Two National Guard members shot dead near White House

Introduction & Market Context

IAC/InterActiveCorp (NASDAQ:IAC) presented its first quarter 2025 earnings results in May, highlighting its diverse portfolio of digital businesses and arguing that the market significantly undervalues its assets. Trading at $34.59 as of October 3, 2025, IAC's stock has experienced volatility since the presentation, including a 13.41% drop following its Q2 earnings despite delivering a surprising positive EPS.

The company's presentation emphasized its position as a leader across multiple consumer categories, from publishing to family care services, while outlining a strategic roadmap focused on business execution, capital allocation, and value creation catalysts.

Executive Summary

IAC's Q1 2025 presentation portrayed a company with substantial hidden value, claiming that after accounting for its MGM Resorts stake and cash holdings, investors are effectively acquiring its private business holdings for free. The company highlighted its diverse portfolio spanning publishing (Dotdash Meredith), care services (Care.com), and significant stakes in MGM Resorts International and car-sharing platform Turo.

As shown in the following slide illustrating IAC's diverse business portfolio:

The company reported having $0.9 billion in cash on hand while emphasizing its ability to span diverse industries and business stages. IAC's presentation focused on its strategic positioning across digital publishing, entertainment, family care, and emerging sectors, with a particular emphasis on its ability to deploy capital for future growth opportunities.

Quarterly Performance Highlights

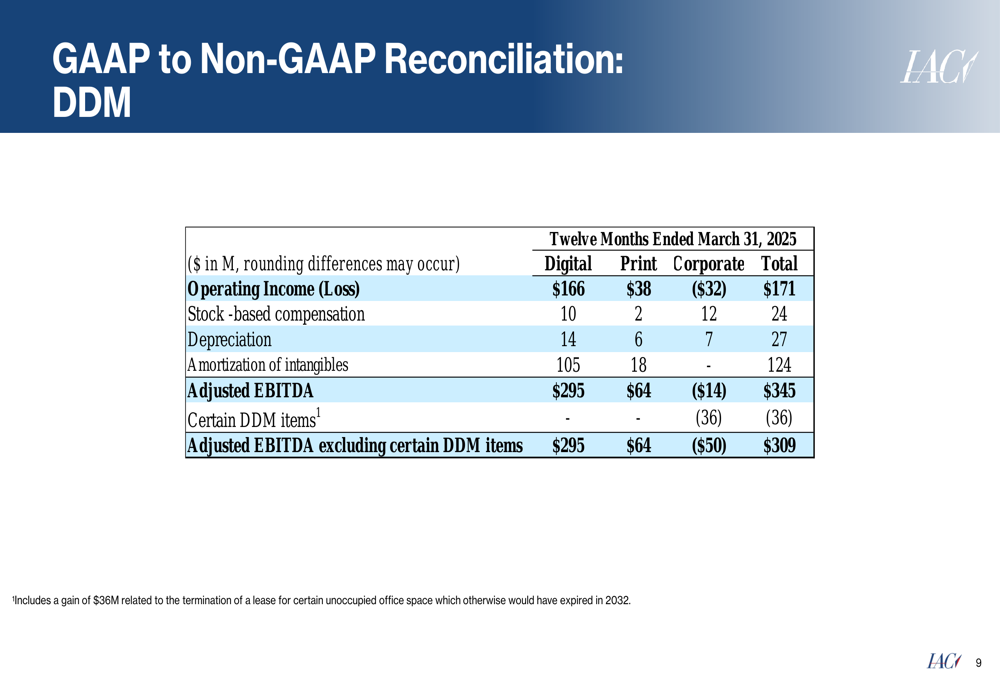

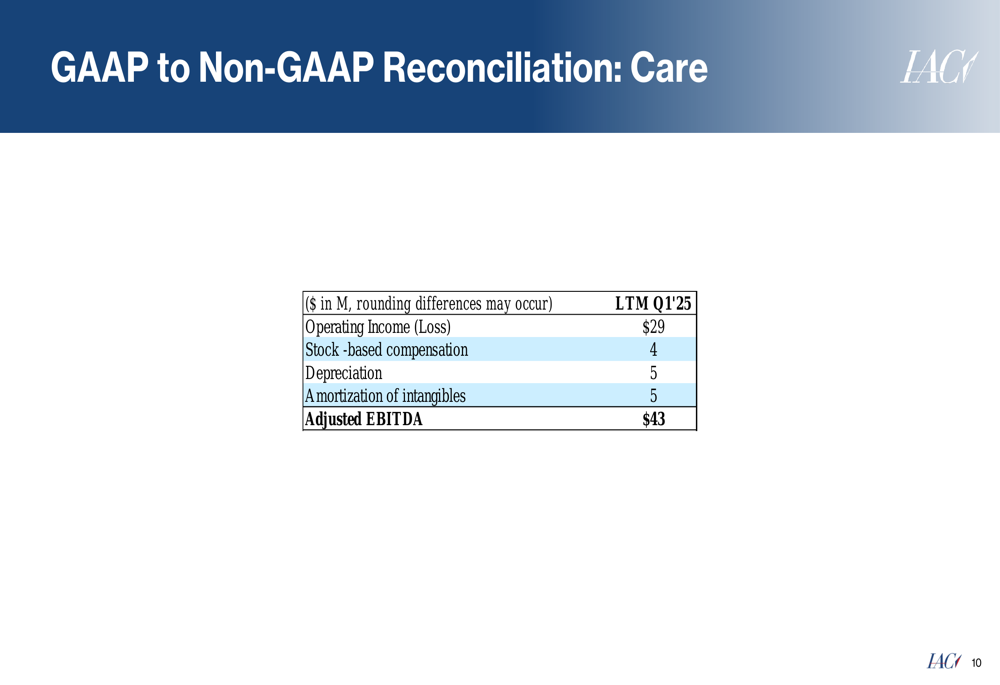

IAC's financial data showed mixed performance across its portfolio. Dotdash Meredith generated $1 billion in digital revenue with $309 million in Adjusted EBITDA, while maintaining $1.2 billion in net debt at 4.0x leverage. Care.com reported $366 million in revenue and $43 million in Adjusted EBITDA.

The company's GAAP to non-GAAP reconciliation for Dotdash Meredith revealed the following performance metrics:

Similarly, Care.com's financial performance showed positive operating income:

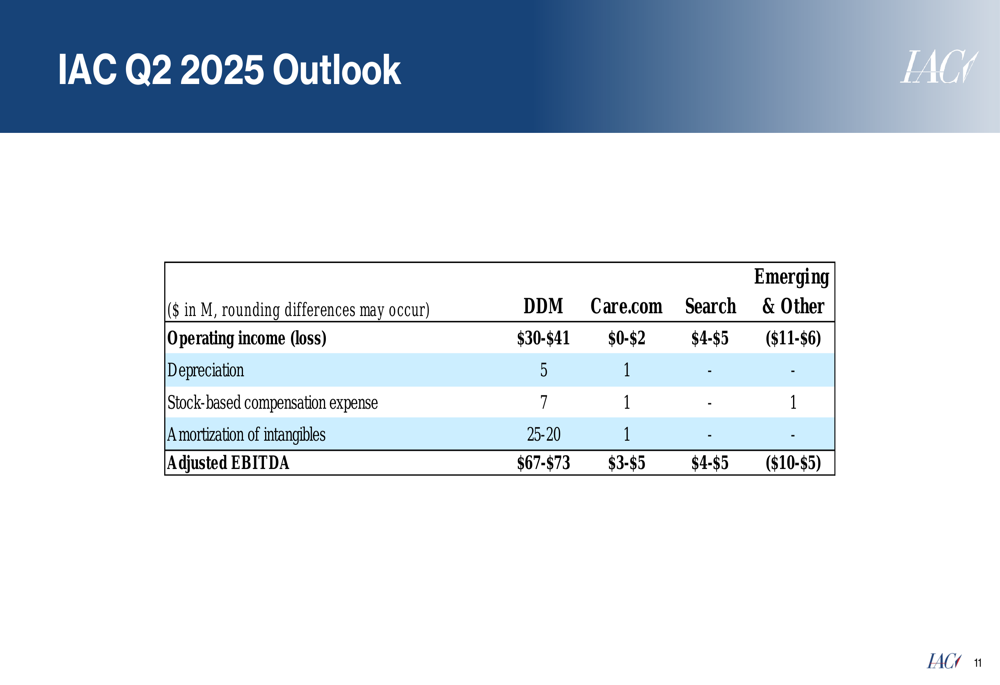

For Q2 2025, IAC provided specific guidance across its business segments:

However, subsequent Q2 results revealed that while IAC delivered a surprising EPS of $2.57 against a forecast of -$0.2927, revenue fell short of expectations at $586.9 million compared to the forecasted $601.35 million, contributing to the stock's negative reaction.

Strategic Initiatives

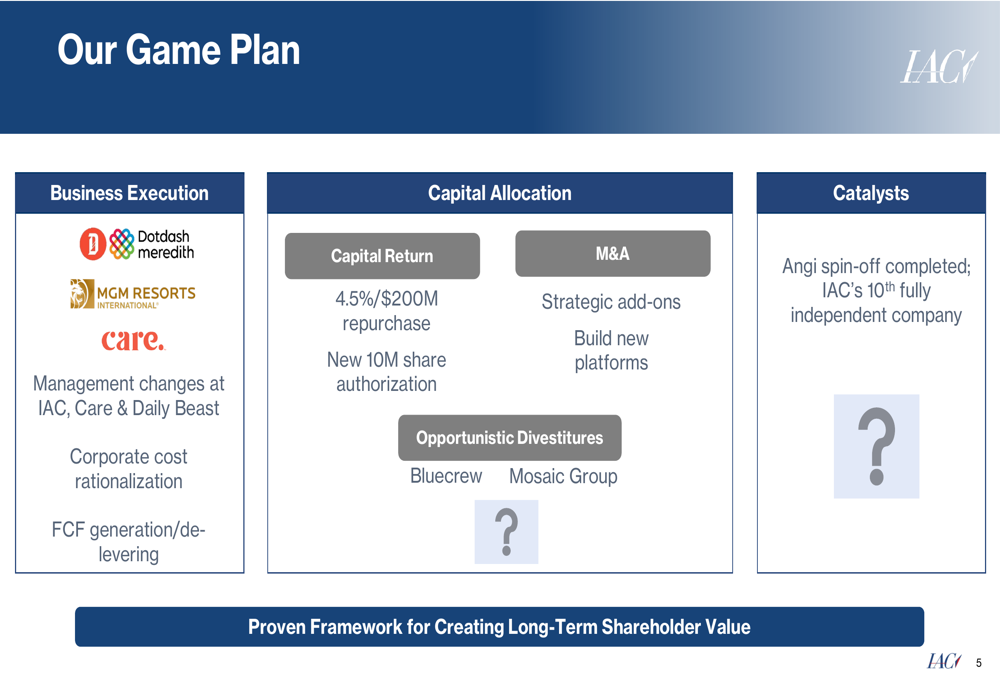

IAC outlined a comprehensive strategic plan focused on three key areas: business execution, capital allocation, and value creation catalysts. The plan includes management changes, cost rationalization, and a focus on free cash flow generation and debt reduction.

The following slide details IAC's strategic roadmap:

The company has authorized a new 10 million share repurchase program, representing significant confidence in its undervalued stock position. Additionally, IAC completed the Angi spin-off, marking its 10th fully independent company.

IAC's M&A philosophy emphasizes its permanent capital advantage and focus on leisure, entertainment, media, travel, and hospitality sectors with sustainable market tailwinds. As IAC founder Barry Diller noted in the presentation: "We are freshened as far as what we are going to do with our capital... there are all sorts of opportunities, whether it's buy, build... We'll do this as we've done it before. Tell us a good idea, and if we think it makes sense, we'll go forward with it."

Forward-Looking Statements

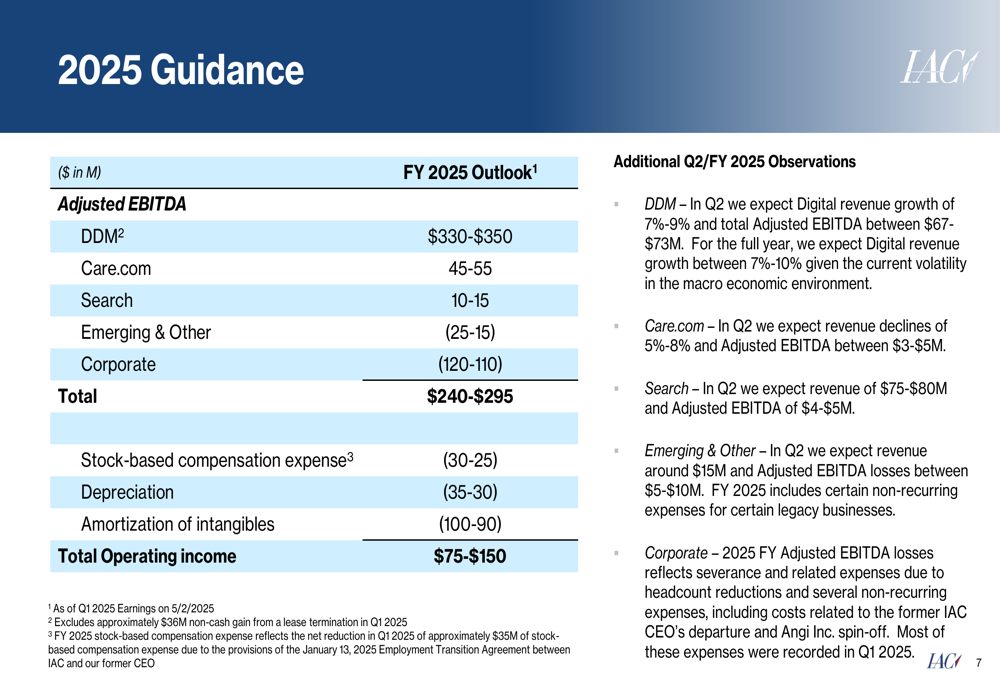

IAC provided full-year 2025 guidance with Adjusted EBITDA projected between $240-295 million. The company later tightened this range to $247-285 million following its Q2 results. Digital revenue growth remains a priority, with the company targeting long-term growth of 10%.

The company's financial outlook for 2025 is detailed in the following slide:

A key strategic focus has been reducing dependency on Google traffic, which the company has successfully decreased from 52% to 28%. CEO Neil Vogel emphasized this strategy during the Q2 earnings call, stating, "We run this business as if Google from search is going to go to zero."

Market Reaction & Analysis

Despite IAC's argument that it trades at a substantial discount to its intrinsic value, the market has remained skeptical. The company presented a compelling case for its undervaluation in the following slide:

According to this analysis, after accounting for IAC's $2.1 billion MGM stake (at $31.97/share) and $0.9 billion in cash, the company's enterprise value calculates to -$0.1 billion, suggesting investors are effectively getting IAC's operating businesses for free.

However, the stock's performance since the presentation suggests ongoing investor concerns about revenue growth and competitive positioning in rapidly evolving digital markets. The 13.41% drop following Q2 earnings indicates that despite positive EPS surprises, revenue shortfalls continue to weigh on investor sentiment.

IAC's strategic initiatives to diversify revenue sources, reduce Google dependency, and optimize its portfolio through potential divestitures (including Bluecrew and Mosaic Group) represent important steps in addressing these challenges. The company's focus on proper compensation for content usage, particularly in the context of AI advancements, also highlights its forward-looking approach to digital publishing challenges.

As IAC continues executing its strategic plan, investors will be watching closely to see if the company can deliver on its promise of unlocking the substantial value it claims exists within its diverse portfolio of digital businesses.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.