Can anything shut down the Gold rally?

Introduction & Market Context

Hydrofarm Holdings Group (NASDAQ:HYFM), a leading independent distributor and manufacturer of controlled environment agriculture equipment and supplies, presented its second quarter 2025 earnings results on August 12, 2025. The company continues to face significant industry headwinds, with net sales declining to $39.2 million in Q2 2025 from $54.8 million in the same period last year, representing a 28.4% decrease.

The company’s stock has struggled to gain momentum, trading near its 52-week low of $1.50, with a current price of $4.51. This performance reflects ongoing challenges in the cannabis industry, including oversupply issues and regulatory uncertainties that have plagued Hydrofarm since its disappointing Q4 2024 results, when the company significantly missed earnings forecasts.

Quarterly Performance Highlights

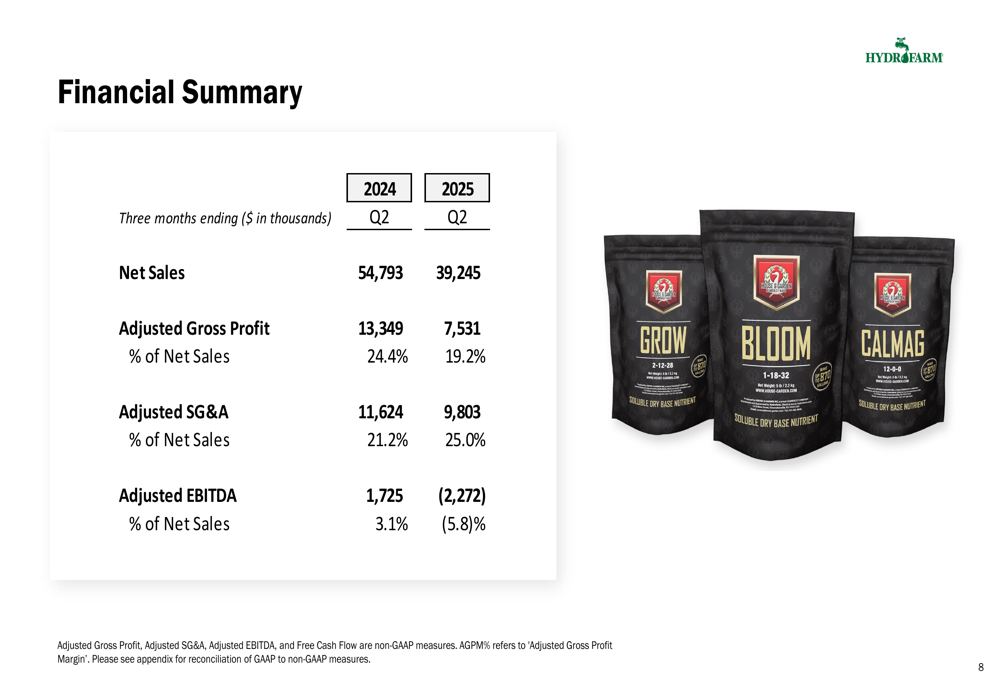

Hydrofarm’s Q2 2025 financial results revealed continued pressure on both top and bottom lines. Net sales decreased to $39.2 million, while adjusted gross profit fell to $7.5 million (19.2% of net sales) compared to $13.3 million (24.4% of net sales) in Q2 2024. The company reported negative adjusted EBITDA of $(2.3) million, representing -5.8% of net sales, down from positive $1.7 million (3.1% of net sales) in the prior year period.

As shown in the following financial summary:

Despite the revenue and profit margin challenges, Hydrofarm highlighted its continued progress in reducing selling, general and administrative expenses, marking the 12th consecutive quarter of year-over-year reductions in adjusted SG&A. These expenses decreased to $9.8 million in Q2 2025 from $11.6 million in Q2 2024, though as a percentage of sales, they increased to 25.0% from 21.2% due to the lower revenue base.

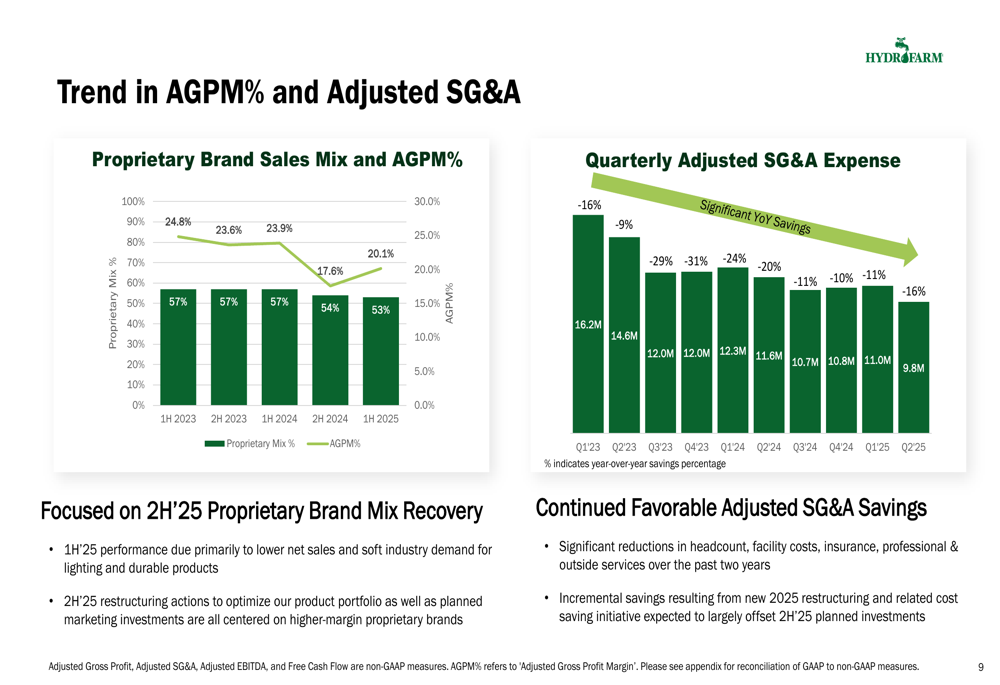

The following chart illustrates the company’s proprietary brand sales mix and adjusted gross profit margin trends, along with the consistent reduction in quarterly SG&A expenses:

Restructuring Initiatives

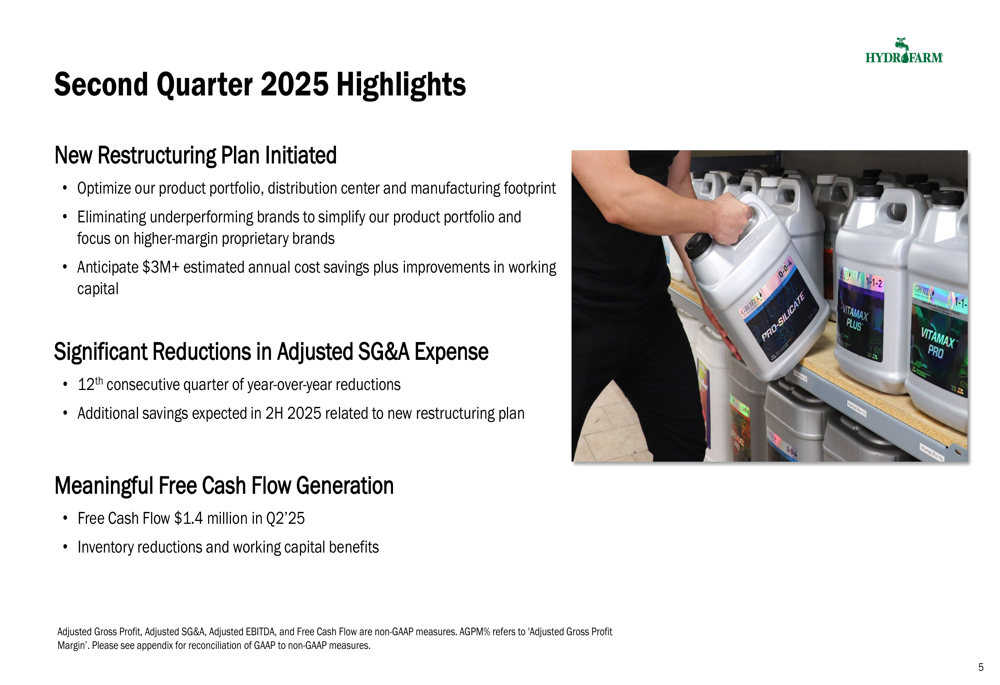

In response to persistent challenges, Hydrofarm announced a new restructuring plan aimed at optimizing its product portfolio and distribution center and manufacturing footprint. The company is eliminating underperforming brands to simplify its product portfolio and focus on higher-margin proprietary brands, with anticipated annual cost savings exceeding $3 million plus improvements in working capital.

The restructuring initiatives are highlighted in the company’s Q2 2025 summary:

CEO John Lindeman has previously emphasized the company’s commitment to improving its proprietary brand mix and diversifying revenue streams, a strategy that continues to be central to Hydrofarm’s recovery plan. The company’s strategic priorities remain focused on three key areas: driving diverse, high-quality revenue streams; improving profit margins; and strengthening its financial position.

Financial Position and Debt Structure

Despite ongoing operational challenges, Hydrofarm reported positive free cash flow of $1.4 million in Q2 2025, driven by inventory reductions and working capital benefits. The company’s cash position stood at $11.0 million as of June 30, 2025, with total liquidity of $20.0 million.

The company’s financial position is summarized in the following slide:

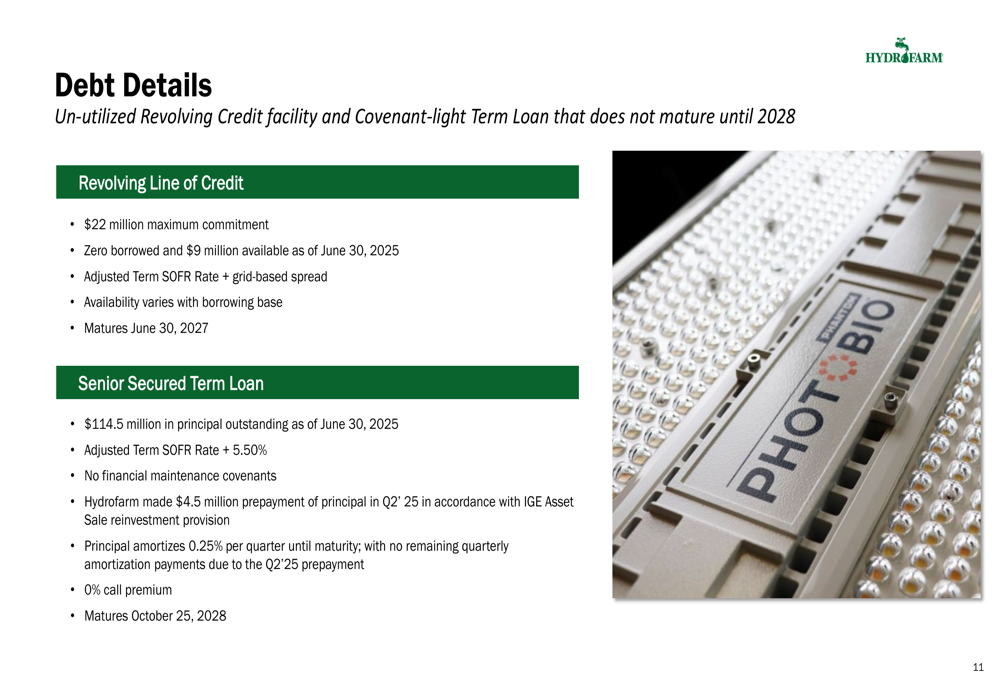

Hydrofarm’s debt structure includes a $22 million revolving line of credit (undrawn as of June 30, 2025) and a senior secured term loan with $114.5 million in principal outstanding. The company made a $4.5 million prepayment of principal in Q2 2025 in accordance with an asset sale reinvestment provision. The term loan matures in October 2028 and has no financial maintenance covenants.

The detailed debt structure is outlined below:

Forward-Looking Statements

Looking ahead, Hydrofarm acknowledged ongoing industry headwinds and tariff uncertainty that could impact performance. High tariffs on imported products from China, or new tariffs on or from other countries, could affect product costs and potentially negatively impact results.

For fiscal year 2025, the company expects improved adjusted gross profit margin compared to full year 2024, reduced year-over-year adjusted SG&A expenses, and a reduction in inventory with positive free cash flow for the last nine months of 2025. These expectations align with the company’s previous guidance from Q4 2024, when it projected a 10-20% sales decline for 2025.

The company’s 2H 2025 restructuring actions to optimize its product portfolio and planned marketing investments are centered on higher-margin proprietary brands, which management believes will help improve gross margins. Additional savings resulting from the new restructuring and related cost-saving initiatives are expected to largely offset second-half 2025 planned investments.

As Hydrofarm continues to navigate challenging market conditions, its focus remains on cost reduction, working capital management, and strategic initiatives to drive long-term profitability and shareholder value. However, investors should note the significant gap between the company’s optimistic restructuring narrative and its recent financial performance, including the substantial earnings miss in Q4 2024 and continued revenue declines in 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.