U.S. futures subdued as government shutdown stretches into second week

Introduction & Market Context

Huntsman Corporation (NYSE:HUN) presented its first quarter 2025 earnings results on May 2, 2025, revealing a mixed performance amid persistent market challenges. The chemical manufacturer reported improved net loss figures compared to the same period last year, but faced declining revenues and adjusted EBITDA as global economic uncertainties and tariff concerns weighed on customer demand.

The company’s stock closed at $13.31 on May 1, 2025, with after-hours trading showing a 2.02% decline to $13.10, suggesting investors’ cautious reaction to the results. This follows a period of volatility for Huntsman, which had seen its stock rise 6.18% after Q4 2024 results despite an earnings miss.

Quarterly Performance Highlights

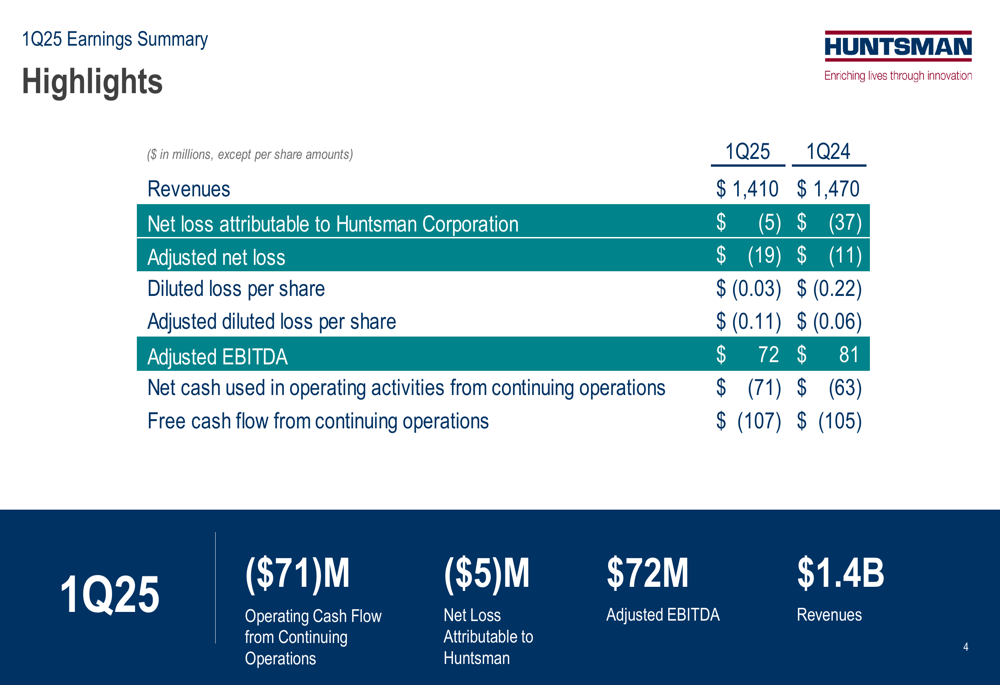

Huntsman reported Q1 2025 revenues of $1,410 million, down 4.1% from $1,470 million in Q1 2024. The company narrowed its net loss to $5 million from $37 million in the prior-year period, while diluted loss per share improved to $(0.03) compared to $(0.22) a year ago.

However, adjusted metrics showed a different trend, with adjusted net loss worsening to $(19) million from $(11) million in Q1 2024, and adjusted diluted loss per share increasing to $(0.11) from $(0.06). Adjusted EBITDA declined 11.1% to $72 million from $81 million in the comparable period.

As shown in the following financial highlights from the presentation:

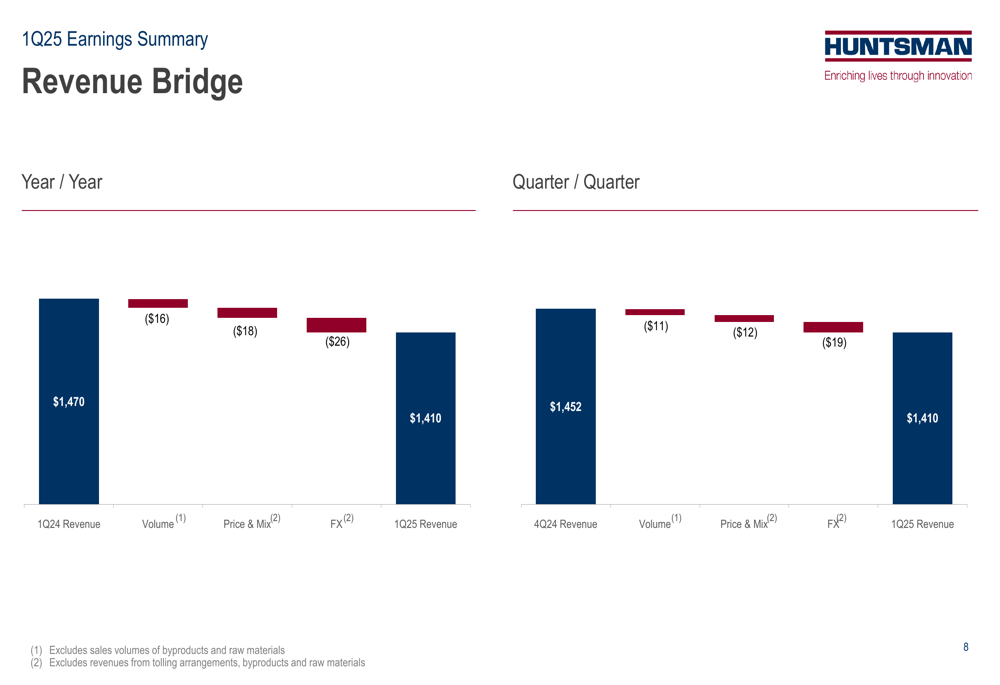

The revenue bridge analysis reveals that the year-over-year decline was driven by multiple factors: $16 million decrease due to lower volumes, $18 million reduction from price and mix effects, and a $26 million negative impact from foreign exchange movements.

Segment Analysis

Huntsman’s three main business segments showed divergent performance in Q1 2025:

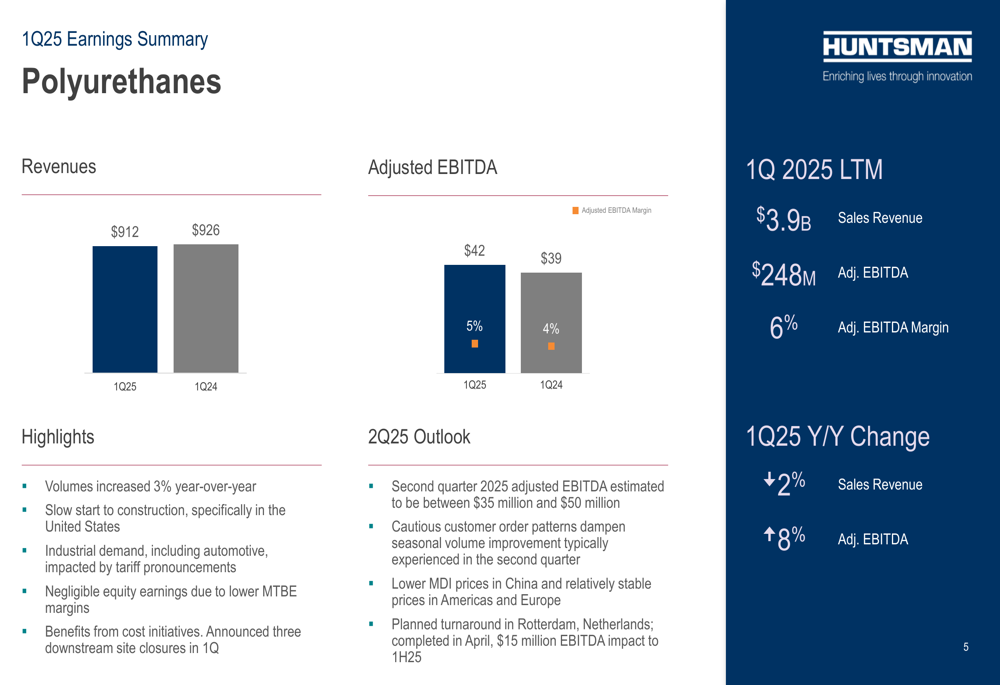

The Polyurethanes segment, the company’s largest division, reported revenues of $912 million, slightly down from $926 million in Q1 2024. However, adjusted EBITDA improved to $42 million from $39 million, with margins expanding to 5% from 4%. The segment benefited from increased volumes year-over-year, though faced challenges from a slow start to construction in the US and impact from tariff pronouncements on industrial demand.

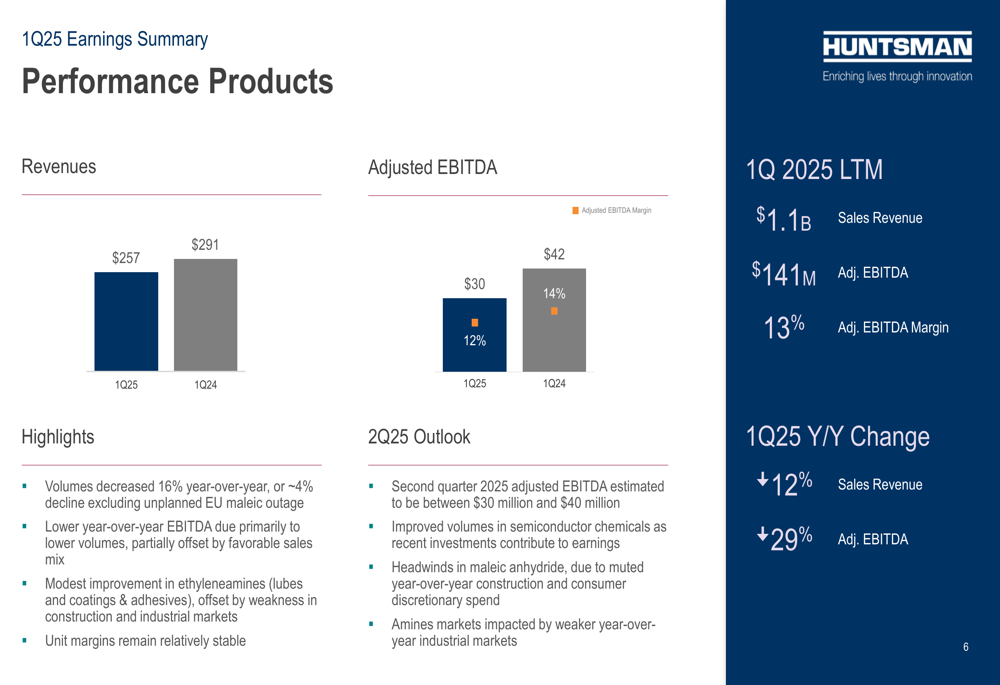

The Performance Products segment experienced more significant headwinds, with revenues declining to $257 million from $291 million in Q1 2024. Adjusted EBITDA fell to $30 million from $42 million, with margins contracting to 12% from 14%. The company attributed this decline to decreased volumes, though noted modest improvement in ethyleneamines and relatively stable unit margins.

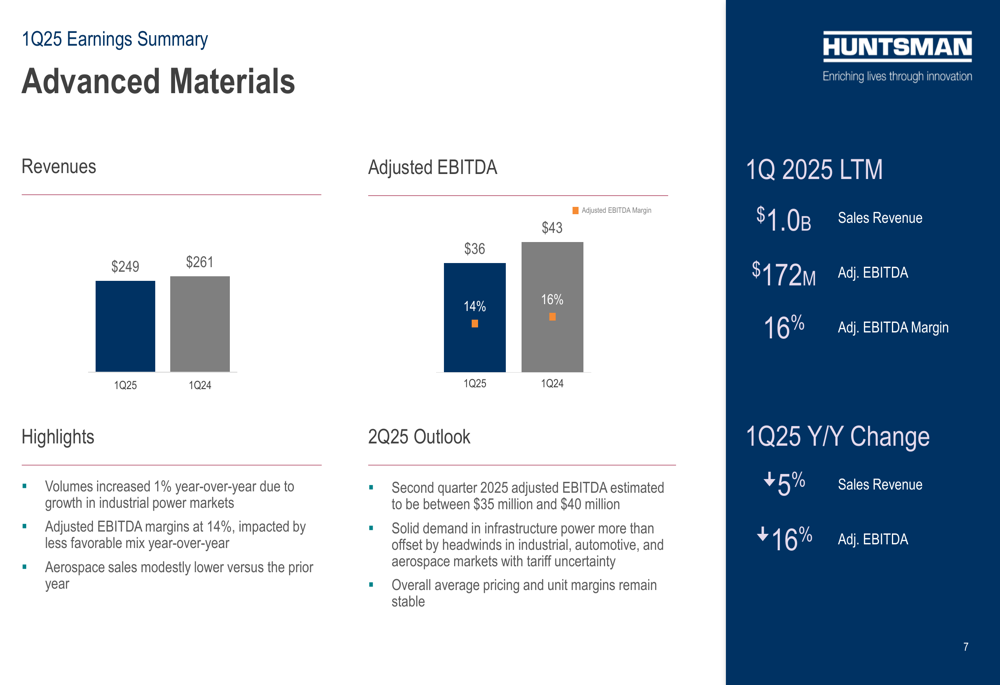

The Advanced Materials segment reported revenues of $249 million, down from $261 million in Q1 2024, with adjusted EBITDA decreasing to $36 million from $43 million. Margins contracted to 14% from 16%, despite increased volumes year-over-year. The company noted modestly lower aerospace sales impacting results.

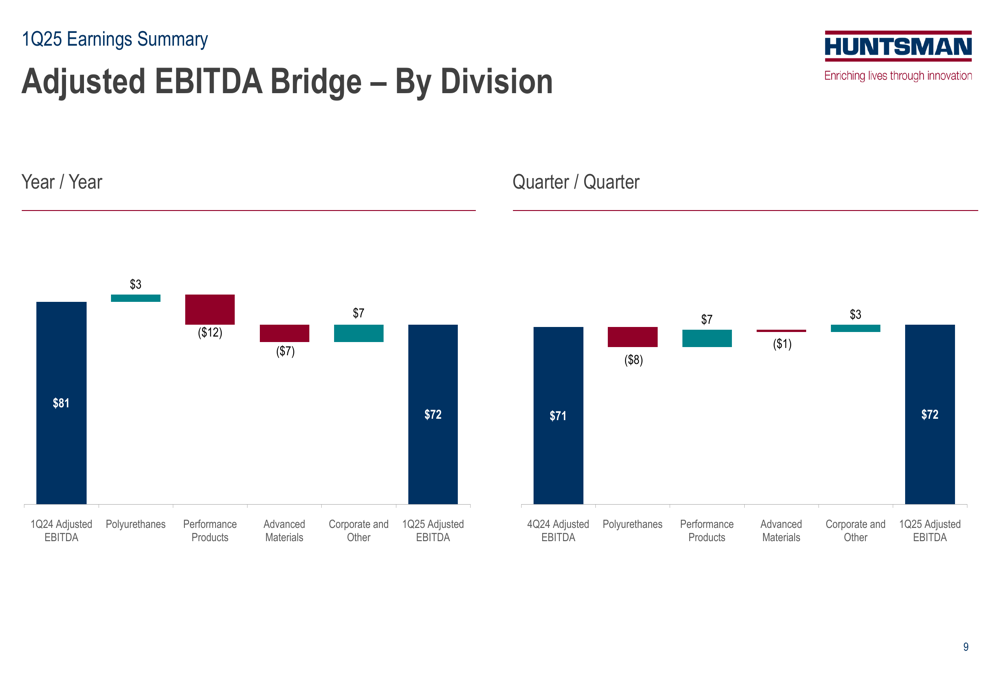

The following bridge chart illustrates how each division contributed to the overall change in adjusted EBITDA:

Strategic Initiatives & Outlook

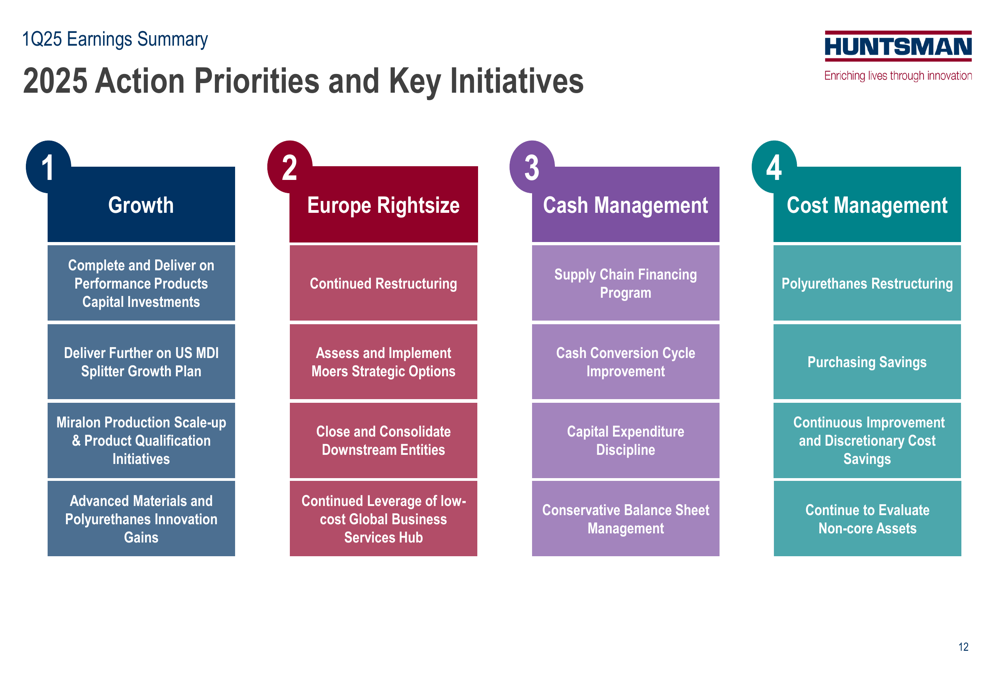

Huntsman outlined four key action priorities for 2025: Growth, Europe Rightsize, Cash Management, and Cost Management. These initiatives include completing capital investments in Performance Products, delivering on the US MDI splitter growth plan, continuing European restructuring, implementing supply chain financing programs, and evaluating non-core assets.

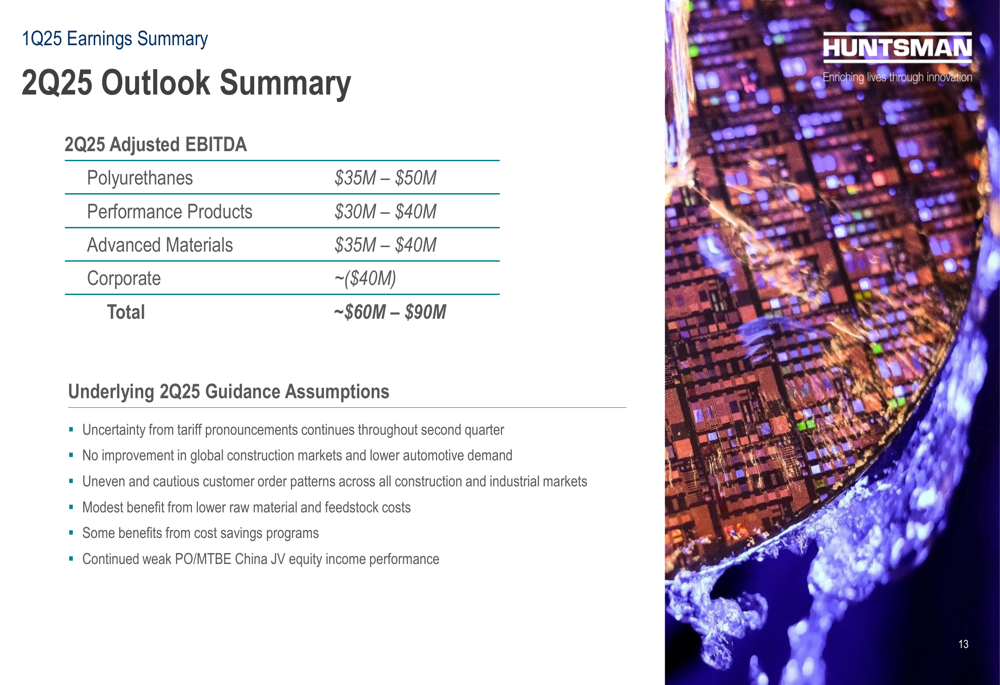

For Q2 2025, Huntsman provided an adjusted EBITDA outlook of approximately $60-90 million, with segment-specific guidance showing expected stability in Performance Products and Advanced Materials, while Polyurethanes faces some near-term challenges:

The company highlighted several underlying assumptions for Q2, including continued uncertainty from tariff pronouncements, no improvement in global construction markets, uneven customer order patterns, modest benefits from lower raw material costs, and some positive impact from cost savings programs.

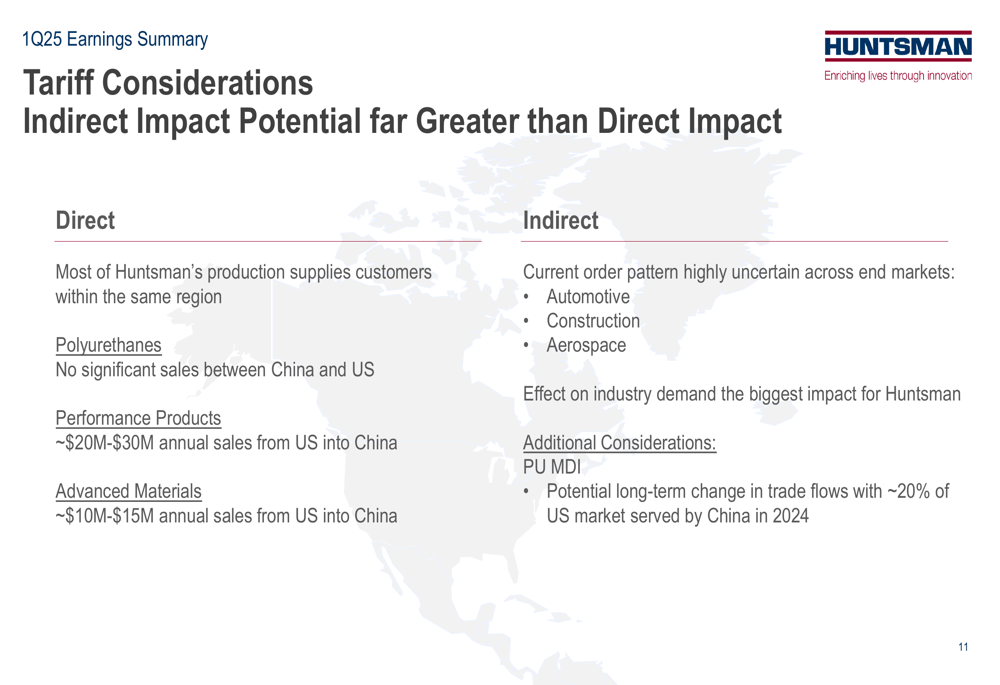

Huntsman specifically addressed tariff considerations, noting limited direct impact from US-China trade tensions, with approximately $20-30 million in annual sales from US to China for Performance Products and $10-15 million for Advanced Materials. However, the company emphasized that the indirect impact on industry demand represents the biggest concern.

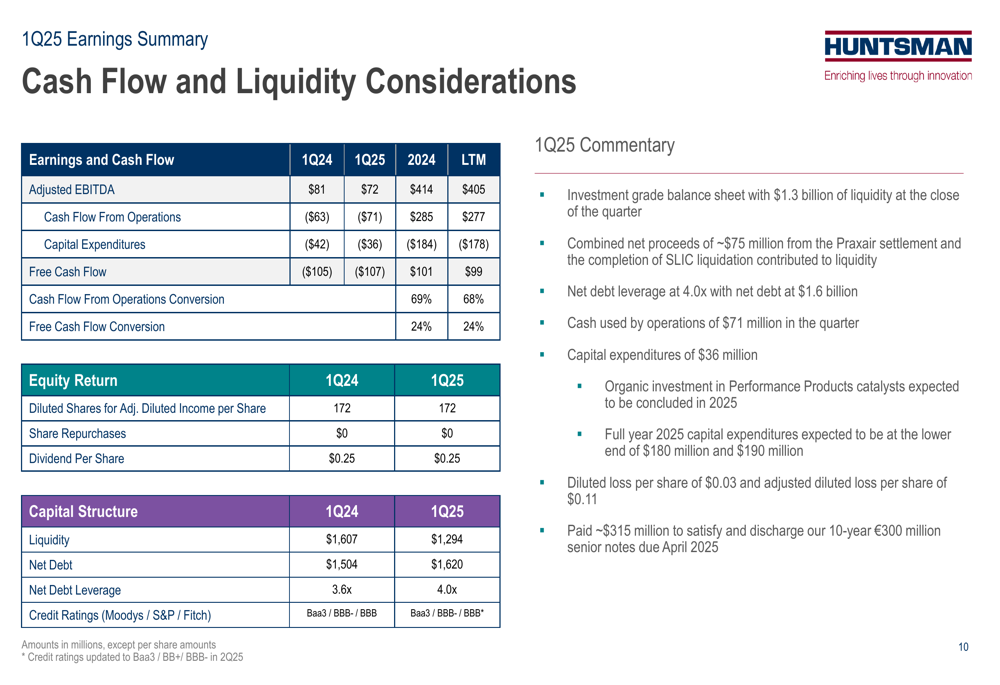

Financial Position & Cash Flow

Huntsman’s cash flow and liquidity position showed some deterioration year-over-year. Net cash used in operating activities increased to $(71) million from $(63) million in Q1 2024, while free cash flow worsened slightly to $(107) million from $(105) million.

The company’s net debt increased to $1,620 million from $1,504 million a year ago, with net debt leverage rising to 4.0x from 3.6x. Despite these challenges, Huntsman maintained its quarterly dividend of $0.25 per share and emphasized its investment grade balance sheet.

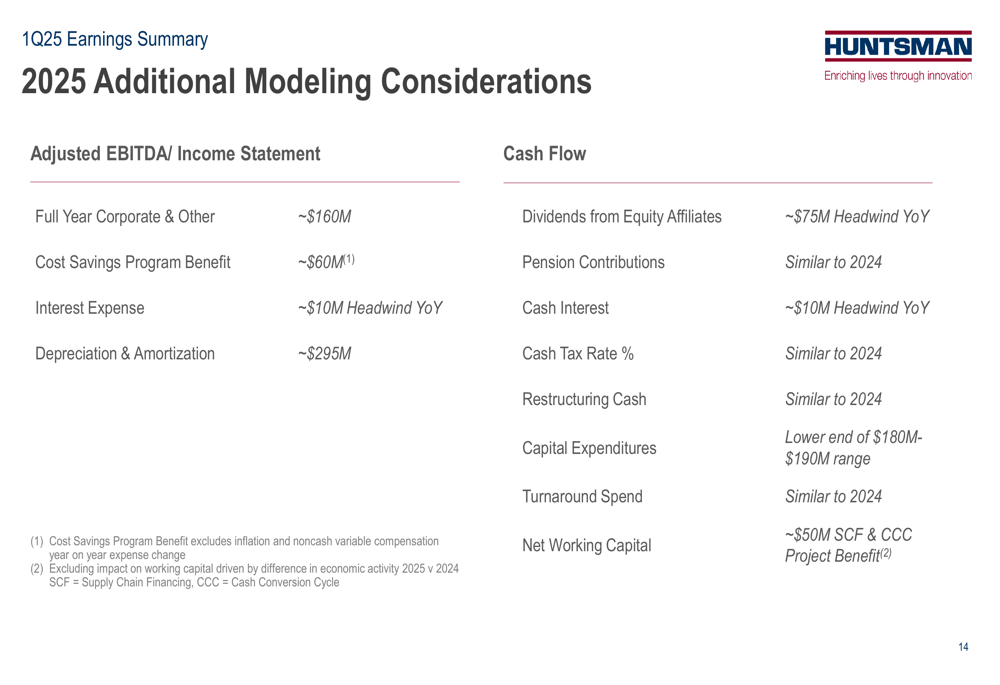

For the full year 2025, Huntsman provided additional modeling considerations, including approximately $160 million in corporate costs, $60 million in cost savings program benefits, and capital expenditures at the lower end of the $180-190 million range. The company also expects to realize about $50 million in benefits from supply chain financing and cash conversion cycle improvements.

As Huntsman navigates through 2025, management remains focused on cost minimization, asset optimization, and margin expansion across all divisions, while carefully monitoring global economic conditions and trade uncertainties that could impact demand patterns in key markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.