Domo signs strategic collaboration agreement with AWS for AI solutions

Introduction & Market Context

Hyperfine Inc (NASDAQ:HYPR) presented its May 2025 corporate strategy on Tuesday, outlining ambitious growth plans for its portable MRI technology amid recent financial challenges. The medical technology company, currently trading at $0.70 per share, has experienced significant volatility, with its stock sitting well below its 52-week high of $1.90 despite extending its cash runway.

The company’s presentation comes after a disappointing Q4 2024 earnings report where revenue of $2.3 million missed analyst expectations of $3.3 million, though it met EPS forecasts of -$0.14. Hyperfine’s stock has continued to struggle, dropping 4.12% in the most recent trading session and falling another 2.84% in after-hours trading.

Executive Summary

Hyperfine positions itself as a pioneer in brain health with the first FDA-cleared, AI-powered portable MR brain imaging system. The company’s Swoop system aims to transform neurological care by making MRI technology more accessible, affordable, and deployable across various healthcare settings.

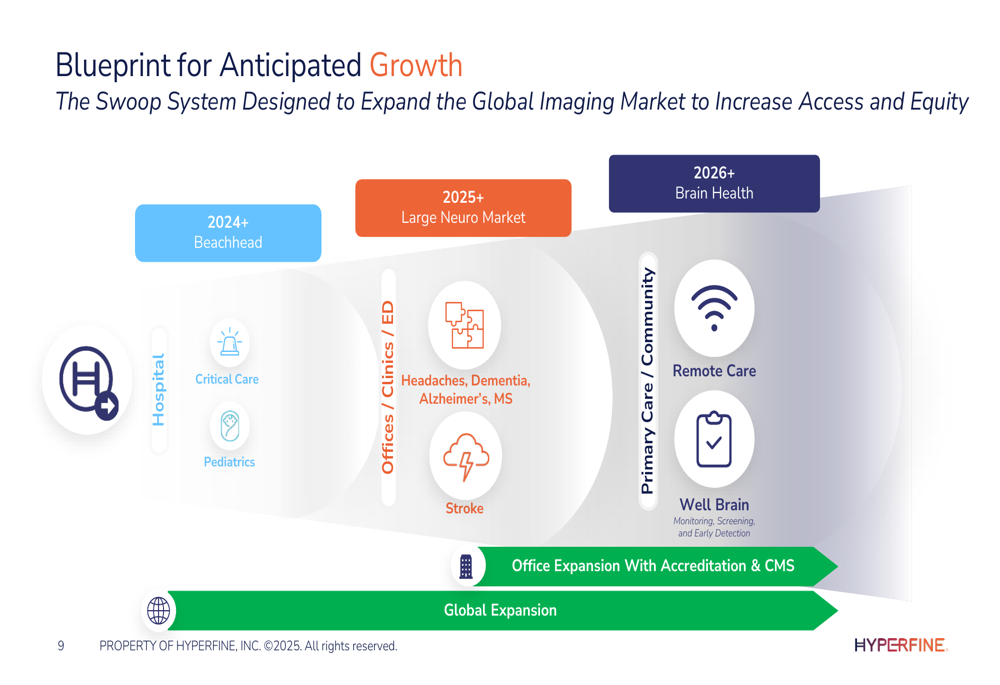

The presentation highlights Hyperfine’s three-phase growth strategy: establishing a beachhead in critical care and pediatrics (2024+), expanding into emergency departments and neurology practices (2025+), and ultimately penetrating primary care and community settings (2026+). This expansion plan corresponds to an increasing total addressable market (TAM) from $1.5 billion to potentially $16+ billion.

As shown in the following chart of the company’s growth blueprint:

Strategic Initiatives

Hyperfine’s strategic roadmap centers on expanding its technology into new care settings while continuing to improve image quality. The company emphasizes that its portable MRI offers significant advantages over conventional MRI systems, including lower upfront capital costs, no specialized construction requirements, and greater accessibility.

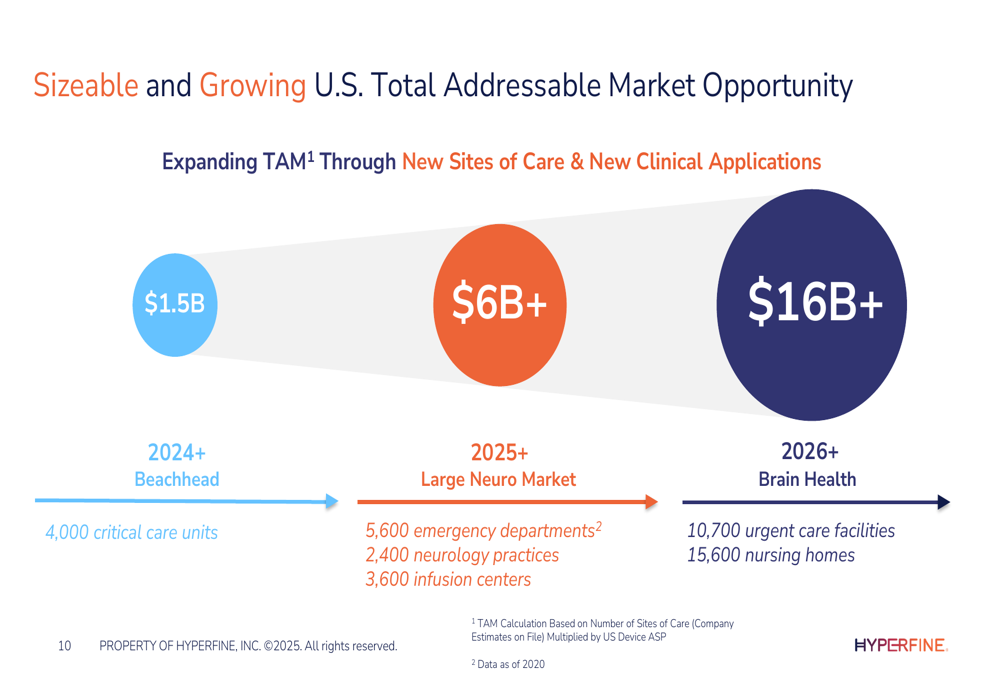

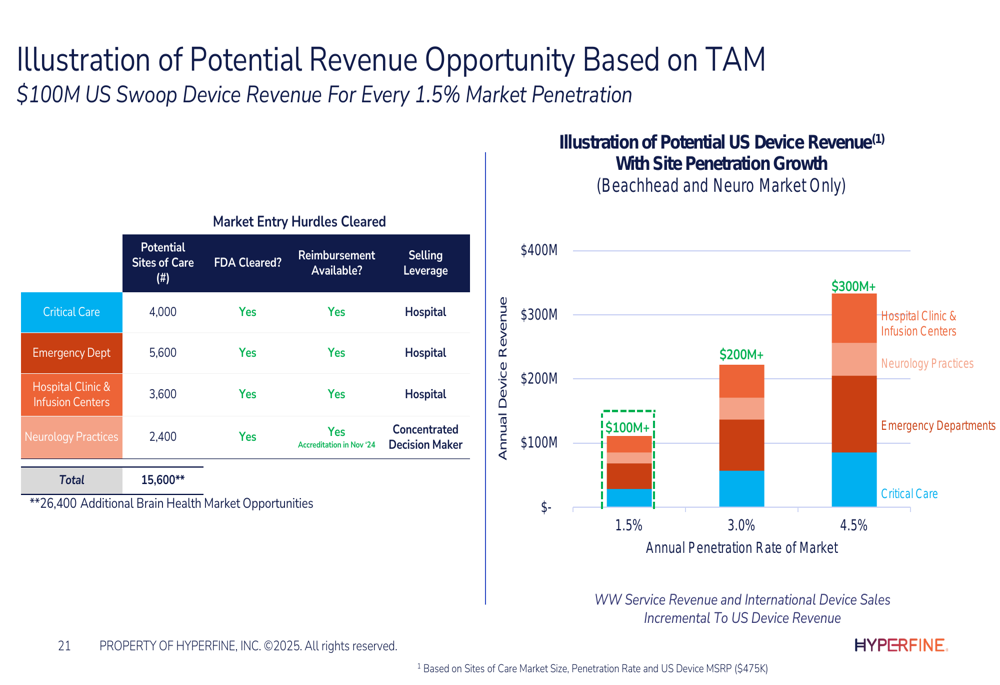

The company’s presentation highlights the substantial U.S. market opportunity, with detailed breakdowns of potential sites for the Swoop system:

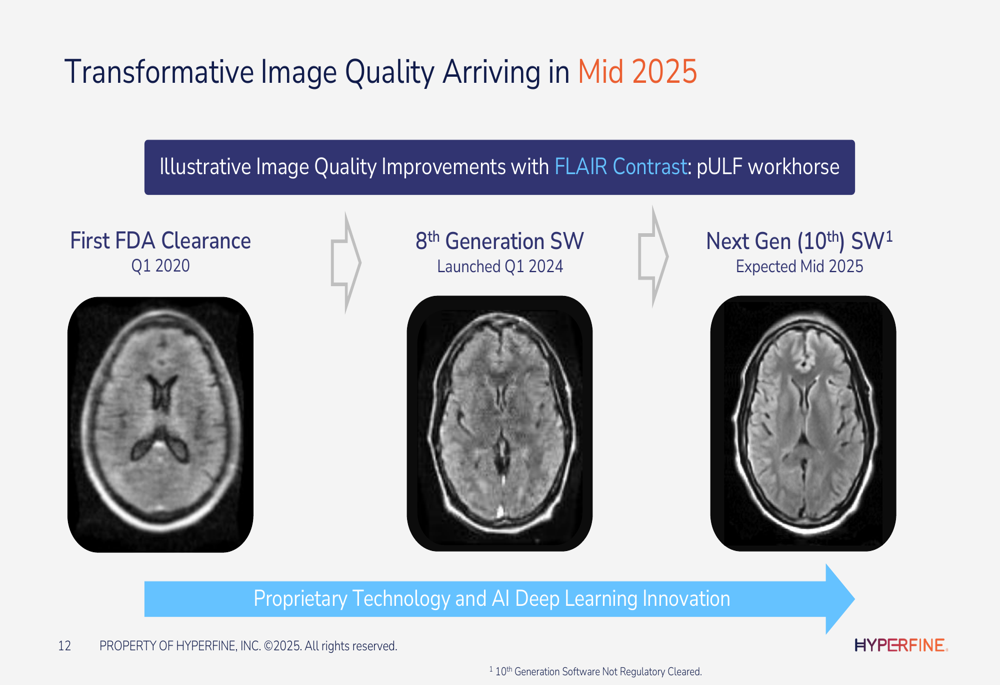

A key component of Hyperfine’s strategy is the continuous improvement of its AI-powered imaging technology. The company plans to release its 10th generation software in mid-2025, which promises significantly enhanced image quality approaching that of conventional 1.5T MRI systems.

The progression of image quality improvements is illustrated in this comparison:

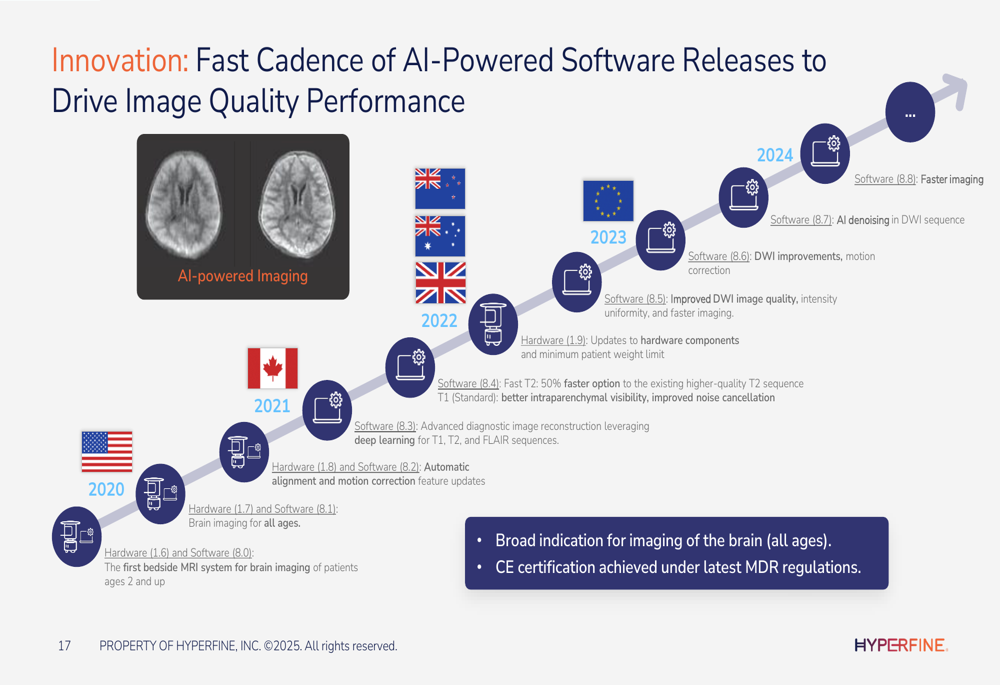

The company is targeting two key expansion areas in 2025: emergency departments for stroke triage and neurology offices. For emergency departments, Hyperfine is conducting the ACTION-PMR multi-center evaluation study to validate the Swoop system’s effectiveness in stroke detection. For neurology offices, the recent publication of Intersocietal Accreditation Commission (IAC) standards in November 2024 represents a significant milestone, as it formally incorporates portable MRI technology into accreditation guidelines.

Hyperfine’s innovation timeline showcases the rapid development of its AI-powered software:

Detailed Financial Analysis

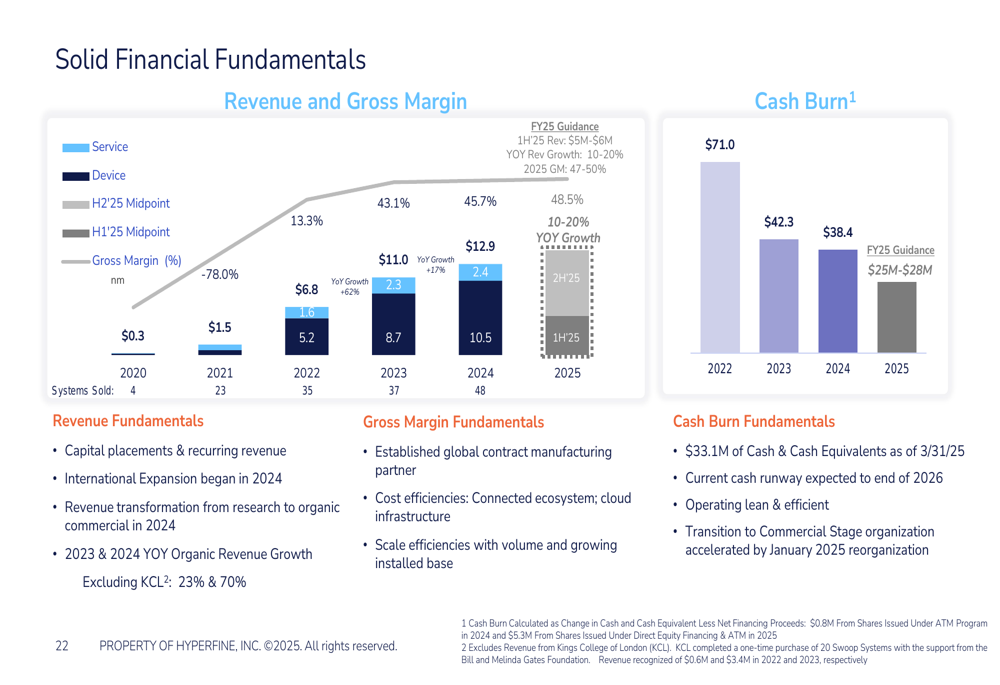

Despite missing Q4 2024 revenue expectations, Hyperfine’s presentation projects continued growth, with 2025 revenue estimated at $12.9 million. This represents a significant increase from previous years but will require substantial acceleration from the $2.3 million reported in Q4 2024.

The company has made progress in improving its financial fundamentals, with gross margins expanding and cash burn decreasing substantially from $71 million in 2022 to an estimated $25-28 million in 2025. As of March 31, 2025, Hyperfine reported $33.1 million in cash and cash equivalents, slightly down from the $37.6 million reported at the end of December 2024.

The financial trends are illustrated in this chart:

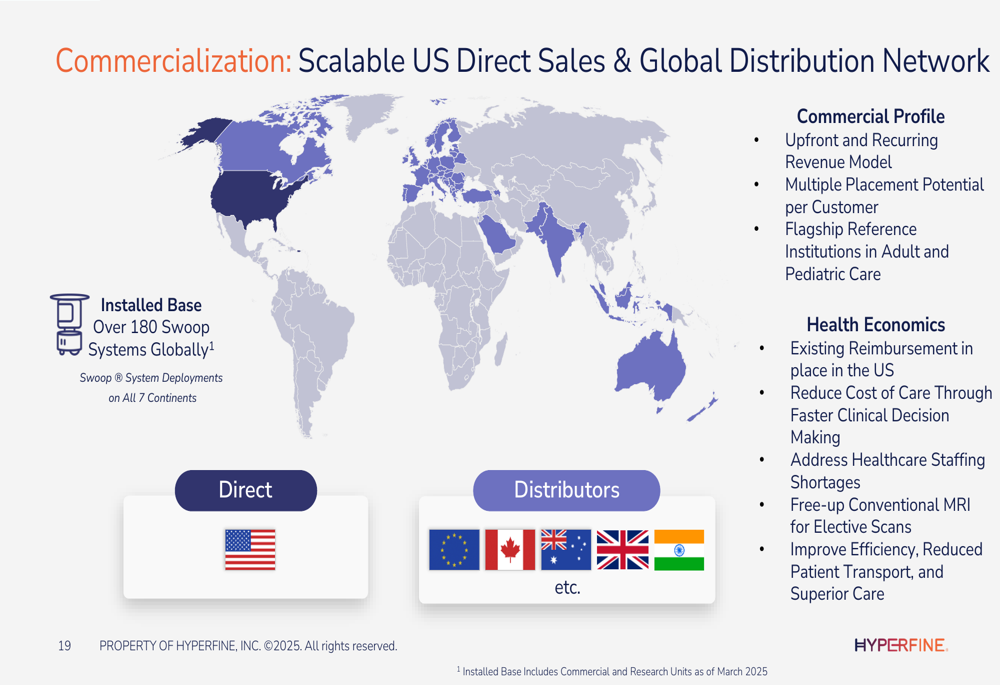

Hyperfine’s business model includes both capital equipment sales and recurring revenue streams from service contracts and software updates. The company believes this model will provide an attractive margin expansion opportunity as its installed base grows beyond the current 180+ systems globally.

The company’s global commercialization strategy combines direct sales in the U.S. with international distribution partners:

Forward-Looking Statements

Hyperfine projects that for every 1.5% market penetration in the U.S., it could generate approximately $100 million in device revenue. The company illustrates potential revenue growth based on various market penetration scenarios:

However, these projections must be viewed in the context of recent performance challenges. In its Q4 2024 earnings call, Hyperfine acknowledged variability in hospital capital spending and noted that it had replaced half of its U.S. sales team, suggesting execution difficulties that could impact near-term results.

The company expects 2025 to be "a tale of two halves," according to CEO Maria Faines, with revenue growth of 20-30% projected for the full year and first-half revenue expected to reach $6 million. This implies stronger performance in the second half, coinciding with the planned launch of the 10th and 11th generation software.

Hyperfine faces several challenges, including revenue variability, regulatory approvals for market expansion, and a competitive landscape that requires continuous innovation. Nevertheless, the company maintains that its current cash runway extends to the end of 2026, providing time to execute its growth strategy despite recent market volatility.

The company summarizes its investment opportunity with these key points:

While Hyperfine’s presentation outlines an ambitious vision for transforming brain imaging, investors will likely focus on the company’s ability to accelerate revenue growth and demonstrate commercial traction in the coming quarters as it works to close the gap between its strategic aspirations and current financial reality.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.