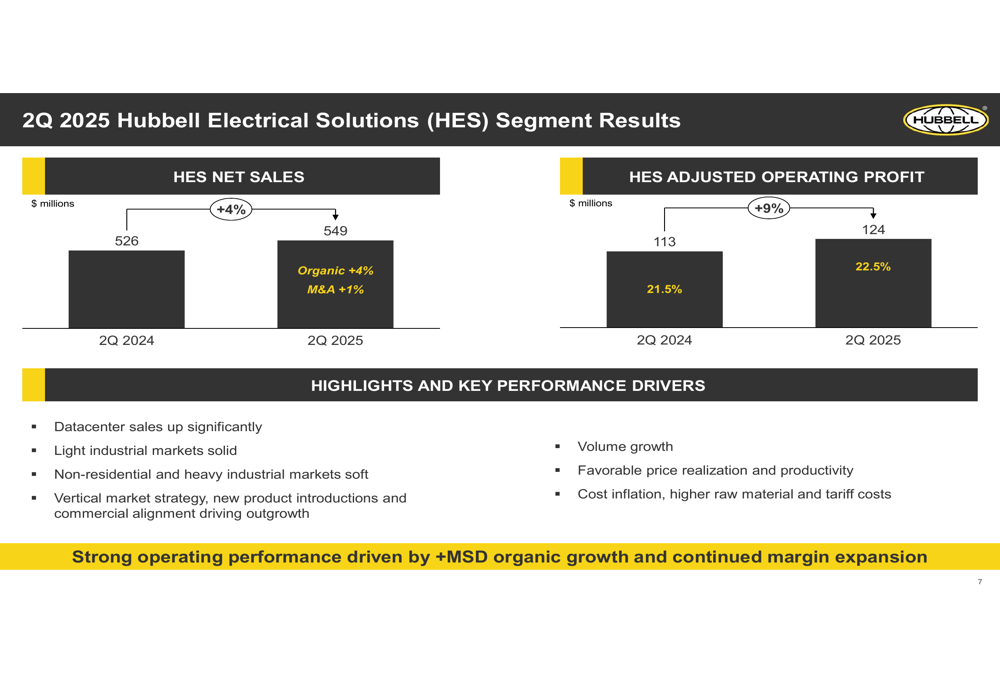

The Electrical Solutions (HES) segment delivered stronger performance, with net sales increasing 4% to $549 million and adjusted operating profit rising 9% to $124 million. The segment achieved an operating margin of 22.5%.

The HES segment results are illustrated in the following chart:

Management highlighted that datacenter sales increased significantly during the quarter, driving the segment’s overall growth. Favorable price realization and productivity gains helped offset cost inflation.

Accounting Change Impact

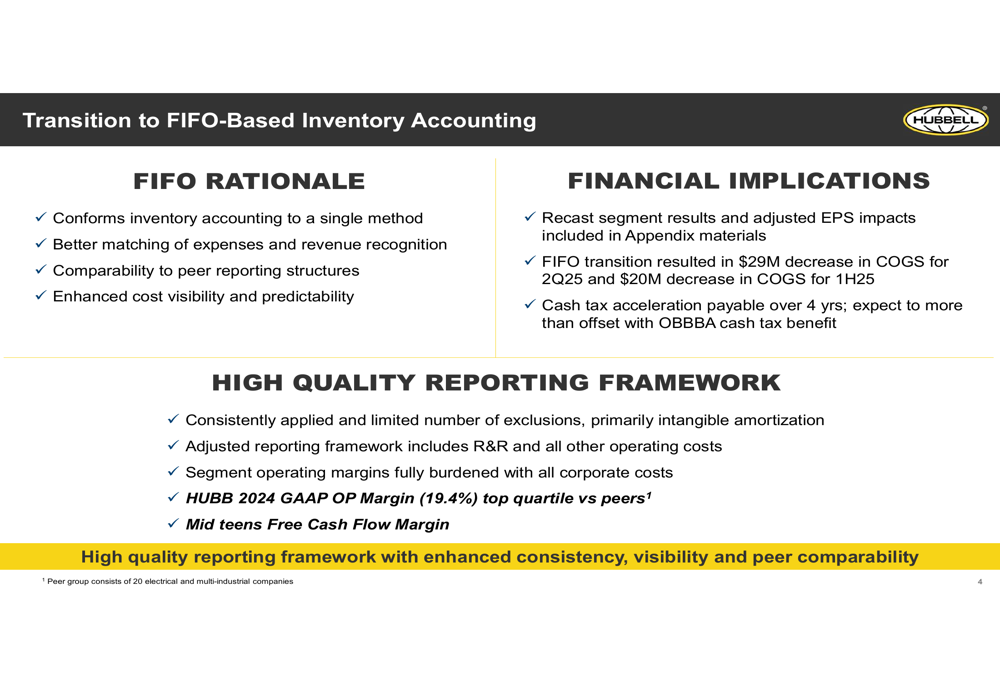

A significant development announced during the presentation was Hubbell’s transition to FIFO (First-In, First-Out) inventory accounting. This change is expected to provide better matching of expenses and revenue, enhance cost visibility, and improve comparability with industry peers.

The financial implications of this transition include a $29 million decrease in cost of goods sold for Q2 2025 and a $20 million decrease for the first half of 2025. The company noted that this change will result in cash tax acceleration payable over four years.

The following slide details the rationale and impact of the accounting change:

Management emphasized that Hubbell’s operating margin of 19.4% places it in the top quartile compared to industry peers, reflecting the company’s strong operational execution.

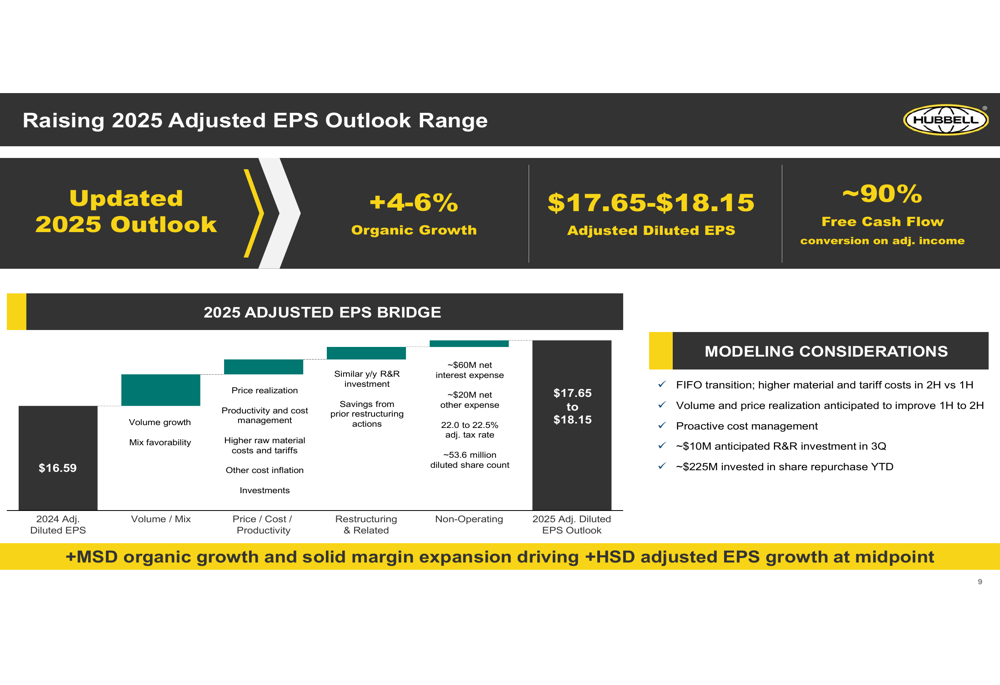

Updated Outlook & Guidance

Based on the strong first-half performance, Hubbell raised its full-year 2025 adjusted earnings per share outlook to a range of $17.65-$18.15, representing significant growth from the $16.59 reported in 2024.

The company anticipates organic growth of 4-6% for the full year, with Grid Infrastructure expected to deliver high single-digit growth, while Grid Automation is projected to decline at a high single-digit rate. The Electrical Solutions segment is expected to benefit from continued strength in datacenter markets, while T&D and light industrial markets remain solid.

The updated guidance is illustrated in the following bridge chart:

Management expects second-half market conditions to remain similar to the first half, with free cash flow conversion of approximately 90% for the full year.

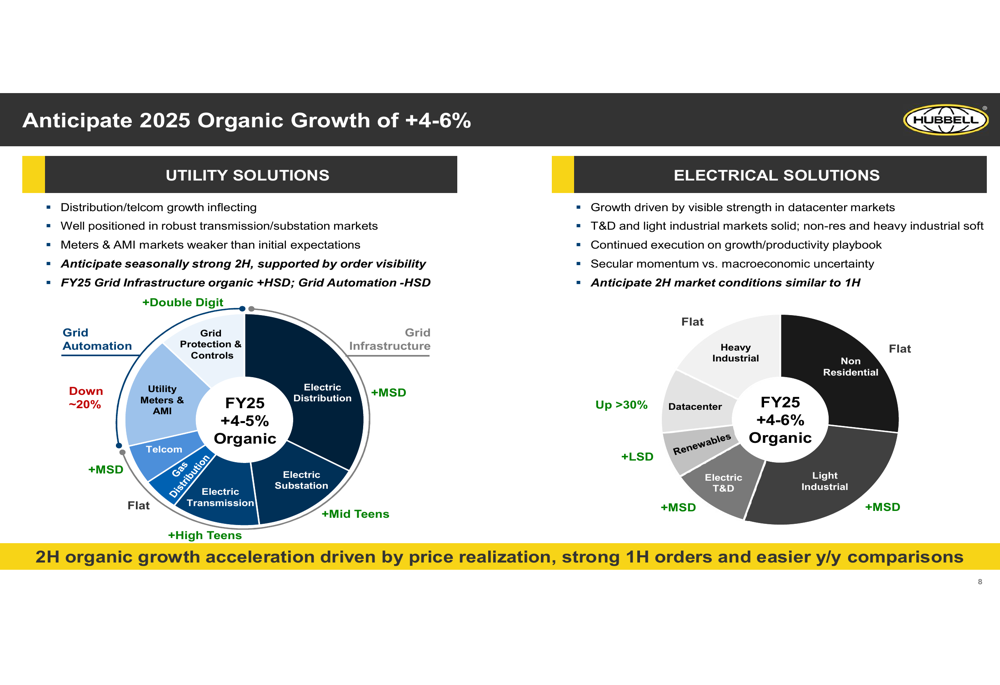

Strategic Positioning and Market Outlook

Hubbell highlighted its strong positioning in transmission and substation markets, which are showing robust growth. The company’s datacenter exposure continues to drive significant growth in the Electrical Solutions segment, offsetting softness in non-residential and heavy industrial markets.

The following slide outlines the company’s growth expectations across different market segments:

Despite the positive earnings report and raised outlook, investors appeared cautious, as indicated by the premarket stock decline of 2.58% to $427.00. This reaction follows a challenging first quarter where Hubbell missed both earnings and revenue expectations, resulting in a 3.35% stock drop at that time.

The company’s ability to deliver on its raised guidance will likely depend on continued strength in datacenter markets and the anticipated recovery in Grid Infrastructure, while managing ongoing cost inflation through pricing and productivity initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.