Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

Hyster-Yale Materials Handling Inc (NYSE:HY) reported a significant revenue decline in its Q2 2025 presentation, continuing the challenging trend seen in Q1. The material handling equipment manufacturer posted $957 million in revenue, an 18% decrease compared to the prior year, while recording a $9 million operating loss. Despite these headwinds, management emphasized their commitment to long-term strategic initiatives and projected improvement in the third quarter.

The company’s stock has struggled in recent months, trading at $41.35 as of August 5, 2025, near its 52-week low of $34.13 and well below its 52-week high of $72.01. This follows a 4.01% drop after Q1 results missed analyst expectations, with the Q2 presentation confirming continued challenges.

Quarterly Performance Highlights

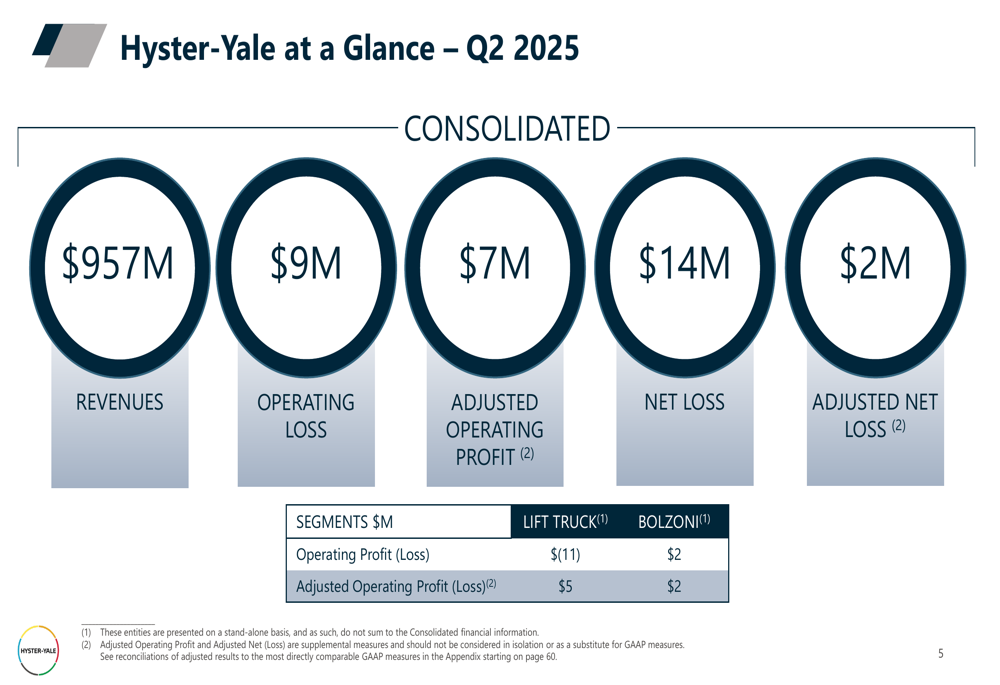

Hyster-Yale’s Q2 2025 financial results showed substantial year-over-year declines across key metrics. The company reported $957 million in revenue, a $9 million operating loss, and a $14 million net loss. On an adjusted basis, operating profit was $7 million with a $2 million adjusted net loss.

As shown in the following summary of Q2 2025 performance:

The company’s Lift Truck segment, which represents the core of its business, posted an $11 million operating loss, though it achieved $5 million in adjusted operating profit. Meanwhile, the Bolzoni attachment business recorded $2 million in both operating profit and adjusted operating profit.

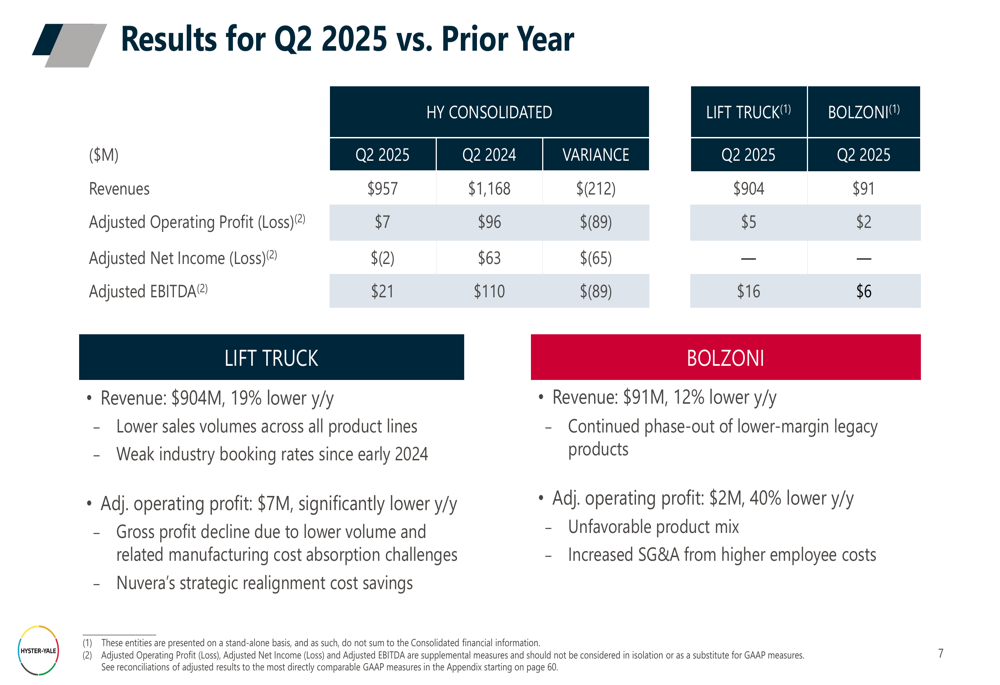

Comparing Q2 2025 with the prior year shows the extent of the decline:

Bookings also showed significant weakness, with unit bookings value of $330 million representing a 44% decrease compared to Q1 2025. The company’s backlog stands at $1.7 billion in unit value. This decline follows the trend seen in Q1, where Hyster-Yale missed analyst expectations with an EPS of $0.49 against forecasts of $1.66.

Financial Position

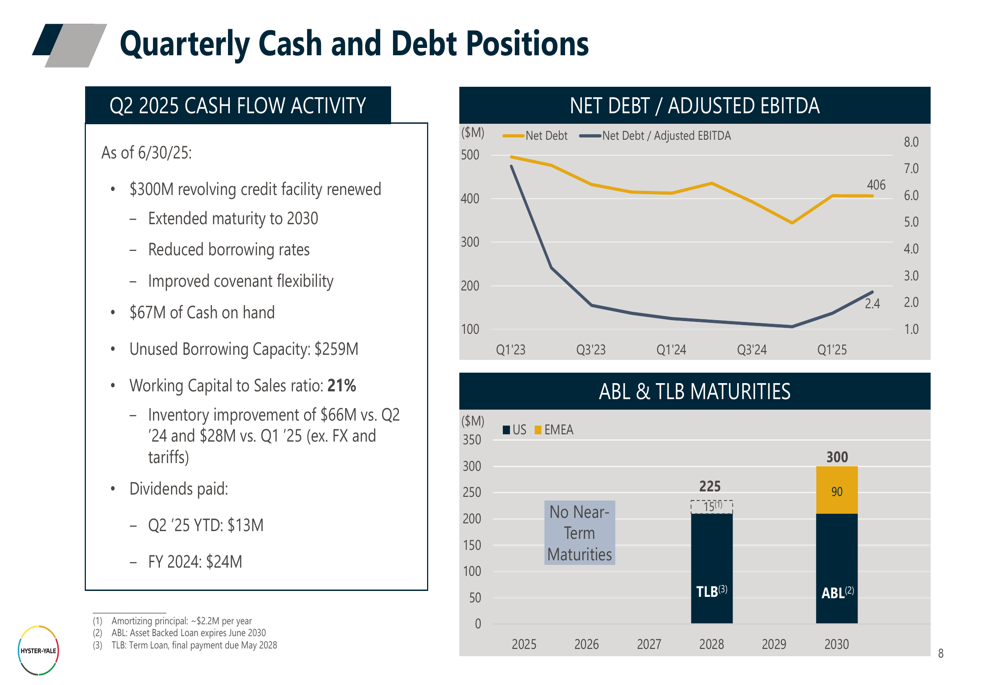

Despite operational challenges, Hyster-Yale emphasized its strong liquidity position. The company has extended its $300 million credit facility to 2030 and reported $67 million in cash on hand with $259 million in unused borrowing capacity as of June 30, 2025.

The company’s quarterly cash and debt positions are illustrated in the following chart:

Working capital management remains a focus area, with the company reporting working capital at 21% of sales. This aligns with management’s long-term objective of achieving 15% working capital to sales ratio, though current economic conditions have made this target challenging to reach in the near term.

Strategic Initiatives

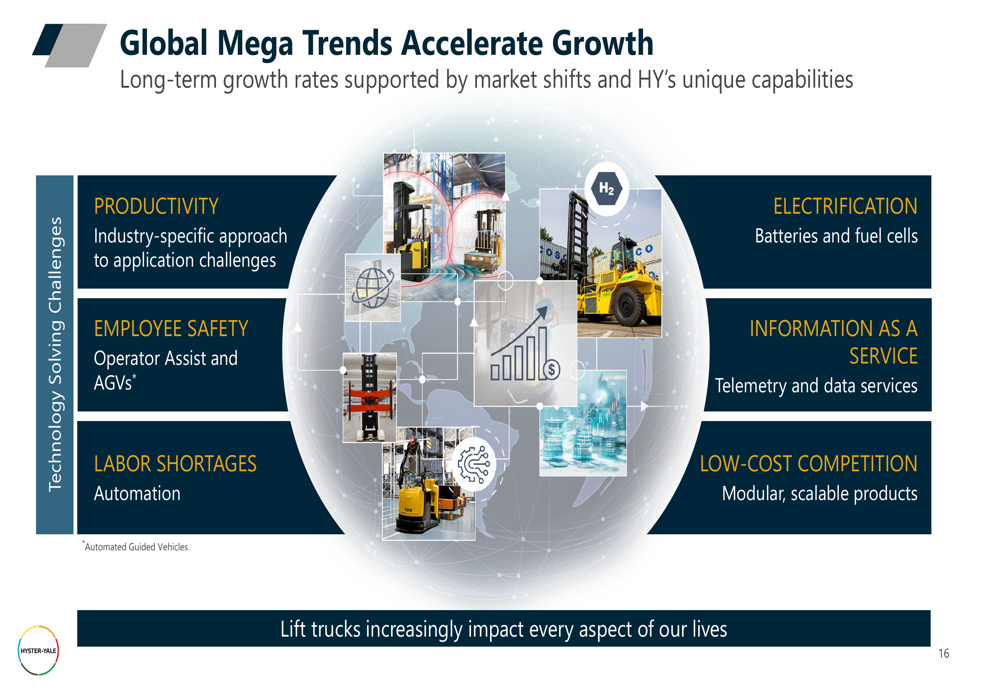

Hyster-Yale continues to emphasize its long-term strategic vision despite current headwinds. The company identified several global trends supporting its growth strategy, including productivity demands, employee safety concerns, labor shortages, electrification, and information services.

The following illustration highlights these global mega trends that the company believes will accelerate growth:

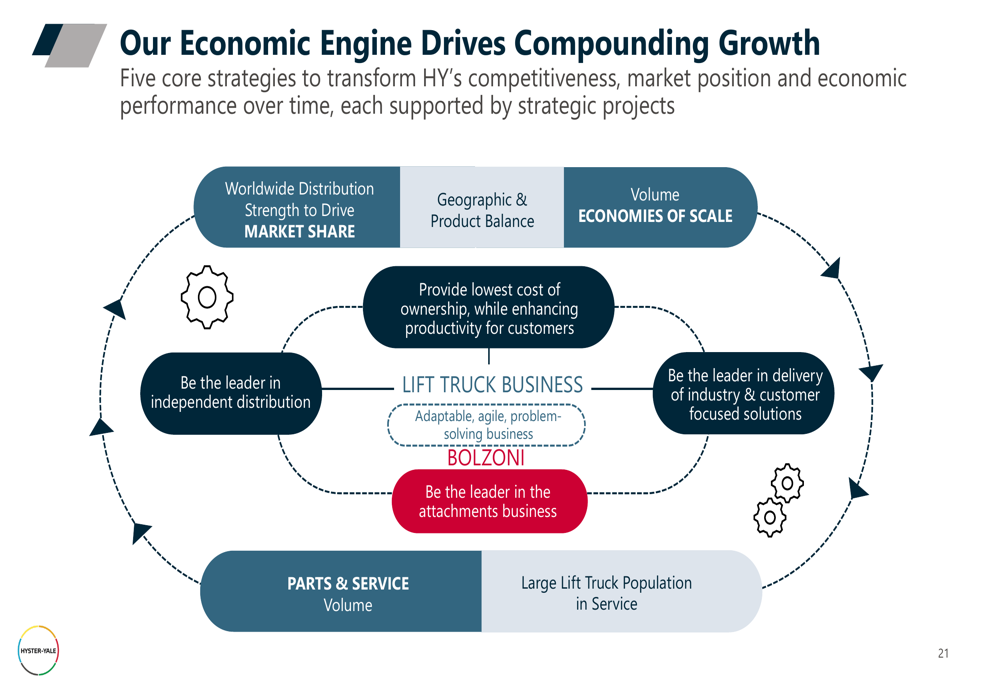

The company’s economic engine for growth focuses on delivering the lowest cost of ownership, improving lift truck adaptability, and increasing service volume through its distribution network:

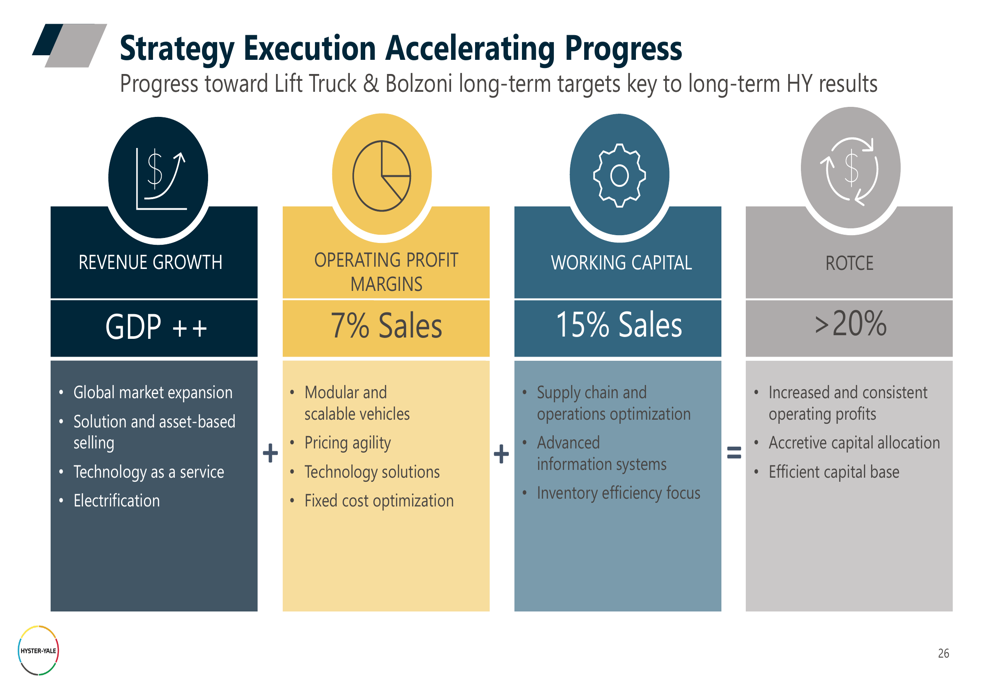

Hyster-Yale has established clear long-term financial objectives, targeting GDP++ revenue growth, 7% operating profit margins, 15% working capital to sales ratio, and over 20% return on total capital employed (ROTCE):

Business Segment Performance

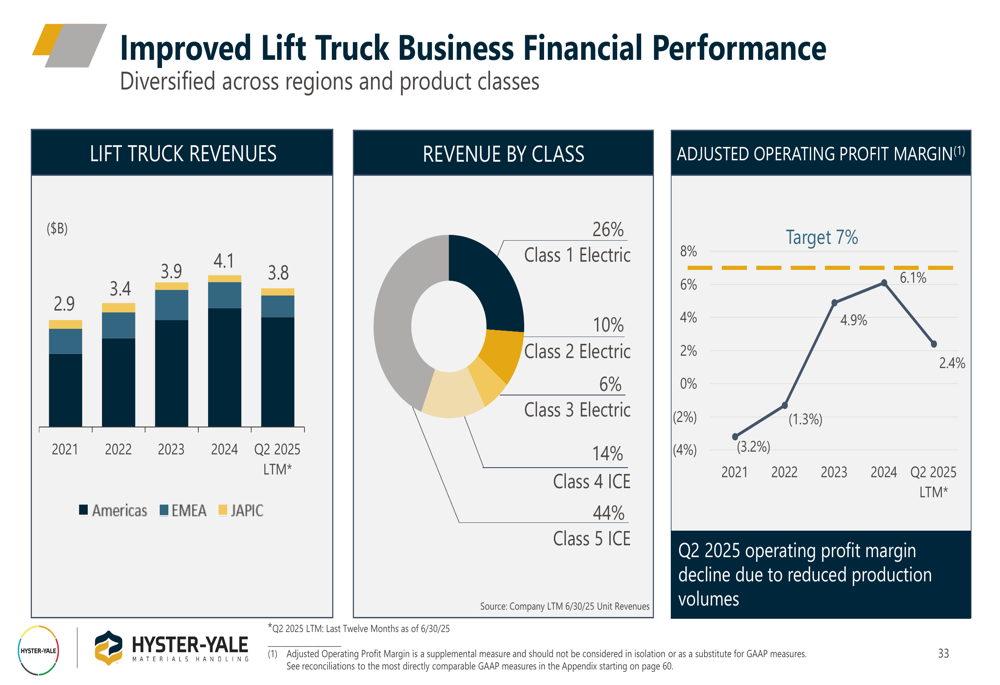

The Lift Truck business, which represents Hyster-Yale’s core operation, has shown improved financial performance in recent years, growing from $2.9 billion in revenue in 2021 to $4.1 billion in 2024, though Q2 2025 LTM figures show a slight decrease:

The company’s revenue is diversified across product types, industries, and distribution channels. Electric units account for 32% of truck sales, while the Americas represent the largest geographic market at 75.3% of sales, followed by EMEA at 14.9%.

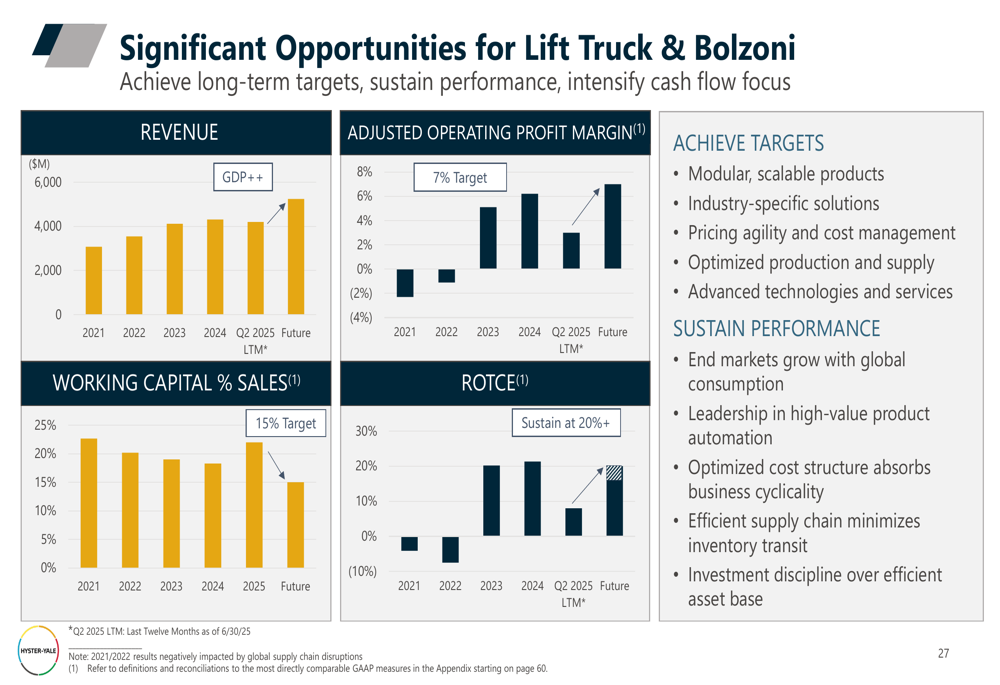

Hyster-Yale has identified significant opportunities for both its Lift Truck and Bolzoni businesses, focusing on modular scalable products, industry-specific solutions, pricing agility, production optimization, and advanced technologies:

Forward-Looking Statements

Management projects that Q3 2025 revenue and operating profit will improve compared to Q2 2025, though full-year 2025 results are expected to be substantially below 2024 levels. The company cited higher tariffs as a key factor affecting performance and noted that working capital improvements are expected from inventory efficiency initiatives.

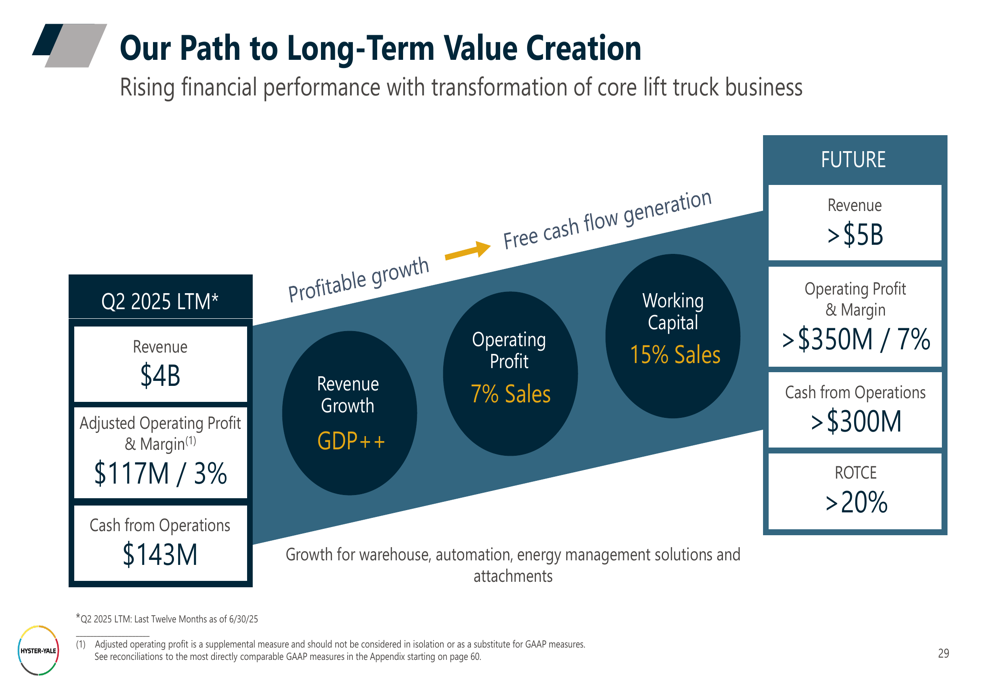

Hyster-Yale’s path to long-term value creation focuses on growing warehouse and automation solutions, with targets of over $5 billion in revenue, more than $350 million in operating profit (7% margin), and over $300 million in cash from operations:

Competitive Industry Position

Hyster-Yale positions itself as a global leader in material handling solutions with 8,300 employees worldwide. The company operates through two synergistic businesses: Lift Trucks (core business) and Bolzoni (attachment business).

The company’s unique business model focuses on efficient capital deployment through investments that enhance the lift truck business, capital-efficient investments in scalable products and footprint optimization, and optimized capital deployment through an independent dealer network.

Hyster-Yale is particularly focused on electrification and automation, with major projects underway in ports in Spain and Germany. The company is also developing automated lift trucks and expanding its energy solutions, including lithium-ion batteries and hydrogen fuel cell technology.

Conclusion

Hyster-Yale’s Q2 2025 presentation reveals a company navigating significant near-term challenges while maintaining focus on long-term strategic initiatives. The 18% year-over-year revenue decline and operating loss reflect difficult market conditions, continuing the trend seen in Q1 2025 when the company missed analyst expectations.

Despite these headwinds, management projects improvement in Q3 2025 and emphasizes the company’s strong liquidity position and strategic investments in electrification, automation, and modular product platforms. However, investors should note that full-year 2025 results are expected to remain substantially below 2024 levels, with higher tariffs cited as a key factor affecting performance.

As Hyster-Yale works toward its long-term financial objectives of GDP++ revenue growth, 7% operating profit margins, and over 20% ROTCE, the company’s ability to execute on its strategic initiatives while navigating current market challenges will be crucial to its future success.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.