Gold prices bounce off 3-week lows; demand likely longer term

Executive Summary

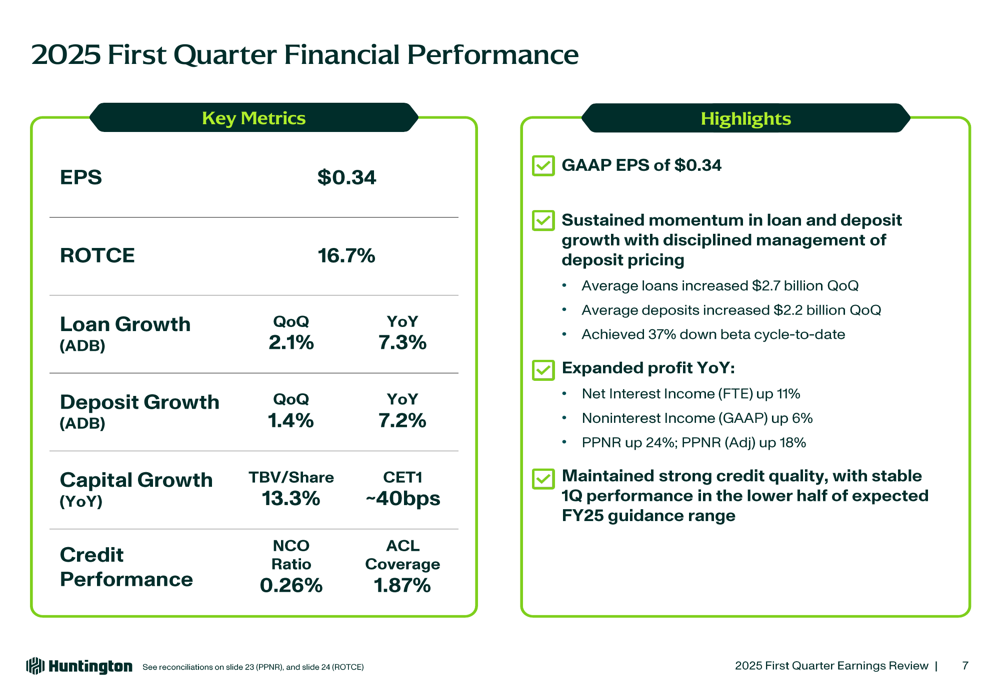

Huntington Bancshares (NASDAQ:HBAN) reported strong first quarter 2025 results on April 17, showcasing accelerated loan and deposit growth alongside expanded margins and robust profitability. The bank delivered earnings per share of $0.34 and a return on tangible common equity (ROTCE) of 16.7%, continuing the positive momentum seen in previous quarters.

The presentation highlighted Huntington’s success in executing its organic growth strategies, with year-over-year loan growth of 7.3% and deposit growth of 7.2%. The bank’s net interest margin expanded to 3.10%, up from 3.01% in the same quarter last year, contributing to a 10.8% increase in net interest income.

As shown in the following comprehensive overview of the quarter’s financial performance, Huntington achieved solid results across multiple metrics:

Quarterly Performance Highlights

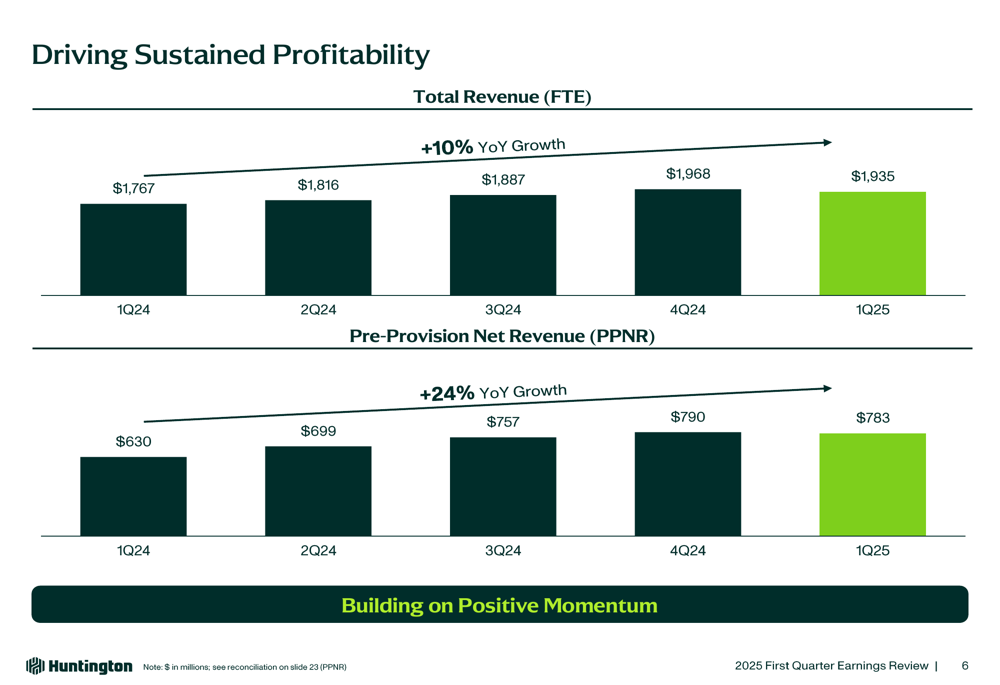

Huntington’s first quarter 2025 results demonstrated strong performance across key financial indicators. Total (EPA:TTEF) revenue (FTE) reached $1.935 billion, representing a 10% increase from the first quarter of 2024. Pre-provision net revenue (PPNR) showed even stronger growth at 24% year-over-year, reaching $783 million for the quarter.

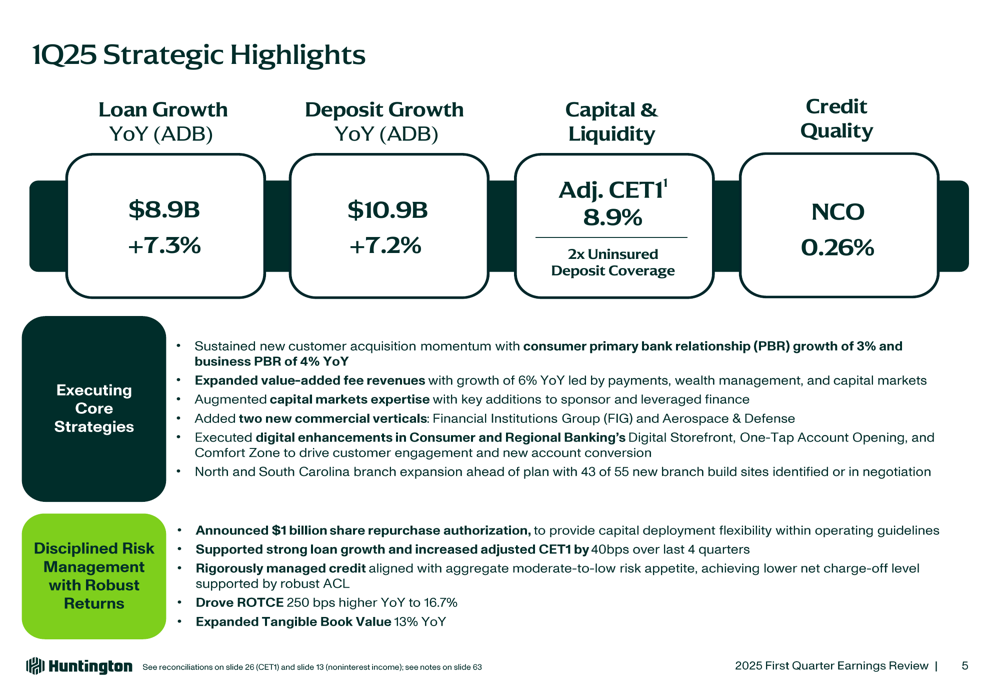

The bank’s strategic highlights for the quarter emphasize the balanced growth across both loans and deposits, with strong capital and credit metrics:

Net interest income continued its upward trajectory, reaching $1.441 billion in Q1 2025, a 10.8% increase compared to Q1 2024. This growth was supported by net interest margin expansion to 3.10%, up 9 basis points year-over-year. The improvement in NIM reflects the bank’s effective balance sheet management and the benefits of its hedging program.

The sustained profitability trends are clearly visible in the bank’s revenue and PPNR performance over the past five quarters:

Strategic Initiatives

Huntington’s presentation emphasized its strategic focus on diversifying fee revenue streams, with particular attention to payments, wealth management, and capital markets. These three areas represent 64% of the bank’s adjusted non-interest income, providing a balanced approach to fee generation.

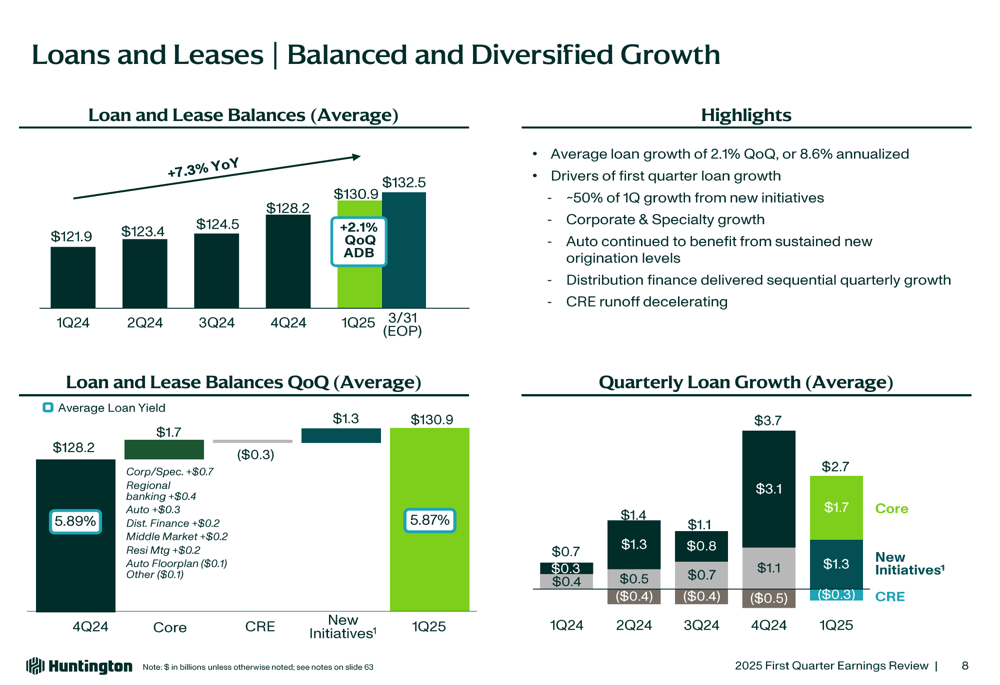

The bank’s loan portfolio showed continued growth and diversification. Average loan and lease balances increased to $130.9 billion in Q1 2025, up from $121.9 billion in Q1 2024, representing a 7.3% year-over-year increase. The quarter-over-quarter growth of 2.1% indicates accelerating momentum in lending activities.

The following chart illustrates the consistent growth in the bank’s loan portfolio:

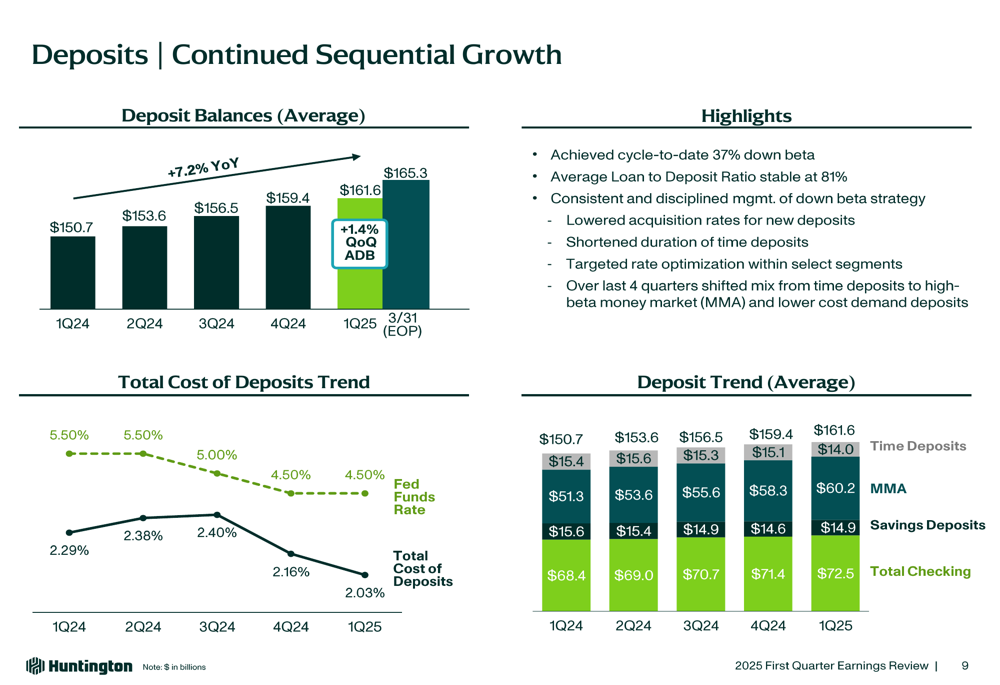

Similarly, deposit growth remained strong, with average deposit balances reaching $161.6 billion in Q1 2025, a 7.2% increase from $150.7 billion in Q1 2024. The bank’s ability to continue growing deposits while managing deposit costs effectively has been a key strength.

The deposit trends demonstrate Huntington’s success in attracting and retaining customer funds:

Credit Quality and Capital Position

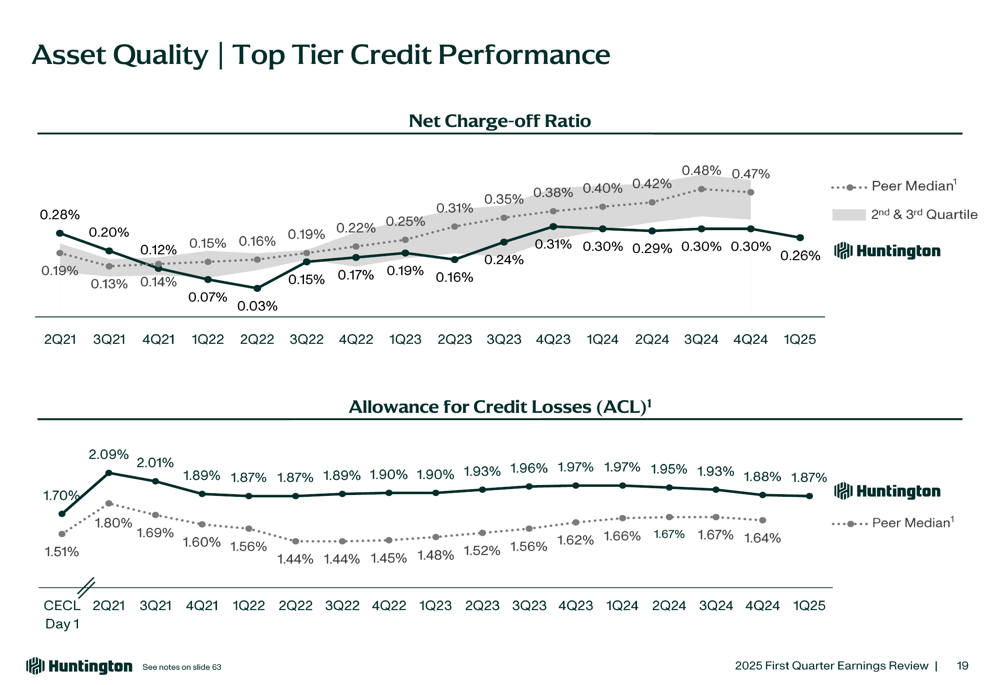

Huntington maintained strong credit performance in the first quarter, with a net charge-off ratio of 0.26% and allowance for credit losses coverage of 1.87%. These metrics reflect the bank’s disciplined approach to credit risk management and its focus on high-quality lending.

The bank’s capital position continued to strengthen, with tangible book value per share growing 13.3% year-over-year and the CET1 ratio improving by approximately 40 basis points. This robust capital generation provides flexibility for future growth opportunities while maintaining a strong buffer against potential economic uncertainties.

Asset quality metrics remained at top-tier levels, as shown in the following chart:

2025 Outlook

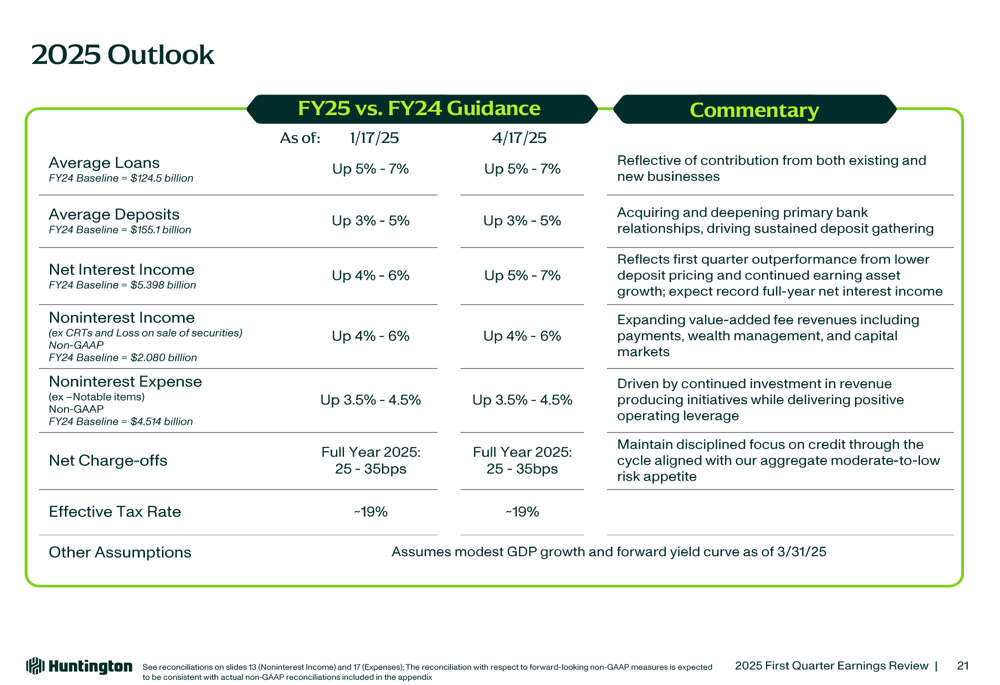

Looking ahead, Huntington provided a positive outlook for 2025, projecting continued growth across key financial metrics. The bank expects average loans to increase by 5-7% from the 2024 baseline of $124.5 billion, and average deposits to grow by 3-5% from $155.1 billion.

Net interest income is projected to rise by 4-6% from the 2024 baseline of $5.398 billion, while noninterest income is expected to increase by 4-6% from $2.080 billion. The bank anticipates noninterest expense growth of 3.5-4.5% from $4.514 billion, demonstrating its commitment to disciplined expense management while investing in growth initiatives.

The detailed 2025 outlook is presented in the following slide:

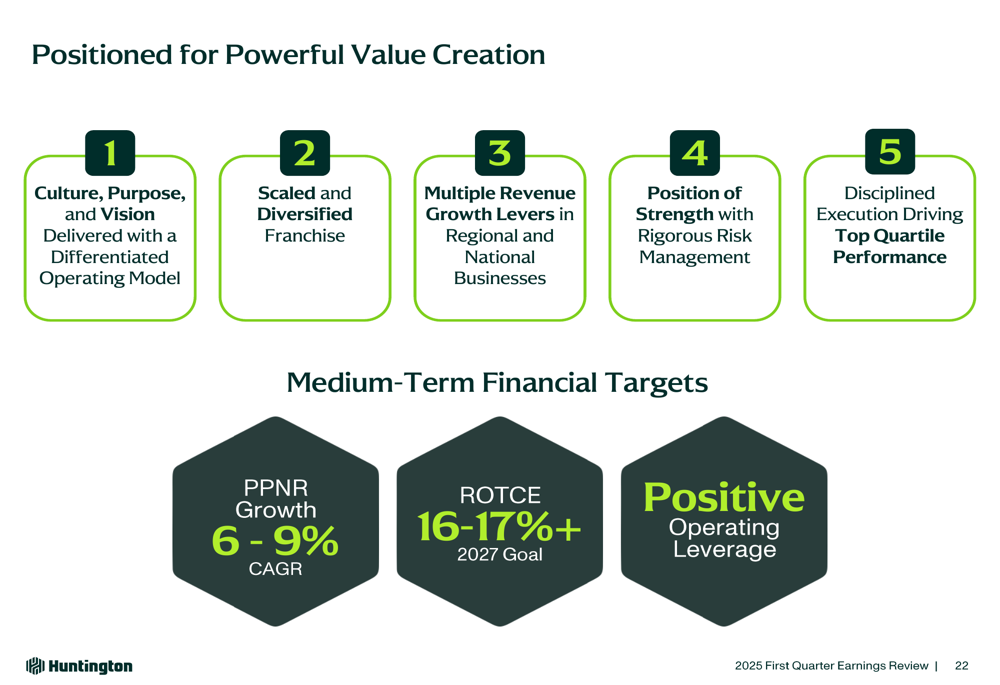

Huntington’s medium-term financial targets include PPNR growth of 6-9% CAGR, ROTCE of 16-17%+, and positive operating leverage. These targets reflect the bank’s confidence in its strategic positioning and ability to deliver sustained value creation.

The bank’s vision and value creation strategy is summarized in this slide:

Market Context

Huntington’s Q1 2025 results build upon the momentum reported in its Q3 2024 earnings. The bank has successfully accelerated loan growth from 3.1% year-over-year in Q3 2024 to 7.3% in Q1 2025. Similarly, ROTCE has improved from 16.2% to 16.7%, indicating enhanced profitability.

The bank’s performance comes amid a changing interest rate environment, with the Federal Reserve having begun its rate-cutting cycle. Huntington appears well-positioned to navigate this transition, with its net interest margin expanding despite the rate cuts, supported by its balance sheet hedging program and disciplined deposit pricing strategy.

Huntington’s stock closed at $13.27 on April 16, 2025, down 0.97% for the day. The shares have traded in a 52-week range of $11.92 to $18.45, suggesting potential upside if the bank continues to deliver on its growth and profitability targets.

Conclusion

Huntington Bancshares delivered a strong first quarter 2025, characterized by accelerated loan and deposit growth, expanded margins, and robust profitability. The bank’s strategic focus on diversified revenue streams, disciplined expense management, and strong credit quality positions it well for continued success throughout 2025.

With a clear outlook for growth across key financial metrics and medium-term targets for enhanced profitability, Huntington appears to be executing effectively on its vision to be "the Leading People-First, Customer-Centered Bank in the Country." Investors will likely be watching closely to see if the bank can maintain this momentum in the face of changing economic conditions and competitive pressures in the banking industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.