China’s Xi speaks with Trump by phone, discusses Taiwan and bilateral ties

Introduction & Market Context

International Business Machines (NYSE:IBM) reported strong second-quarter 2025 results on July 23, exceeding expectations across revenue, profit, and free cash flow metrics. The technology giant demonstrated continued momentum in its strategic focus areas of hybrid cloud and artificial intelligence, with its generative AI book of business now exceeding $7.5 billion.

IBM shares responded positively in after-hours trading, rising 0.68% to $283.88, adding to the stock’s 52-week performance that has seen shares trade between $181.81 and $296.16.

Quarterly Performance Highlights

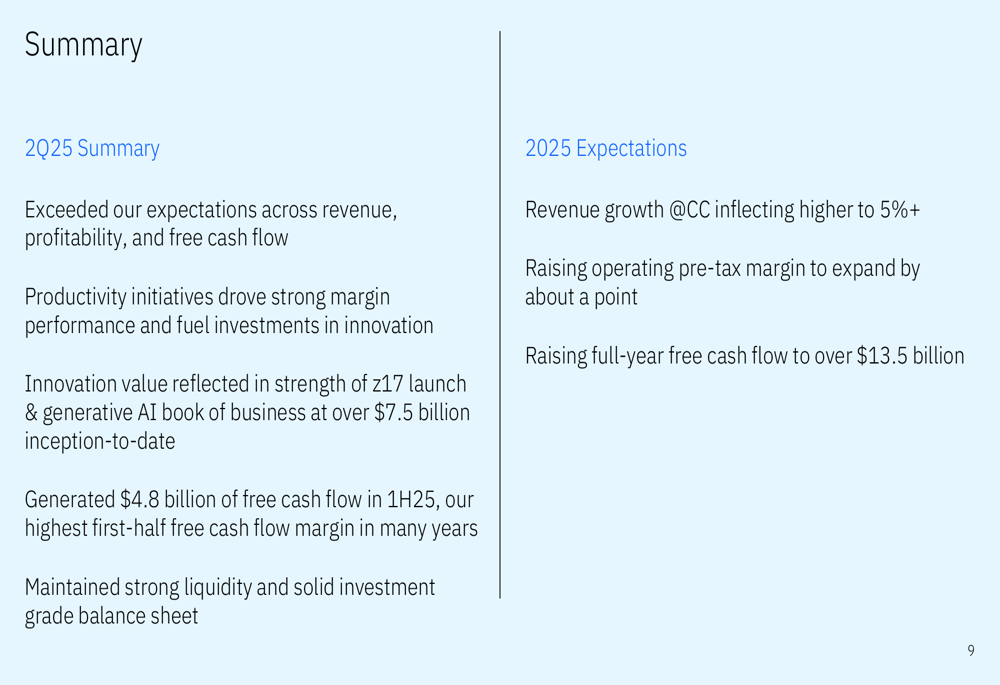

IBM reported revenue of $17.0 billion for the second quarter, representing growth of more than 5% year-over-year. The company generated $2.8 billion in free cash flow for the quarter, contributing to a first-half total of $4.8 billion – which IBM noted was its highest first-half free cash flow margin in many years.

"We exceeded expectations for revenue, profit, and free cash flow in the quarter," said Arvind (NSE:ARVN) Krishna, IBM Chairman, President, and CEO. "Our differentiation through deep innovation and domain expertise is crucial for clients deploying and scaling AI."

As shown in the following financial highlights:

Operating earnings per share grew 15% year-over-year, while adjusted EBITDA increased by 16% with margin expansion of approximately 200 basis points. The company’s pre-tax margin expanded by more than 110 basis points, reflecting IBM’s successful execution of productivity initiatives.

James Kavanaugh, IBM SVP & CFO, emphasized that "innovation is resonating with clients and driving revenue growth and margin expansion."

Segment Analysis

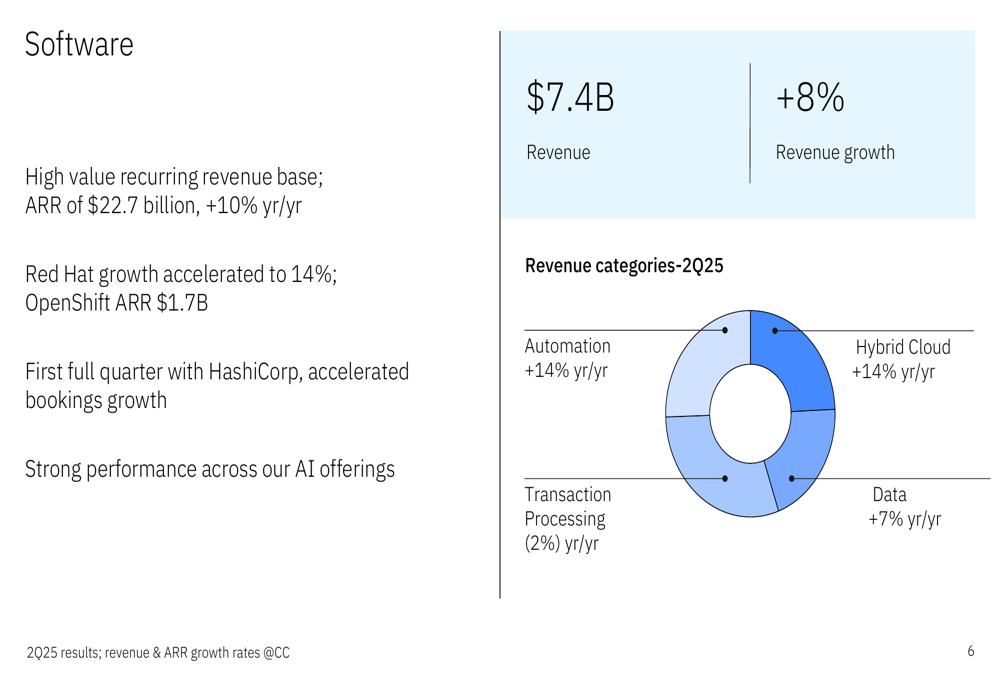

IBM’s Software (ETR:SOWGn) segment delivered revenue of $7.4 billion, up 8% year-over-year, with a high-value recurring revenue base reaching an annual recurring revenue (ARR) of $22.7 billion, up 10% from the previous year. Red Hat growth accelerated to 14%, with OpenShift ARR reaching $1.7 billion. The quarter also marked the first full period with HashiCorp (NASDAQ:HCP) included in results.

The software segment breakdown by category shows:

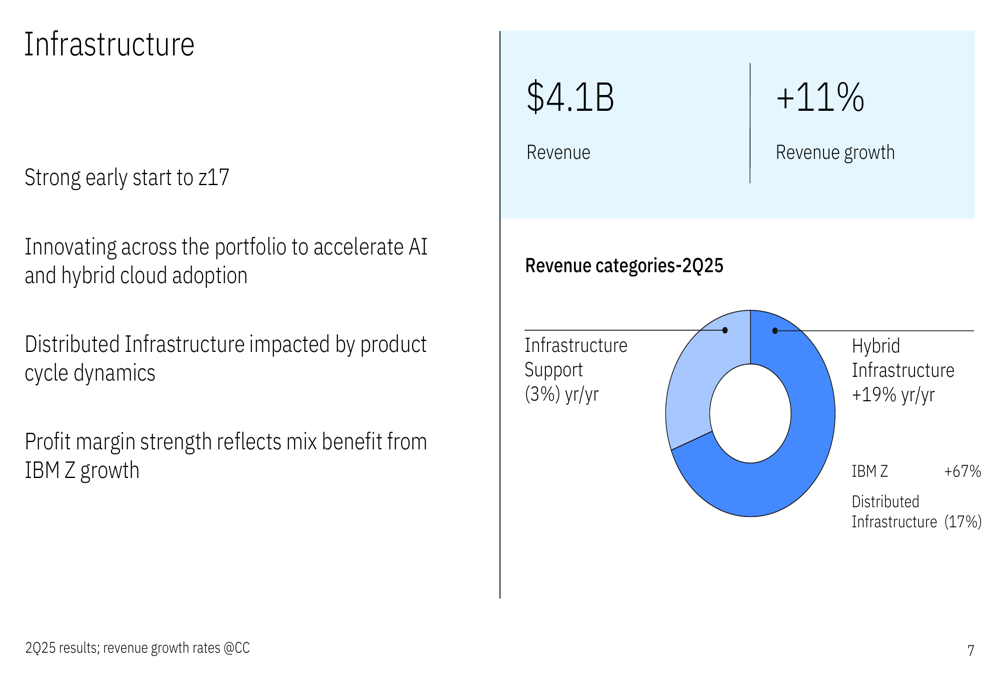

The Infrastructure segment posted strong results with revenue of $4.1 billion, up 11% year-over-year. This performance was driven by a strong early start to the z17 mainframe cycle, with IBM Z revenue increasing by 67%. The segment’s profit margin strength reflected the mix benefit from IBM Z growth.

The infrastructure segment performance is illustrated here:

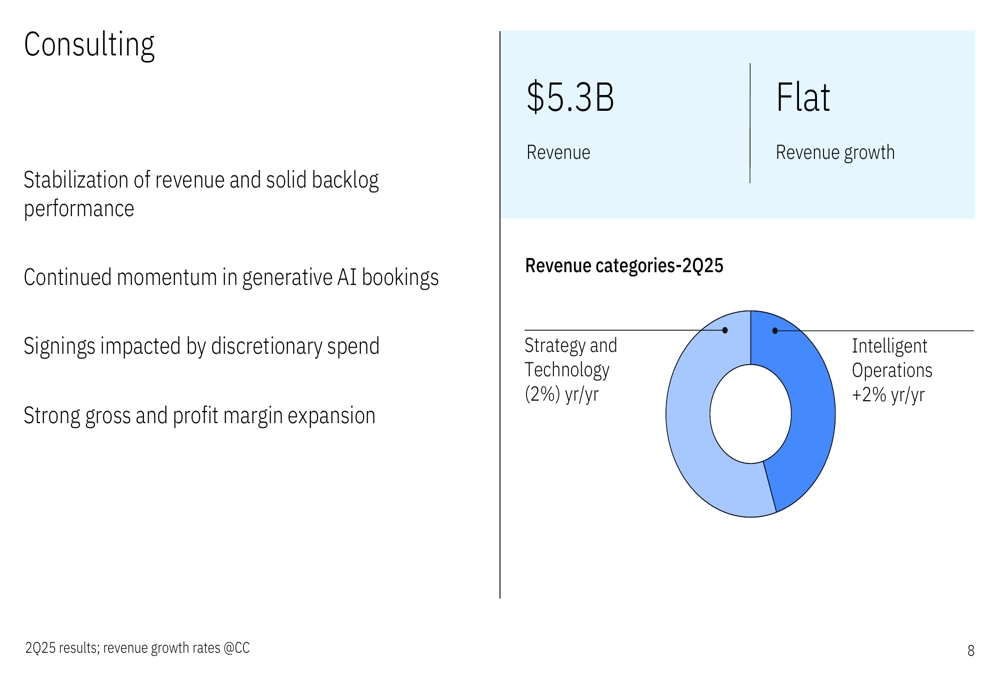

The Consulting segment reported revenue of $5.3 billion, flat year-over-year, but showed signs of stabilization with solid backlog performance. The segment demonstrated continued momentum in generative AI bookings and achieved strong gross and profit margin expansion.

The consulting segment breakdown shows:

Geographically, IBM saw revenue growth of 7% in the Americas, 8% in Europe/Middle East/Africa, while Asia Pacific declined by 3%.

Strategic Initiatives and AI Progress

IBM’s strategic focus on artificial intelligence continues to gain traction, with the company’s generative AI book of business accelerating to over $7.5 billion inception-to-date. This represents significant progress in one of the company’s key growth areas.

The company’s hybrid cloud strategy also showed momentum, particularly through Red Hat’s performance. OpenShift, Red Hat’s container platform, reached $1.7 billion in ARR, underscoring IBM’s strong position in the hybrid cloud market.

IBM’s productivity initiatives have driven strong margin performance while fueling investments in innovation. This balanced approach has enabled the company to expand margins while continuing to invest in strategic growth areas.

Forward-Looking Statements and Guidance

Based on its strong first-half performance, IBM raised its full-year outlook for free cash flow to exceed $13.5 billion, up from previous guidance. The company also expects revenue growth at constant currency to inflect higher to more than 5% for the full year, with operating pre-tax margin expanding by about a point.

The summary of Q2 results and 2025 expectations highlights IBM’s confidence in its outlook:

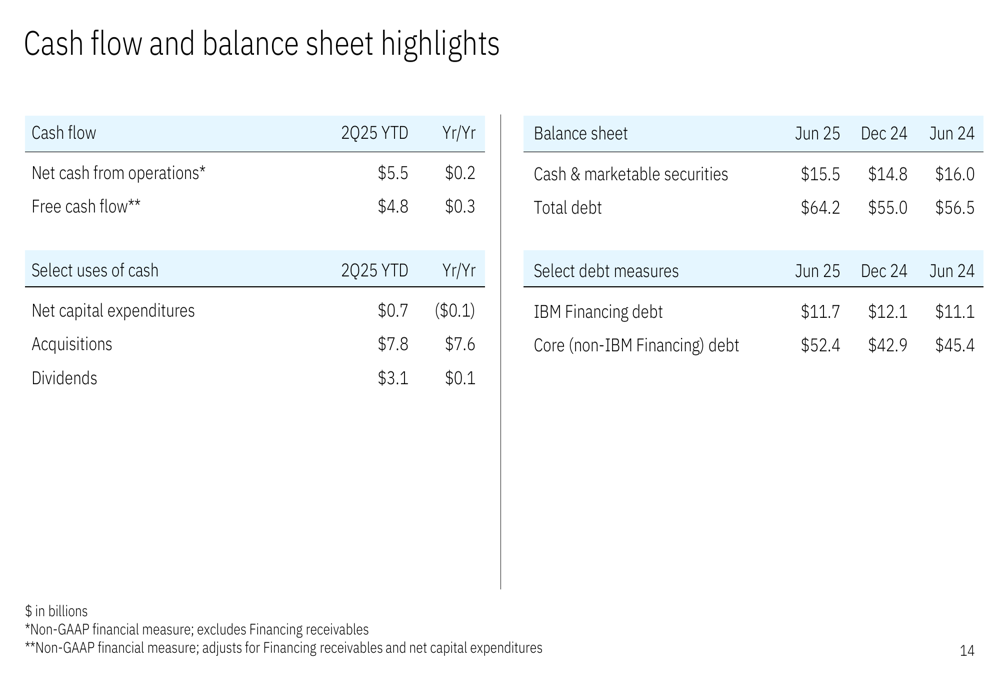

IBM maintained a strong liquidity position and solid investment-grade balance sheet, with cash and marketable securities of $15.5 billion as of June 2025. The company’s total debt stood at $64.2 billion, with core (non-IBM Financing) debt of $52.4 billion.

Cash flow and balance sheet highlights provide additional context:

Conclusion

IBM’s second-quarter 2025 results demonstrate the company’s successful execution of its hybrid cloud and AI strategy. With strong performance across key financial metrics, accelerating momentum in strategic areas like generative AI, and raised full-year guidance, IBM appears well-positioned to continue its growth trajectory.

The company’s ability to expand margins while investing in innovation highlights management’s effective balance between current performance and future growth. As IBM continues to leverage its strengths in the mainframe business while building momentum in software and AI, investors will be watching closely to see if this positive trajectory can be maintained through the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.